CA - With A 7.5% Yield And An Upcoming Spinoff TC Energy Is Attractive

2023-11-07 19:48:54 ET

Summary

- TC Energy is an attractive investment opportunity in the energy sector, with the spinoff and reorganization offering potential for high-yield stocks.

- The company's fundamentals, including revenue and EBITDA growth, make it a solid dividend growth stock with a track record of consecutive increases.

- TC Energy's focus on natural gas, electricity, and hydrogen presents growth opportunities, and its diversification across the energy value chain reduces risk.

Introduction

As a dividend growth investor, I seek new investment opportunities in income-producing assets. I often add to my existing positions when I find them attractive. I also use market volatility to my advantage by starting new positions to diversify my holdings and increase my dividend income for less capital. The current interest rates allow dividend growth investors to find more high-yield opportunities.

The energy sector is attractive, and TC Energy ( TRP ) is exciting due to the high yield and the broad market decline. The energy sector has enjoyed a rally since the end of the pandemic and the war in Ukraine. Companies enjoyed higher profits, resulting in more cash and higher resilience. The higher rates that have affected the share price negatively may offer an opportunity for investors seeking high-yield stocks. Two years ago, in 2021, I analyzed the company and found it to be a HOLD. The shares offered a decent yield, but the valuation was not attractive enough.

I will analyze TC Energy using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company's fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it's a good investment.

Seeking Alpha's company overview shows that:

TC Energy operates as an energy infrastructure company in North America. It operates through five segments: Canadian Natural Gas Pipelines, U.S. Natural Gas Pipelines, Mexico Natural Gas Pipelines, Liquids Pipelines, and Power and Energy Solutions. The company builds and operates a network of 93,700 kilometers of natural gas pipelines, which transports natural gas from supply basins to local distribution companies, power generation plants, industrial facilities, interconnecting pipelines, LNG export terminals, and other businesses. It also has regulated natural gas storage facilities with a total working gas capacity of 532 BCF. In addition, it has approximately 4,900 kilometers of liquids pipeline system that connects Alberta crude oil pipeline to refining markets in Illinois, Oklahoma, and Texas. Further, the company owns or has interests in seven power generation facilities with a combined capacity of approximately 4,300 megawatts.

Fundamentals

Revenues of TC Energy have increased by 36% over the last decade. It equates to roughly 3% per year. The company constantly builds new projects and sells less lucrative ones to improve cash generation. The company increases sales by getting more projects online and by increasing the prices of new contracts. In the future, as seen on Seeking Alpha, the analyst consensus expects TC Energy to keep growing sales at an annual rate of ~3% in the medium term.

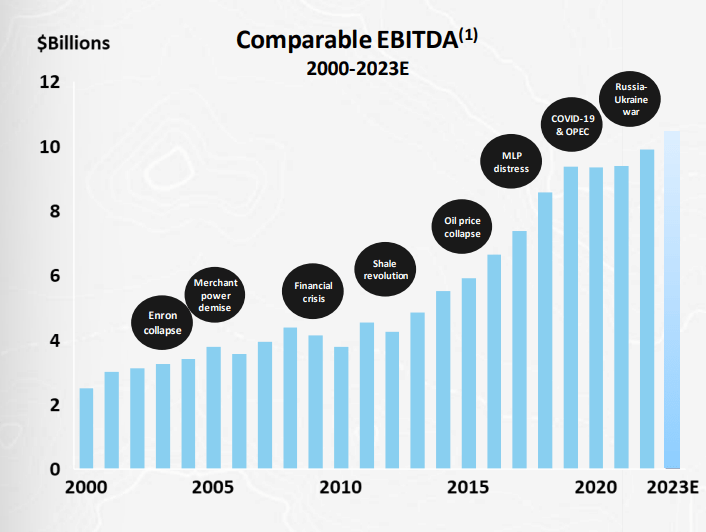

The company is enjoying a growing EBITDA over the same decade. While the sales grew by 36%, the EBITDA more than doubled. This is the result of improved margins together with sales increases. As a pipeline company, the classic EPS (earnings per share) measure is less useful as it constantly invests, and the depreciation and amortization make it harder to understand the underlying financial situation. In the future, as seen in TC Energy's Q2 results, it is expected to keep growing its adjusted EBITDA by 7% annually between 2022 and 2026.

{kind=link}

The company is a devoted dividend payer on its way to becoming a dividend aristocrat. It has a track record of 23 consecutive increases with a CAGR of 7%. The company maintains a conservative FFO payout of 51%, making this 7.5% dividend yield likely sustainable. The company aims to increase that generous yield by 3-5% annually, according to its Q2 2023 results. Thus, investors can achieve a decent payout with higher than inflation increases.

In addition to the dividend, companies tend to return capital via buybacks to support EPS and FFO per share growth. In the case of TC Energy, we see the opposite as the company has increased the number of shares by 41% over the last decade. The shares are issued to fund the growth projects, yet they dilute shareholders. Since the company constantly invests in new projects, it will likely keep issuing shares long-term. However, post-spinoff, the liquid pipelines company, which will be less of a growth company, aims to execute buybacks.

Valuation

The company's P/E, when using the forecasted EPS of 2023, stands at 12.18. Paying 12 times earnings for a growing company with a long track record is reasonable. When using the FFO multiple, the multiple stands at 6.8. Investors should consider that companies like TC Energy are usually leveraged, and their growth is often regulated. Therefore, the companies tend to have a lower P/E ratio.

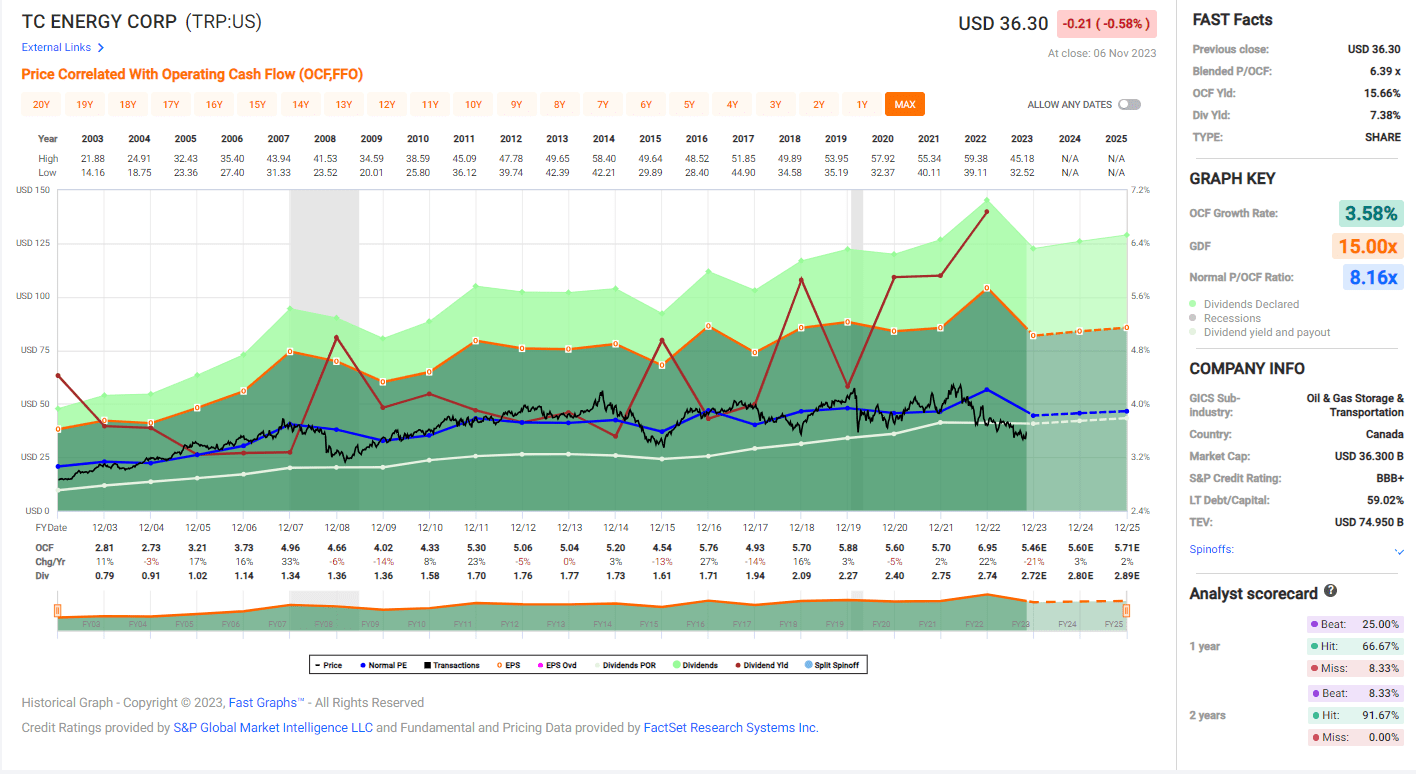

The graph below from Fast Graphs shows that the company is now attractive. The company's P/FFO stands at 6.4 compared to the average P/FFO of 8.2 over the last decade. Moreover, the company forecasts that it will be able to grow at a 7% annual growth rate, more than double the historical growth rate of 3.6%. The fair valuation of the company in the current business environment is a share price of $40-$42. It implies a price to FFO of ~8. Therefore, I believe that the shares of TC Energy are attractively valued today.

{kind=link}

Opportunities

The company's strategic spinoff of its liquid pipeline business is critical and positive. Currently, TC Energy has five business segments: Canadian Natural Gas Pipelines, U.S. Natural Gas Pipelines, Mexico Natural Gas Pipelines, Liquids Pipelines, and Power and Energy Solutions. In its reorganization and spinoff, it will merge the American, Mexican, and Canadian segments and spinoff its liquids pipelines segment into a new company.

By distancing itself from the oil industry, which faces long-term challenges, TC Energy is positioning itself to concentrate on the more resilient and sustainable segments of the energy sector, including natural gas and electricity. With the increasing importance of natural gas as a cleaner energy source and the expanding role of electricity in the American energy landscape, TC Energy's focus on these areas aligns with the evolving energy market.

TC Energy

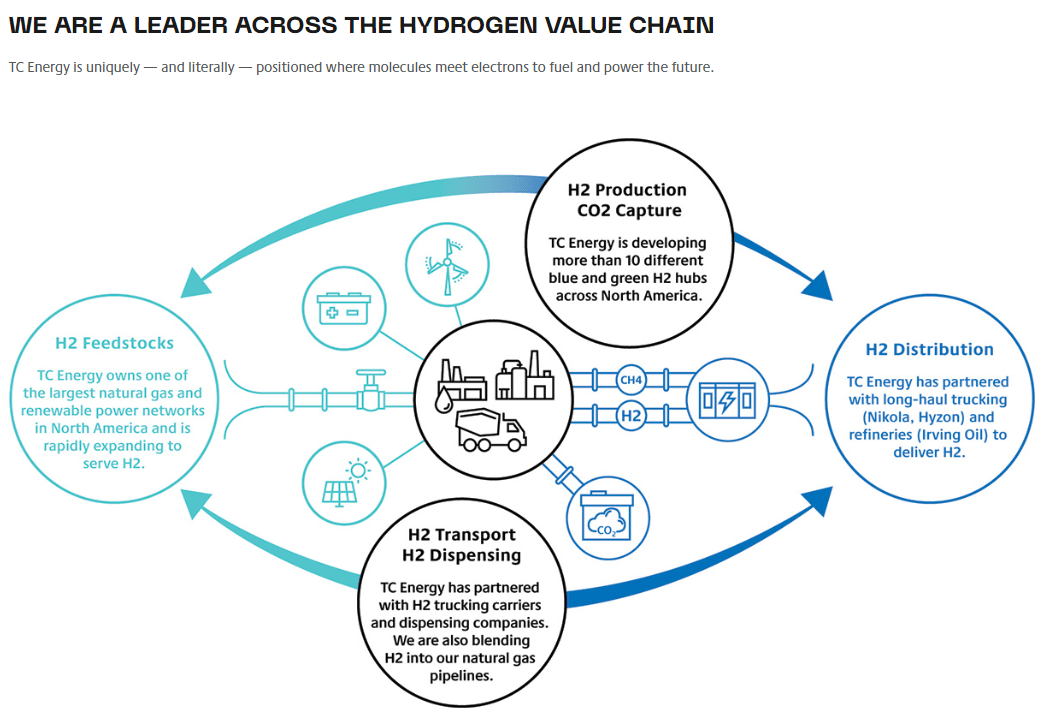

Moreover, TC Energy's commitment to hydrogen presents an exciting opportunity. The company is already investing in hydrogen facilities, and its extensive pipeline network is well-suited to adapt for hydrogen transportation, especially blue hydrogen production, which utilizes natural gas- its strategic focus. As the energy industry explores hydrogen as a cleaner fuel source and energy carrier, TC Energy's involvement positions it to benefit from the growing interest in hydrogen-related projects.

{kind=link}

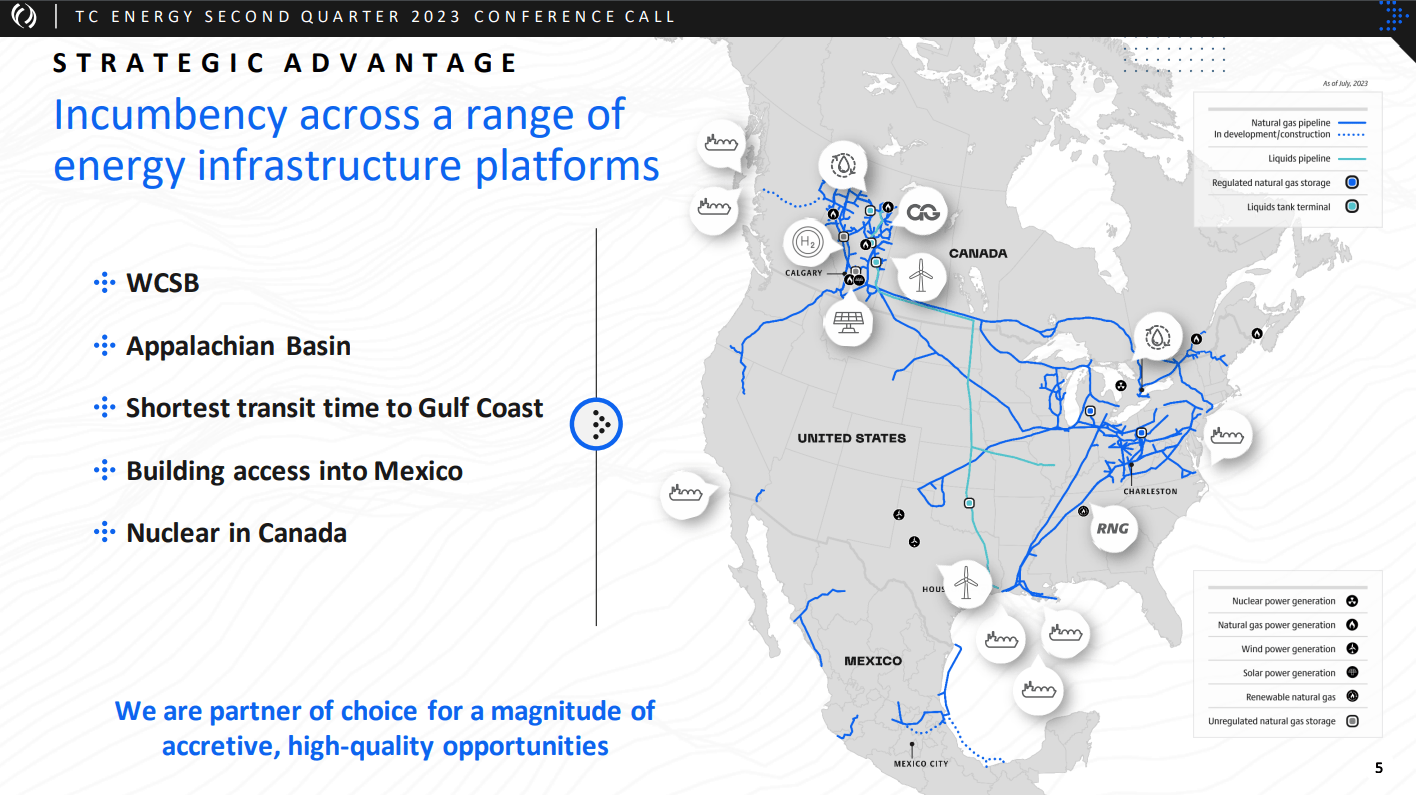

TC Energy's diversification across the entire energy value chain is another key advantage. The company operates in multiple segments, including gas transportation, storage, power generation, and hydrogen production. This broad footprint allows it to weather fluctuations in different energy markets, reduce risk, and maintain a steady income stream. It provides investors with a well-rounded and resilient investment option with assets across the value chain.

{kind=link}

Risks

The investment thesis has several risks. Firstly, the weak growth prospects in the liquid pipeline business post-spinoff pose a notable concern. With an annual growth rate projected at only 2-3% according to the company's Q2 2023 results, this segment may not be particularly attractive for investors seeking robust revenue and earnings expansion. The sluggish growth in liquids could potentially hinder the company's overall financial performance and limit its ability to generate higher shareholder returns . This risk can be avoided following the spinoff by selling the new business.

In addition, the negative free cash flow is another risk to consider. TC Energy's investments require capital, resulting in negative free cash flow. To fund these investments, the company may resort to options like stock issuance at a relatively high dividend yield of 7.5% or further debt accumulation. Such financial maneuvers can place additional pressure on the company's balance sheet, impacting its ability to manage its obligations effectively and potentially affecting its dividend sustainability .

Lastly, TC Energy's high leverage, as evidenced by a debt-to-EBITDA ratio already exceeding 8, is a substantial concern. The higher cost of borrowing, exacerbated by rising interest rates, can make it increasingly challenging for the company to finance its growth initiatives through debt. The elevated debt levels may limit the company's financial flexibility, potentially leading to more conservative growth strategies or dilution for existing shareholders if TC Energy needs to raise equity capital. This increased financial risk is a critical factor for investors to weigh when considering an investment in the company .

Conclusions

To conclude, while some pipeline companies tend to be highly cyclical regarding returns, TC Energy is a leading blue chip. The company has solid fundamentals, with revenues and EBITDA growing and leading to a relatively increasing dividend. The company has attractive growth opportunities, mainly around natural gas and hydrogen as its byproduct.

Moreover, the company is trading for an attractive valuation. The valuation is attractive when considering the risks as well. The leverage may slow down the growth, but at the current valuation, this is still an attractive proposition. Therefore, I believe that the shares of TC Energy are not a HOLD anymore, and I change my ratings to a BUY. The better valuation and a higher yield, together with the spinoff that will accelerate growth, justify the rating change. Investors can lock on a 7.5% yield with decent growth opportunities, limited risks, and an attractive valuation.

For further details see:

With A 7.5% Yield, And An Upcoming Spinoff, TC Energy Is Attractive