COST - Williams-Sonoma: India B2B And Brand Extensions Are This Decade's Growth Drivers

2023-03-22 18:59:58 ET

Summary

- We read through Williams-Sonoma's latest earnings call and learned about some exciting growth initiatives the company is executing.

- Global Expansion in India, Celebrity Collaborations, Business-to-Business Opportunities, New Brand Extensions, and Emerging Brand segments will be WSM's growth engine for this coming decade.

- The stock also sports very strong fundamentals, low valuations, and dividend growth, all adding to its appeal.

- We conduct a deep dive into Williams-Sonoma's growth initiatives as well as assess risks with a potential economic downturn, and advise readers on our approach to investing in the stock.

Investment Thesis

Williams-Sonoma ( WSM ) recently announced Q4 results and we read through the company's earnings call transcript . In addition to the company's prepared remarks and question and answer session, we also pored over their investor presentation that was released the following day.

There was a ton of material to parse through and unpack, but after we combed through it all, we came away quite impressed and rather bullish on the stock. However, we had to apply our mental brakes because a consumer cyclical company is a potentially counterintuitive investment in the current environment. With consumer sentiment trending down over the last few years, uncertainty in the banking sector, and fears of a recession looming, you'd likely want to steer clear of any company in the discretionary space.

The market tends to agree, with WSM shares down roughly 40% from their 2021 high in the midst of the pandemic. However, we think shares are trading at attractive levels. And after looking at the company in further detail, we believe there are a multitude of positive factors in the company's favor that should offset concerns around a downturn, and even help the company to thrive and take market share if a downturn were to come.

We think investors with a long-term horizon, and a penchant for dividend growth, will find a solid investment opportunity in Williams-Sonoma.

Growth Catalysts

Williams-Sonoma is a specialty retailer focusing on home goods such as home d é cor, furniture, kitchenware items, bedding, and just about every other item you can think of that would furnish every room of a home - rugs, curtains, faucets, pillows, small kitchen appliances, outdoor patio accessories. The list is endless. They operate several brands including namesake Williams-Sonoma, but also the popular Pottery Barn, as well as Pottery Barn Kids, Pottery Barn Teen, and West Elm.

What truly separates Williams Sonoma from the pack of other specialty retailers is their in-house design and relentless focus on ecommerce, which represents a full 2/3 of revenue. There's been a handful of articles written on Williams-Sonoma so we won't rehash every detail about the company's background history and where's its been. For that, we'd like to point you to The Pineapple Investor's article on Williams-Sonoma that does a terrific job taking you through the company's background.

Instead, in this article, we'd like to focus on where the company is going and how it's planning to get there. We've identified a number of catalysts that are poised to accelerate the company's growth prospects.

Growth Initiatives (Williams Sonoma Investor Presentation, March 2023)

{kind=link}

Let's get started!

India

Believe it or not, Williams-Sonoma is no stranger to the global stage. The company opened their first international store in Canada over 20 years ago, and has since expanded to Australia, the U.K., the Middle East, Australia, the Philippines, and Mexico. The company's operating model is to partner with a local retail franchise operator with a native knowledge of the local retail landscape. Williams-Sonoma is taking this approach once again, by partnering with Reliance Industries, and expanding their footprint in India.

Williams-Sonoma debuted their ecommerce sites and physical Pottery Barn and West Elm flagship stores in Delhi, India last Fall, and CEO Laura Alber has stated that she has plans for further expansion in the country. Plans are to expand into additional cities across India, as well as debut other brands such as Pottery Barn Kids.

Pottery Barn store in India (Architectural Digest, photo by Ashish Sahi)

{kind=link}

Alright, so why does this excite us? First, we like that Williams-Sonoma partnered with Reliance Industries. Reliance has a massive retail division which is the largest in India sporting a network of retail outlets across the country. They have successfully helped a number of high profile brands expand their presence in India including Armani Exchange, Burberry, Ermenegildo Zegna, Marks and Spencer, Brooks Brothers, Steve Madden, and quite a few others. They operate over 12,000 stores across 7,000 cities, so Williams-Sonoma is able to tap into that network to quickly scale up their presence in the country.

Second, we like India from a demographic standpoint. We think that Williams-Sonoma will find a successful niche in the country that will contribute to the company's growth in the coming years. India's middle class continues to grow at a torrid pace. The share of the middle class more than doubled from 14% in 2005 to 31% in 2021, and is projected to double again, to 63% by 2047.

So there is an irrefutable secular trend that will see the average Indian gain more wealth in their lifetime, leading to higher consumption of goods and by extension, pursuit of status and lifestyle expression. Supporting, and perhaps accelerating this trend, is the redirection of investment away from China into other Asian markets, including India. As part of its pivot away from China, Apple (AAPL) supplier Foxconn announced they will build a 300-acre factory in India leading to job growth and investment in that country that should set an example for other companies to follow suit.

Another demographic element in Williams-Sonoma's favor is the average age in India is only 28 years old, compared to 39 in the United States. Taking into account the size of India population (over 4x that of the U.S.) and the fact that the vast majority of this population is about to enter their 30's, as well as experience a relative increase in earnings potential, we are seeing a confluence of factors that should provide a strong tailwind for any company looking to capture a fraction of the Indian market.

Williams-Sonoma is using their blue print of chef and designer collaborations they've done in the United States, and is leveraging that for the Indian audience. Late last year, the company announced a partnership with Indian actress Deepika Padukone. Deepika signed on to be a brand ambassador to promote Pottery Barn's international expansion and will co-create a collection with the company.

All signs point to continued success in the company's global expansion strategy and this is only one of several growth catalysts they have in store.

Hotels, Stadiums, and Offices: Growth in B2B

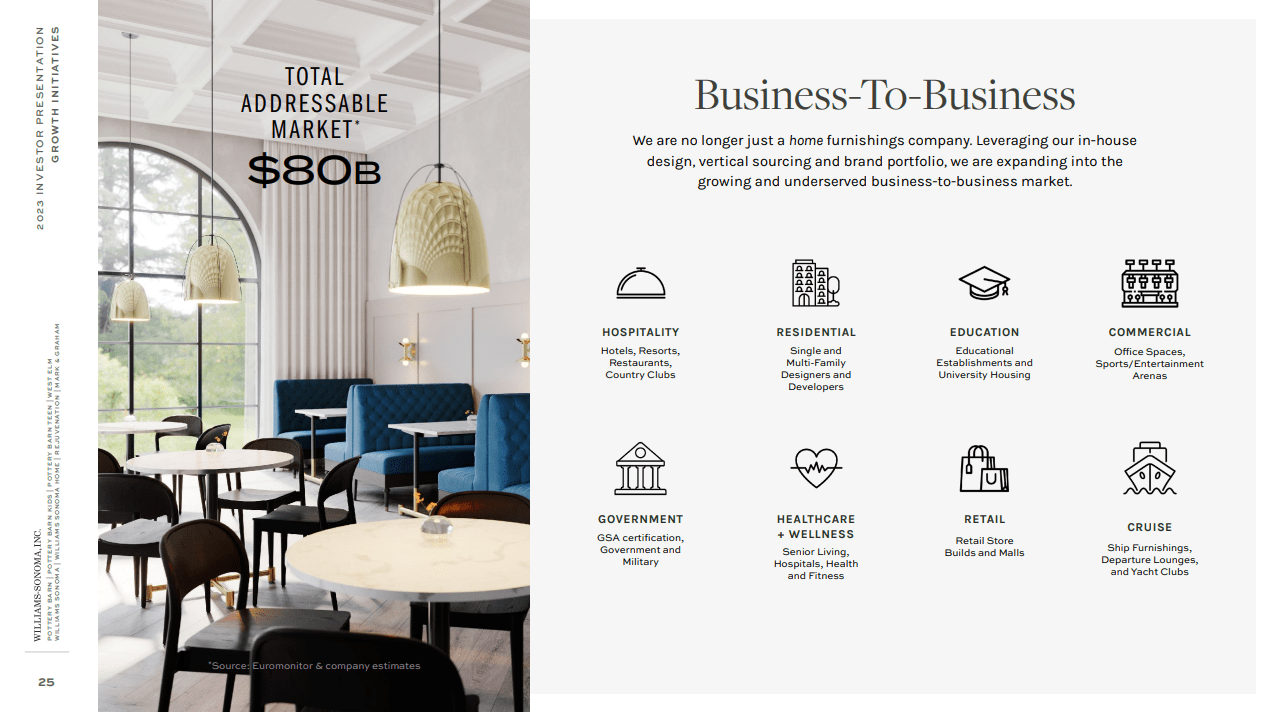

Perhaps one of the most exciting growth drivers at Williams-Sonoma is their pursuit in the business-to-business space. They have long been known as a furnisher for your home, however they have keenly realized that they can expand beyond residential space, and penetrate the $80 billion business-to-business market. Taken from their investor presentation, they state: "We are no longer just a home furnishings company. Leveraging our in-house design, vertical sourcing and brand portfolio, we are expanding into the growing and underserved business-to-business market."

Below are the various B2B customer end markets where Williams-Sonoma believes they can successfully penetrate including hotels, resorts, apartments, universities, offices, stadiums, offices, and cruise lines - just to name a few.

Williams Sonoma B2B Initiative (Williams Sonoma Investor Presentation, March 2023)

{kind=link}

During the Q4 earnings call, CFO Jeff Howie made the following statement about the inroads the company is making in B2B:

B2B is one of our most exciting growth initiatives, as you know, and we finished this year just shy of $1 billion, growing 27% in a one year and 166% on a two-year. In terms of where we see next year, it should continue to be accretive to our comps, probably in the neighborhood of about 100 basis points to our comps in '23. There's some really exciting things going on in B2B.

And as you know, we're not always at liberty to talk about our clients. But in Q4, we saw some notable wins we can talk about. In office space, we outfitted Carl's Jr.'s corporate office. And unfortunately, there was no free food, was not part of the deal. We also outfitted Google's Midpoint office. In stadium space, we furnished the Golden Guardians e-sports facility in Los Angeles. And in the hotel space, we saw a large number of hotel projects complete with Marriott SpringHill.

The growth rates that Howie highlights are pretty incredible. Revenue growth of 27% year over year is five times the overall growth rate that Williams-Sonoma as a company did in 2022, so this business is truly helping to accelerate company growth as well as become a contributor to earnings starting this year.

We also like the diversity of client accounts that Howie mentioned, highlighting corporate office space, sports stadiums, and hospitality. There's undoubtedly client accounts they've won in other end markets that they couldn't mention on the call, but this small sample of referenced wins showcases that Williams-Sonoma has broad appeal in the B2B space.

Innovating Through Brand Extensions

We've reviewed how Williams-Sonoma is taking their core brand strength and leveraging that to create additional opportunities in other geographic markets as well as other customer markets. Another exciting area for the company is taking their brand power and innovating through brand extensions.

Think about Pottery Barn. The company was founded in 1949 and acquired by Williams Sonoma in 1986. (Fun fact: the company started off as a literal barn full of pottery). Then, in 1999, Williams-Sonoma opened up Pottery Barn Kids to focus on children's home furnishings, and in 2003, started Pottery Barn Teen to cater towards the teenage lifestyle for bedding, d é cor, and accessories.

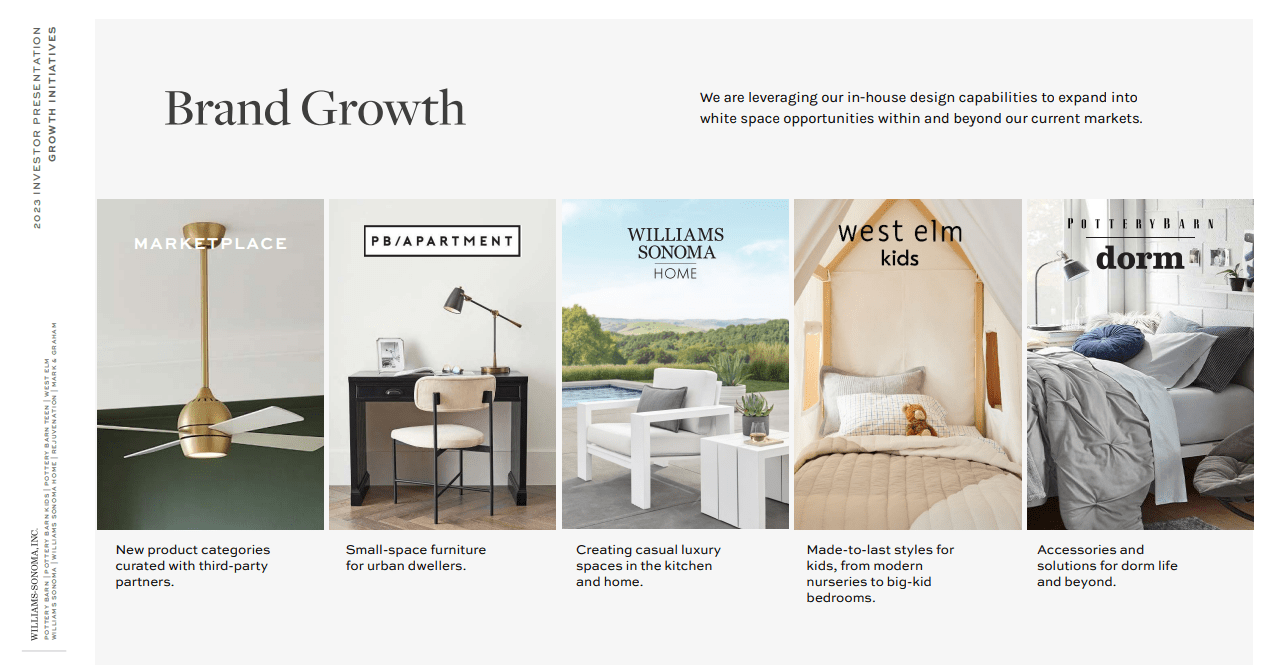

Recently Pottery Barn opened up PB Apartment and Pottery Barn Dorm to capitalize on this brand power. And it hasn't just been Pottery Barn that has been growing and extending their brand. West Elm has expanded into the kids market to appeal to an additional set of customers a little lower on the price point scale. On the other side of the price spectrum, Williams-Sonoma's Home category is an upscale extension of the namesake brand. And the company's nascent marketplace business, where it sells third-party branded goods, is on track to grow 20% annually.

Brand Growth (Williams Sonoma Investor Presentation, March 2023)

{kind=link}

Emerging Brands

In addition to its core brands of Williams-Sonoma, Pottery Barn, and West Elm, the company also has two emerging brands of Mark & Graham and Rejuvenation. Rejuvenation was acquired in 2011 and Mark & Graham was launched a year later.

Rejuvenation is known for classically-designed lighting and hardware. This fits well as an adjacent category for the company, as customers who are furnishing a room or outdoor space may also wish to add or update lighting fixtures, drawer handles, and door knobs.

Mark & Graham is more well known for its line of handbags, totes, suitcases, wallets, and other like items. This opens up cross selling opportunities between brands and caters towards Williams-Sonoma's more affluent customers.

During the Q4 conference call, CEO Laura Alber highlights the growth these brands are experiencing and mentions how they're capitalizing on remodeling and travel-related trends.

In our new businesses, Rejuvenation and Mark and Graham, have also provided incremental growth. Together, in fiscal 2022, they represented nearly $270 million in revenues and drove nearly a 10% comp on the year. These two brands service white space needs of customers. At Rejuvenation, we're expanding into remodel categories related to kitchen and bathroom, including vanities, cabinet hardware and custom wall lighting. And at Mark and Graham, our high-quality gift and personalization business is resonating with our customers, and we see outsized growth in the travel space, including luggage and accessories.

Risks

Williams-Sonoma is laying the foundation for this decade's growth and we are huge fans of this strategy. Additionally, there are other fundamental factors that only add to our bullish stance of the company. The company has zero debt, stellar operating margins, return on invested capital margins that triple their peers, and a growing dividend for the last 14 years. The stock also seems to trade for a low valuation at the current time, with a PE ratio of less than 9. In fact, WideAlpha recently published a superb write-up on the company that dives into the undervaluation of the shares.

However, as we mentioned earlier, as excited as we are about the potential that is about to be unleashed, we are applying our mental brakes and reviewing what could possibly upend our bullish view on the company.

A key risk at the forefront of everyone's mind is the supposed impending recession that's right around the corner. We've been waiting for this for quite some time and it is truly anyone's guess at this point when or if a recession will come, along with how deep or mild it will be. And yes, this is something to keep in mind when investing in a consumer cyclical stock like Williams-Sonoma. A deep recession will hit home goods categories hard.

Furniture, bedding, small kitchen appliances, cookware, and similar items are discretionary in nature. Consumers like to spend on their home, remodel, and buy a new sofa or two when they feel optimistic about the economy and have perceived job security. However consumers can also be very fickle and sentiment can turn on a dime if things start to go south.

William-Sonoma's customer base is relatively more affluent in nature than other retailers such as Target ( TGT ), Costco ( COST ), or Home Depot ( HD ). And affluent consumers are usually the last to feel the pressures of an economic downturn. Even during a downturn, these consumers are more likely to turn to small luxury items the likes of what Mark & Graham sells.

However, should a downturn become prolonged or deep enough, there would no doubt be decreased demand for Williams-Sonoma's brands, as consumers would shop only for necessity-based items such as food at Costco and tools at Home Depot for critical repairs. In the minds of belt-tightening consumers, brands like Pottery Barn would fall a couple of rungs on the priority ladder during this time, and the share price wouldn't be far behind.

However, it may not be all doom and gloom for the company if this were to transpire. The business model is more resilient than meets the eye.

CEO Laura Alber actually discussed this very topic during the earnings Q&A session, when one of the analysts questioned how the company is responding to an uncertain housing market. Her response shows a very insightful look into the mindset of the company and resilience of their business model:

People love their homes. They learned how to cook in the pandemic. And now as they continue to cut back spending elsewhere, they realize that going out to dinner is really expensive. So, the dinner party is back in full force, and it's an area that we're really focusing on. The other dynamic just to remind everybody is, if you can't move, what do you do? Eventually, you remodel. When you remodel, you buy new furniture.

So while fears of a potential downturn is likely keeping a lid on the share price for now, we think that the company's growth initiatives and strong fundamental profile can help them weather a coming storm. Being in a highly fragmented market is an added benefit for Williams-Sonoma. In a downturn, as smaller competitors contract, pull back ad spend, close stores, or go out of business, Williams-Sonoma is in a position to take market share and come out stronger on the other side.

Takeaway

To sum up, we like WSM stock for many reasons. The company sports truly impressive profitability and return-on-capital figures and a strong balance sheet. Shares are decently valued and sport a near 3% yield which was just raised for the 14th consecutive year. What we are really excited about is the runway for growth that the company is laying out to drive market share penetration in new categories, countries, and end markets.

We have confidence in CEO Laura Alber to continue driving this strategy forward and capturing as much potential as each of these initiatives can bring. After all, she's been at the helm since 2010, helping to steer the company in the right direction coming out of the Great Recession. She also successfully navigated the changing landscape over the last decade and pivoted towards ecommerce to enable the company to thrive, even as other retailers struggled to survive as they competed against Amazon's ( AMZN ) increasing dominance.

We usually don't actively seek out cyclical companies like Williams-Sonoma, however after recently offloading shares of V.F. Corp. ( VFC ) due to its dividend cut, we have been looking for a quality replacement. We think we have found just that in Williams-Sonoma, and plan to initiate a position in the near future.

There is a lot to like about this company, and for those readers who are intrigued, we encourage you to explore other Seeking Alpha articles on the stock as well as the company's investor relations site.

If you are looking for a high quality, mid-cap consumer stock with a safe dividend, strong fundamentals, and tremendous growth prospects, we think investors should look no further than Williams-Sonoma.

As always, thanks for reading. We hope you enjoyed this article! Feel free to let us know your thoughts in the comments section.

For further details see:

Williams-Sonoma: India, B2B, And Brand Extensions Are This Decade's Growth Drivers