WSM - Williams-Sonoma Stock: Too Far Too Fast

2023-12-15 10:32:26 ET

Summary

- Williams-Sonoma, Inc. stock has surged 85% in the past six and a half months, even as the company is expected to show its first annual net revenue decline in 14 years.

- The rally has occurred despite largely negative analyst firm opinion on Williams-Sonoma stock and some recent insider selling in the shares.

- The stock seems vulnerable to profit taking after its big run. An analysis around Williams-Sonoma, Inc. follows in the paragraphs below.

Perhaps home is not a place but simply an irrevocable condition .”? James Baldwin.

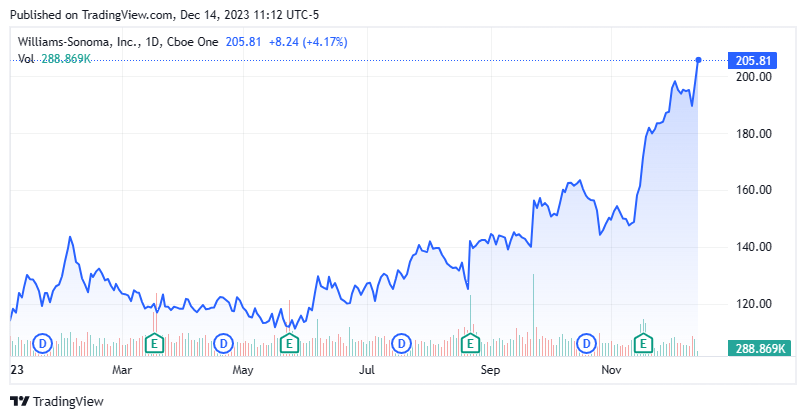

Shares of furniture and home textile concern Williams-Sonoma, Inc. ( WSM ) have surged 85% in the past six and a half months on improved operating margins, including a record in Q3 FY2023 . However, the company is on pace to register its first annual net revenue decline – forecasted at -11% – in 14 years, after initial expectations were for a flat FY23.

{kind=link}

Company Overview:

Williams-Sonoma, Inc. is a San Francisco-based specialty retailer of products for the home, featuring nine brands and five storefront concepts, including namesake Williams-Sonoma, Pottery Barn, and West Elm. The company employs over 150 designers and artists to create proprietary home furnishings, cookware, and lighting (amongst many other offerings) that are sold in 532 locations in the U.S., Canada, Australia, the UK, and online. Williams-Sonoma’s first store opened in 1956, later moving from Sonoma, California to San Francisco that same year. The company went public in 1983, raising gross proceeds of $23 million at $0.76 per share, after giving effect to five 3-for-2 and two 2-for-1 stock splits. Shares of WSM trade at just over $205 a share, translating to an approximate market cap of $12.7 billion.

The company operates on a 52- or 53-week fiscal year ending the Sunday closest to January 31st. For the avoidance of doubt, the 52-week period ending January 29, 2023 was FY22.

Revenue Disaggregation

Although Williams-Sonoma essentially breaks out its sales by physical storefront, it derives approximately two-thirds of its top line online, making it the 22nd largest such retailer in the U.S. and the number one non-pure play ecommerce home furnishing brand. The segments are Pottery Barn, West Elm, Williams-Sonoma, Pottery Barn Kids and Teen, and Other.

Pottery Barn offers furniture, home textiles, and decorating products from 191 locations. For the 39 weeks ending October 29, 2023 (YTDFY23), it generated net revenue of $2.33 billion, down 10% from YTDFY22.

West Elm sells relatively lower-priced modern furniture and home décor from 123 properties. It was responsible for YTDFY23 net revenue of $1.40 billion, lower by 20% from YTDFY22.

Williams-Sonoma provides items predominantly for the kitchen and dining room out of 164 storefronts. It accounted for YTDFY23 net revenue of $735.9 million, down 4% from YTDFY22.

Pottery Barn Kids and Teen offers furnishing, bedding, and accessories from 46 locations. It contributed YTDFY23 net revenue of $749.2 million, lower by 8% from YTDFY22.

Other consists of the Rejuvenation, Mark and Graham, and GreenRow brands, as well as the company’s international franchise operations. It generated YTDFY23 net revenue of $252.4 million, down 20% from YTDFY22.

Approach

Despite the disruption from the pandemic, Williams-Sonoma has grown net revenue every year since an 8% downturn in FY09. With the company more recently employing a digital-first but not digital-only strategy, the store count has decreased by 15% since FY19 with an eye on closing another 10% over the next three to five years. To continue to grow its borderline iconic and mature brand, management has expanded into the $80 billion business-to-business furnishings market; introduced relatively new brand concepts, including the aforementioned Mark and Graham (monogrammed home gifts, luggage, and handbags) and Rejuvenation (classic lighting, hardware, and home décor) offerings; and employed a capital-light franchise model to move into international markets.

Capital is returned to investors through both share repurchases and dividends.

Share Price Performance

With consistent growth over the past decade and through the pandemic, shares of WSM have soared 5,034% in a 13-year stint, peaking at $223.32 in November 2021, which represented a 15.0 P/E on FY21 non-GAAP EPS of $14.85. However, despite growing its non-GAAP EPS 11% to $16.54 on a 5% net revenue increase in FY22, its stock began a six-month, 55% downdraft to $101.58, for a P/E on FY22 non-GAAP EPS of 6.1, as the market fretted about inflationary impacts on both expenses and discretionary spending. Shares of WSM were still as low as $109.44 in May 2023 after the company’s initial FY23 outlook of flat net revenue growth – below its stated long-term goal of mid-to-high single digit growth – somewhat validated the bearish camp’s concerns about the macroeconomic backdrop.

However, from that point forward, Williams-Sonoma stock has rallied some 85% despite a revision to its FY23 net revenue estimate from flat to negative 7.5% (based on range midpoints) concurrent to the release of its 2QFY23 financial report in August.

Q3 FY2023 Financials

Oddly, on the surface, it was more of the same when the company reported 3QFY23 financials on November 16, 2023, posting earnings of $3.66 per share (non-GAAP) on net revenue of $1.85 billion versus $3.72 per share (non-GAAP) on net revenue of $2.19 billion in the prior year period, representing declines of 2% and 16%, respectively. However, the bottom line was $0.33 a share better than consensus, although the top line was $90 million shy of expectations, reflecting a year-over-year comp of negative 14.6%. The "disconnect" was Williams-Sonoma’s operating margin, which at a Q3 record of 17%, was approximately 2% better than expectations as full-price selling and supply chain efficiencies (i.e., lower shipping and ocean freight costs) were cited for a 290-basis point year-over-year improvement at the gross margin line to 44.4%, overcoming the drop in volume.

Furthermore, management stated in the earnings press release that, “ early seasonal reads are strong and we are optimistic about the holiday season .” That said, it lowered its FY23 net revenue outlook again, from down 7.5% to down 11%, but upped its operating margin forecast from 15.5% to 16.25%, based on range midpoints. With the market focusing on the bottom line, shares of WSM, which were already up $12.63 in the prior two trading sessions, surged another $20.56 over the subsequent three days to $181.95, capping a one-week, 22% heater.

Balance Sheet & Analyst Commentary:

Additionally, Williams-Sonoma’s balance sheet is in pristine condition, reflecting cash of $698.8 million and no debt. The company has repurchased 2.6 million shares on its current $1 billion program during FY23, but elected not to buy back stock in 3QFY23 – citing its stock’s strong performance – leaving $690 million remaining on its authorization. It also pays a $0.90 a share quarterly dividend for a current yield of 1.8%.

Ten Street analysts used the strong operating margin news as a reason to lift their price objectives, but as a whole, they are downbeat on Williams-Sonoma’s prospects, featuring two sell, three underperform, and 16 hold ratings against only one buy and four outperforms. Their mean price objective is slightly north of $170. On average, they expect the company to earn $14.55 a share (non-GAAP) on net revenue of $7.7 billion in FY23, representing the first yearly decline in that metric since FY09. In FY24, they forecast non-GAAP earnings of $14.70 on another net revenue decline to $7.68 billion.

It is also noteworthy that President & CEO Laura Alber has sold 120,000 shares of WSM since late September. Additionally, Chief Talent Officer Karalyn Smith (1,945 shares at $179.85) and Pottery Barn CEO Marta Benson (5,374 shares at $178.86) were sellers on November 21-22, 2023.

Verdict:

While Williams-Sonoma, Inc. stock is not outrageously expensive at 14.2 times FY24E non-GAAP EPS, the recent run to north of $205 a share puts Williams-Sonoma stock at risk if the consumer does not turn meaningfully around. In other words, shares of WSM are not going to climb 66% next year if net revenue numbers are again adjusted from flat to down 11%. Cheaper freight prices are likely secular, adding to the durability of the company’s operating margins. However, if its more affluent consumer base continues to shy away from buying or replacing furniture, promotions or higher inventories may be in the company’s future, especially as competitors are offering considerable discounts to list price. Obviously, that outcome would negatively impact margins.

The bet here is that the hangover from a tapped-out consumer will continue, and next year’s top-line forecast, although lower, is simply overly optimistic after Williams-Sonoma, Inc. experienced its first net revenue decline in 14 years.

If the best things in life are free, the second-best things cost only a handful of pennies .”? Gabriella Bennett.

For further details see:

Williams-Sonoma Stock: Too Far, Too Fast