WSM - Williams-Sonoma: Hitting 2023 Forecasts Looks Tough

2023-04-26 12:22:54 ET

Summary

- WSM's stock is cheap if it can hit numbers, but it is facing a number of industry headwinds.

- While the BBBY liquidation could help longer term, it will likely be a negative in the short term.

- I'd wait for a revision to numbers before considering the stock.

Williams-Sonoma ( WSM ) stock looks cheap, but hitting analyst expectations won't be easy.

Company Profile

WSM is a home furnishings, décor, and cookware retailer. The company operates several concepts including Pottery Barn, West Elm, Williams-Sonoma, Pottery Barn Kids, and Pottery Barn Teen.

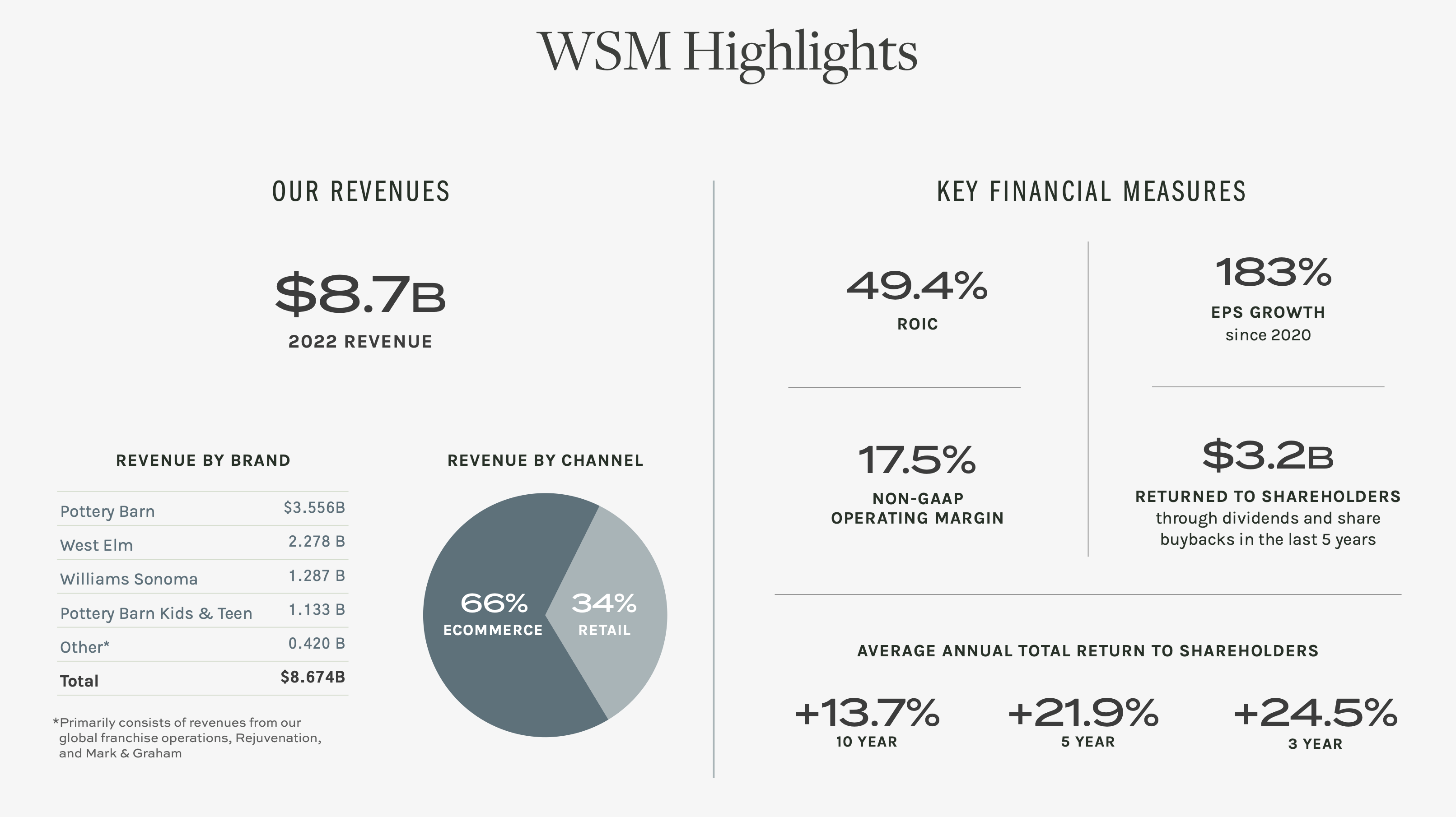

WSM's largest concept is Pottery Barn, which accounted for about 41% of its 2022 revenue. The brand sells things such as furniture, bedding, rugs, lighting, and decorative accessories. Its Pottery Barn Kids and Teens brands combined represent over 12% of WSM's revenue and feature furniture, bedding, and accessories aimed toward their respective age groups.

West Elm is its second-largest concept, making up over 26% of its 2022 sales. The brand focuses on modern and contemporary furniture and home décor, as well as kitchen and cookware. Its namesake William Sonoma brand, meanwhile, accounted for about 15% of its 2022 sales. The brand is focused on dining and entertaining, and sells things such as cookware, tools, electrics, cutlery, tabletop and bar, outdoor, furniture, and cookbooks.

{kind=link}

WSM also owns a few smaller brands such as Rejuvenation, Mark and Graham, and Outward. Rejuvenation designs and makes made-to-order lighting, hardware, and furniture, while Mark and Graham is a monogrammed brand that offers personalized products and custom gifts. Outward, meanwhile, is a 3-D imaging and augmented reality platform for the home furnishings and décor industry.

Opportunities and Risks

One of the big opportunities that WSM is going after is expanding into the business-to-business (B2B) market, which the company thinks is underserved. This hospitality industry, which includes hotels, restaurants, resorts, and country clubs, is one area the company is looking to serve. However, it is also looking to serve the education, healthcare, retail, cruise, government, and commercial markets as well. It sees this as an $80 billion addressable market.

So far, this plan has been working, with the company posting nearly $1 billion in B2B revenue in 2022, up 27% year over year. The company said it has a strong backlog of projects on the commercial side that it's won.

Discussing its B2B opportunity of its Q4 earnings call , CFO Jeff Howie said:

"B2B is one of our most exciting growth initiatives, as you know, and we finished this year just shy of $1 billion, growing 27% in the 1 year and 166% on a 2-year. In terms of where we see next year, it should continue to be accretive to our comps, probably in the neighborhood of about 100 basis points to our comps in '23. There's some really exciting things going on in B2B. And as you know, we're not always at liberty to talk about our clients. But in Q4, we saw some notable wins we can talk about. In office space, we outfitted Carl's Jr.'s corporate office. And unfortunately, there was no free food, that was not part of the deal. We also outfitted Google's midpoint office. In stadium space, we furnished the Golden Guardians' esports facility in Los Angeles. And in the hotel space, we saw a large number of hotel projects complete with Marriott SpringHill.

"Now one thing to remember with B2B is there's 2 customer groups, trade and contract. While trade is more volume, contract is a source of growth. Trade maybe more sense of the B2C trends, but contract continues to drive the growth in B2B. We're not seeing a slowdown in the commercial side as there's a backlog of projects coming out of the pandemic, and we have a steady pipeline of RFPs we've gone out of. In fact, Q4 was the largest quarter of contract to date. The key point here is B2B continues to be a winning strategy for us, and we continue to capture market share in the $80 billion fragmented B2B market. It leverages our portfolio of brands, in-house design and global sourcing capabilities and our digital first but not digital-only strategy means that we can service the B2B customer in multiple ways."

In addition to B2B, WSM is also looking to expand internationally. It entered the Indian market through a partnership with Reliance Group and has three stores and websites in the country. It also relaunched its website in Canada.

The company is also looking to grow its newer brands Rejuvenation and Mark and Graham, which combined accounted for nearly $270 million in revenue in 2022. It said it is expanding into the remodel category with Rejuvenation, offering things such as vanities, cabinet hardware, and custom wall lighting. With Mark and Graham, meanwhile, it is focusing on the travel space with monogrammed luggage and accessories.

The retailer could also be a beneficiary of the recent bankruptcy announcement from Bed Bath & Beyond ( BBBY ). Its brands tend to be a little more high-end than BBBY, but its namesake brand and Pottery Barn could take some share after BBBY winds down. Before that happens, though, BBBY liquidation sales could negatively impact WSM's sales during a period of heavy discounts.

WSM has also been aggressive on the capital allocation side of the business. In March, it announced a new $1 billion stock repurchase plan. It also raised its quarterly dividend by 15% to 90 cents a share. The stock currently yields about 3%. These are sometime shareholder-friendly moves.

When looking at risks, the macro environment is the biggest one. Thus far, the company's sales have held up pretty well, with Pottery Barn comps up 5.8% in Q4 and PB Kids & Teens up 4.0%. The lower-end West Elm didn't fare as well, with same-store sales plunging -10.7%, while Williams Sonoma SSS fell -2.5%. Nonetheless, in a poor home furnishing market, those results are very solid. However, we'll have to see if they can hold up, and that will largely depend on if we get a recession and how bad it is if we do get one. WSM posted -17.2% comps back in 2008, and while this isn't likely going to be similar to 2008, it does show that things can get bad.

Gross margin is another area to watch. WSM has had very strong gross margins of over 42% the past two years compared to the typical 36-39% it's historically posted. The home furnishings environment has been very promotional recently, and the BBBY liquidation isn't going to help in the near term. That could pressure both sales and gross margins at the company.

Valuation

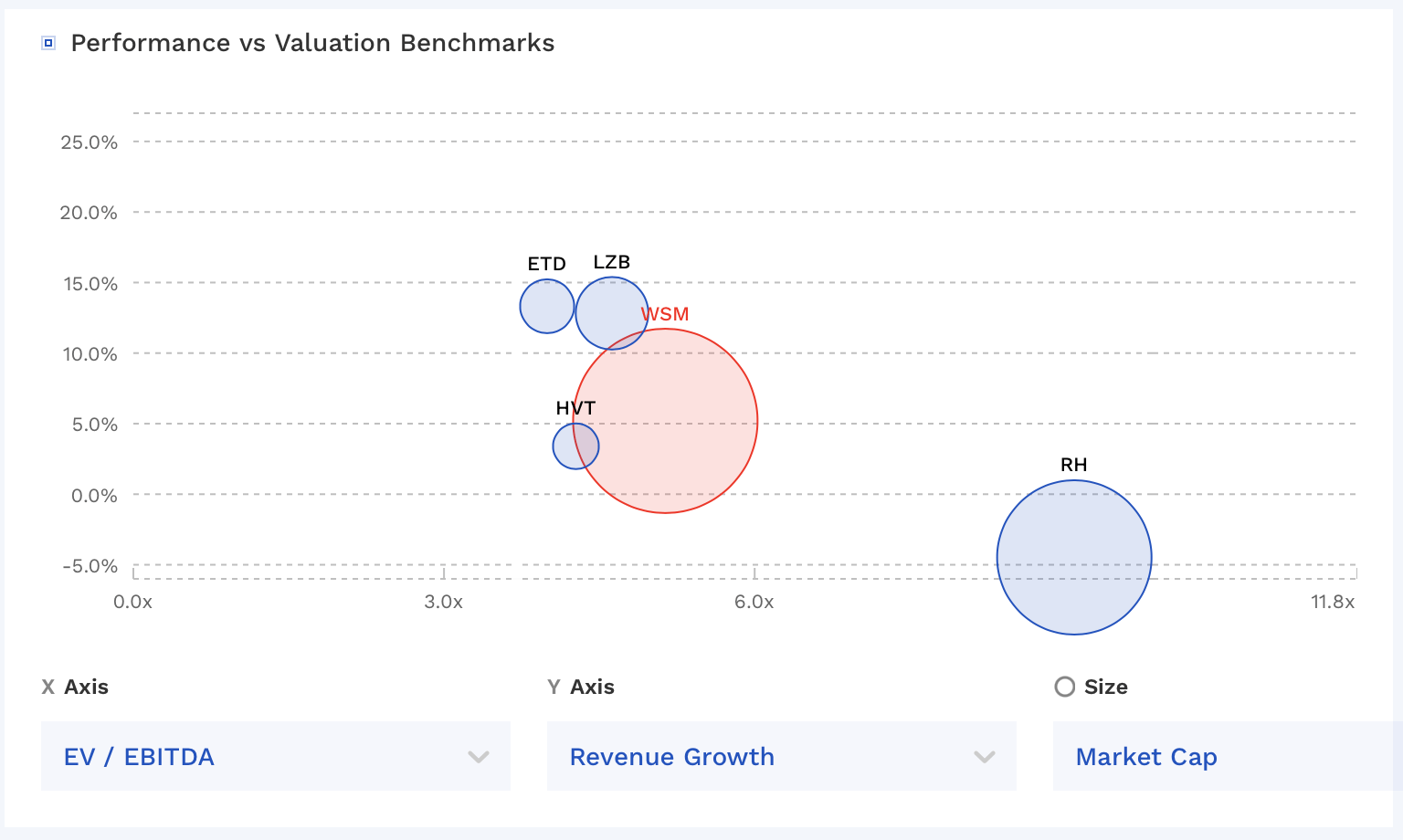

WSM's stock currently trades under 6.3x the FY2024 (ending January) consensus EBITDA of $1.42 billion and 6.2x the FY2025 consensus of $1.43 billion.

It trades at a forward P/E of nearly 8.7x the FY24 consensus of $13.63 and just over 8.4x the FY25 consensus of $14.24.

Revenue growth is expected to drop -3.2% this year, and then grow 2% next year.

Outside of RH ( RH ), which I recently wrote-up , WSM trades at a slightly higher valuation than other furniture companies.

{kind=link}

Conclusion

WSM has been doing well in a tough macro environment. At the same time, the stock is pretty inexpensive if it can hit its numbers. However, its 2023 outlook doesn't seem particularly conservative in my view.

The home furnishing category got a bit of a push coming out of the pandemic, and the category typically doesn't do well doing periods of economic weakness as it is typically one of the first places people pull back. That, along with liquidating BBBY, doesn't seem to bode well for the company in the near term.

Given that I think its numbers are likely too high for this year, I'm going to stay away from the name at this time. Longer term, I like the direction the company is moving with its push into the B2B space and would revisit the stock at a later time.

For further details see:

Williams-Sonoma: Hitting 2023 Forecasts Looks Tough