WSM - Williams-Sonoma: Examining A Possible Worst-Case Scenario

Summary

- In the wake of economic uncertainty, Williams-Sonoma reported stellar Q2 earnings.

- For the quarter, the company delivered an 11.3% comp on the top line along with 19% earnings growth. This is after very strong comps in 2021.

- Management also reiterated its 2022 guidance and longer-term guidance outlook.

- However, the market is skeptical. Recessionary fears are front of mind and one strong quarter isn’t enough to convince anyone otherwise.

- In addition to looking at current data, I’ll review results from the 2008 recession to understand what a worst case scenario could look like for Williams-Sonoma.

In a recent article , I wrote that Williams-Sonoma, Inc. ( WSM ) is well equipped for an economic downturn. So far that is proving to be true. While other home furnishing businesses have missed earnings expectations and lowered guidance, Williams-Sonoma beat expectations and reiterated 2022 and long-term outlook guidance in the Q2 report.

I was keeping an eye on the stock’s price action after the Q2 report was released. Immediately after it came out, the stock price went up as much as 7% but soon went into negative territory by the end of after-hours trading. The next day it ended slightly up after volatile trading where it spent most of the day down. This seems to reflect immediate relief given the beat and guidance update but general pessimism for the economy and consumer discretionary businesses in general. This pessimism was very apparent after the hawkish update from Jerome Powell at Jackson Hole. That day consumer discretionary stocks were down big; in the home furnishings industry specifically Restoration Hardware ( RH ) was down 9%, Wayfair ( W ) was down 7% and Williams-Sonoma was also down 7%.

This pessimism overrode the positive report from Williams-Sonoma and the upbeat commentary from management. It may seem unwarranted but it’s not for bad reason. I still think Williams-Sonoma will hold up relatively well in an economic downturn when compared to its industry peers but it will surely suffer in the case of a major recession. I don’t think we will see a major recession like that in 2008 but I went back and looked at results from that period to familiarize myself with a worst case scenario. I will review those results in more detail below but even though business slowed significantly, the company managed the situation well.

All of this to say, I am reiterating my buy rating for WSM. However I’m doing so while trying to strike a balance between acknowledging the positive report, and being aware of the acute risks that will come with a major recession.

My Take on the Global Macro Environment

I’m including this section to provide some context on my perspective and how that is factoring into my investing thoughts.

I personally find it hard not to be bearish. I think that inflation is more of a structural issue and that the fed funds rates will likely be elevated for a long period of time. Even if inflation eases greatly over the next few months, I think any sort of pause or pivot from the Fed will send inflation up again. Couple this with a questionable global energy situation and a seemingly higher likelihood of tail end geopolitical risks, and there’s not much to be optimistic about.

But I also see more fiscal stimulus on the horizon like we recently got with the cancellation of some student loans. This could help juice corporate earnings but could potentially lead to more inflation thus increasing the need for higher interest rates to squash demand further, as the structural causes of the current inflation will likely not be resolved.

The thing that makes me most optimistic is that just about everyone on Twitter thinks this too (I’m basically regurgitating the takes that make the most sense to me) and the future has a funny way of unfolding in unexpected ways. I try not to let these beliefs influence my investments in a direct way but I have reduced my exposure to consumer discretionary stocks. I do however still hold shares of Williams-Sonoma.

On to the Positives

While the global economic outlook seems gloomy, Williams-Sonoma is holding up well. Some of the Q2 highlights include comparable brand revenue of 11.3% with especially strong comps from Pottery Barn, operating income up 13% year over year and earnings per share up 20% from the prior year. These results paint a picture of a resilient consumer and increased operational efficiency.

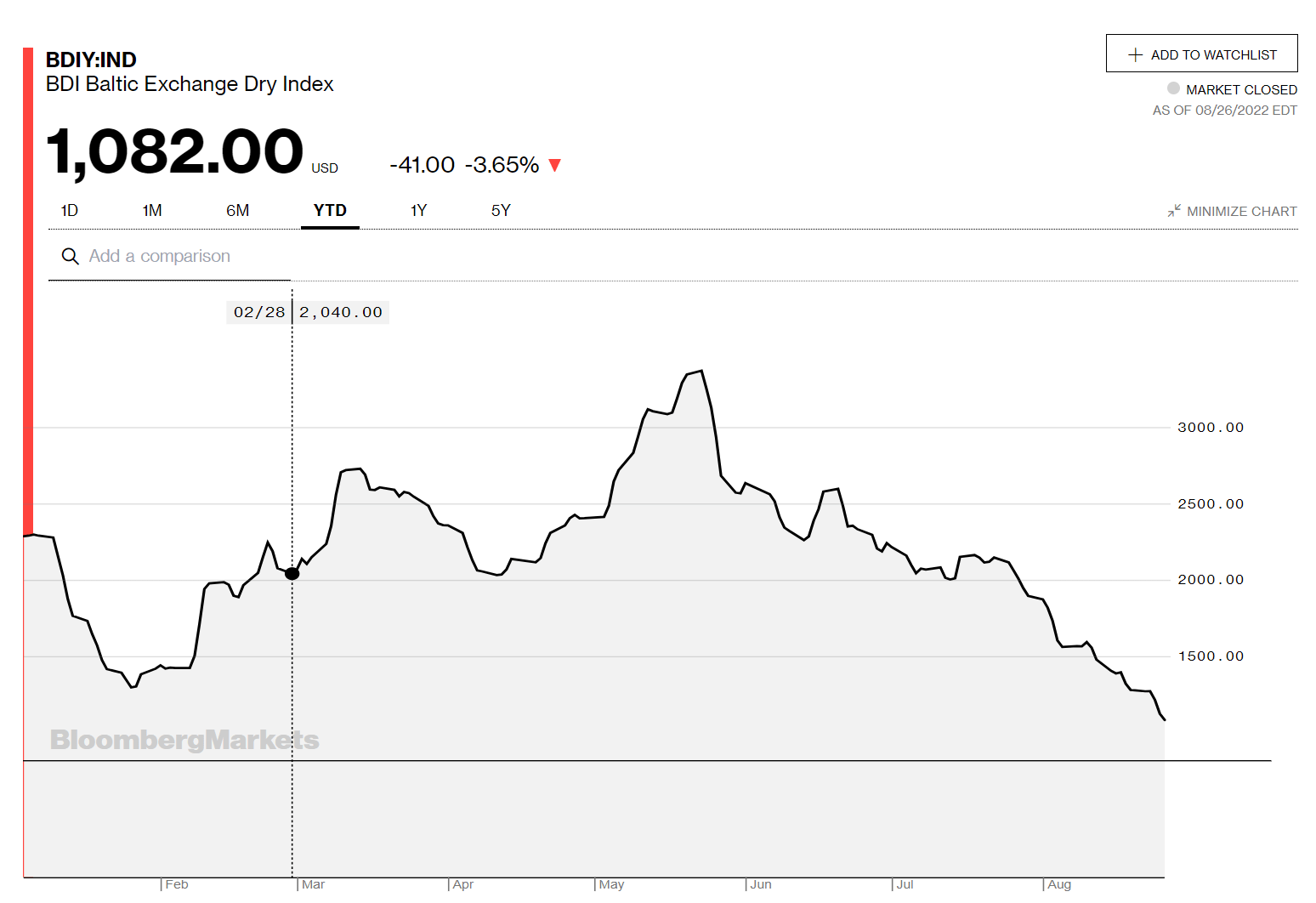

Along with these results, management reiterated 2022 and longer term outlook guidance while providing very upbeat commentary on the conference call. They highlighted many aspects of the B2B segment, market share gains amongst millennials and gen z, and growing comps through the start of Q3. The one area of caution they noted was in regards to freight costs but ocean freight costs have dropped dramatically from their peaks in Q2. If demand continues to hold up while these freight costs drop, the operating margin guidance should be achievable.

Baltic Exchange Dry Index (Bloomberg)

{kind=link}

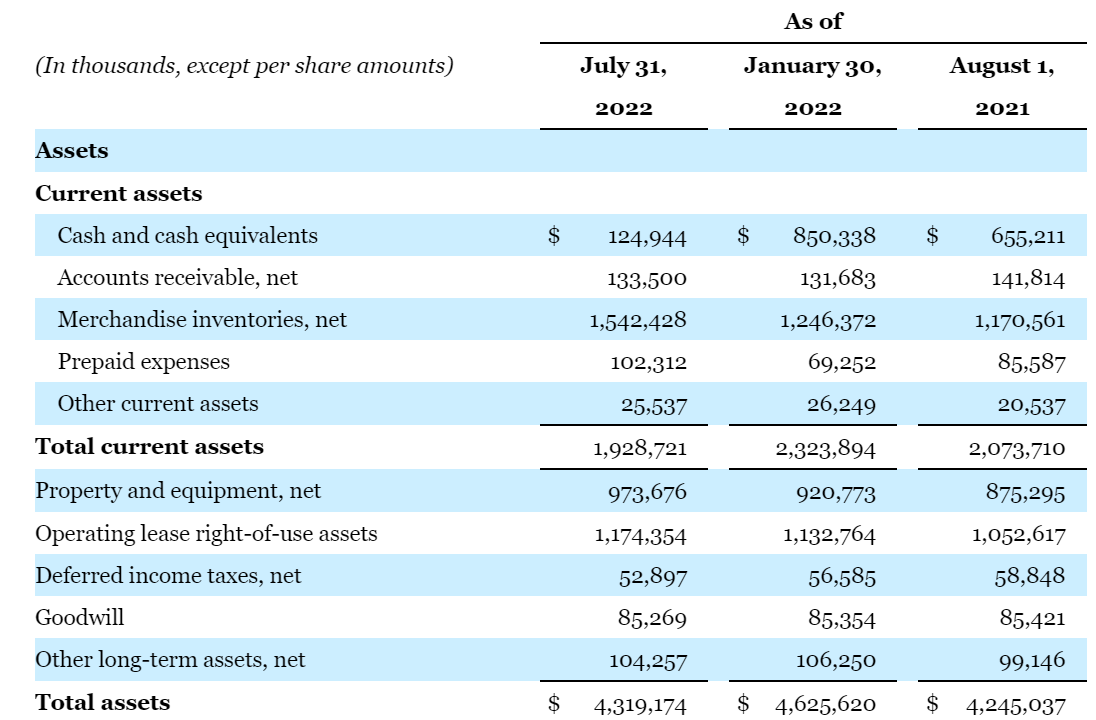

Regarding capital allocation, the company has drawn down its cash balance massively to repurchase shares. About $700 million was used to repurchase shares since the start of the year and their cash balance is also down about $700 million to $125 million.

Williams-Sonoma Balance Sheet ( Williams-Sonoma Q2 2022 Earnings Release) Cash Flows from Financing Activities ( Williams-Sonoma Q2 2022 Earnings Release)

{kind=link}

{kind=link}

This signals huge confidence from management in their business prospects and longer term guidance. Both Laura Alber and Julie Whalen said as much on the conference call while firmly indicating that they think the stock is underpriced and that they will continue to repurchase shares. I don’t think they would make a decision to drawdown cash reserves in the face of a recession unless they had the utmost confidence in the business going forward, considering they have experience navigating the 2008 financial crisis.

Speaking of the financial crisis…

A Look Back to 2008

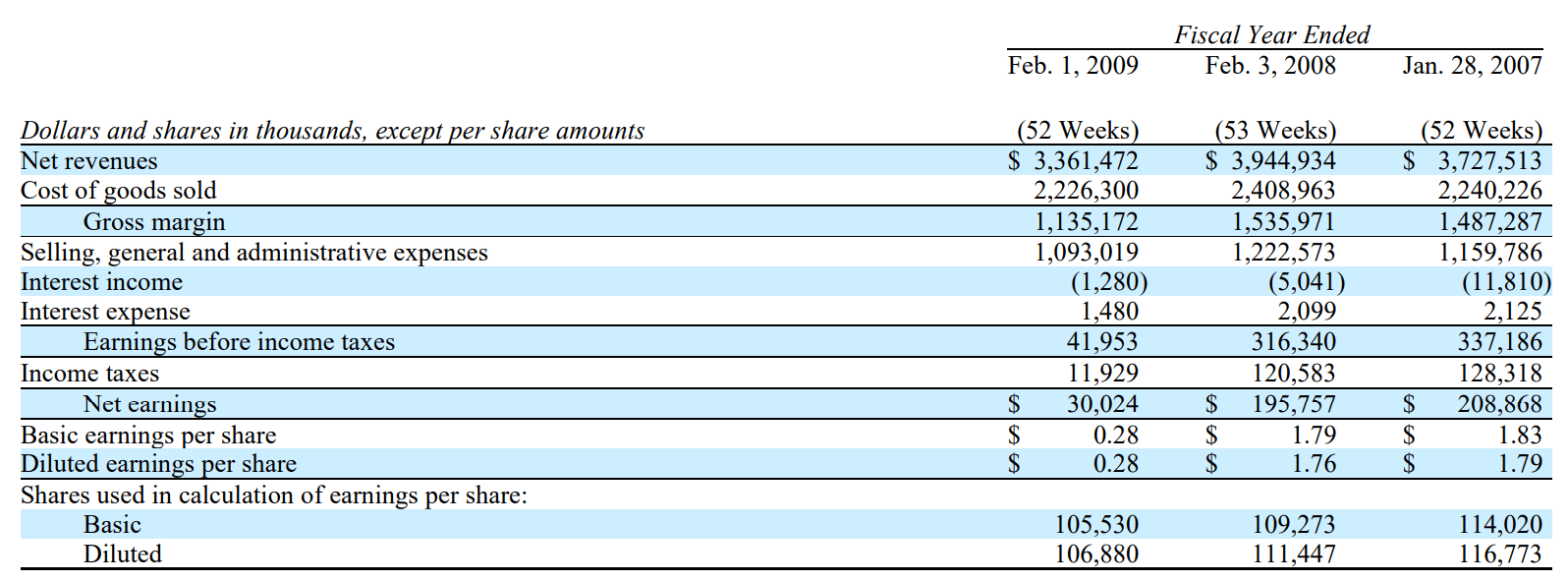

In order to understand what a worst case scenario would look like for Williams-Sonoma, I looked back to the 2008 annual report. The great recession was a housing led recession with job losses and forced selling of homes. This meant that home furnishing companies were rocked. Williams-Sonoma was no exception; sales fell 20% and EBIT fell almost 90%.

Williams-Sonoma FY 2008 Income Statement (2008 Annual Report)

{kind=link}

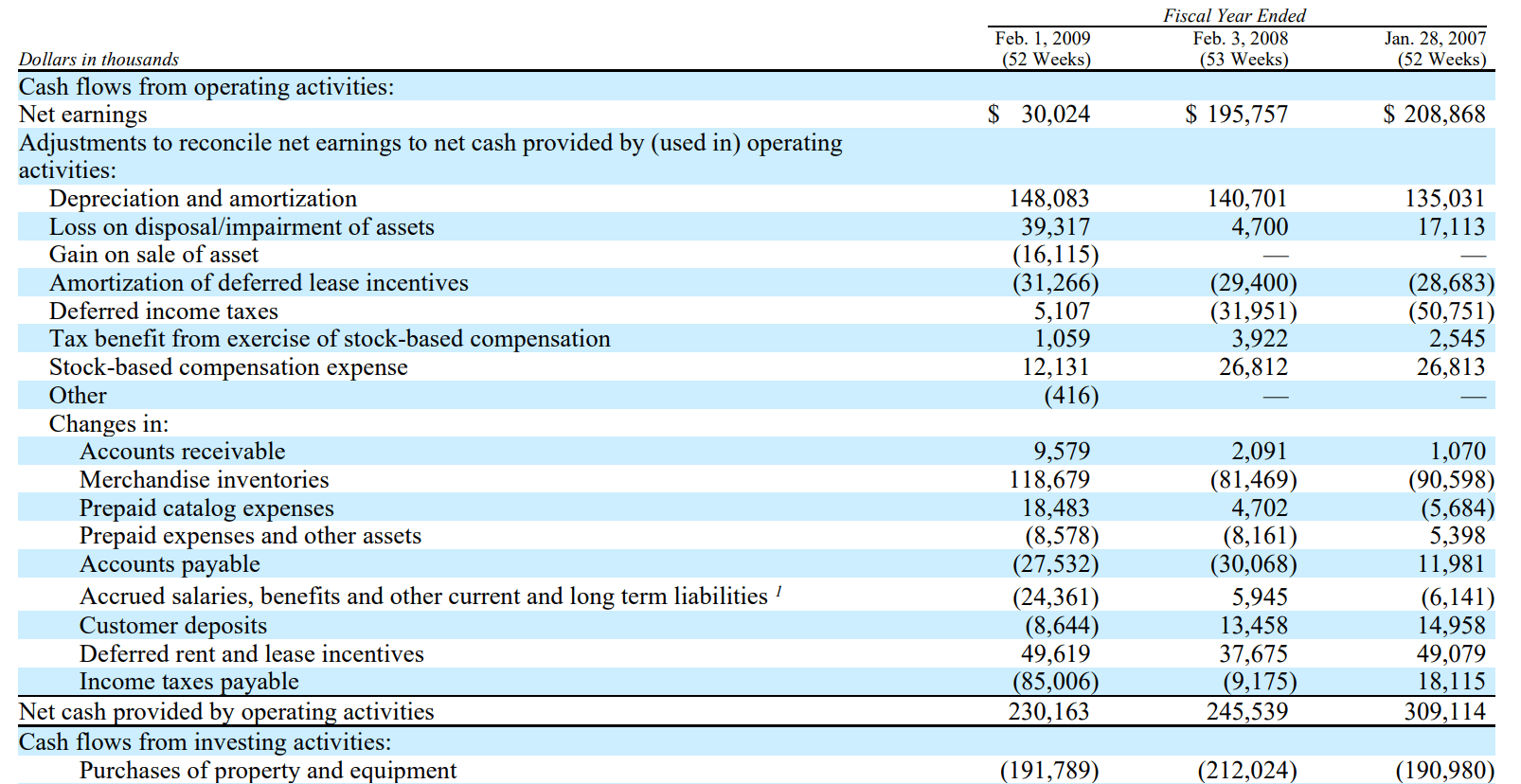

What’s interesting is that cash flow stayed very consistent despite the drop off in earnings due to good management of inventories. This allowed them to stay basically debt free and to maintain the dividend. This was extremely impressive for a retailer that has such a direct link to the housing market.

Williams-Sonoma FY 2008 Cash Flow Statement (2008 Annual Report)

{kind=link}

I don’t expect anything close to a recession like that from 2008 to happen anytime soon but as a shareholder it’s comforting that the current management team has experience dealing with a situation like that. Add to this the higher margins of the business today, a more diverse customer base with the B2B segment, and falling input costs when compared to earlier this year, and there are reasons to have confidence in the face of a recession.

As a note, the consistent cash flow in 2008 didn’t help the stock price (it dropped about 80% from its peak in 2008) but it removed existential business risk from the equation.

Final Thoughts

Strong earnings, reiterated long-term guidance and upbeat commentary from management in the Williams-Sonoma Q2 earnings release directly contradicts the mood of market participants as recessionary fears are front of mind. I’m not immune to these fears but knowing that the company was able to maintain strong cash flow during the 2008 recession makes owning shares easier for me. Again, I don’t expect a recession similar to 2008 but it’s good to know that even if that worst case scenario did occur, the company will likely maintain its dividend and won’t have to take on loads of debt for survival purposes.

For further details see:

Williams-Sonoma: Examining A Possible Worst-Case Scenario