SHOP - Wix.com Beat Q4 Earnings Prospects Are Bright

Summary

- Wix.com Ltd. trumps earnings, suggesting its business model is taking off amid robust growth in the SME space.

- Although the company has yet to achieve profitability, its up-the-line margins are improving. Moreover, Wix.com's earnings quality is advancing with a reduction in deferred revenue.

- The website builder market is growing, and Wix.com is ideally placed to benefit, regardless of rising competition.

- A share buyback program and improved margins suggest Wix.com is adding to shareholder value.

Are you looking for an overlooked growth stock? Well, you have landed on the right page.

Website building tool Wix.com Ltd. ( WIX ) beat its fourth-quarter earnings estimates on Wednesday, illustrating continued progress with a model suitable to today's business environment. In addition to beating earnings, a few distinctive attributes have started aligning for Wix, which could cause its stock to surge in the coming quarters.

Without further ado, let us commence with a deeper discussion about Wix.com's stock.

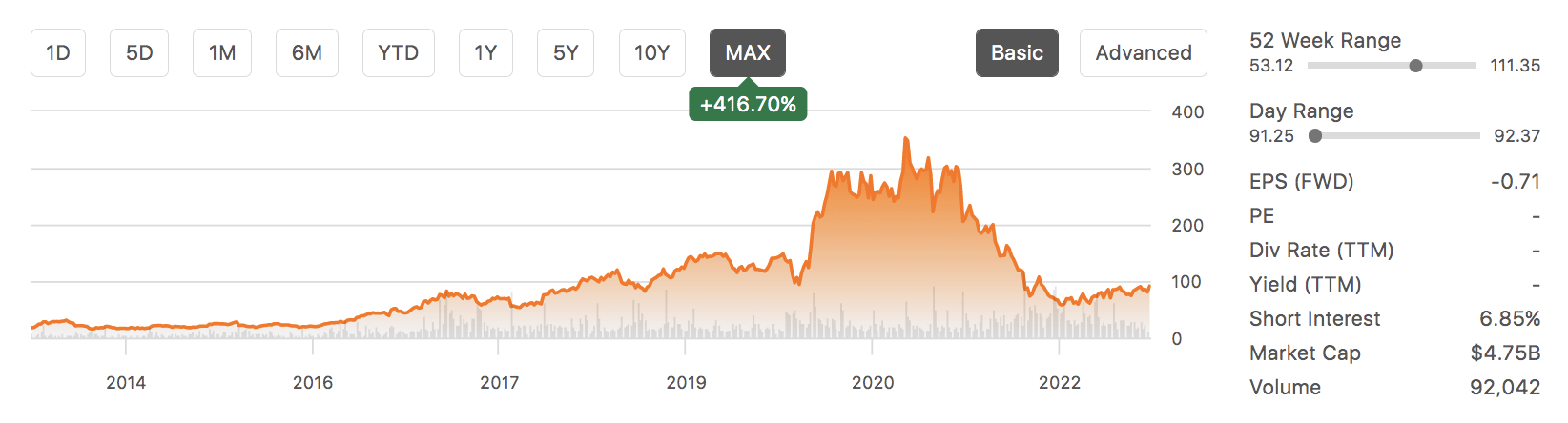

WIX stock's performance since its IPO (Seeking Alpha)

{kind=link}

Assessing Key Variables

A detailed assessment is delivered later in the article; however, a look first at headline Q4 earnings shows that Wix delivered year-over-year revenue growth worth 6% during its fourth quarter and increased its gross profit margin by 330 basis points to reach a cushion of 65%. Although Wix has yet to deliver a profitable business model, the firm's trajectory suggests that investors can expect residual value to realize in due course.

Click on Image to Enlarge (Wix)

{kind=link}

Wix's subscription-based revenue remains the interface of its business, with 8% in year-over-year growth. More importantly, the company's income statement shows a full-year decrease in deferred revenue. Receding deferred revenue implies higher quality earnings, resulting in fewer loose ends. When deferred revenue reduces, credit agencies might often place a company on a "positive outlook" list, which could result in an improved capital structure.

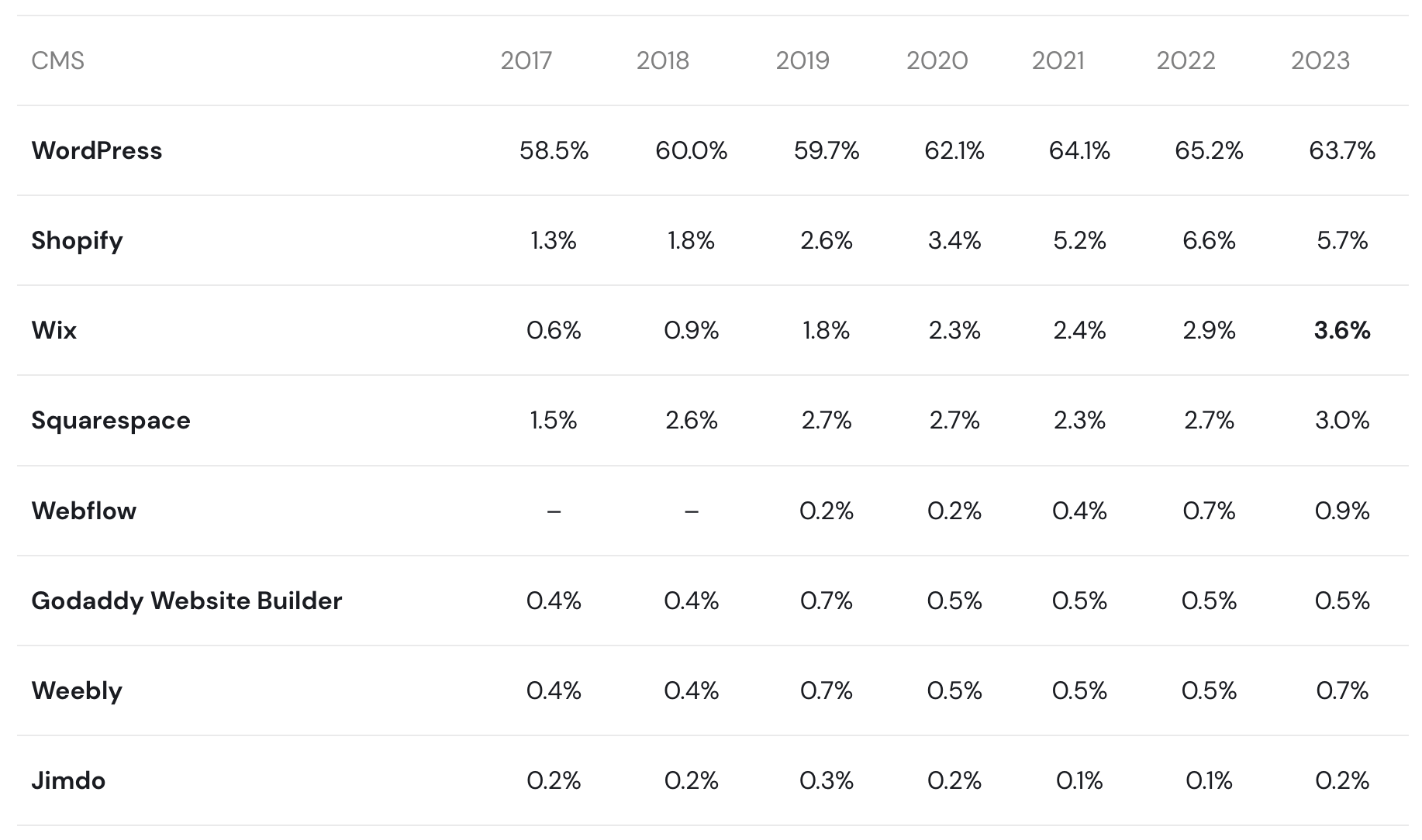

Although Wix's subscription revenue is growing slower than Shopify Inc.'s ( SHOP ) 21% year-over-year growth, we think the 7.1% CAGR of the website builder market and the steep emergence of SMEs that require affordable "drag and drop" websites phase out peer risks. We consolidate this argument by outlining the consolidation of key players in the website-building space and Wix's growing market share in recent years.

To expand on the argument, WordPress' substantial market share provides a differentiated product with a "low-code" platform instead of Wix's drag and drop. Even though Wix will eventually face significant competition with the likes of Shopify, the website-builder market is still in an early-stage growth phase, essentially meaning there is a piece of the pie available to all primary market participants.

Wix's growing market share (Tooltester.com)

{kind=link}

On an ancillary front, Wix continues to up-sell through its business solutions and booking segment. Although the unit follows an up-sale approach, its revenue mix contribution is officially more substantial than its subscriptions segment. According to Wix's management, its bookings' success is due to extended product flow, which has created a more diversified ecosystem of applications.

Similar to the company's subscriptions segment, Wix's bookings division has tapered its deferred revenue, suggesting: 1) higher quality earnings; and 2) an enhanced hold over its customers.

It is perhaps trivial to say, but Wix's bookings division is inextricably linked to subscriptions. Subscription-based revenue is considered a more constant source of income, whereas bookings can be more variable per the economic cycle. Nevertheless, an anecdotal opinion from our side is that online engagement is increasing by the "minute," which requires SMEs to expand their websites' functionality; I mean, the cost vs. benefit is not even an argument, right?

Building Up Value?

Two viewpoints need to be considered here. Firstly, it needs to be established whether Wix is showing signs of enhancing its intrinsic value. And in addition, an outward vantage point is required to discover if the current stock market environment is aligned with growth stocks such as Wix.

Starting with valuation, Wix has announced that it repurchased 5% of its share float during its full-year 2022 (with some repurchased in Q1 2023). Wix's aggressive share buybacks indicate that the company anticipates a growing free cash flow. Moreover, it raises the possibility of an accretive per-share value, which the financial markets usually see as beneficial.

On top of its buyback program, Wix is tapering its operating expenses, indicating that future residual value to its shareholders is en route. Adding to the argument is that the company's bottom line improved in the past year, even though a challenging macroeconomic environment surfaced. Lastly, consider that Wix is still in a growth phase, meaning its top-line figures are more relevant for now.

{kind=link}

Risks To Consider

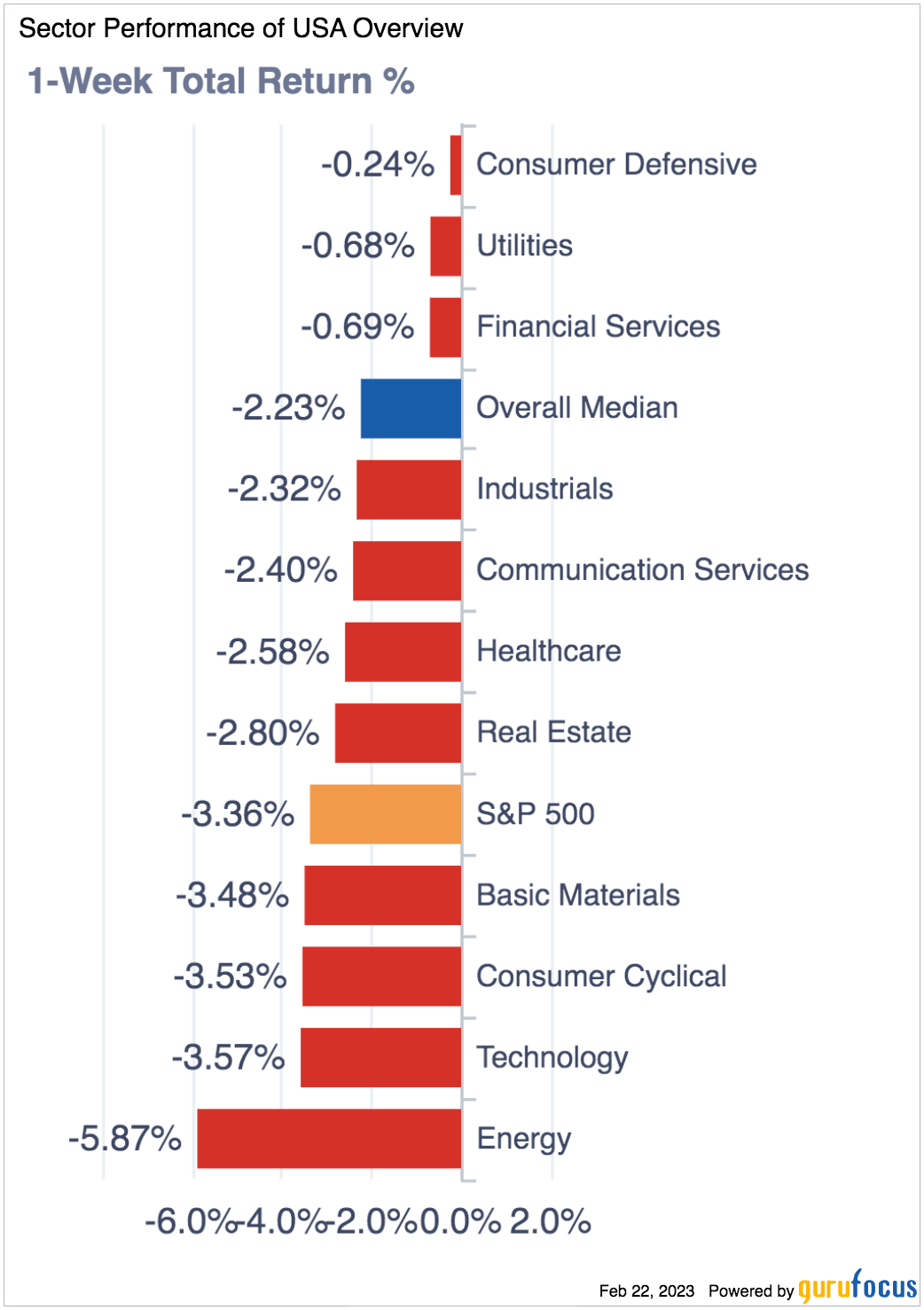

While its prospects are seemingly bright, Wix does host a few notable risks. As a point of origin, the U.S.'s unwanted January CPI surprise has thrown off a few of the technology stocks, as the market has abated its optimism about a growth stock recovery. This is because the market anticipates discount rates and credit risk to remain elevated, which is disadvantageous to growth securities like Wix. Thus, we anticipate technology growth stocks to experience added risk premiums in the coming months, potentially leading to retracements within the sector.

Sector Performance Since CPI Report (Gurufocus)

{kind=link}

Another component investors should be wary of relates to the aforementioned possibility that Wix is facing direct competition from companies that are growing at faster rates. Although we think it may take some time to play out, consolidation will lead to receding top line growth for Wix unless it adds value to its business model through either product differentiation or price leadership.

Concluding Thoughts

Wix.com Ltd. 's fourth-quarter earnings report illustrates both the success of the company's business model and the potential of online website-building platforms.

Critical year-over-year features such as lower deferred revenue and expanded margins are encouraging to see. Moreover, the Wix.com Ltd. recent share buybacks may lead to an accretive stock price and illustrate a growing free cash flow.

- Buy Rating Assigned to Wix.com Ltd. With A 12-Month Horizon In Mind.

For further details see:

Wix.com Beat Q4 Earnings, Prospects Are Bright