WSM - Williams-Sonoma: Promotions Picking Up

2023-06-27 03:34:33 ET

Summary

- Williams-Sonoma has said it is looking to avoid sitewide promotions, but its Pottery Barn website paints a different story.

- The company's Q1 results show self-inflicted issues and a difficult market environment, making its full-year outlook seem optimistic.

- Despite navigating the market reasonably well, WSM's forecast may be too high; the "Sell" rating remains unchanged.

Back in April , I placed a “Sell” rating on Williams-Sonoma ( WSM ), saying that while the stock looks cheap if it can hit its numbers, it is facing a number of industry headwinds. Since then the stock has underperformed the S&P 500 but has managed a small positive return. Let’s catch up on the name.

Company Profile

As a reminder, WSM is a home furnishings, décor, and cookware retailer that operates under Pottery Barn, West Elm, Williams-Sonoma, Pottery Barn Kids, and Pottery Barn Teen banners. The company sells its goods both through its retail locations as well as through its e-commerce sites.

Pottery Barn is its largest concept, representing about 41% of its 2022 sales, while its Pottery Barn Kids and Teens brands were another 12%. It sells such things as bedding, furniture, rugs, decorative accessories, and lighting.

West Elm, which focuses on modern and contemporary furniture and home décor, is its second-largest concept representing over 26% of sales, while its name-sake brand was about 15% of sales in 2022. The William Sonoma brands sells items such as cookware, cookbooks, cutlery, tabletop and bar items, outdoor, and furniture. It also owns a few smaller brands including Rejuvenation, Mark and Graham, and Outward.

Margin Pressure And Lackluster Demand

One of the big themes when I’ve looked at companies in the home furnishings and décor space this year is that it’s become a very promotional environment. However, WSM has not gone that route, deciding to forgo site-wide promotions and only mark down items where it has too much inventory.

Despite not falling into the highly promotional environment, the company nonetheless saw gross margin pressure in Q1. Adjusted gross margins fell -520 basis points to 38.6%. Merchandise margins declined due to higher product costs, ocean freight, detention and demerge, while selling margins were hurt by higher outbound customer shipping costs.

The latter seems mostly self-inflicted, as the company said it was often shipping items to customers from out-of-market distribution centers and sometimes would have multiple shipments for orders with several units. The company is looking to rebalance its regional inventory and inventory composition to help this.

In Q1, the company was also hit by some of the general softness in the category, with sales off -7.2%, and comparable-brand revenue down -6.0%. The company said that demand was down about -10%, with notable softness in its high-end furnishing business.

West Elm has been its most impacted brand, with same-store sales down -15.8%. Pottery Barn has held up pretty well, with comps -0.4%, while William Sonoma comps were -4.4%.

Talking about the current environment on its Q1 earnings call , CFO Jeffrey Howie said:

“And we've talked a lot about how the first half of the year is going to be materially tougher, especially on the top line, we're up against last year's more higher demand comps and the back order fill. But the back half is a different story, where our demand really started to decelerate last year after Labor Day. And that's where some of our headwinds right now should become tailwinds. [With] respect to things like Bed Bath & Beyond, that's an area where we continue to believe we gain market share. It's clear to us we're gaining our share of the Bed Bath & Beyond volume up for grabs. For example, in the Williams-Sonoma brand, we're picking up share in kitchen electrics and registry. In Kids, we're picking up share from buybuy BABY. Those customers want certainty when decorating their nurseries and know that the store they're buying from will still be there in a few months. And in Teen, we're seeing an early benefit in dorm that we anticipate will ramp as we hit the back-to-school season. Bottom line is we think well positioned to gain market share in this fractured home furnishings industry with our in-house design, our digital-first, but not digital-only channel strategy and our strong and stable portfolio of brands.”

One area of potential opportunity I discussed in my original article was its expansion into the business-to-business (B2B) market. However, even that side of the market saw weakness. Overall B2B sales were down -7%, with most of the weakness on the trade side of the business. The company did see the contract side of the business see mid-double digit growth and said its pipeline for projects out to bid was stronger versus last year.

International expansion was another opportunity I touched on, and the company said it was seeing strength across all of its brands in the Middle East. Meanwhile, it said its early results in India were above its expectations. It also launched its B2B business in Canada in Q1.

Despite the weak Q1, the company maintained its full-year guidance for sales growth of -3% to +3%, as it believes current headwinds will turn into tailwinds as it sees easier comps in the second half. Longer term, it continues to expect mid- to high single-digit top line growth.

Overall, given its Q1 results, some self-inflected wounds, and a difficult home furnishings environment, I still feel that its full-year outlook looks a bit optimistic. While the company has refrained from full site promotions, it is currently running an up to 50% warehouse sale with over 7,700 items listed, and when just browsing the non-clearance section of its website there are a lot of items on sale.

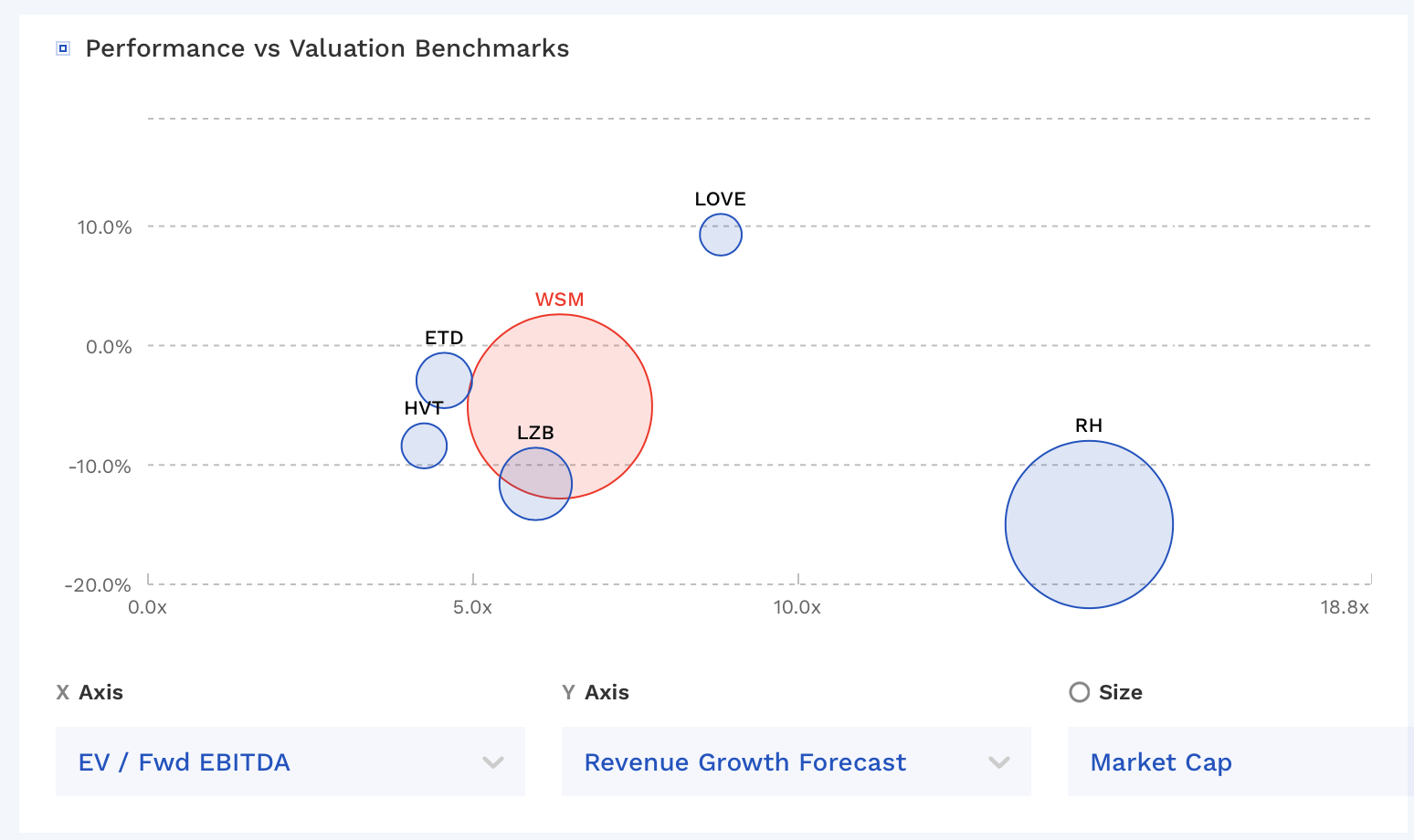

Valuation

WSM's stock currently trades under 6.4x the FY2024 (ending January) consensus EBITDA of $1.39 billion and 6.5x the FY2025 consensus of $1.37 billion.

It trades at a forward P/E of nearly 8.8x the FY24 consensus of $13.60 and just over 8.6x the FY25 consensus of $14.05.

Revenue growth is expected to drop -5% this year, and then grow 1% next year.

Outside of luxury furniture company RH ( RH ), which I recently wrote-up , and the faster-growing Lovesac ( LOVE ), which I wrote up here , WSM trades at a slightly higher valuation than other furniture companies.

{kind=link}

Conclusion

WSM is navigating a difficult home furnishings and décor market. The comps and drop in traffic certainly aren’t great, but they aren’t disastrous. Pottery Barn is holding up very well under the circumstances, showing the strength of its main brand. The company doesn’t want to play the deep promotional game that some peers are playing, which I view as smart. However, given its current sales going on now, that tone may have changed.

The margin deterioration looks self-inflicted, but is something that should be able to be fixed. Many companies have seen improved freight prices and improved supply chains. Why WSM is still dealing with these issues is a question, but it shouldn’t be something that is lasting.

The valuation isn’t a stretch, although is higher than many of peers. That said, I prefer the faster-growing LOVE in the space, as it has more distribution growth opportunities.

Overall, I still feel WSM’s forecast may be too high, as it expects a recovery in the back-half of the year in the face of a difficult environment. As such, there is no change to my “Sell” rating at this time.

For further details see:

Williams-Sonoma: Promotions Picking Up