DASH - Wingstop: Betting Big On A Superior Company But Not Now

2023-04-12 19:25:35 ET

Summary

- Wingstop Inc. franchises and operates restaurants.

- The company has done a fantastic job of utilizing technology and has now built the foundations for sustainable future growth.

- Wingstop's financial profile is impressive, with the business likely able to achieve an EBITDA margin of 25-27% and FCF yield of 15% long-term. This far exceeds its peers.

- Unfortunately, the business faces short-term headwinds with slowing demand.

- Wingstop is trading at an unbelievable 57x EBITDA, far above its peers. Investors would do well to remain patient as we see no upside.

Company description

Wingstop Inc. ( WING ) franchises and operates restaurants, with its key product offering being wings sauced in its various flavors.

As of December 2022 , the company has 1,959 franchised and owned restaurants in 44 states and 7 countries worldwide.

Share price

WING's share price has had a monumental rise in the 7 years, gaining over 400% in its short history. This has been driven by substantial growth in the company's brand and rapid expansion to meet ravenous demand. Unlike many of their US counterparts, the business moved early to expand its overseas presence and that is also paying dividends.

The share price has been volatile in the last few years as investors become more sensitive around valuation and whether growth can continue. We are currently close to the company's ATH, with its financial performance alone supporting this level.

Investment thesis

WING has been very popular among investors looking for "compounders" attracted by its unique characteristic of being both incredibly fast growth and profit making. This naturally comes with an expensive valuation which makes it more of a difficult decision for investors looking to buy today. If growth continues at its current trajectory, investors should not care about the current multiple as this will contract with an increase in the denominator. Equally, if growth is slowing, valuation becomes far more important.

For these reasons, the purpose of this paper is to understand where WING is going in the coming years and how they are positioned in the fast-casual industry. We will assess the current macro climate, the company's current financials, and the trends impacting the fast-food industry.

Technology and apps

One of the key trends in the fast-casual industry is the significant growth in delivery businesses such as DoorDash ( DASH) . They have changed the dynamic of how businesses operate in the industry, with consumer trends changing. Before their growth, consumers would make decisions based on their prior spending habits as it was difficult to understand what choice they have, whereas now consumers can endlessly scroll through as many options as they like.

This has been both positive and negative depending on whom you are looking at. For traditional market leaders such as McDonald's ( MCD ), this is an issue as consumers now have far more choices rather than defaulting to them. For the "far more choice" businesses, they are now able to showcase their offering and grow quickly if they have a genuinely good product.

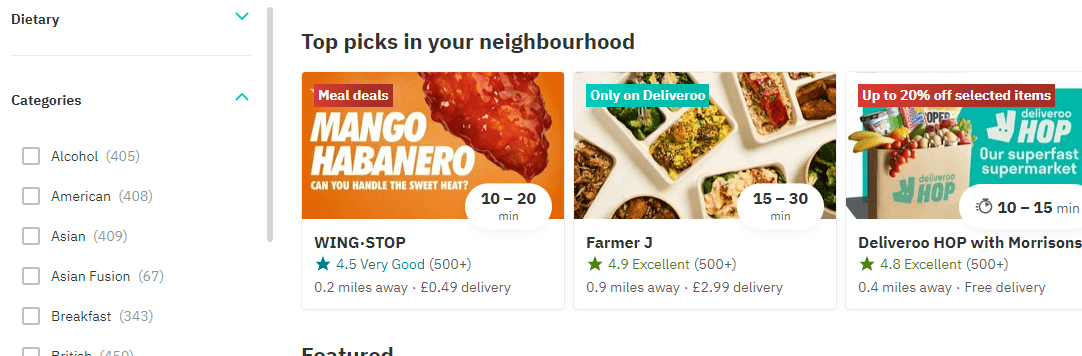

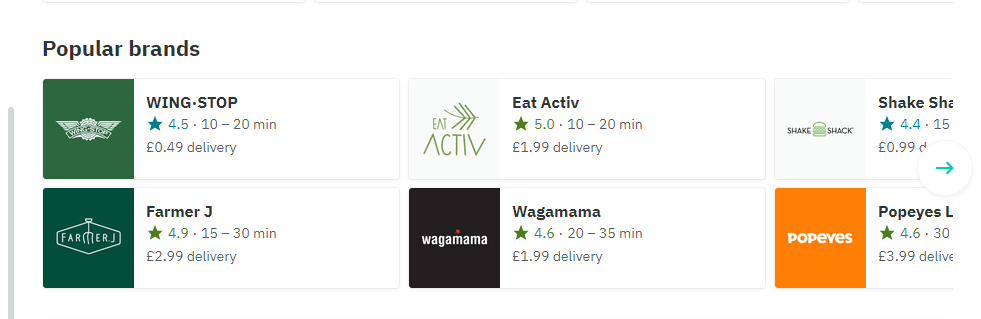

Our view is that WING falls into the second category. Here in the UK, the business has blown up in London due in part to it being easy to get on Deliveroo ( DROOF ) (DoorDash equivalent), where they offer low delivery costs to entice consumers. WING has a genuinely great product and seems to have understood that rather than fighting the delivery businesses, leaning into their rise has allowed the business to gain market share.

Wingstop on the front page of Deliveroo in London (Deliveroo) Wingstop listed first as a Popular brand (Deliveroo)

{kind=link}

{kind=link}

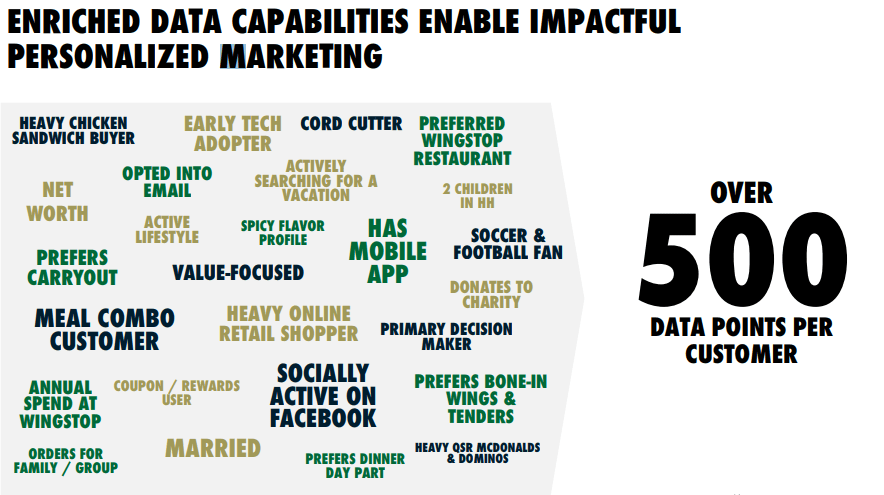

WING interestingly considers itself to be a tech-driven business, which sounds like a marketing line but is supported by how operates the business. Management is very particular about how they strategically progress the business, such as using data to personalize their engagement with customers. It would not be surprising if the business identified that exploiting its relationship with delivery businesses would help its growth.

As of today, 27% of their sales are through deliveries, intending to reach 50%+. Further, 62% of sales were through digital services overall. Recently, WING decided to drop DoorDash as their exclusive partner and begin distributing with Uber Eats too ( UBER ). This looks to be another move to further expand their potential customer base, as WING likely feels it is reaching a ceiling with DASH. This has been a shrewd move as being exclusive with DASH has allowed them to receive preferential treatment to gain market share, now with the customers gained, they can move onto the wider market.

{kind=link}

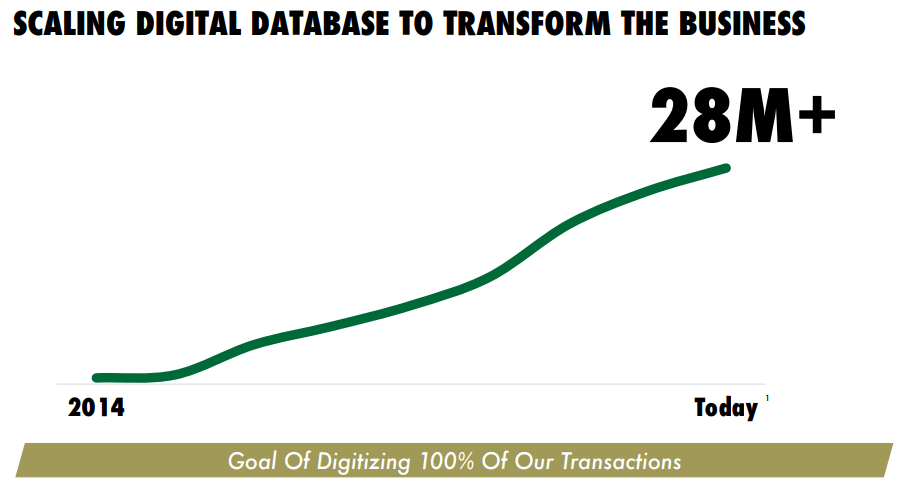

Speaking of the technological approach more generally, WING is invested in this eclipsing the current status quo. The business plan to transition 100% of its transactions to digital.

Digitization of business (Wingstop)

{kind=link}

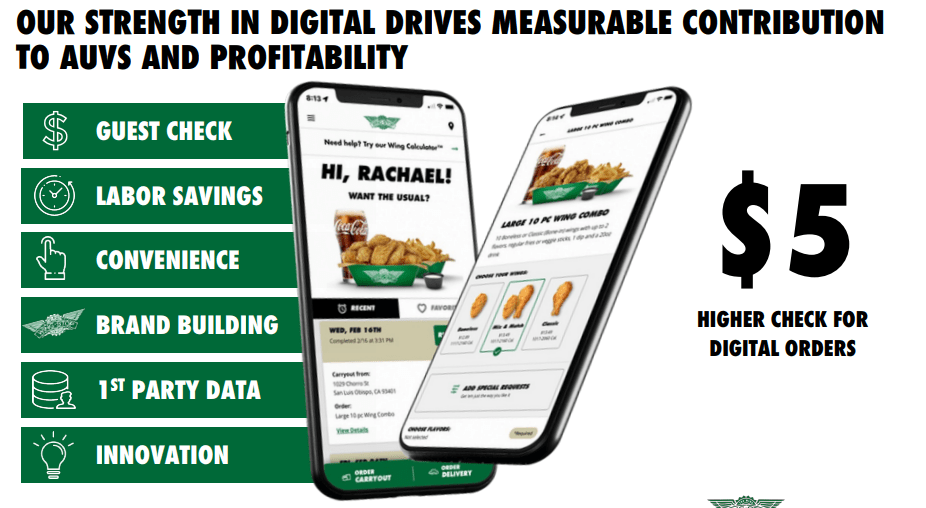

From a financial perspective, this streamlining can transition to margins, especially if the business can untether itself from the delivery businesses in the future. WING currently quantifies the digital benefit as $5, which is a substantial amount if you consider the average order size in the region of $15-$25.

Value of tech drive (Wingstop)

{kind=link}

From a commercial standpoint, we buy into what WING is doing. They are not the first to utilize digital, Domino's ( DPZ) , Subway, and Papa John's ( PZZA) all have strong digital sales. However, the difference is that these brands utilize digital as a means of executing sales and maintaining customers. They are not driving growth through this channel. With WING, investors get exposure to both the growth channel and superior economics.

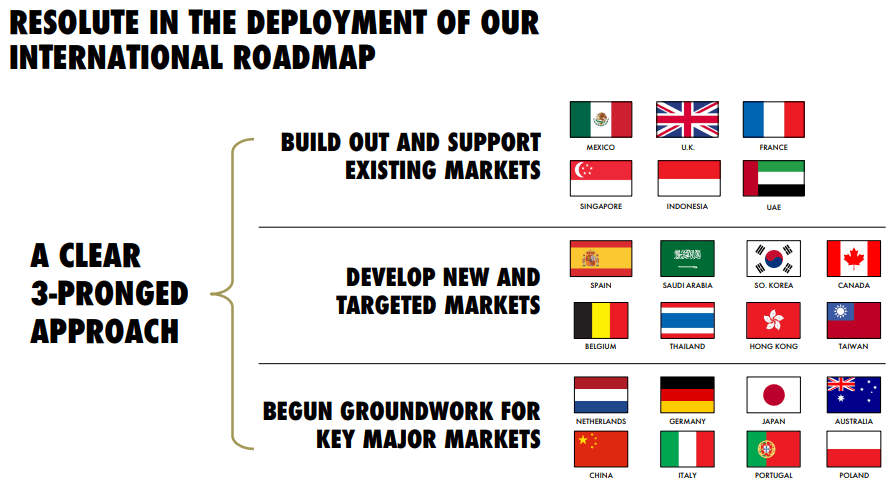

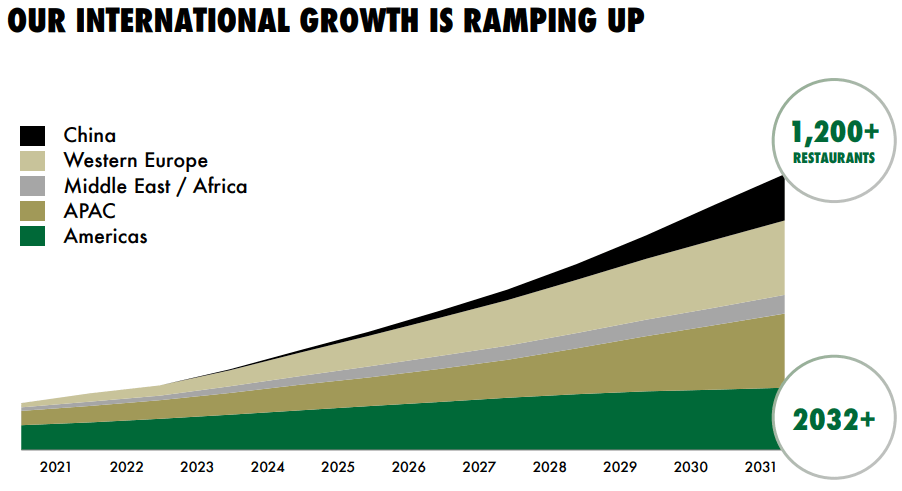

International Expansion

Unlike many of WING's peers, they have been early to expand overseas. If we look at Chipotle ( CMG ) for example, they have $8.6BN in global revenue and 13 locations in the UK. WING on the other hand has $358M in global revenue and 24 locations in the UK.

{kind=link}

Historically, this made sense as to succeed overseas required significant resources and a proof of concept in its home nation. With the power of social media and technology, it is far easier to understand your target audience and leverage your current marketing capabilities to target a new audience. The UK has seen WING, CMG, Wendy's, Popeyes, and many other US food businesses coming over in recent years for this reason. Why we think starting so early is great for WING is that it will help with maintaining their current growth trajectory, and the shared marketing capabilities are more efficiently utilized.

{kind=link}

Macro landscape

We are currently experiencing heightened inflation due to supply-side issues and historically relaxed government policy. This has been wreaking havoc on consumers' finances as living expenses increase more than wage inflation. The use of interest rates as a means of combating this is the correct decision but only acts to compound the issue for consumers. The problem for WING here is that as consumers experience a tightening of finances, they are more likely to reduce unnecessary spending / find areas to cut back, which in many cases includes eating out. Generally, it is cheaper to cook and eat in, with consumers seeing eating out as more of a luxury. This could contribute to a reduction in fast-casual spending and we do not see how a company could remain resilient against this.

Looking ahead, we forecast that things remain as they are for most of the year, if not worsen. Inflation only marginally dipped in Jan23, suggesting rates may need to increase further to bring it below 4%. This could trigger a recession or bring growth to a standstill. Our view is that WING should maintain growth but at a far lower level than historically achieved, as the rapid expansion of locations will drive revenue. Same-store sales will be closer to market levels.

Readers must remember that this is only theory, economies can very much surprise. The recent announcement of retail spending picking up is one such example, with the February restaurant survey showing robust demand also.

Commodity prices

Historically, the cost of commodities remained relatively flat as part of production costs. With supply-chain issues in mind, we have seen a rise in the cost of many commodities, including chickens. As the below graphs illustrate, the cost of feed and chickens has increased substantially in recent months and remains elevated.

This has the potential to contract WING's margins in the short term as their franchises are less profitable, potentially causing stagnation in the company's profits even if revenue grows. Between FY22 and FY21, WING GPM margin declined 2.1%, suggesting the impact has not been significant.

Having said this, we are seeing a relative stabilization in many commodities and some are even trending down. WING has stated that the cost of bone-in chicken wings has declined in Q4. We have likely seen the worst of the supply-side issues. Therefore, we consider this a short-term headwind, with margins likely to improve from 2024 onwards.

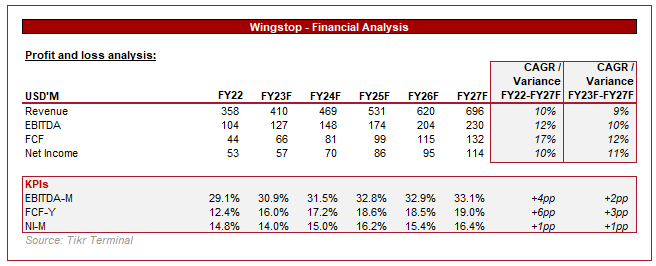

Financials

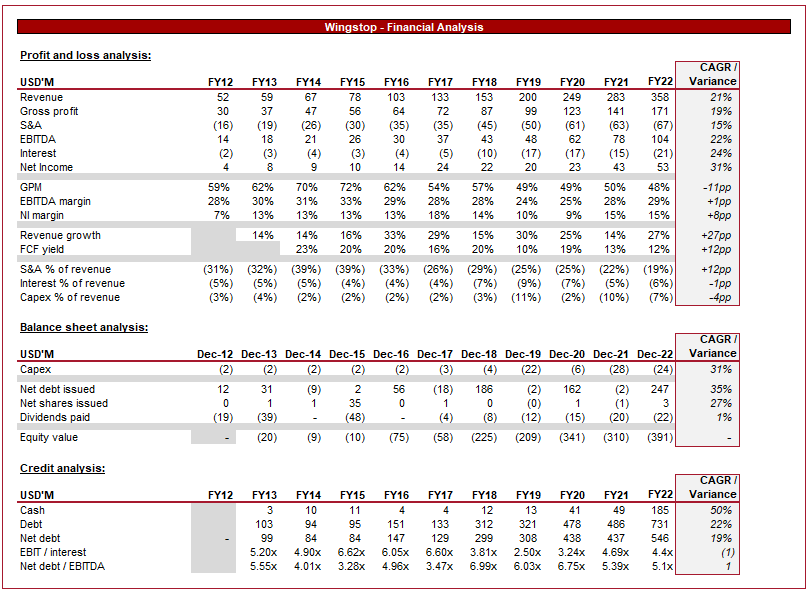

Wingstop financials (Tikr Terminal)

{kind=link}

As we have mentioned previously, WING has grown quickly in the last decade and has been able to maintain profitability by doing so.

Revenue has grown at a CAGR of 21% across the historical period, picking up significantly in the second half of the decade. This has been driven by its prior efforts to grow the brand, with momentum picking up as consumers buy into the product. Despite this, sales have slowed in the most recent period, suggesting economic conditions are beginning to bite. This is concerning as the business is still opening a considerable number of restaurants and so even if demand is slowing, one would expect their ramp-up toward maturity would drive revenue.

Further, we see the impact of production costs increasing, with GPM declining. Regardless, the business is impressively profitable across the board. Margins have been ticking down in recent years but this is due to the business increasing its investment in growth, particularly marketing spend and Depreciation. Our view is that the business can normalize at an EBITDA margin level above 25%.

WING's FCF yield has declined compared to prior years as a result of recent capex expenditure. Before this, the business has consistently achieved over 15%. Assuming regular ongoing capex to fund growth, the business will likely normalize in the mid-to-high teens.

Moving onto the balance sheet, WING has seen its debt balance grow as it funds its expansion. Although the business is FCF positive, it does not generate enough cash to sustain growth, therefore further debt is likely assuming EBITDA is still growing. EBIT/Interest has fallen to 4.4x and so the business does need to be careful with how it raises debt, especially in this environment. We could see the business hold off until rates become more attractive.

From a financial perspective, we also see the hype. The business has the characteristics to be incredibly profitable while having the de-risked nature of the franchise model.

Outlook

Wingstop outlook (Tikr Terminal)

{kind=link}

Management is currently forecasting mid-single-digit growth in the 3-5 years, with higher annual unit growth as locations increase. Analysts concur with this assessment, forecasting 10% total growth. They do, however, expect a rapid improvement in margins. Our view would be that this is certainly possible, but as soon as FY24 is slightly optimistic given that management should still be focused on driving growth.

Relative performance

Relative performance (TIkr Terminal)

Presented above is a cohort of franchise-led food businesses.

We observe impressive profitability from the businesses and good growth. WING outperforms them all across all relevant metrics. We care less about FCF as WING is far more sensitive to capex spending compared to the others. On an EBITDA and GPM level, the business significantly outperforms. Growth is as we would expect as without Chipotle, WING is almost double the average.

Valuation

So far this paper has been showering praise on WING, a seemingly revolutionary business. A great business is great regardless of valuation but sometimes the cost already reflects the future greatness you are buying. In WING's case, there may actually be value for investors.

Valuation (Tikr Terminal)

In the case of WING, the business is trading at an eyewatering 57x LTM EBITDA. This is almost triple that of our cohort's average. Investors are pricing in a bright future for the business and are seemingly sure of it.

Our view is that WING must be considered with a medium term lens, due to its rapid growth. Our current fair value is 57x EBITDA, slightly below the consensus Wall Street view. This sounds crazy but our commercial view in conjunction with the follow financial analysis supports this. We have derived the 57x EBITDA valuation based on the following steps.

- Assuming WING can sustainably reach the profitability profile we are forecasting (EBITDA margin of 25-27% and FCF-Y of 15%) alongside the growth achieved by a mature business such as Domino's, we believe a 30x EBITDA multiple is fair. Chipotle has shown trading evidence that its inferior margins to this can justify a c.30x multiple.

- Our EBITDA growth assumption is slightly more conservative than analysts, expecting FY27 to be $178M rather than $230M.

- Should this play out, Wingstop would be valued at 31x EBITDA in 5 years, 28x in 6 years, and 25x in 7 years based on today's enterprise value.

Therefore, based on our 5-year view of the business, a 57x multiple today equals 30x in 5 years' time.

Beyond 6 years is where the real value will be for investors and so this company must be looked at with a long-term trend. The nature of this industry is that more locations can keep growth going as long as there is a market to reach. WING is still small when it comes to reach and so our concerns around achievability are far lower than for companies in other industries.

Final thoughts

We do not actually think WING has reinvented the wheel, but the business has done a fantastic job of building a superior business model in a mature industry. The company is far more profitable than its peers and is seemingly ahead of the game. The company now has a large stable customer base and is expanding its marketing reach. Our view is that the next decade will be similarly impressive as the one just gone.

However, the business is facing short-term headwinds, and noticeable ones at that. Demand looks to be slowing and it is difficult to judge how difficult 2023 will be for trading. The top line will be supported by new location growth, which should mean the company is insulated.

WING's valuation is a big problem, however. Although WING stock is performing impressively, it inevitably faces the risk of slow-downs and problems along the way. With a valuation this high, the execution risk is far above usual, but our view is that the 5-10 year return reflects this, but with no upside today. Investors looking for a high-risk, high-reward play could do well looking into WING further. For most, however, looking to pick up the stock cheap in the coming year looks to be a fantastic opportunity... if it presents itself.

For further details see:

Wingstop: Betting Big On A Superior Company But Not Now