WSM - Williams-Sonoma: Top Pick As Recessionary Pressures Wane With Multiple Strong Growth Vectors

2023-04-26 15:25:15 ET

Summary

- WSM is facing recessionary pressures and its near-term growth outlook is murky.

- Operating metrics are impressive, the balance sheet is pristine, and I see the potential for continued strong FCF generation.

- The valuation today is compelling, and improvements in the overall economic picture should be a catalyst heading into 2024.

Following full year 2022 results, I am writing today to update my outlook on Williams-Sonoma ( WSM ). Until recently, the company has been relatively immune from recessionary pressures.

{kind=link}

Over the longer term, WSM has modestly outperformed the S&P 500. However, recent performance appears to mark an inflection point. As the company has embraced the omnichannel approach, margins have drastically improved along with overall profitability. The store footprint is down 20% over the past five years as e-commerce now accounts for 66% of sales.

{kind=link}

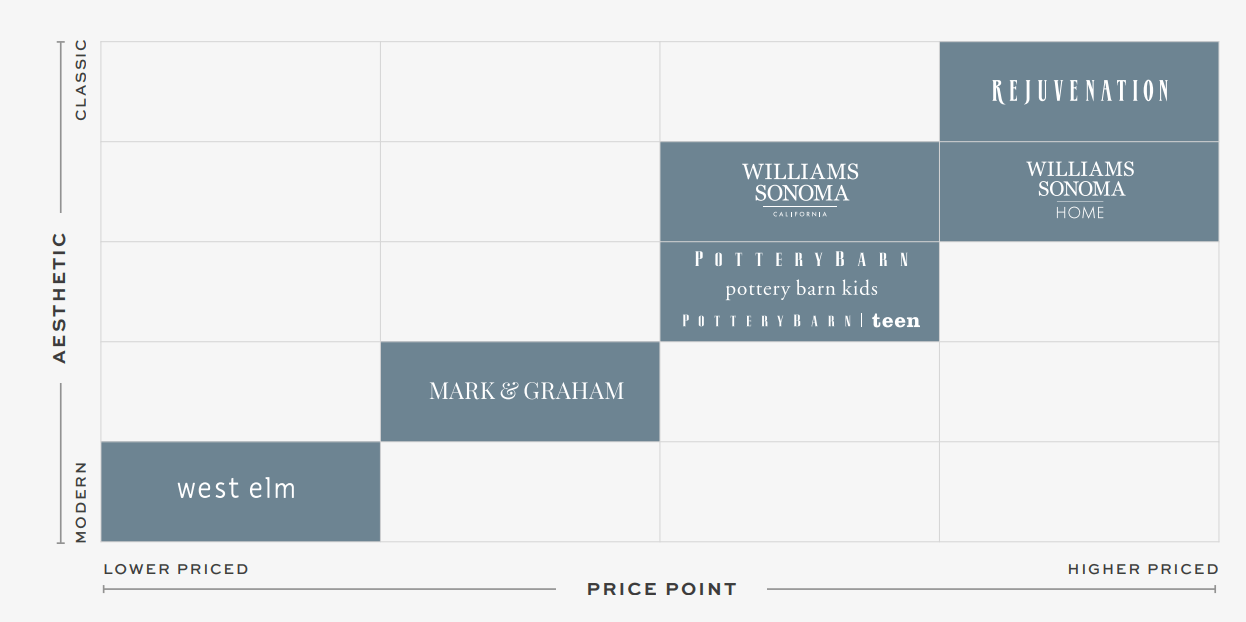

The company's brands are established with the intention of marketing across age groups and price points. Mark and Graham and Rejuvenation are two of the newer brands with strong growth, driving 10% comp's in 2022. The company's cross-brand loyalty program drives meaningful data for targeted advertising, and minimizes cannibalization between brands. Additionally, the age disparity is a solid strategy of attempting to gain new customers as they move into their first house/apartment and locking them in to the loyalty program early.

Company presentation

The company's overall strategy has borne fruit. In 2022, the company well outpaced the overall market in revenue growth, showing a gain in market share.

I've read plenty of prognostication that Wayfair ( W ) and other e-commerce native retailers will prevent WSM from continuing its march forward in home furnishings. However, looking above, WSM managed to vastly outpace revenue growth through COVID in top-line growth.

Despite growing the top-line faster, the company has also done it much more profitably. With a streamlined advertising budget and modest and improving SG&A to revenue profile, the company has done well to expand margins over time. Like I mentioned above, there was a positive inflection point in 2020 and management now projects an effective operating margin floor at 15%.

Despite gross margin pressures in the most recent quarter due to higher shipping costs and input cost inflation, the company was able to pull through, overall, as they continued to maintain positive leverage in SG&A expenses.

Revenues in 2022 were up 6.5% to $8.674B, with e-commerce growth of 4.5% and retail growth of 11.1%. The beauty of the omnichannel here is WSM's ability to outpace e-commerce growth with its store footprint despite the massive shift the business has seen to online sales. GM deleveraged 380 bps, as I discussed above, offset by a 140 bps improvement in SG&A to revenue. Operating margin came in at 17.5% on the quarter.

Looking forward, 2023 projections are still wide and not great, however. Macroeconomic pressures are projected to materially impact the business in the front half of the year based on softening through the fourth quarter. Management guided to -3% to +3% revenue growth for the year on a 14-15% operating margin.

However, these pressures will pass, and are expected to improve into the back half of the year. I remain bullish on the long-term prospects here. The company's B2B ventures have been nothing short of a smashing success. Last year, the company booked nearly $1B in B2B revenue, up 27% yoy and 166% over the past two years. The company is aiming for $2B in revenues and sees the total addressable market at $80B. Additionally, the foray into India appears to be a win-win for WSM. The company is leveraging a local partnership to break into what is likely to be the most important market of the century. I prefer local partnerships to allow savvy businesspeople who understand the market to build out the business, reducing the overall risk of failure.

The company's capital position is sound. WSM carries no debt with $367M on the balance sheet in cash. The dividend was just hiked for the 13th consecutive year by 15%, and management appears committed to continuing that streak. The board approved a $1B share buyback program, which seems appropriate given the company's valuation. Looking at capex, 2023 is projected to be 20% lower than 2022 at around $250M, which is well within the company's free cash flow means. All in all, WSM's balance sheet looks to be in great shape, and I anticipate solid cash flows for shareholders from here.

{kind=link}

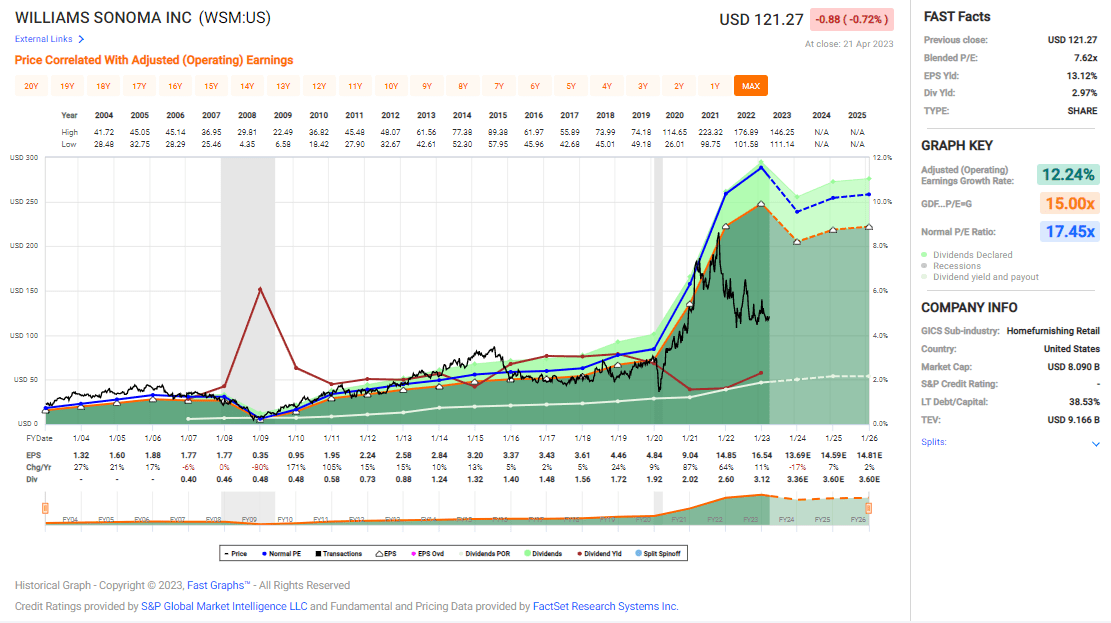

The earnings growth into 2021 was a thing of beauty. However, looking ahead, it's expected to materially level off as the company's margin expansion isn't projected to continue. Earnings growth over the long-term sits at around 12%.

{kind=link}

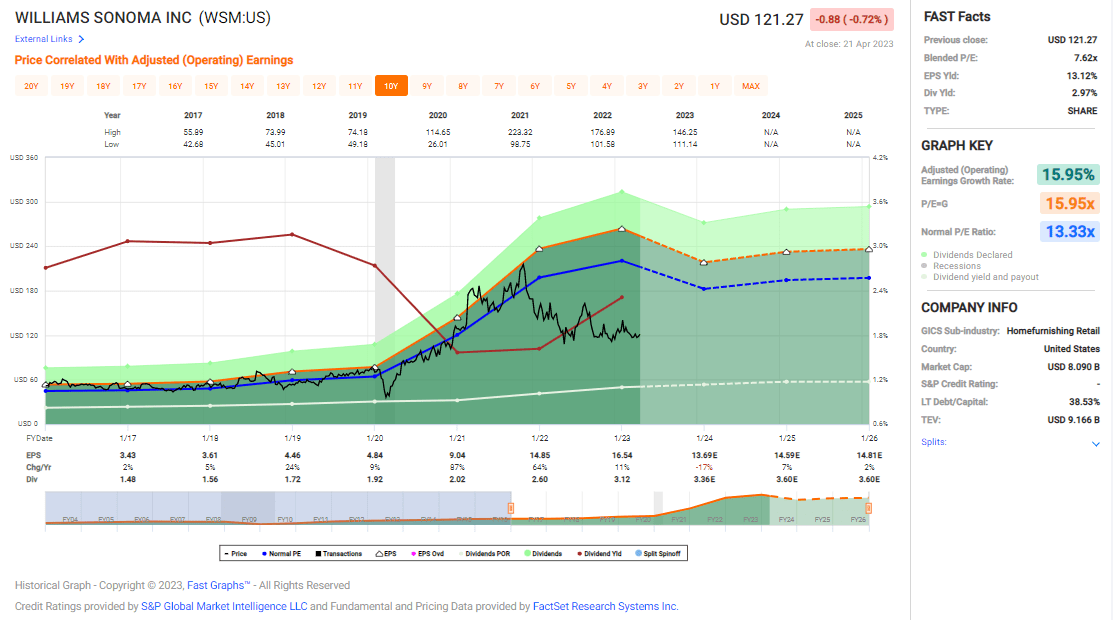

Zooming in, however, and earnings growth averaged since 2012 shoots up to nearly 16%. The average valuation remains modest.

{kind=link}

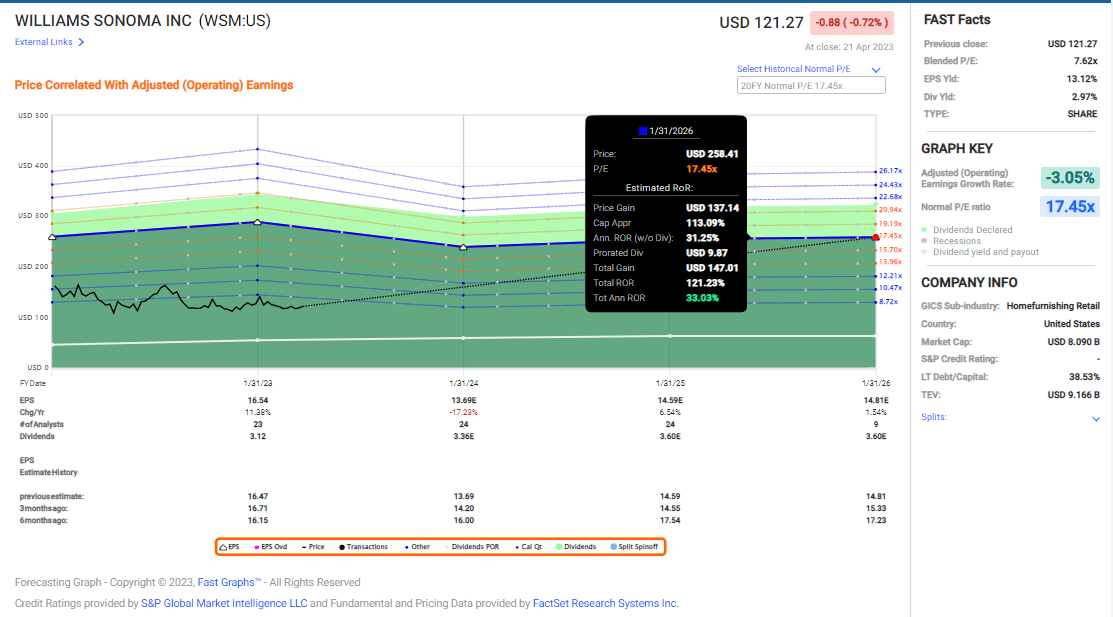

Based on a return to the longer-term average valuation of 17.5X earnings, which seems fair, an investment today could yield upwards of 33% annualized returns into 2026.

{kind=link}

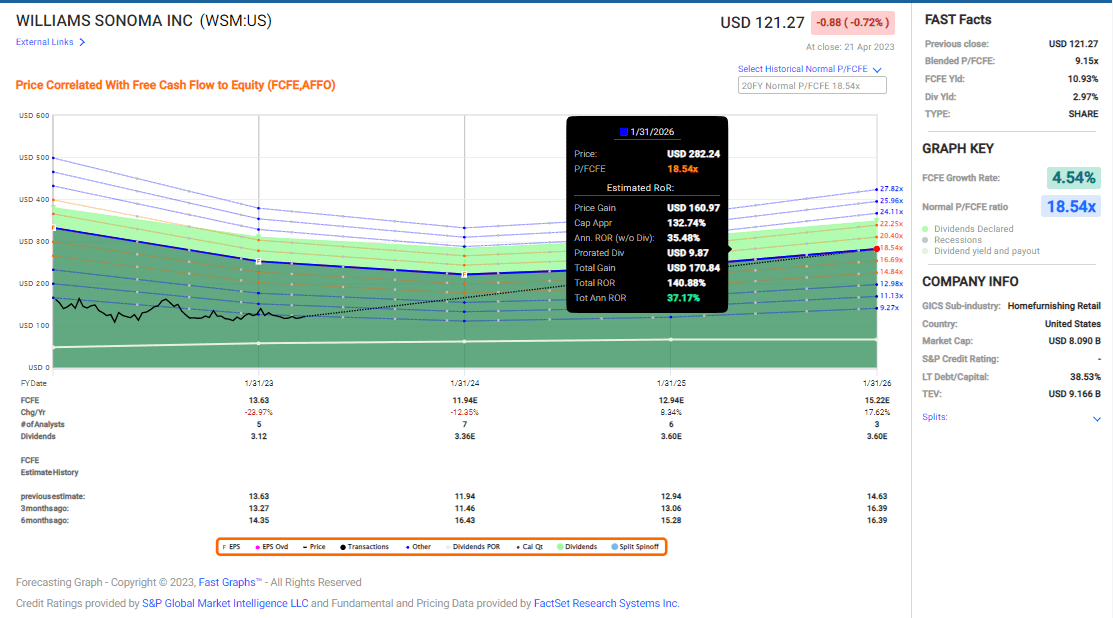

Looking at free cash flow growth projections, an investment today could yield upwards of 37% annualized total returns on a return to the long-term average valuation. Projections drop to returns of 21% on more modest 13X free cash flow.

These projected returns are just a method of tracking the company's current valuation against a likely path for metrics from here. Don't hang your hat on them, but it shows me that WSM is materially undervalued considering the strength of the business. The company has multiple strong growth vectors, is a best-in-class operator taking market share, and nearly every metric is pointed in the right direction. The balance sheet is pristine, but near-term growth remains murky considering the macroeconomic backdrop. I'm happy to wait. WSM is a strong buy, and one of my top picks for the 3–5-year time horizon.

For further details see:

Williams-Sonoma: Top Pick As Recessionary Pressures Wane With Multiple Strong Growth Vectors