WIX - Wix.com: Freemium Model And AI Tools Driving Growth

2023-06-29 08:37:03 ET

Summary

- Wix.com Ltd. has a promising growth outlook due to its freemium business model, a large user base, and impressive cohort retention.

- Despite a focus on expanding the payments segment, the core business of Wix remains strong with potential for growth as more small and medium-sized businesses establish or upgrade their online presence.

- The company is focusing on expanding its payments segment and leveraging AI tools to streamline customer experience and reduce operational costs.

- I am bullish on WIX stock and have an end-of-year price target of $88.

Thesis

With its freemium business model, Wix.com Ltd.'s ( WIX ) strategy of acquiring users through a wide funnel approach is appealing from both a value creation and marketing efficiency standpoint. I believe that there is still significant room for growth in the penetration of websites among small and medium-sized businesses, presenting opportunities for Wix as more companies establish an online presence or transition to more industry-specific designs. The company benefited from the pandemic with accelerated user and premium subscription growth and now focuses on expanding its payments segment. I maintain a positive outlook on its core business, with a passionate user base and impressive cohort retention. The introduction of AI tools and the growth potential in payments and SMB websites contribute to Wix's optimistic prospects in a large, fragmented market. My end-of-year price target of $88 is based on an EV/Sales multiple of 3x applied to the 2024 revenue estimate.

Company Description

Wix is a leading cloud-based web development platform structured for website creators of all levels of proficiency. The company has spearheaded the DIY market, offering its customers products ranging from drag and drop visual development to developer capabilities. With roughly 165 million registered users, the company offers a unique narrative that allows Wix to leverage its freemium-based business model to convert non-paying registered users to premium subscriptions using its large audience base and verticalized solutions for SMBs looking to create an improved static or e-commerce web presence.

Q1 Review & Outlook

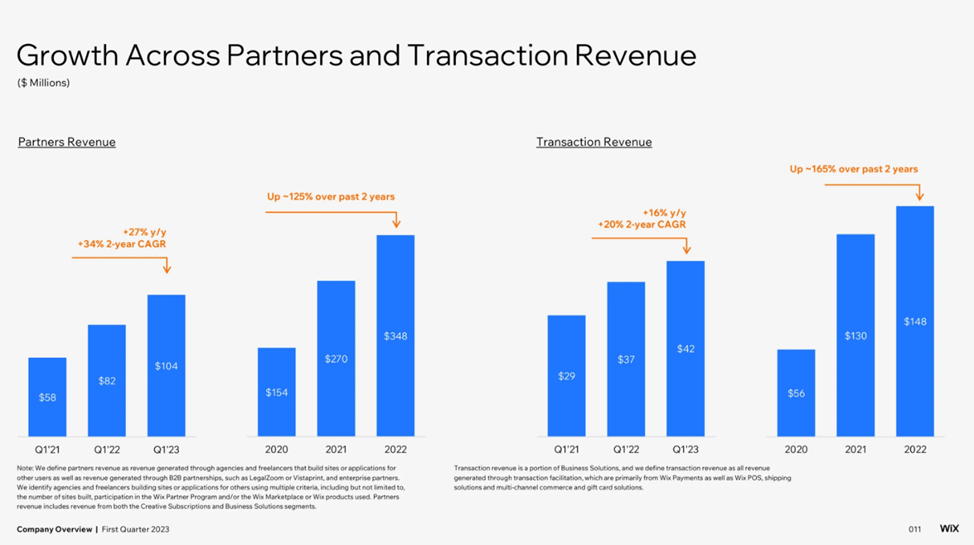

WIX exceeded expectations in the first quarter, surpassing estimates by 1.3%. This was primarily driven by a stronger-than-expected performance in Business Solutions and, to a lesser extent, Creative Subscriptions. The management attributed these positive results to the strong performance of customer cohorts, with more customers showing high intent and generating higher average revenue per user (ARPU). This is particularly encouraging since WIX reduced its sales and marketing expenses significantly, accounting for only 24% of revenue in 1Q23 compared to 43% in Q122. I am pleased to see the B2B Partnerships segment starting to generate revenue from bookings, although it will likely remain a small contributor this year.

WIX has a history of investing in artificial intelligence, as evidenced by their site creation platform, ADI, and the numerous AI-based products currently offered, with more in the pipeline. The management believes that generative AI will streamline the customer experience at the initial stages and facilitate the adoption of their more advanced tools.

Leveraging AI tools

WIX has introduced two intriguing products. The first one is an AI text creator integrated into the Wix editor. This innovative product aligns with WIX's core strength as a user-friendly platform for easy content creation. I am keen to observe how competitors utilize similar technology and how it affects WIX's competitive advantage in terms of user-friendliness.

The second product involves employing large language models across their self-service channels, including the Chatbot and Help Center. This implementation is expected to generate cost savings over time, as WIX has been actively reducing costs related to customer care. By leveraging these language models, WIX aims to enhance their customer support capabilities while optimizing operational expenses.

Bullish on Payments & Core Business

WIX experienced significant benefits from the COVID-19 pandemic as small and medium-sized businesses sought to quickly establish their online presence and e-commerce platforms. Consequently, there was accelerated growth in both user and premium subscription numbers. In order to sustain revenue growth, WIX is focusing on expanding its payments segment. Although Business Solutions revenue currently represents only about a fraction of overall revenue. I view payments as an emerging opportunity that WIX has been prioritizing, and I believe the current period presents an optimal time for the company to capitalize on it.

Despite the current focus on payments, I maintain a positive outlook on WIX's core business. The company possesses a broad base of registered users, many of whom were attracted during the COVID-19 pandemic. Furthermore, WIX demonstrates impressive annual cohort retention and growth, which I expect to continue due to the substantial customer base acquired during the pandemic.

{kind=link}

Valuation

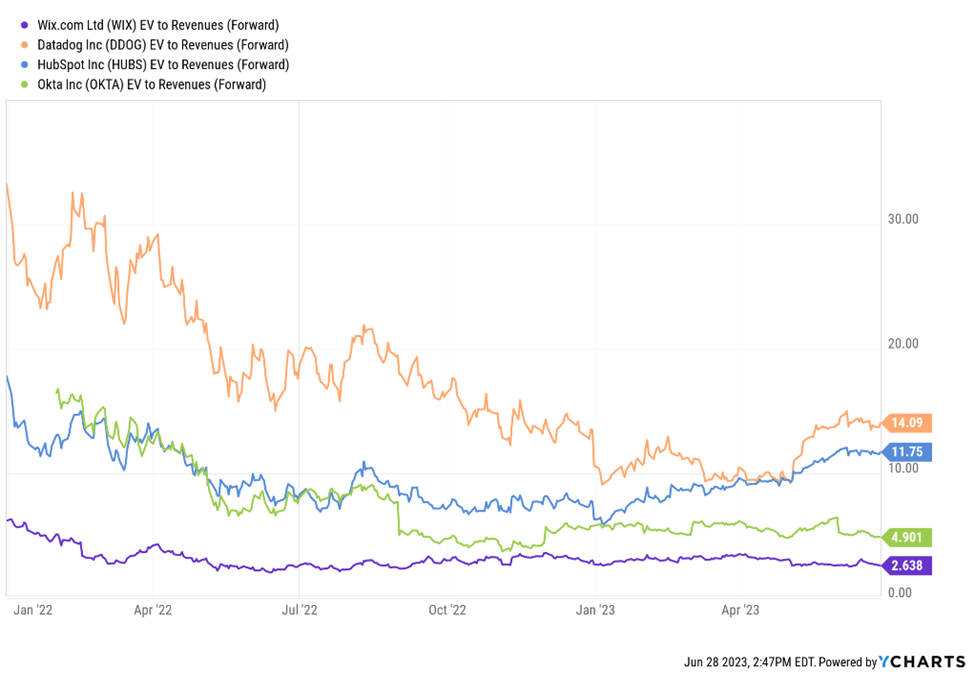

My end-of-year price target of $88 is based on an EV/Sales multiple of 3x applied to the 2024 revenue estimate. I look for success in payments to drive revenue growth estimates higher and make the stock more attractive relative to the company's SAAS peers. My bullish scenario relies on higher revenue growth in the "Do-It-For-Me" (DIFM) tools segment due to increased investments in research and development, customer care, and better-than-anticipated acceptance of the payments feature.

{kind=link}

Risks to Target

If WIX encounters difficulties in further penetrating the small and medium-sized business, prosumer, and individual markets worldwide, it could lead to a slowdown in revenue growth and collections. Any early indications of negative changes in cohort behavior or signs of deceleration in Average Collections Per Subscriber ((ACPS)) or Average Revenue Per Subscriber (ARPS) could potentially result in a reevaluation of the stock's valuation multiple and a reduction in free cash flow. Moreover, although the company has achieved significant growth in the United States, which accounts for approximately 52% of its revenue, primarily driven by SMBs recognizing the importance of transitioning their operations online, other high-growth regions like Europe and Latin America are expected to contribute significantly to future expansion. Consequently, any deceleration in these regions could have a negative impact on sales.

Conclusion

Wix has a robust product offering in the do-it-yourself site builder market and is making progress in catering to the larger do-it-for-me and web professional community. There is considerable untapped potential for website adoption among small and medium-sized businesses, which creates favorable prospects for Wix as more companies seek to establish an online presence or upgrade to industry-specific designs. I am bullish on the stock and have an end-of-year price target of $88.

For further details see:

Wix.com: Freemium Model And AI Tools Driving Growth