LHX - With Significant Potential L3Harris Remains My Favorite Deep Value Dividend Stock

2023-11-19 22:25:01 ET

Summary

- I'm putting a heavy focus on aerospace, defense, and REITs, with a keen interest in key players like Lockheed Martin, Northrop Grumman, RTX Corp., and L3Harris Technologies.

- Due to global tensions, defense stocks, including L3Harris, are holding strong. The company's solid performance, diverse segments, and smart moves in the space industry are contributing to its resilience.

- L3Harris looks promising with robust financials, improving margins, a healthy order book, and a diverse business portfolio.

- Strategic moves, like the Aerojet Rocketdyne merger, position it as a top-tier defense investment with solid long-term potential.

Introduction

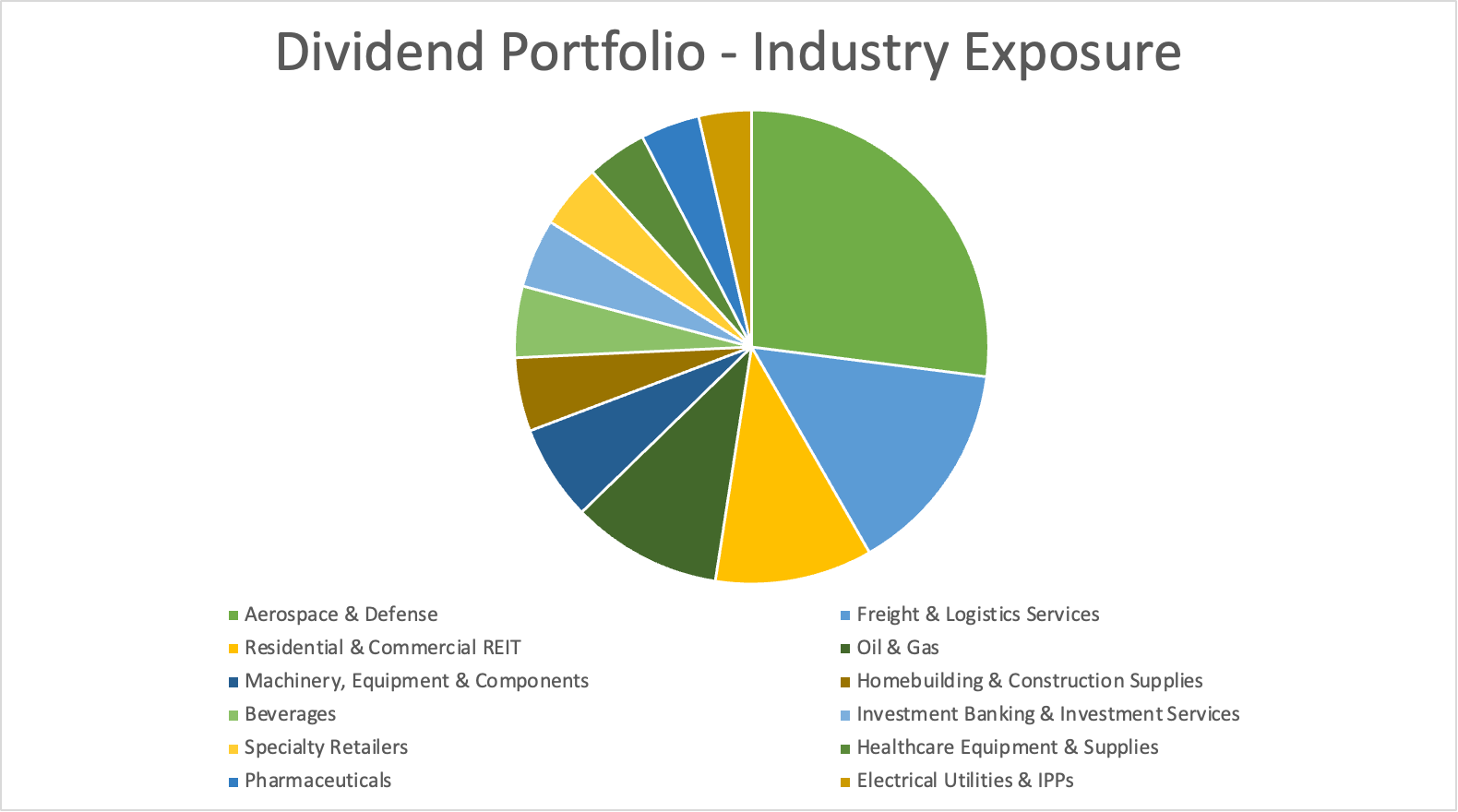

When it comes to long-term investing, I've clear favorites. Although I try to keep a balanced portfolio, I am significantly overweight three industries: aerospace & defense, freight & logistics (railroads), and REITs (self-storage).

Leo Nelissen (Dividend Growth Portfolio)

{kind=link}

Energy is also an industry I'm overweight when adding the exposure I have in my trading account.

This year, I went massively overweight in defense contractors. It has always been a large industry in my portfolio. However, this year, I've been an aggressive buyer of all of my defense investments, as ongoing supply chain issues, funding issues, and macroeconomic woes have caused most of them to perform poorly - at least in the first two quarters of this year.

Defense contractors now account for more than a quarter of my dividend growth portfolio.

As a matter of fact, all four of my defense investments are in my top five. My entire top 5 consists of industrial companies.

I own (in this order):

- Lockheed Martin ( LMT )

- Northrop Grumman ( NOC )

- RTX Corp. ( RTX ) - formerly known as Raytheon Technologies

- L3Harris Technologies ( LHX ) - the star of this article.

With that said, last month, the Wall Street Journal wrote an article focused on the performance of the nation's largest defense contractors.

{kind=link}

According to the Journal, major defense contractors, including Lockheed Martin, General Dynamics ( GD ), and BAE Systems ( BAESY ), have seen a significant uptick in their stock prices, reflecting a heightened perception of geopolitical risk stemming from the recent attack on Israel.

While localized conflicts historically provide short-term boosts to defense stocks, lasting gains need regional expansions and shifts in global politics.

The current conflict raises questions about the possibility of Israel facing a multi-front war, especially if Hezbollah militias in Lebanon escalate their involvement.

Although I'm not going to predict what may or may not happen in the ongoing Israel war, we see that defense contractors have lost momentum already, suggesting that we may not be dealing with a major conflict, which is obviously a good thing.

The Journal notes the same with regard to the war in Ukraine.

Despite geopolitical tensions with China and Russia, defense stocks haven't provided a clear indication of an increasingly perilous global situation.

Since the invasion of Ukraine, these stocks have outperformed the S&P 500 but without a noticeable premium on valuations.

This brings me back to what I always say: I do not buy defense contractors because I'm betting on a war - let alone hoping for war.

I believe that defense companies benefit from their ability to innovate, creating defense solutions that prevent war and keep defense capabilities up-to-date.

Generally speaking, this means long-term growth in orders - often with barely any cyclical characteristics. If anything, defense spending tends to pick up during recessions, as defense investments are a great way to keep manufacturing output going.

Looking at the chart above, we see that LHX is the worst-performing defense contractor in the United States.

Over the past three years, LHX is down 5%, excluding dividends, which is an abysmal performance.

However, it's great news for investors like me who aren't done buying LHX.

On September 6, I wrote an article titled Up To 50% Undervalued - Why L3Harris Has Become My Favorite Dividend Growth Stock .

Since then, the company has rallied 8.3%, including dividends, beating the S&P 500 by almost 800 basis points.

I'm now breakeven again on my LHX investment (excluding dividends), as I have been an aggressive buyer on weakness this year.

In this article, I'll elaborate on my call, update my view, and explain why the company is still my go-to stock for deep value and top-tier dividend growth capabilities.

The company also reported its 3Q23 earnings since my prior article was released, which tells us a lot about its progress.

So, let's get to it!

Growth Despite Demand Uncertainty

Below is a part of the takeaway from my prior article. I added some emphasis.

My decision to increase my investment in L3Harris Technologies by 55% is driven by a belief that the market is undervaluing this powerhouse of a company. While there are challenges, such as inflation concerns and supply chain issues , LHX's strong performance, diversified business segments, and strategic moves in the space industry make it a compelling choice.

The space sector, in particular, holds enormous potential, and LHX's acquisition of Aerojet Rocketdyne positions it as a key player. With a favorable outlook for defense spending in this arena , LHX is well-prepared to capitalize on these opportunities.

So far, everything is going according to plan.

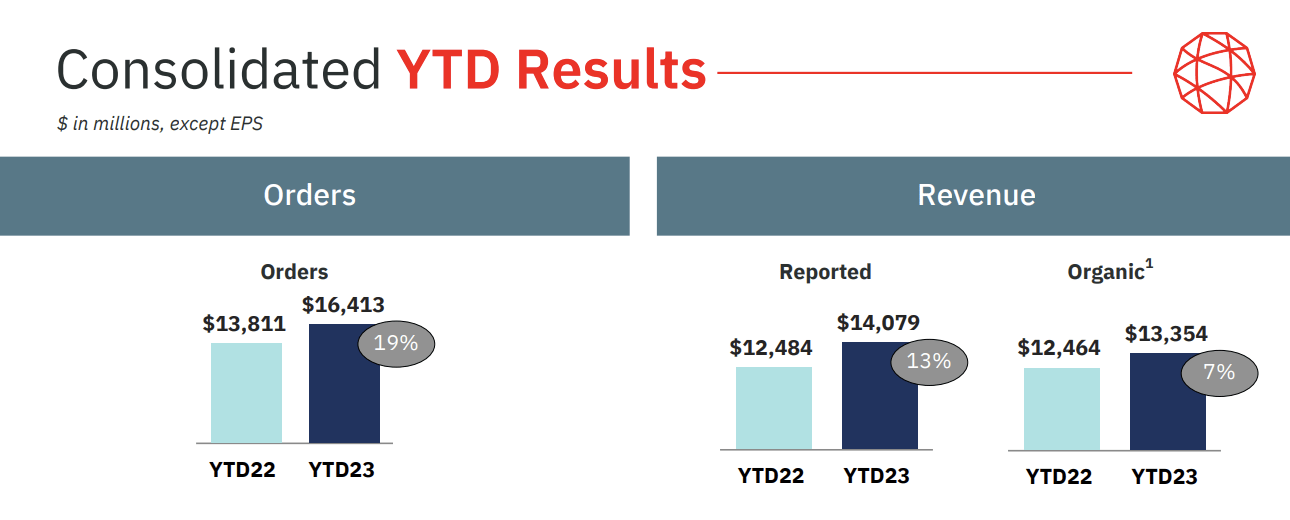

For example, on October 26, the company reported its 2Q23 earnings. Total revenue came in at $4.92 billion, beating estimates by $50 million.

Top-line growth was 16%.

Organic revenue was up 3%, which excludes the impact of recent mergers.

Adjusted EPS came in at $3.19, $0.16 higher than analysts expected.

The third quarter marked a second consecutive quarter of sequential margin improvement and strong cash generation, resulting in over 100% free cash flow conversion.

The company has consistently generated positive free cash flow in each quarter since the merger of L3 and Harris.

While these numbers tell us that the company is performing better than analysts expected, we need to dig deeper to find out how LHX is really doing.

For starters, the third quarter showed strong orders. LHX got $5.0 billion in new orders, which brings the fully-funded book-to-bill ratio to 1.02x. Although some peers have higher ratios, the company is seeing favorable trends in demand.

- 3Q23 orders were down 1%.

- YTD orders are up 19% to $16.4 billion.

Hence, when ignoring short-term noise, it has a year-to-date fully funded book-to-bill ratio of 1.17x, indicating that it gets $1.17 in new business for every $1.00 in finished work.

{kind=link}

Regarding its demand environment, the company noted challenging developments, as prolonged Continuing Resolutions ("CR") are likely.

Quantifying the potential impact of an extended CR remains challenging at this time. The company is closely monitoring developments in Congress. While the GFY24 budget still needs to go to conference, it is worth noting that a consensus appears to be forming around the President's budget request at $842 billion.

[...] Now, following the attacks in Israel, the White House and Congress may consider providing funding for both countries via a supplemental measure or via separate pieces of legislation, either of which could be addressed separately from broader GFY24 budget negotiations. - LHX 3Q23 Investor Letter

In other words, funding growth uncertainties remain an issue. However, global developments pressure Washington to boost spending.

Furthermore, one major benefit of LHX is its well-diversified business portfolio, which focuses on issues that require more funding than other areas. This allows it to grow despite overall funding uncertainty.

Within the Future Years Defense Program (FYDP), investment accounts are growing at approximately 1% on an annualized basis. However, L3Harris remains differentiated from its peers with a national security, technology-focused portfolio, and well positioned within key growth domains, namely space (up ~5% CAGR) and missiles & munitions (up ~5% CAGR). Classified DoD budgets are also up over the FYDP, while other domains remain flat to down slightly. - LHX 3Q23 Investor Letter

Based on this context, demand developments are tied to margins, as there's a lot to take into account in light of inflation and supply chain challenges.

Inflation, Supply Chains & Cost Benefits

During the 3Q23 earnings call, the company CEO, Chris Kubasik, provided insights into the Space business.

The portfolio comprises a mix of fixed price and cost-plus contracts, with a shift towards a 50-50 distribution over the last decade.

Challenges in the industry, particularly in the supply chain, have evolved, impacting both short-cycle and longer-cycle businesses. Challenges include supply chain issues related to inflation and labor.

L3Harris continues to see positive trends driven by supply chain resiliency initiatives. However, full supply chain recovery remains uneven. The company continues to work closely with suppliers to mitigate future potential impacts, and has been successful in mitigating most of these challenges to manage the evolving 'new normal' in supply chain operations. - LHX 3Q23 Investor Letter

Furthermore, with regard to inflation and new orders growth, the company emphasizes bidding discipline, learning from past challenges in estimating and delivering products.

Kubasik highlighted the importance of not bidding on fixed-price development programs simultaneously requiring development and production commitments.

The focus is on protecting profitability, cash, and margin, even if it means sacrificing top-line growth.

As a result, the company undergoes regular independent reviews of key programs to identify and address risks early.

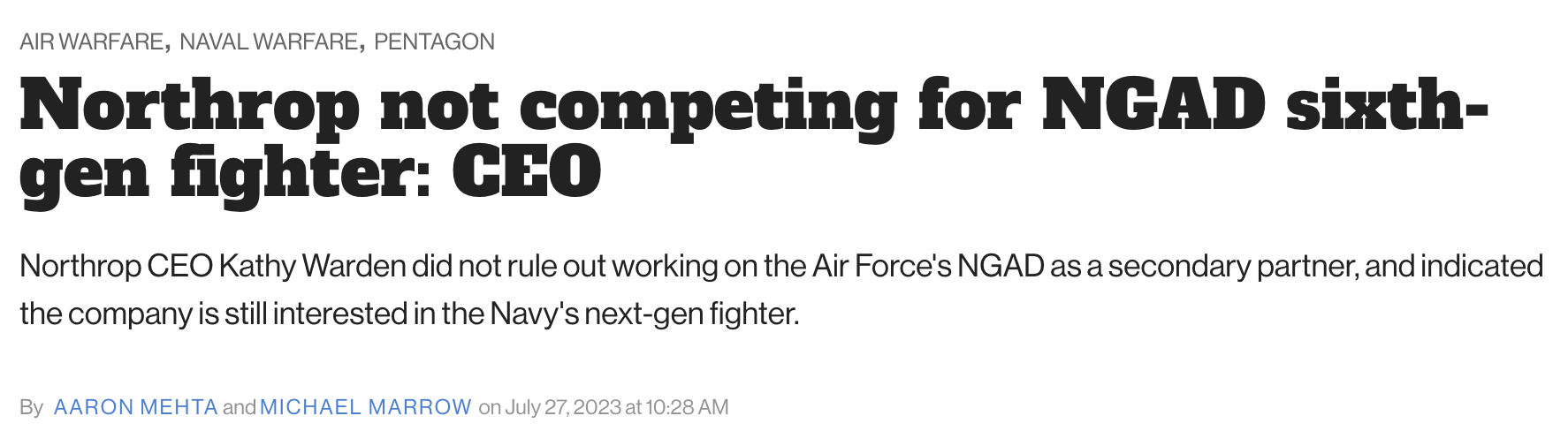

This is happening in the entire industry. I also believe that this is the reason why Northrop Grumman quit bidding for the contract of being the contractor of the next-generation fighter jet.

{kind=link}

I think L3Harris is applying a smart strategy. Top-line growth isn't the issue. Pressure on margins is what scares investors.

Also, if all contractors shift their focus on margins, the government will be forced to change the way they structure new contracts. I believe this could be more efficient for all parties and cut waste.

With that said, the merger with Aerojet Rocketdyne is going smoothly.

The company plans to maintain its annual CapEx in the range of $50-60 million for Aerojet Rocketdyne, considering it as part of the overall investment target.

It also has an LHX NeXt plan.

This initiative focuses on leveraging scale to drive efficiencies and optimize functional organization for value creation.

During its earnings call, the company mentioned an anticipated $400 million investment for the next phase of this program, with examples of early successes in renegotiating employee benefit packages and streamlining communication workflows.

Ultimately, net of reinvestment back in the business, LHX NeXt is anticipated to provide tailwind opportunity for margin expansion over the next three years. During our Investor Day in December, management will provide additional information about how these savings will strengthen the company's future financial profile. - LHX 3Q23 Investor Letter

L3Harris is also making progress with regard to its balance sheet.

The target is to bring the debt down to $13 billion by the end of the year, with a leverage ratio goal of 3.5x, which is expected to go below 3 in the next few years.

A 3.5x leverage ratio after aggressive M&A is a great number. LHX maintains a BBB credit rating, which I expect to be boosted to BBB+ once it hits its leverage target.

Also, the company's expectations seem to be conservative, as analysts expect the company to end 2024 with a 2.9x leverage ratio, which would mean that it can accelerate dividend growth and buybacks in early 2025 - unless it encounters severe headwinds that derail its cash flow outlook.

Since its merger in June 2019, the company has bought back 15% of its shares. The dividend has been raised by more than 50%, with aggressive double-digit hikes in the first years after the merger.

Once LHX was done selling non-core assets, it shifted its focus to buying new assets, like Aerojet, which requires a focus on debt reduction over shareholder distribution growth.

As much as I like dividend growth, I believe this strategy is great.

If everything goes right, two years from now, investors will have stock in a top-tier defense giant with disrupting qualities and the ability to accelerate dividend growth and buybacks.

- The current dividend yield is 2.5%, which isn't half bad!

- The dividend is protected by a sub-40% payout ratio.

Valuation

Even after its recent rally, the stock offers deep value.

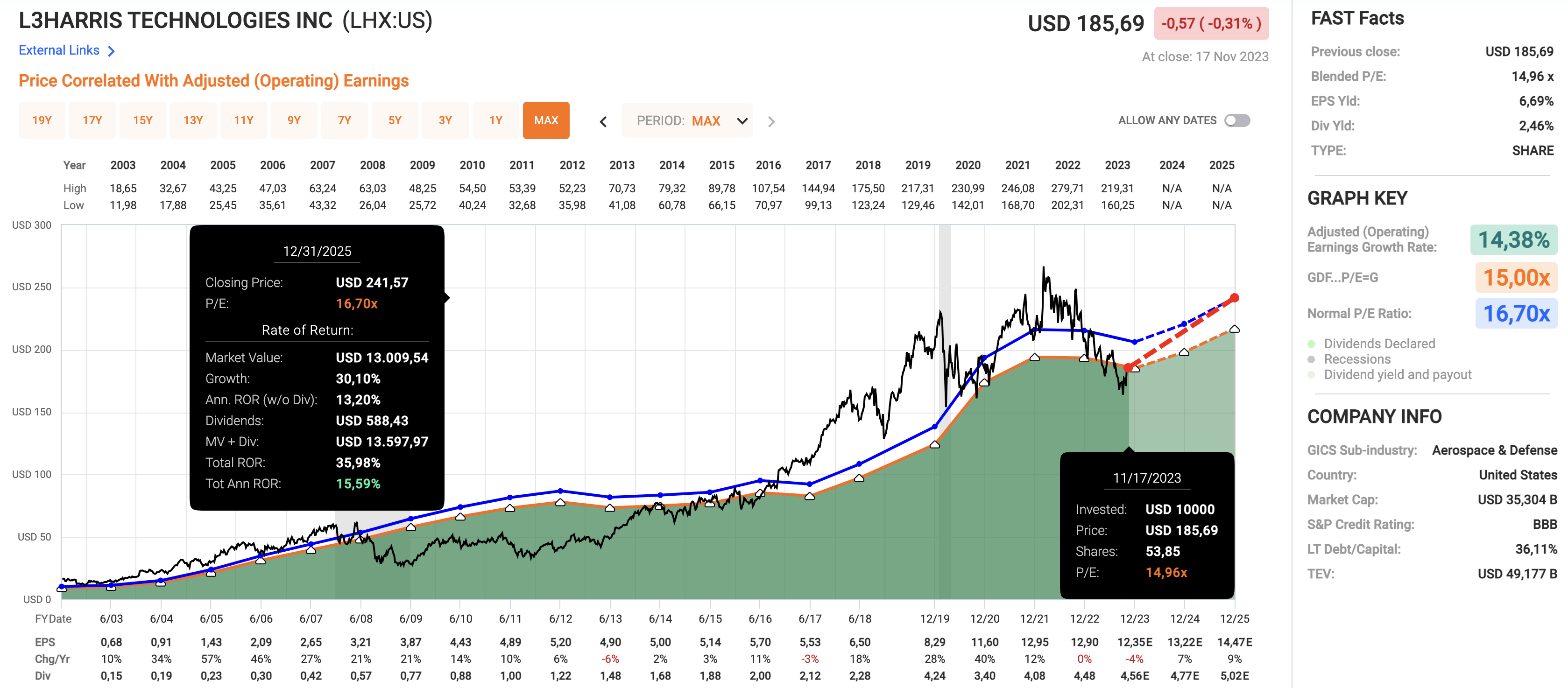

Using the data in the chart below:

- LHX is trading at a blended P/E ratio of 15.0x.

- Going back 20 years (roughly 16 years of this are L3 as a standalone company), the company has traded at a normalized P/E ratio of 16.7x.

- This year, EPS is expected to decline by 4%, followed by a growth recovery in the high-single-digit range.

- Given the company's ability to grow, I believe that a 16.7x multiple makes sense. If we get a return to that valuation by incorporation of expected EPS growth rates, we get a POTENTIAL annual return of 15.6% through 2025.

{kind=link}

This potential return includes dividends.

Although I expect the company to outperform the market on a long-term basis, it may take a while until the stock price reaches its prior highs.

As we can see in the chart above, after the Great Financial Crisis, the company traded at a discount for many years despite aggressive EPS growth.

Interestingly enough, it didn't keep the company from returning 14.5% per year since 2009!

In other words, buying great companies at great valuations almost always pays off in the long term.

Given the attractive valuation of LHX, caused by industry headwinds, some M&A uncertainties, and long-term growth opportunities, it remains my go-to investment.

I have aggressively bought LHX for my portfolio, my family's portfolio, and other portfolios that I manage.

If the market presents new opportunities, I will continue to add to my position.

My rating remains a Strong Buy rating.

For further details see:

With Significant Potential, L3Harris Remains My Favorite Deep Value Dividend Stock