WSM - Williams-Sonoma: Retail Winner With A Growing Dividend

2023-12-18 04:29:22 ET

Summary

- Williams-Sonoma is a retail company that has outperformed other retailers, with an 80% increase in stock price this year.

- The company has strong brands, an experienced CEO, and has been steadily increasing its dividend yield.

- WSM has growth opportunities in business-to-business sales, emerging brands, and international expansion.

It's been a tough year for many retailers as companies such as Target (TGT), Home Depot ( HD ) and Lowe's ( LOW ) have all underperformed compared to the S&P 500.

However, not all retailers have struggled. One retailer is up over 80% YTD and is up nearly 300% over the past five years.

The company has an experienced CEO, powerful brands, and has been steadily increasing its dividend yield.

The company is Williams-Sonoma, Inc. (WSM). Let's dig into the company to see if this retailer can have continued success in 2024.

The Company

Williams-Sonoma is specialty retailer known for selling premium high-quality products. The company's mission is to "Enhance the quality of life at home and beyond."

WSM has eight brands as you can see below:

Investor Presentation

The Pottery Barn brand (excluding Kids and Teens) generates the most revenue for the company followed by West Elm, and Williams-Sonoma, then followed by Pottery Barn Kids and Teens. Rejuvenation and Mark & Graham are usually categorized as "Other" within their segment reporting disclosure .

I've shopped at Pottery Barn (the main brand as well as Pottery Barn Kids), West Elm and Williams-Sonoma. I can attest to the fact WSM does create quality products that have improved our home experience. For instance, I've purchased a waffle maker and an outdoor pizza oven, both of which have created fun, memorable dining experiences with our friends and family.

Regarding Pottery Barn although their items are at a high price point, the in-store design element is a key differentiating in the market and one the company specifically mentioned in their latest investor presentation. When we were expecting our first child, we looked at Pottery Barn Kids and purchased a few items for our nursery. I remember being impressed by the various options and how a couple could, with the help of Pottery Barn, design their nursery there from top to bottom.

If you don't want to go visit a Pottery Barn location and use their in-design service, the company offers online options as well. WSM's e-commerce business has been growing over the last few years as you can see from the image below. Two-thirds of the company's total revenue now comes from their online business:

Investment Presentation

Moat and Opportunity

WSM believes they have an addressable market of $80 billion. The management team has noted three growth initiatives for the company which are business-to-business, emerging brands, and global reach.

Regarding B2B opportunities, the company believes they have opportunities to serve various different organizations and industries some of which could include hotels, resorts, universities, hospitals, and entertainment arenas. On the company's Q3 earnings call , CEO Laura Alber noted a few positive developments on this front including partnerships with Pendry Hotels and Dave & Buster's.

The company's two emerging brands are Rejuvenation and Mark & Graham. Alber noted it was positive quarter as Rejuvenation opened new stores in San Diego and North Carolina.

Lastly, for the current quarter international sales accounted for roughly 4% of total revenue. Alber noted momentum in Mexico and Canada but it certainly seems like WSM has plenty of opportunity to expand internationally.

Overall, I do think WSM has a moat. This company has unique, distinctive brands and I believe the design-in-store feature is differentiating. I don't think with other brands it's as easy to walk into a store and create a custom bedroom, child's room or nursery but that's what you can get when you walk into a Pottery Barn.

Management

Laura Alber has been with WSM for nearly two decades now as she first joined the organization in 1995. She has been the President and CEO of WSM since 2010.

Jeff Howie is the company's current CFO. Similar to Alber, Howie has a long tenure with WSM as he's been with the company since 2002, although he hasn't held his current title for that entire duration.

As you can see from these Glassdoor ratings , the company isn't receiving rave reviews with a mere score of 52%. However, as this is a retail operation it is comparable to other retailers such as Lowe's and Target. The employees do seem to approve of Alber as she has a decent approval rating as you can see below:

Glassdoor

One of my favorite investors to follow is Terry Smith. Similar to Warren Buffett, Smith believes in buying and holding excellent companies at reasonable prices. In his book, "Investing for Growth" Smith discusses a key metric he looks at shareholder returns. Return on equity ((ROE)) and return on invested capital ((ROIC)) are two key metrics I review when assessing companies and it's clear Alber and her team have done a tremendous job generating industry-leading returns as the below graphic illustrates:

Investor Presentation

As a long-term investor, I'm also looking for companies that generate returns for shareholders, whether that's in the form of continued growth, dividends or even share repurchases. WSM has constantly provided returns to shareholders. The company has increased its dividend yield for 13 consecutive years and as you can see below the company has continued to buy back its own shares as well:

Investor Presentation

Financials

In Q3 2023, the company generated net revenue of roughly $1.854 billion which was a decrease of nearly 15% compared to Q3 2022. The two-year stack was also negative at -6.5% however, compared to 2019, revenue grew roughly 15%. Furthermore, looking at this graphic from an investor presentation, despite some recent year-over-year revenue declines the company has grown revenues at a CAGR of over 11% over the last five years as you can see below:

Investor presentation

Alber noted the revenue decline was due to the macroeconomic climate as consumers aren't spending as much on big-ticket items such as furniture.

Despite this decline in revenue, gross margins were 44% for the quarter and operating margin was 17% which is a record for the company.

WSM has a stellar balance sheet. The company's cash balance is nearly $700 million as of October 29, 2023, and their current assets balance can cover all of the organization's current liabilities as you can see below:

SEC.gov

The company has no debt and retaining earnings continues to grow which is certainly a positive.

Risks

WSM lists numerous risks to the business on its 10-K statement . I'm going to discuss two risks that I believe could hurt the organization.

At least in the short term, I view consumer spending as a risk for the organization. Debt (especially credit card debt ) levels are extremely high currently and many Americans are resuming paying off their student loans. Furthermore, I think WSM has higher end products, even West Elm, I don't view as particularly cheap. Many consumers may not have the income for such costly home furnishings or may shop at stores such as Target or Costco for cheaper alternatives.

For the long term, I think it's vital WSM keeps its brand image intact. Brands such as Target and Bud Light clearly suffered from mishaps this year which clearly hurt their brands. I think Alber has a clear image of the business and the distinct brands that fall under WSM's umbrella. Nonetheless, any future marketing or product mishap could tarnish the company's image, impacting the financials and long-term outlook of the organization.

Valuation

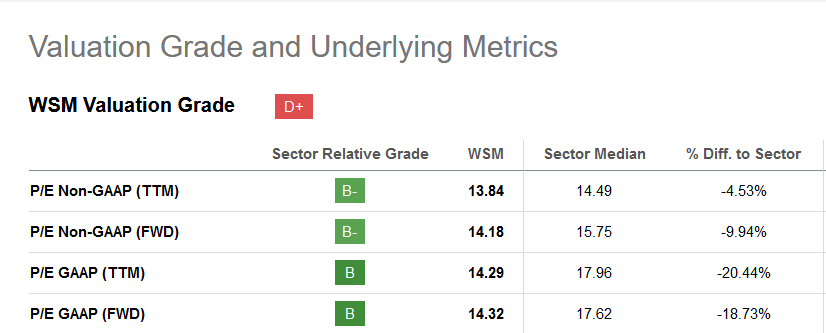

As you can see from the below valuation metrics from Seeking Alpha, the overall value grade for WSM is a "D+."

{kind=link}

In the above metrics, WSM is viewed as favorable compared to many of the sector median values. Given it's profitable, I think Price/Earnings ratio is a good metric to view this company. The forward P/E ratio of 14.32 is below the median of 17.32 and given the company's growth prospects domestically with B2B and internationally I think investors could add or initial a position at these levels.

Conclusion

I believe WSM is an excellent company. The organization has an experienced management team and is focused on continued growth while rewarding shareholders. WSM has several growth opportunities such as selling to businesses and expanding internationally.

The company's financial performance has been impressive over the last five years as revenue has continued to grow while the company has increased its dividend yield and repurchased stock.

WSM has several unique brands giving them an advantage in the retail market and I would state they have been succeeding in their mission of enhancing the quality of life in the home.

2023 has been a fantastic year for WSM as the company has surged past the S&P 500 and I see no reason as to why 2024 won't be similar given the track record of this organization.

Long-term investors can add this stock to their portfolios and sleep easy knowing this company will likely continue to thrive in the years to come.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short competition, which runs through December 31 . With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Williams-Sonoma: Retail Winner With A Growing Dividend