WSM - Williams-Sonoma: Timing Is Still Great

2023-09-08 08:14:56 ET

Summary

- Williams-Sonoma's stock price drop presents a great opportunity for investors to buy into the consumer discretionary company.

- Despite the current bumpy performance, the Williams-Sonoma stock offers an excellent investment opportunity.

- On the one hand, the dividend yield and expected increases are attractive.

- The company is making progress in reducing its inventory and addresses the $80 billion B2B market.

- On the other hand, the stock also has further upside potential from a fundamental perspective.

Williams-Sonoma ( WSM ) has been on my watch list for many years. I took advantage of the price drop of more than 40 percent since the end of 2021 to build up my first position in the company. Since then, I have been investing about 4 percent of my available capital in the stock every month (I have about 20 savings plans running at the same time). While the stock is not quite as attractive as it was a few weeks ago after the recent price increase of more than 20 percent, the current price regions are still providing investors with a great window to invest in the consumer discretionary company.

Sure, the current fiscal year might be a bit bumpy but after that I expect sales and earnings performance to improve. With a decent dividend yield of 2.4%, a very comfortable payout ratio, and fairly cheap valuations, fans of dividend growth companies and value investors alike will get their money's worth.

Looking at the inventory

One issue I've noticed at Williams-Sonoma is the increased inventory. This forces companies to dump inventory on the market at a discount, which in turn adversely affects margins and brand image.

At Williams-Sonoma, however, I want to put things into perspective. Even though too much inventory is always the result of mismanagement, this was not atypical in but affected the entire industry. Companies like Wayfair ( W ) and Fortune Brands Innovation ( FBIN ) also struggle with too much inventory. Williams-Sonoma, however, is making progress.

For example, inventories are only 4.4 percent higher than they were at the beginning of 2022, a significant reduction in comparison, as inventories increased 30 percent by the end of 2023 compared to the beginning of 2022. Williams-Sonoma also compares favorably to Wayfair and Fortune Brands Innovation.

It should also be taken into account that the inventory can also grow due to the underlying business, for example because more products are sold or more stores are opened. In this respect, it is absolutely correct when management emphasizes in the previous earnings cal l:

And finally, third, our Q2 ending inventory levels are up only 9.5% versus same period in 2019, and that's with revenue comps of 40% over the same time frame.

In this respect, we can note two results here:

- Williams-Sonoma has the inventory problem under control and is reducing existing inventories faster than other competitors.

- Overall, the inventory is very small compared to total sales. Therefore, we should not make the problem bigger than it is. Inventory growth of less than 10 percent coupled with a 40 percent increase in sales is an impressive achievement.

Outlook is good

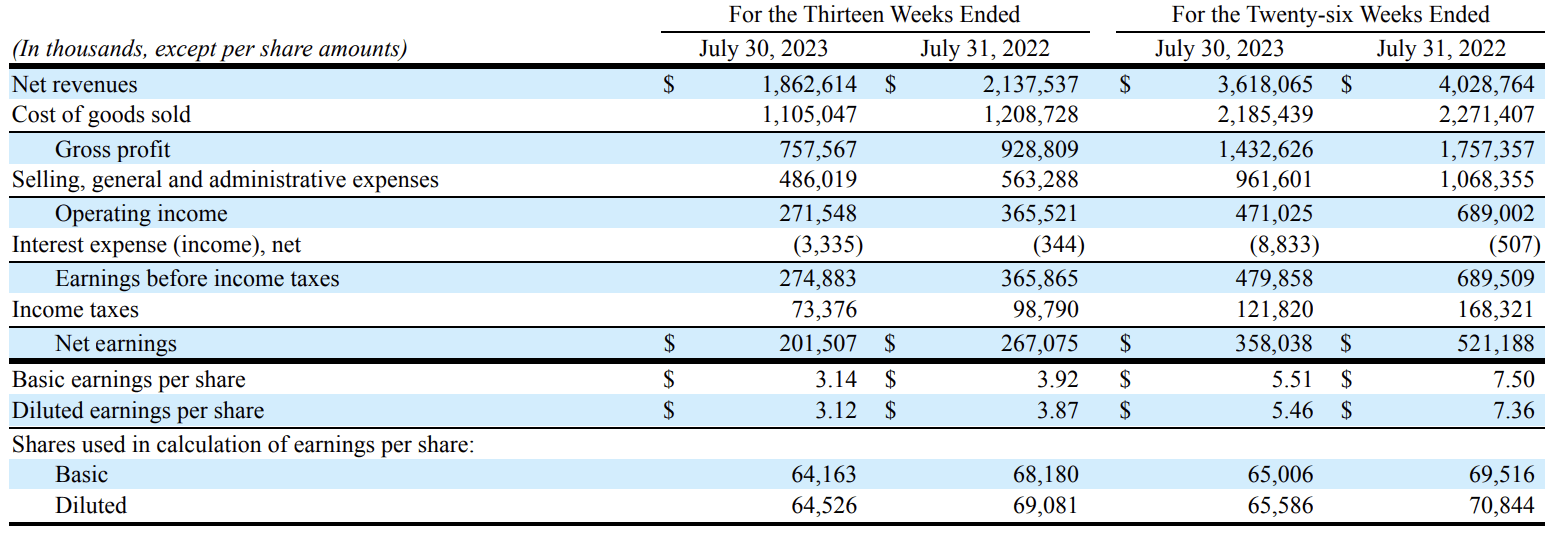

Despite the current improvement in inventories, the current fiscal year is still likely to be somewhat bumpy. For example, second quarter sales were down 11% compared to the same period last year. On a six-month basis, revenue fell from $4.03 billion to $3.62 billion. Net earnings fell from $521 million to $358 million. EPS fell from $7.5 to $5.5.

{kind=link}

Form 10Q Williams-Sonoma (Investor Relations Sec filings)

Management also had to withdraw its forecast for the fiscal year. There was one piece of good news and one piece of bad news. Although the decline in sales will be worse than feared, management has raised its expectations for margins.

We are revising our fiscal 2023 guidance to reflect lower net revenue trends and higher operating margin expectations.

In fiscal 2023, we now expect net revenue growth in the range of -5% to -10% with an operating margin between 15% to 16%.

Over the long-term, we continue to expect mid-to-high single-digit annual net revenue growth with operating margin above 15%.

While the news of better-than-expected profitability was obviously very well received by the market, I expect the revenue momentum to improve in the coming years as well. For one thing, we must not forget that Williams-Sonoma came out of an extreme growth phase in which it increased sales from $3 billion in 2010 to $8.6 billion in 2022, nearly tripling its revenue. It is normal for such growth to run out of steam sooner or later in a cyclical sector of the economy.

So let's look at Williams-Sonoma's fundamental positioning because it is very compelling. First, there is e-commerce. The company now generates 66% of its sales online with a CARG of 16.6%. Besides that, I find the entry into the $80 billion B2B market extremely interesting and very promising, given Williams-Sonoma's brand breadth. With hotels, schools, offices or public facilities, I see completely new areas opening up for the company to sell its products.

Analysts are also optimistic that after a transitional year in 2023, both profits and sales will pick up again in the coming years. EPS, for example, is expected to rise to over $15 by 2026. Sales are also expected to improve again to around $8.3 billion.

Dividend is safe and more hikes likely

Now forecasts and flowery promises are one thing. Besides, the projected growth is not exorbitant, so I wouldn't invest in Williams-Sonoma just because of the growth story. Personally, I like my food on the table rather than on the menu anyway.

So let's look at the dividend. Williams-Sonoma has paid a dividend for 15 years and has increased it every year for the past 12 years. The increases have averaged between 11% and 15%. The fastball effect is enormous. While the quarterly payout in 2006 was $0.1, it is currently $0.9. The payout ratio is 23% based on earnings and 20% based on FCF. Thus, despite the expected decline in profits, further dividend increases in the range of 8% to 10% are possible in the coming years. It is therefore not unlikely that the yield on cost will be well above 3% in three years' time. And we all know that this is when the snowball really starts rolling.

Taking the upside potential into account

In addition, Williams-Sonoma is currently also very attractively valued from a fundamental perspective. For example, the 5y median PE ratio is 14.3, while the current PE ratio is in the single digits. Even taking into account the decline in earnings for the current fiscal year, the earnings multiple is just 10.

For a company as solidly managed as Williams-Sonoma, this is an extremely attractive valuation and almost makes it a steal. Given the earnings decline, it is not necessarily justified that we see earnings multiples above 14 or 15 or even higher, but I still think a valuation with a PE ratio of 12 to 14 is absolutely justified. This still gives the share price a very attractive upside potential of 20% or more for the next 12 to 24 months.

Conclusion

Despite the current bumpy performance, the Williams-Sonoma stock offers an excellent investment opportunity. On the one hand, the dividend yield and expected increases are attractive. On the other hand, the stock also has further upside potential from a fundamental perspective. From my point of view, the stock is therefore a buy and part of my monthly savings plans.

For further details see:

Williams-Sonoma: Timing Is Still Great