WNS - WNS Holdings: I'd Like To See Margins Improve

2023-10-12 12:08:10 ET

Summary

- WNS Holdings is a Business Processes Management outsourcing company based in India, operating in various industries.

- The company's financials show solid performance, but the share price has decreased due to fears of AI replacing its services.

- I believe that AI will enhance efficiency rather than replace human expertise, but want to see improvements in certain metrics before recommending a buy rating.

Investment Thesis

WNS Holdings ( WNS ) is going to announce Q2 earnings shortly, so I wanted to take a look at the company’s financials and if the underperformance YTD is valid. The company sports solid financials with slight decreases in some metrics, however, the company’s share price went down recently due to the fears of AI. The company is still trading at a premium of its fair value and what I would be willing to pay for it, therefore, I assign a hold rating, until I see improvements in some metrics detailed below, as I believe the AI fears are overblown.

Briefly on the Company

WNS Holdings is a Business Processes Management outsourcing company based out of India. It operates in many industries; however, the primary segment would be within the insurance industry (~27% of total FY23 revenue), followed by travel and leisure (~17% of total revenue), healthcare (~16% of total revenue), diversified businesses like manufacturing, retail and CPG, media and entertainment, and telecom (~15% of total revenues), and banking and financial services (7%) to name a few.

WNS is a leading BPM company that, as you can see, serves many different industries and is leveraging advanced technologies like intelligent automation, and artificial intelligence, coupled with natural language processing and machine learning.

The company has a lot of expertise in helping enterprises accelerate their digital transformation, and automate business processes, all while employing the use of AI and ML to be as efficient as possible.

The company had its IPO in 2006, which enabled it to expand into other areas of enterprise, including voice and blended data capabilities, travel and leisure, insurance, and banking and financial services. Now T&S and Insurance becoming the company's top revenue generators.

Over the next decade or so, the company went on an aggressive expansion and acquired many different outsourcing companies to expand its portfolio and global reach, while opening many more offices in India, Sri Lanka, Romania, the Philippines, Costa Rica, Poland, Spain, and Australia. Since its IPO, the company made 12 notable acquisitions that helped the company become an expert in many different industries, especially the insurance, healthcare, and travel and leisure industries.

My Thoughts on AI Threat

I believe that as usual, investors overreact to a new technological disruption and think that companies like WNS will become obsolete in a matter of a couple of years because of AI. I believe that companies like WNS will find ways to enhance their efficiency through the means of generative AI and will put it to good use. AI will be able to help the company with monotonous/repetitive tasks, so that the expertise of people can be put to better use, in situations where critical thinking is very much essential in the operations of an enterprise. Harvard Business Review believes in the same idea that mindless tasks will be taken over by AI, which will allow people to focus on what is important.

I’ve been using the integration of ChatGPT in Microsoft’s ( MSFT ) Bing browser and I can confidently say that the AI is nowhere near replacing anyone, and that will be the same for more advanced AIs that will be built to work in tandem with the human’s critical thinking, creativity, and problem-solving skills.

Financials

Just to note, all the graphs below will be as of FY23, which ended at the end of March ’23. I will add any relevant information from the most recent quarter for extra color if needed.

As of Q1 ’24 , the company had $165m in cash and equivalents against $129m in long-term debt. How worrisome is this for the company? I don’t think it is very bad, considering that the debt amount isn’t substantial. The historic interest coverage ratio of the company is very healthy, and as of Q1 ’24, the ratio stood slightly over 5x, which means that EBIT can cover annual interest expense on debt 5 times over. For reference, many analysts consider 2x to be a healthy ratio. I don’t agree with that, and I look for at least 5x as I believe 2x is slightly too close for comfort because of one year of bad earnings and the company might struggle to cover the interest expense. I like to be more conservative, therefore, 5x seems sufficient for me.

{kind=link}

The company’s current ratio has been right at the range I consider efficient, which is 1.5-2.0. I believe this is an efficient ratio range because it tells me that the company has enough liquidity to be able to pay off its short-term obligations and is not hoarding cash that could be used to further the growth of the company. Anything massively over 2 I feel is a lost opportunity and the assets are not being used very efficiently in my opinion. It is better to have a high current ratio than under 1 that is for sure, but there are also downsides in my opinion. The company's short-term investment went down by around 50% y/y, which brought its CR down to around 1.5, which I'm okay with. In the latest quarter, the CR went down to around 1.4, which some far doesn't tell me much, however, I would have to monitor over upcoming quarters to see if the downtrend continues.

{kind=link}

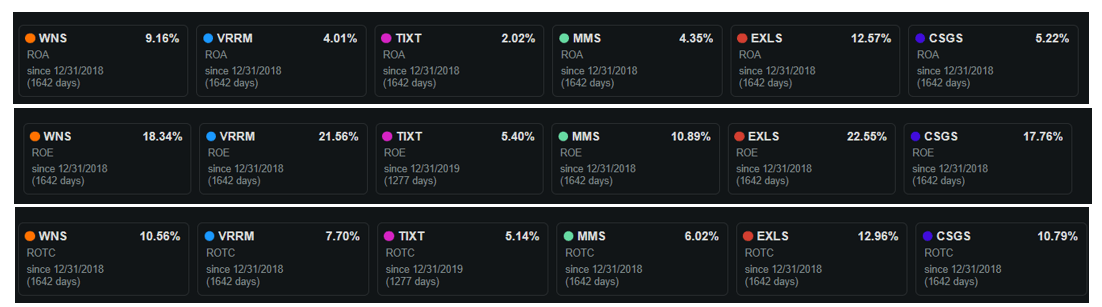

In terms of profitability, the company’s ROE and ROA have been outstanding over the years, which tells us that the management is very adept at utilizing the company’s assets and shareholder capital efficiently, thus creating value.

Looking back at the company's financials, I can see there was a big jump in ROA and ROE from FY17 to FY18 when net income increased by 126% y/y and revenues by around 26%. This jump in revenue and net margins can be attributed to the company's ability to squeeze out more revenue from existing clients (80% of total increases), while the other major contributor was acquisitions. So, I would say a combination of management's ability to get more out of existing clients coupled with strategic acquisitions in FY17 (Denali, HealthHelp), provided better profitability and a much higher bottom line that translated into great ROA and ROE numbers.

Are these high metrics unique to the company? If we look at the company's peers as provided by Seeking Alpha, we can see that WNS is at the top of the range of competition, which means you'd be investing in the top performer. One thing to note is these have been trending slightly downward, so I will have to monitor these going forward. So, it seems the company's ROA is above average compared to the companies below by about 50%, while ROE is around 12% above the average. WNS is more efficient at generating profits than the industry average (or at least the listed competitors' average).

Efficiency and Profitability metrics vs Competition (Seeking Alpha)

{kind=link}

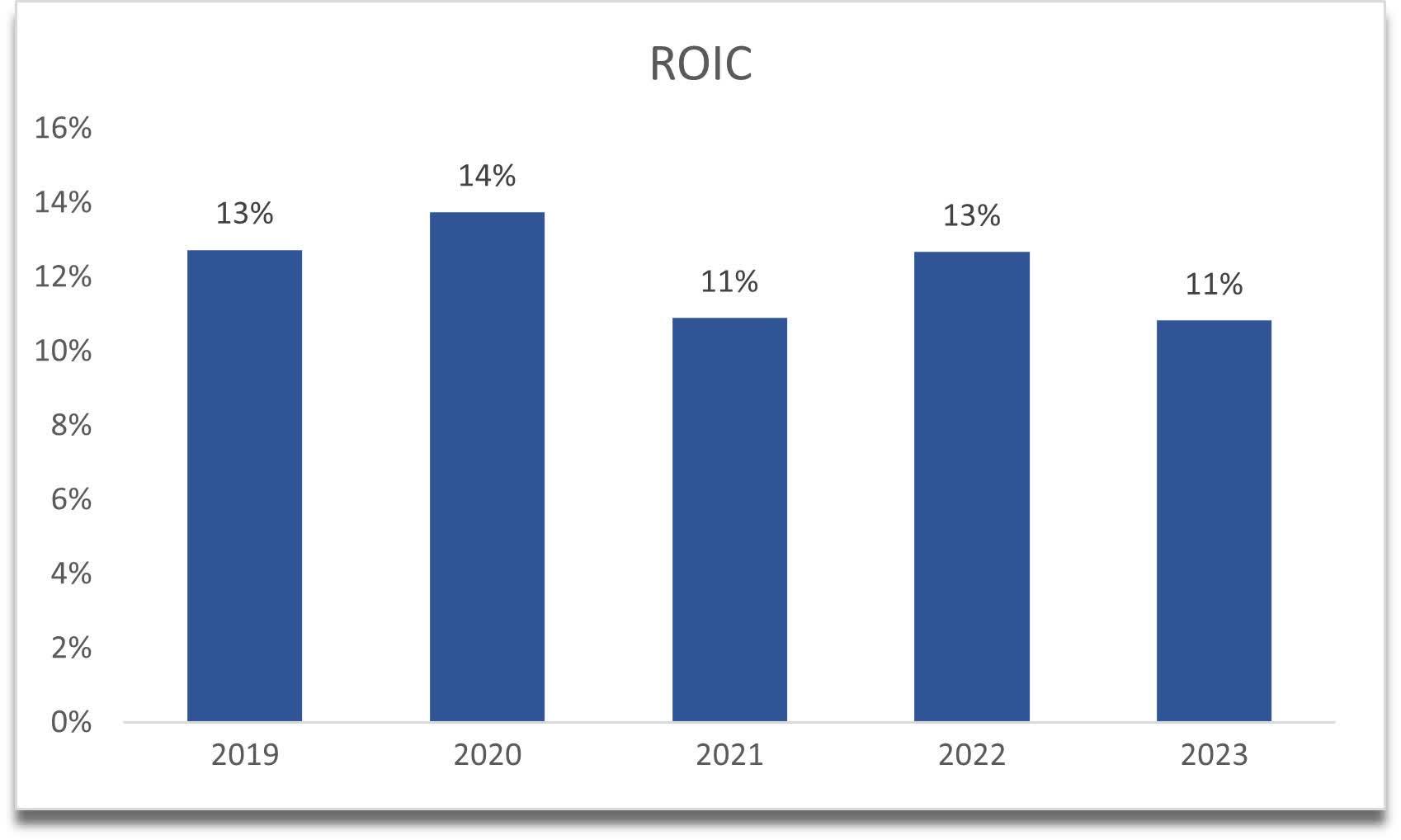

A similar story has been unfolding in the company's return on invested capital, however, it is still above my minimum of 10%, which tells me that the company may be enjoying a competitive edge and a moat. The management can reinvest capital into very profitable projects, however, not as profitable as before when it was aggressively acquiring smaller companies to expand its portfolio. A good way of looking if the company is destroying value or creating it is if the ROIC is higher than its Weighted average cost of capital (or the WACC). I have calculated the company's WACC to be at around 9.5% (see below picture of the components used), which means the company is creating value. On top of that, the company is above the average of the mentioned competition's ROIC of around 8.8%.

WACC Calculation (Author)

The cost of debt was calculated by taking the company's outstanding debt which were made up of variable interest rate plus some percentage to end up averaging around 6.6%. Tax rate I calculated by taking the company's average tax expenses over the last three years. As you can see the company mainly uses equity, so no wonder the WACC is very close to the cost of equity figure (which was calculated using the capital asset pricing model or CAPM)

{kind=link}

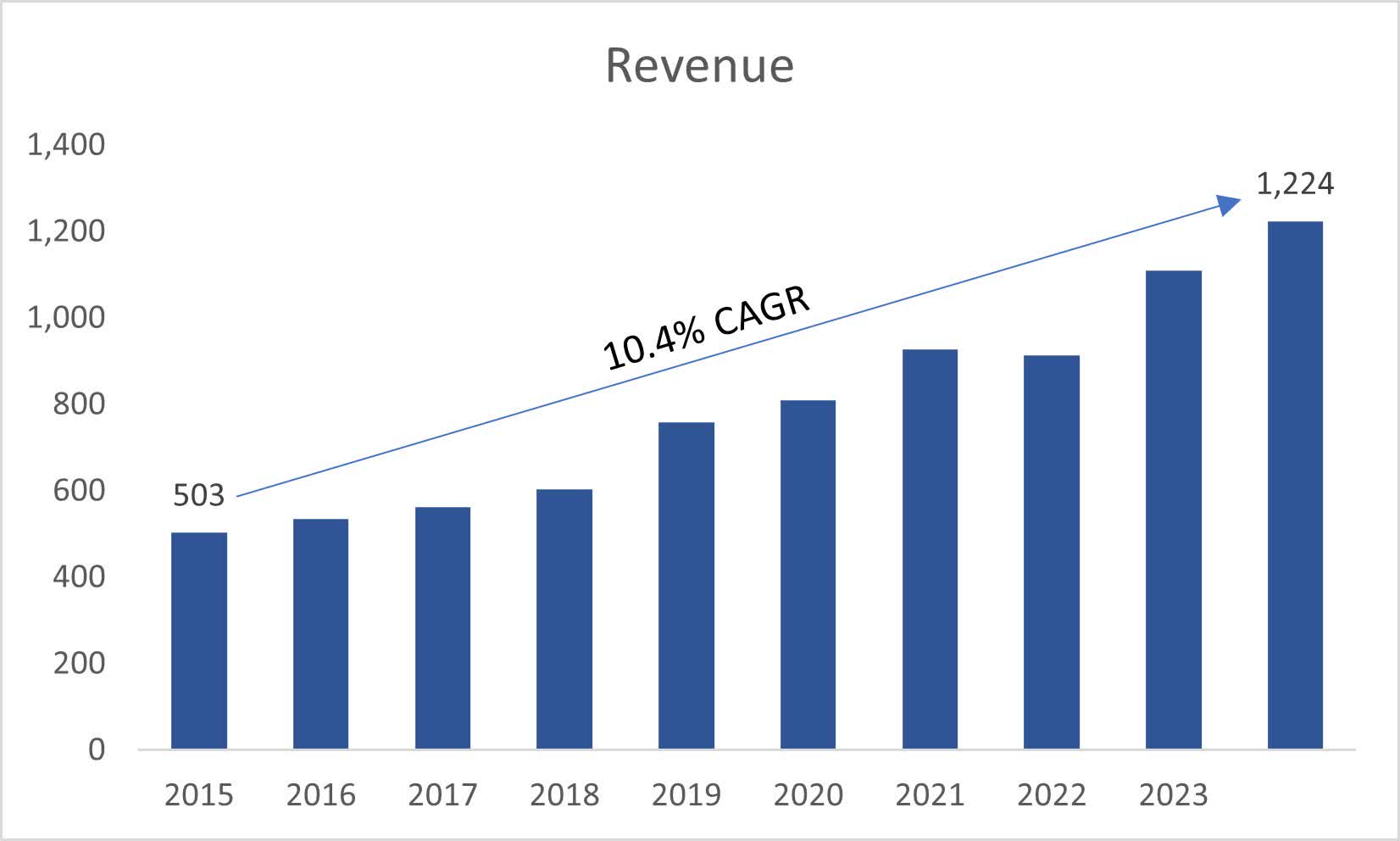

In terms of revenues, the company's historic growth has been commendable in my opinion, growing at a respectable 10% CAGR over the last decade. For my valuation in the next section, I will more or less anchor my assumptions to the historic performance, but a little bit more on the conservative side for that extra margin of safety, which is supported by analysts' estimates , and management's guidance .

{kind=link}

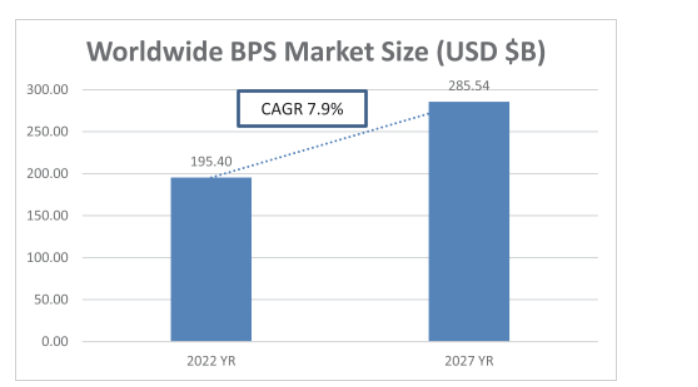

I believe that the company will be able to achieve such revenue growth in the future because Gartner projects the BPS market to grow at around 8% CAGR and the company managed to beat these estimates by a couple of percentage points.

{kind=link}

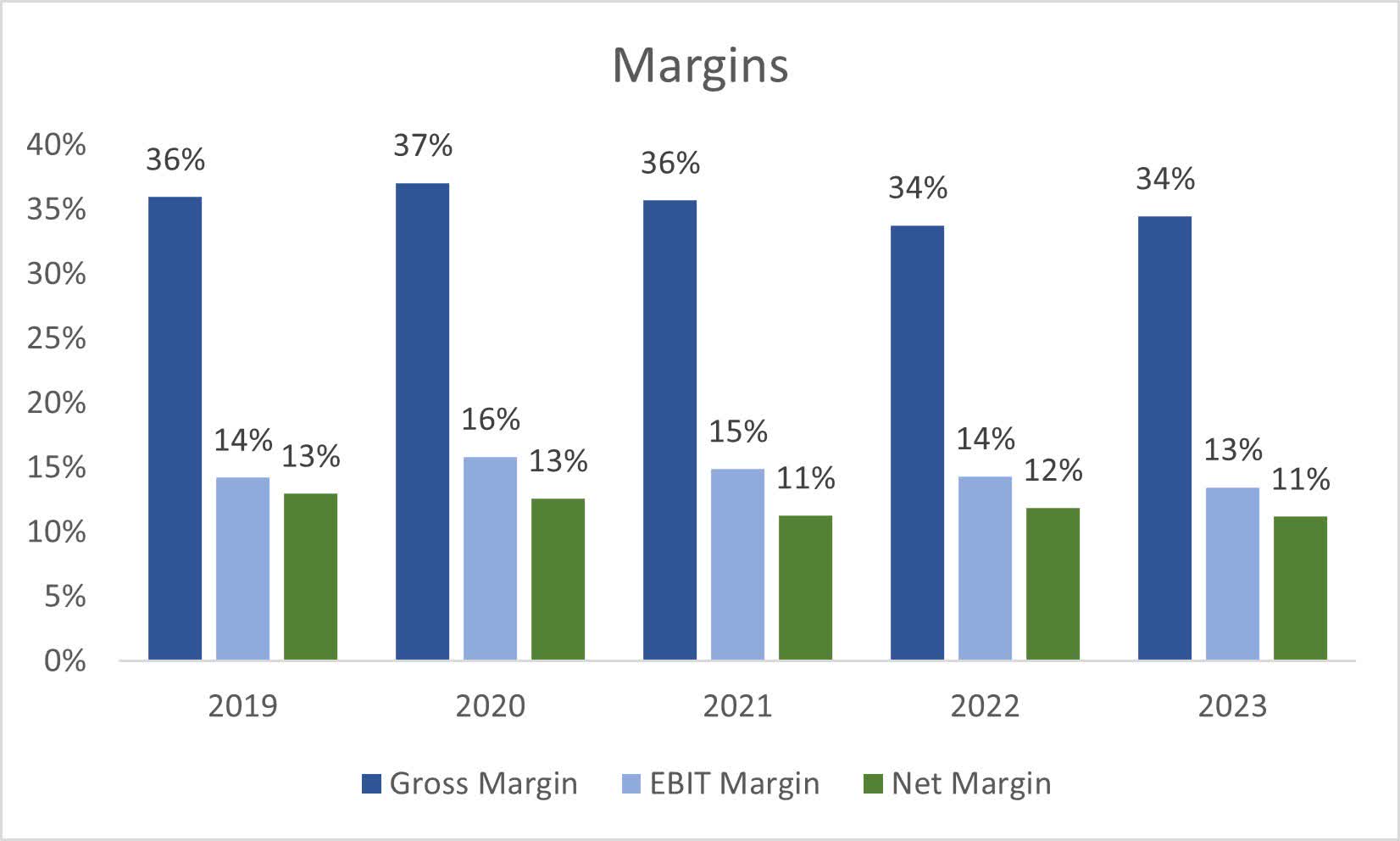

The company’s margins have been somewhat steady over the years, with a similar decline observed in the most recent year. The same margins remain as of Q1 '24, which is not a bad sign but I would like to see improvements going forward, and when the company announces 2 nd quarter results, I would like to see some initiatives/ cost-cutting measures introduced to regain profitability and efficiency.

{kind=link}

Overall, a decent company from what I can see from the historic performance. I can see that it has been slightly less efficient and profitable over the last while, which may be a sign of further deterioration in terms of margins, but we will have to wait for the next couple of quarters to see how this situation develops. The company still has a decent competitive advantage, is profitable, and has a very strong financial position in general but the downtrends are worrisome.

Valuation

As I mentioned earlier, I will be on a slightly more conservative end of assumptions here, so for my base case scenario revenue growth, I went with a 9% CAGR. For the optimistic case, I went with around 11% CAGR, while for the conservative case, I went with around 7% CAGR for the next decade. I believe these assumptions are reasonable and likely to occur in the future.

{kind=link}

In terms of EPS, for my base case scenario, I went with around 14% CAGR through FY33. FY24 will see EPS of $2.85, $3.17 in FY25, and $3.75 in FY26, while analysts say the company will earn $2.9, $3.39, and $3.94, respectively, so my assumptions are on the slightly more conservative end, which will give me more margin of safety. For the optimistic case, I went with a 16% CAGR of EPS growth, while for the conservative case, I went with around 13% CAGR for the next decade.

How I got to these EPS estimates is I assumed the company's gross and operating margins as below for all three scenarios, which show a gradual improvement in profitability over time. This is supported by the management's view on Gen-AI in the latest quarter results:

" We also see gen-AI as a catalyst for driving higher value services solutions, as well as engagement models. We believe that gen-AI will enable WNS to continue moving our relationships up the value chain and shift engagements from headcount-based pricing to models based on ownership and accountability for results. As a result, we will be able to better align relationship objectives, delivering great outcomes for clients and stickier revenues with increased margin opportunities for WNS."

So, I believe slight margin improvements over the next decade are justifiable.

Gross and Operating Margin assumptions (Author)

{kind=link}

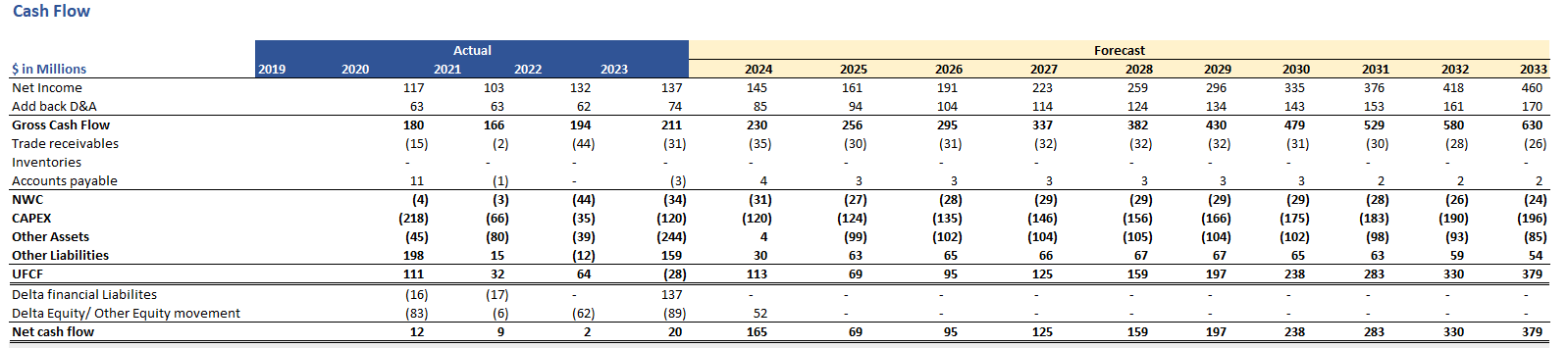

Below is the breakdown of the cash flow statement that I modeled after all the assumptions on revenue, margins, and EPS were made. For the DCF valuation, I took the Unlevered Free Cashflow or UFCF which doesn't take into account financial obligations, hence unlevered, however, in this case, I assumed the company is not going to pay off that small amount of debt it has over the model period, so net cash flow and UFCF are almost identical apart from some adjustments in shareholder equity in FY23. The WACC used was mentioned in the Financials section and how I calculated it.

Cash Flow Statement Forecast (Author)

{kind=link}

On top of these estimates, I decided to add a 15% margin of safety for extra cushion, as it is better to be safe than sorry. You can still lose money if you’re buying a great company at an inflated price, so the more margin of safety the better your returns will be in the end. With that said, WNS’s intrinsic value is $65.84 a share, which means that the company is trading slightly above its fair value and what I would be willing to pay for it.

{kind=link}

To get the Terminal value of the company, I took the last forecast cashflow which is pictured in the cash flow statement forecast above, used the terminal value formula, and then discounted it back to the present to get the PV of the terminal value using the basic formula: FV/(1+r)^n, where FV is terminal value, r is the WACC, which is 9.58%, n is the last period of the model, which is 10.

Terminal Value Formula (Valentiam)

I chose a terminal growth rate (g) of 2.5% because I like to think of it in terms of inflation, which historically has been around this number.

Closing Comments

I would like to see some cost-cutting initiatives introduced in the following quarters that would improve the company’s profitability and reverse the downtrend. I would like to see the margins at least stabilize and not fall further as time goes by.

If I were to open a position, I would be willing to pay around $60-$65 a share and preferably less because of uncertainties in the sector in which the company operates. It is hard to know what Gen-AI is going to do to the industry the company is in, however, I don't think it is going to replace and make companies like WNS obsolete any time soon. AI still has many flaws, and I wouldn't trust it to do something that requires critical thinking. I would and I do, however, use it for simple queries on the browser, and yet it sometimes gives me the wrong information anyway, with a lot of confidence.

I will check back in on the company after it releases its 2 nd quarter results to see how the company feels about the near future and what the management is doing to regain profitability and stay ahead of the game.

For further details see:

WNS Holdings: I'd Like To See Margins Improve