WSM - Williams-Sonoma: Environment Remains Difficult

2023-10-06 15:59:58 ET

Summary

- Williams-Sonoma's stock has performed well despite cutting its sales guidance.

- Meanwhile, the company's CEO has sold shares into its recent rally.

- With no signs of the home furnishing market improving soon, I'd be a seller of the stock.

Back in April, I wrote that while Williams-Sonoma's ( WSM ) stock looked cheap, but hitting analyst expectations for 2023 wouldn't be easy. Since then, the stock has performed well, up nearly 30% versus a less than 5% return for the S&P over the same period. Let’s catch up on the name.

Company Profile

As a refresher, WSM is a home furnishings, home décor, and cookware retailer that operates under the Pottery Barn, West Elm, Williams-Sonoma, Pottery Barn Kids, and Pottery Barn Teen banners.

Pottery Barn, which sells furniture and home décor, is WMS’ largest brand, representing over 40% of its 2022 revenue, while its Pottery Barn Kids and Teens brands combined account for about another 12% of sales.

WSM’s second-largest concept, making up over 26% of its 2022 revenue is West Elm, which focuses on modern and contemporary furniture and home décor. Its namesake William Sonoma brand, meanwhile, represented about 15% of its 2022 sales and is more centered on dining and entertaining items.

Q2 and Revised Outlook

In my original write-up, I said that WSM’s 2023 forecast looked too high, and on that front the company did reduce its full-year sales outlook when it reported its Q2 results. However, the sales forecast cut didn’t have the reaction I was anticipating, as the stock rose when the company projected higher operating margins.

For Q2, the company saw sales decline -13% to $1.86 billion, missing the analyst consensus for revenue of $1.96 billion.

Adjusted EPS came in at $3.12, topping analyst estimates by 40 cents.

Gross margins came in at 40.7%, down -280 basis points year over year. However, they did rise 210 basis points from 38.6% in Q1. The company said that gross margins were hurt by capitalized costs from higher product costs and ocean freight.

Overall same-store sales declined -11.9%. Once again WSM’s West Elm brand was the worst performer, with comparable-store sales dropping -20.8%. Overall, West Elm sales declined -20.3% to $484 million. West Elm is the WSM brand that has the most furniture exposure, which is why it has been hit the hardest.

Same-store sales at Pottery Barn, meanwhile, declined -10.6%, and Pottery Barn Kids and Teen SSS fell -9.0%. Total Pottery Barn sales fell -10.6% to $786 million, while Barn Kids and Teen revenue dropped -9.9%. The company said that while furniture demand has been weak, it was seeing relative strength in items such as decorating, frames, pillows, throws and table linens. It also said early Halloween décor sales were off to a good start.,

William Sonoma brand sales, meanwhile, fell -1.6% to $245 million, while its same store sales were lower by -0.7%. The company said its kitchen business was strong, comping positive with strength in high-end electronics, particularly in coffee and espresso machines.

The company ended the quarter with 532 stores at the end of July, 14 less than a year ago, but one more than Q1.

WSM’s burgeoning B2B business, saw sales decline -5% in the quarter. Its contract business, however, was up 23%.

Turning to its balance sheet, merchandise inventories were $1.3 billion, down -16% versus a year ago.

Looking ahead, WSM revised its revenue forecast lower to a decline of -5% to -10% versus a prior range of -3% to +3% growth. It expects its operating margin to be 15-16% versus a prior outlook of 14-15%

Discussing its outlook on its Q2 earnings call , CFO Jeff Howie said:

“On the top line, our updated guidance is based upon the facts and trends we know today by extrapolating our 1-, 2- and 4-year trends in Q2 to full year '23 net revenues. Specifically, our Q2 1-year trend yields full year revenues at the low end of guidance. While our Q2 2-year trend yields full year revenues at the midpoint of guidance, and our Q2 4-year trend yields full year revenues at the high end of guidance. While our top line year-over-year comparison gets easier in the back half, we recognize the challenging environment for home furnishings. On the bottom line, when aligned with historical quarter-over-quarter builds, our strong Q2 operating margin produces full year operating margin within our updated range of 15% to 16%. Additionally, in the back half of the year, our headwinds from the short-term supply chain costs will become tailwinds to support our operating margin guidance. We also expect our full year income tax rate to be approximately 26%. Our 2023 capital allocation plans remain unchanged. We will continue to prioritize funding our business operations. Commensurate with our industry-leading return on invested capital, we will also invest $250 million in capital expenditures in high-return projects to support our long-term growth. … As we look further into the future, we are reiterating our long-term guidance of mid- to high single-digit top line growth with operating margins exceeding 15%. We're confident we'll continue to outperform our peers and deliver profitable growth for these reasons. Our ability to gain market share in the fractured home furnishings industry, the strength of our in-house proprietary design, the competitive advantage of our digital-first but not digital-only channel strategy, the ongoing strength of our growth initiatives and the resiliency of our fortress balance sheet.”

While WSM rallied off its earnings report, rising 11.5% the next session, and showing continued strength into September, the quarter itself and guidance were not great. Revenue missed expectations by about -5%, while the company significantly took down its sales guidance for the year.

On the positive side, the company’s gross margins did improve sequentially, and it raised its operating margin guidance. With ocean freight coming down, and positively impacting many companies earlier than WSM, this improvement shouldn’t be a huge surprise. However, given the promotional environment, WMS has done a good job keeping inventories down and not getting too promotional as well.

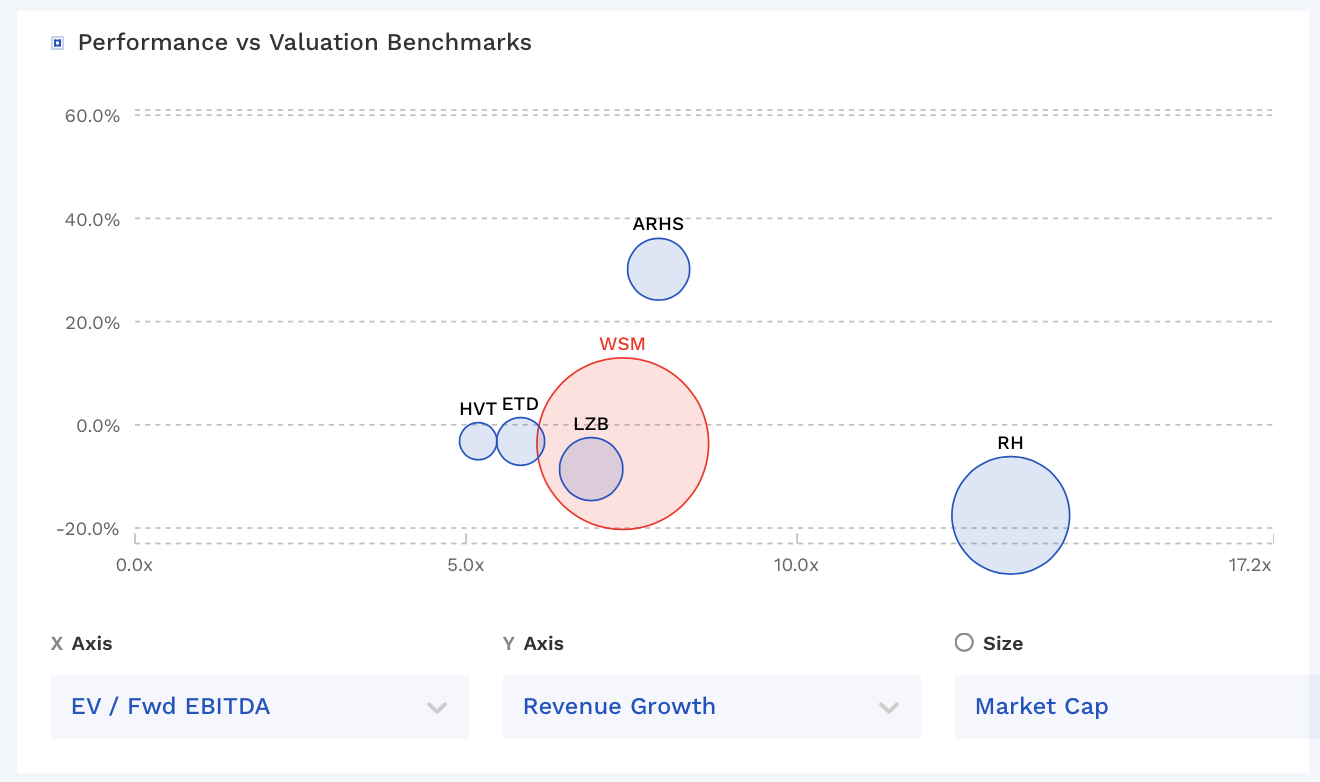

Valuation

WSM's stock currently trades under 7.4x the FY2024 (ending January) consensus EBITDA of $1.44 billion and 7.4x the FY2025 consensus of $1.43 billion.

It trades at a forward P/E of nearly 10.7x the FY24 consensus of $14.08 and just over 10.4x the FY25 consensus of $14.51.

Revenue growth is expected to drop -8.6% this year, and then grow 0.8% next year.

WSM trades at a slightly higher valuation than other furniture companies, outside of RH ( RH ), which I recently wrote-up , and Arhaus ( ARHS ).

{kind=link}

Conclusion

Given the big revenue guidance cut and general trend in the market, it’s surprising that WSM has rallied the way it has on the back of its Q2 results and guidance. While the company is dealing with a difficult home furniture and home décor market, there is nothing that points to a rebound coming anytime soon. The pandemic pulled forward home remodeling and redecorating, and with home sales down, these areas are only expected to continue to slow in the near term.

While its valuation isn’t overly expensive, I still think the current environment will remain difficult. It's also worth noting that WSM's CEO decided to sell $15 million in shares recently, possibly taking advantage of the rally in the stock in my view. As such, I'd follow suite. My “Sell” rating remains unchanged.

For further details see:

Williams-Sonoma: Environment Remains Difficult