WSM - Williams-Sonoma: Very Undervalued For The Long Run

Summary

- Williams-Sonoma is a leading lifestyle brand and generates strong margins.

- It has a robust analytics platform and growth opportunities through its B2B strategy.

- Meanwhile, it maintains a strong balance sheet and offers compelling total return potential.

Many stocks have fallen into deep bargain territory, with strong potential for capital appreciation. What's even better is if they pay a dividend to investors for being patient. This brings me to Williams-Sonoma ( WSM ), which has a number of premium brands that strongly resonate with consumers.

As shown below, the stock is now well off its 52-week high while paying a respectable dividend yield. In this article, I highlight why WSM is a stock that should be on a value investor's radar for potentially strong total returns, so let's get started.

{kind=link}

Why WSM?

Williams-Sonoma was founded in 1956 and is a specialty retailer of home furnishings, including kitchen appliances, cookware, and home decor. Its brands and stores include its namesake Williams-Sonoma, which offers high-end cooking products, Pottery Barn, and West Elm, which is an emerging concept for young professional. WSM also caters to developers of commercial and residential projects.

What sets WSM apart from the average retailer is its strong brand recognition and customer loyalty. The company has a reputation for offering high-quality products and excellent customer service, which has helped it build a loyal customer base. It also has a robust online presence with a strong social media following, as reflected by the 1.6 million Instagram ( META ) followers that it currently has.

WSM's premium brands also enable it to generate well above average margins. This is reflected by its strong A Profitability grade, with EBITDA and Net Income margins of 20% and 13.5%, which as seen below, are well in excess of the sector median.

WSM Profitability (Seeking Alpha)

{kind=link}

Meanwhile, it appears that WSM is doing just fine, with third quarter comparable brand sales growth of 8% YoY, and an impressive 25% and 50% sales growth on a 2 and 3-year stacked basis, respectively. Notably, WSM has maintained disciplined cost control and inventory management, as reflected by EPS achieving a faster growth rate than revenue, with 12% YoY growth to a record $3.72.

Looking forward, management is guiding for steady operating margins compared to last year, and mid-to-high single digit revenue growth for the full year. However, the market has reacted badly to the stock price in recent months, of fears of slowing revenue growth, and the fact that management pulled guidance for next year and 2024.

WSM does have risks from economic uncertainty induced by higher interest rates, as customers may pull or delay purchases on home furnishings. Moreover, WSM may see a slowdown in its B2B business, as commercial residential projects may be delayed due to higher cost of funding.

Notwithstanding the near term challenges, I see potential for WSM to come out stronger on the other side, as it's proactively working with its supply chain to reduce costs and pass value to customers, which should put it on stronger competitive footing. Moreover, it shouldn't be ignored that WSM has a robust analytics platform to drive customer loyalty and its expanded B2B strategy has great potential. These attributes were noted by Morningstar in its recent analyst report :

Williams-Sonoma's ability to drive repeat business relies on customer loyalty and smart marketing and merchandising and the firm has access to some of the best analytics in retail. This should help Williams-Sonoma outperform its competitors and grow its market share, aided by new category expansions.

In recent years, Williams-Sonoma has set its sights on expanding its total addressable market outside of furniture and home furnishings, via B2B and marketplace efforts, categories with robust end markets that remain fragmented. These white-space business lines, along with faster growth from both franchise and the e-commerce channels (which accounted for 66% of 2021 sales) should help Williams-Sonoma reach $10 billion in sales in 2026.

Importantly, WSM carries a very strong balance sheet, with a net debt to TTM EBITDA ratio of just 0.75x. While the 2.6% dividend yield isn't particularly high, it does come with a very low 18% payout ratio.

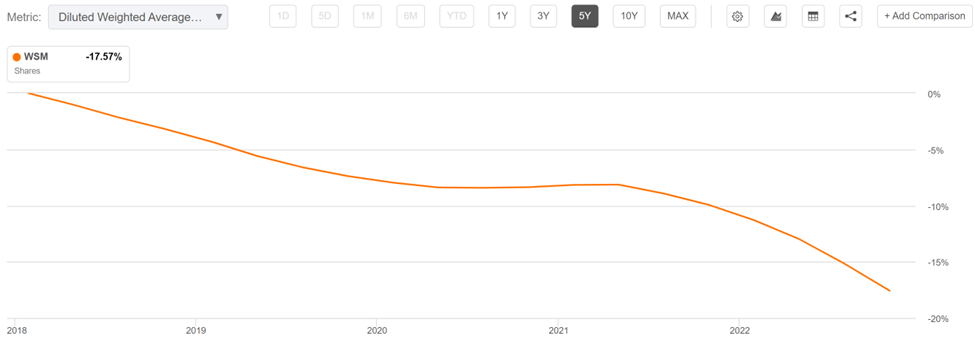

Moreover, WSM has shown a knack for dividend growth, with a 15% 5-year dividend CAGR and 16 consecutive years of growth. WSM should also be considered more of a total return story. As shown below, it's reduced its share count by 18% over the past years alone.

WSM Shares Outstanding (Seeking Alpha)

{kind=link}

While there are some companies for which share repurchases simply don't add much value due to high PE valuations, that's certainly not the case for WSM. That's because at the current price of $118, it comes with a forward PE of just 7.2, implying a 14% earnings yield for every dollar spent on share buybacks.

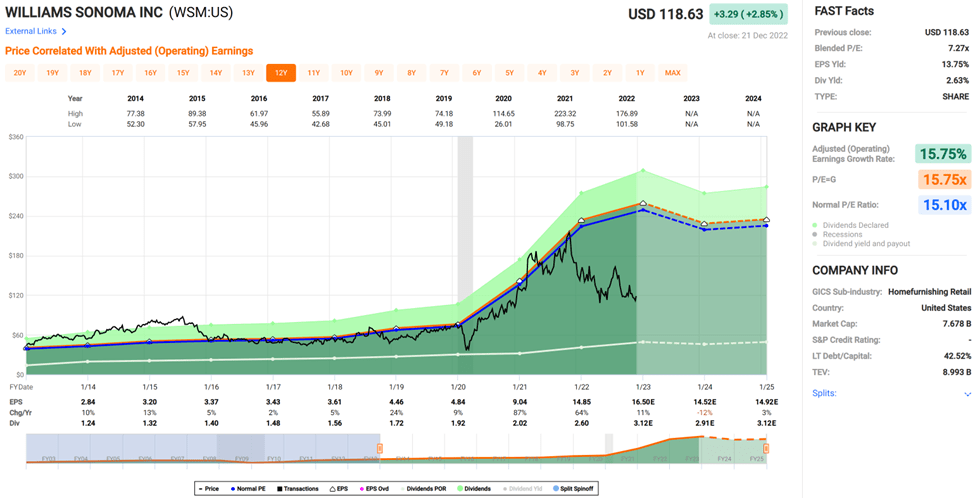

At the current valuation, WSM is also sitting materially below its normal PE of 15.1. With WSM trading at less than half of its normal valuation, I find the near term uncertainties as being way more than baked into the current price. Morningstar has a $233 fair value estimate on the stock, and analysts, which generally hold a shorter term view, have an average price target of $133. Using the latter, more conservative price target would still equate to a respectable 15% total return potential over the next year.

{kind=link}

Investor Takeaway

With a strong brand, robust analytics and proactive supply chain management, WSM has proven to be rather resilient amidst economic uncertainties. Moreover, it's well positioned for the future with a robust B2B strategy to capture fragmented markets.

While there are potential near-term economic challenges, I believe they have already been more than priced into the stock at current levels. Considering all the above, WSM could give investors potentially strong total returns from current levels.

For further details see:

Williams-Sonoma: Very Undervalued For The Long Run