XENE - Xenon Pharmaceuticals: De-Risked Late-Stage Neurology Biotech Buy

Summary

- We initiate Xenon Pharmaceuticals with a BUY rating.

- We see XENE as one of the most de-risked and compelling SMID-cap biotech companies with a lead late-stage clinical candidate.

- We build a high degree of conviction based on recent phase 2b X-TOLE data that demonstrated a significant ability to reduce seizures across primary and secondary endpoints in difficult-to-treat FOS.

- Company currently holds around $600M of cash and has a cash runway of 2-3 years.

Background

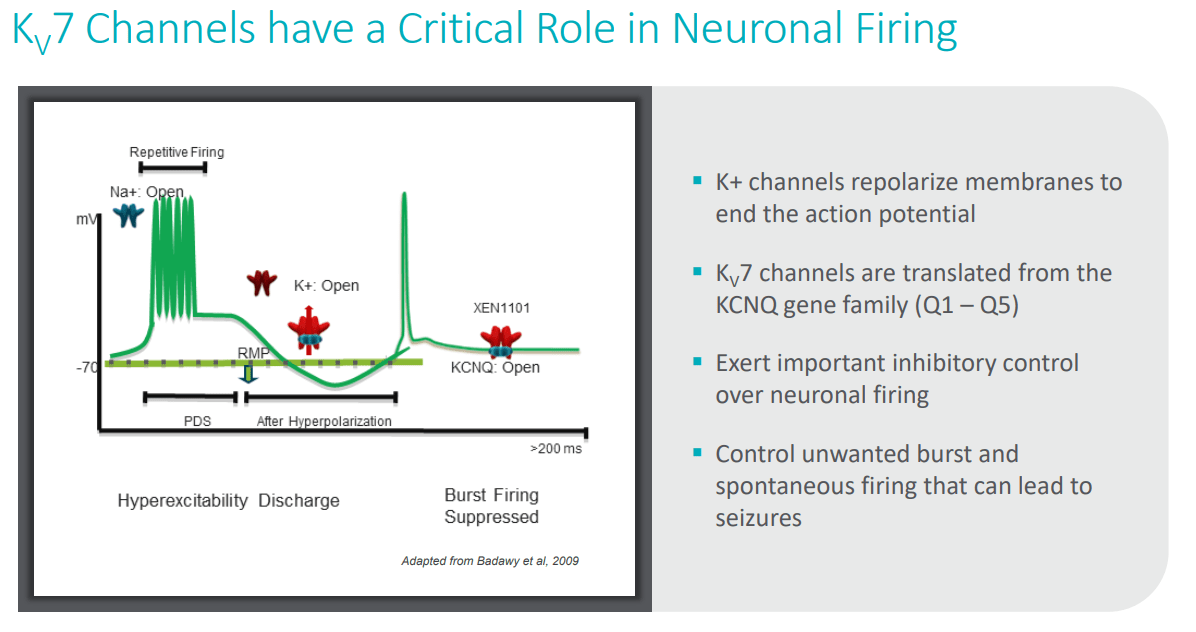

Xenon Pharmaceuticals (XENE) is an exciting Canadian SMID-cap biotech focusing on development of treatments for rare genetic disorders. We initiate Xenon Pharmaceuticals with a BUY rating; even with the meteoric rise in stock price, we see XENE as one of the most de-risked and compelling SMID-cap biotech companies with a lead late-stage clinical candidates, XEN1101, that is expected to enter multiple phase 3 studies in epilepsy with high unmet medical need and high market potential. At the moment, the company's most advanced pipeline candidate is XEN1101, which is a novel oral small-molecular drug designed to selectively target and open KCNQ2/3 (Kv7.2/7.3) channels that are highly expressed in the central nervous system and achieve therapeutic potential by reducing hyperexcitability the of the brain, which is the key root cause of epilepsy.

{kind=link}

Pipeline overview

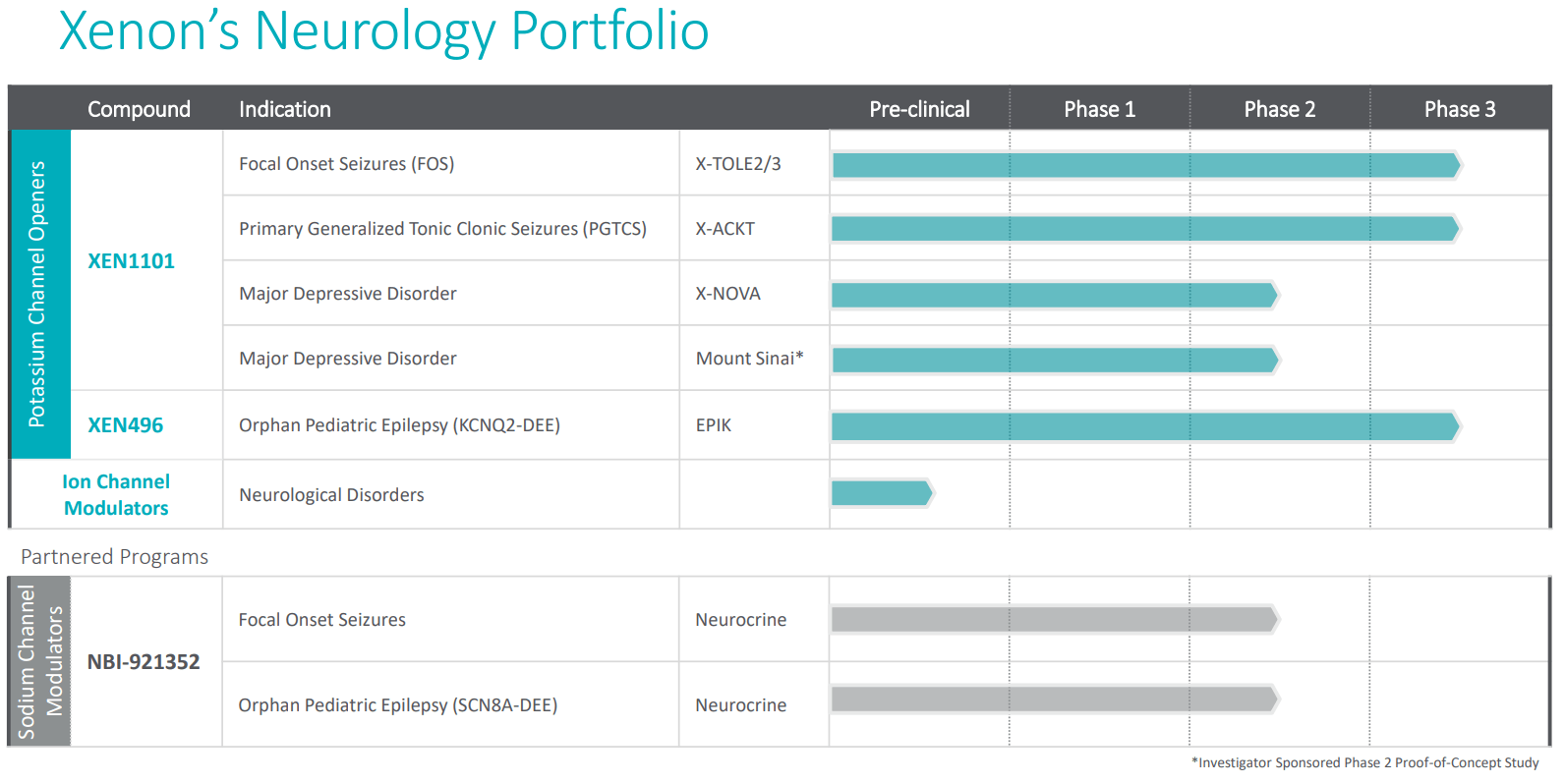

At the moment , XEN1101's primary focus is on epilepsy indications such as i) Focal onset seizures ((FOS)), ii) primary generalized tonic-clonic seizures (PGTCS), and iii) major depressive disorder ((MDD)). There are a few other candidates that the company is developing, such as: a) XEN496, targeting KCNQ2-DEE, which we believe can be seen as a hedge against potential underwhelming data readout of XENE1101, and b) XEN496, a selective small-molecule ion channel modulator, targeting orphan pediatric epilepsy, which we see it as a free option.

The company's phase 2b X-TOLE FOS trial showed a statistically significant reduction in a seizure while treating the difficult-to-treat FOS group with adverse events with standard-of-care treatments. The company emphasized that they have aligned with the FDA on using X-TOLE and phase 3 X-TOLE2 data to support NDA submission for FOS indication. The phase 3 program is underway with X-TOLE2 studying the FOS patient group, and the phase 3 X-ACKT trial studying PGTCS is ongoing.

{kind=link}

We are most interested in XENE1101 positioning as an adjunctive treatment of FOS.

Our bullish view is based on XENE1101's recent phase 2b X-TOLE data that demonstrated a significant ability to reduce seizures across primary and secondary endpoints in difficult-to-treat FOS of adult patients. The key attributes of the treatment that we like in particular are i) compelling efficacy (primary & secondary endpoints) with broad spectrum activity, ii) once a day dosing schedule that does not require titration, which offers a great degree of convenience, and iii) robust safety without concerning serious adverse events.

We find epilepsy a highly attractive market, with a 27-51% relapse rate, and epilepsy syndromes such as JME require lifelong therapy.

Many people relapse and switch around different AEDs with different mechanisms of action. We like the fact that XEN1101 and XEN496's differentiated mechanism of action, K+ channel targeting, as we expect it to offer an attractive alternative (or add-on) treatment option for epilepsy patients. Moreover, we believe there will be multiple combination opportunities for XEN1101 in the future, and we see great potential in pipeline expansion in other psychiatric indications.

We view XENE1101 as de-risked.

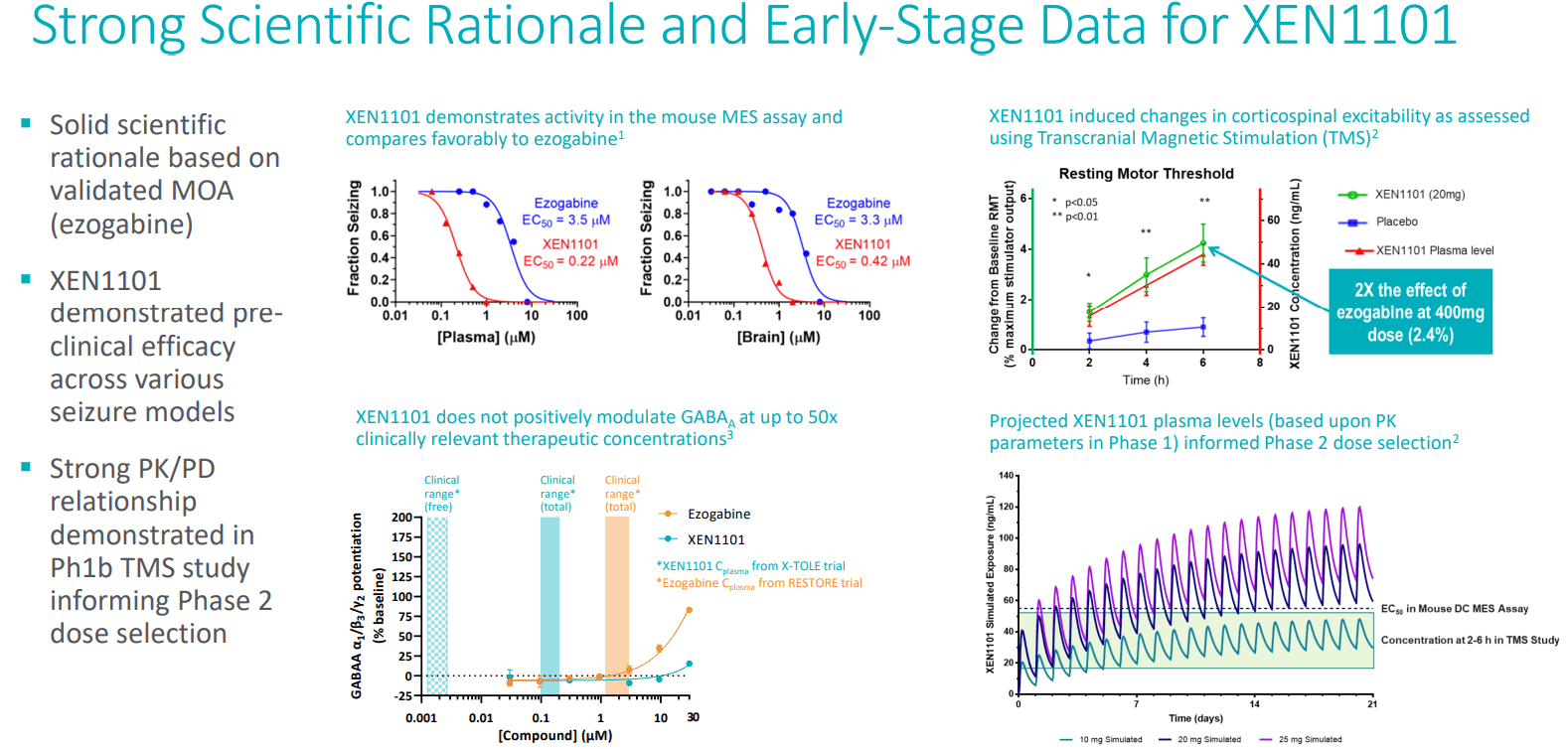

We highlight that XEN1101 is an adapted version of the first-generation Kv7.2-7.5 potassium channel opener, ezogabine . We note that ezogabine was effective but had some concerning side effects (pigmentations). Ezogabine/Retigabine (brand Potiga) was launched in 2011 but got pulled out of the market due to pigmentation and urinary retention issues. We highlight that it was withdrawn because physicians didn't prescribe it, not because the FDA banned it.

Based on the data on hand, XEN1101 shown to not form pigmentation dimers, albeit we believe long-term safety data, perhapse post-marketing surveillance data would be needed to de-risk pigmentation issue fully. We see urinary retention to be a manageable concern. Besides safety concerns, XEN1101 has shown to have a superior once-a-day dosing schedule vs. 3 times per day, a PK profile that allows missed doses, and 20 times greater potency compared to ezogabine. The trials to date have shown statistically significant, dose-dependent seizure reduction compared to standard-of-care treatments, which seems comparable with current standard-of-care anti-epileptics.

{kind=link}

Phase 2b X-TOLE study was compelling.

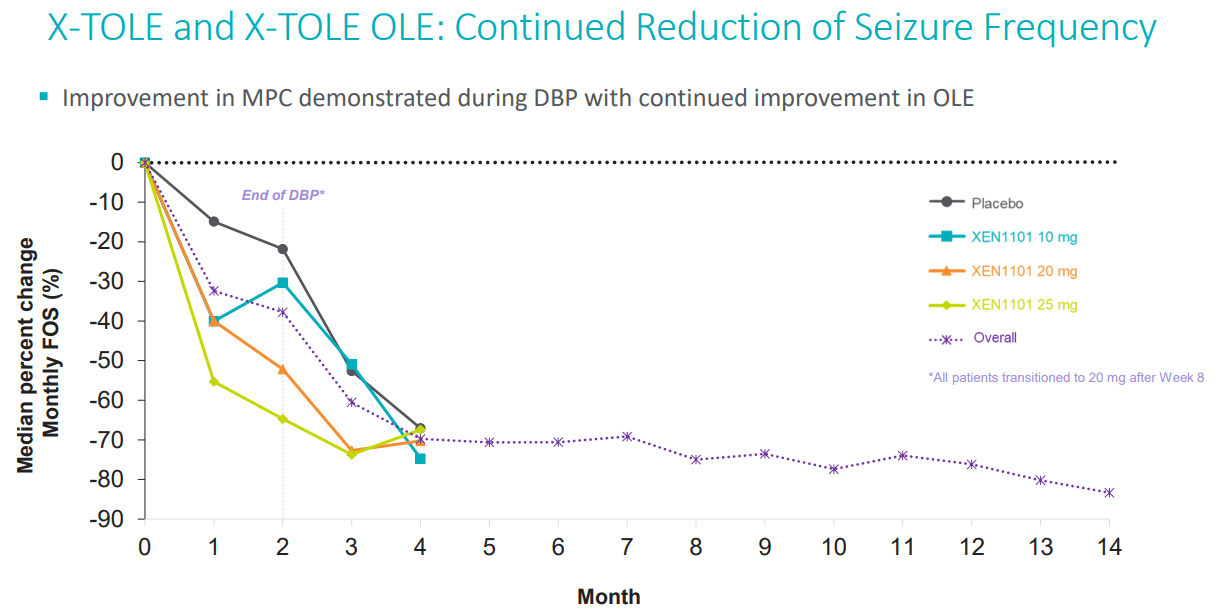

The XEN1101 's phase 2b X-TOLE study evaluated adjunctive XEN1101 therapy in an adult patient population with focal onset seizures ((FOS)). We highlight that this patient population represented a "difficult-to-treat group" that involved many prior failures and an extremely high burden of disease. The patients enrolled in the trial were on 1-3 stable background anti-seizure medications (ASMs) during the study period but failed a median of 6 previous ASMs prior to initiating the XEN1101. XEN1101 continuously showed compelling efficacy with promising dose-dependent improvements in seizure reduction at 10mg to 25 mg doses, as shown below.

{kind=link}

{kind=link}

We summarize key takeaways from the trial.

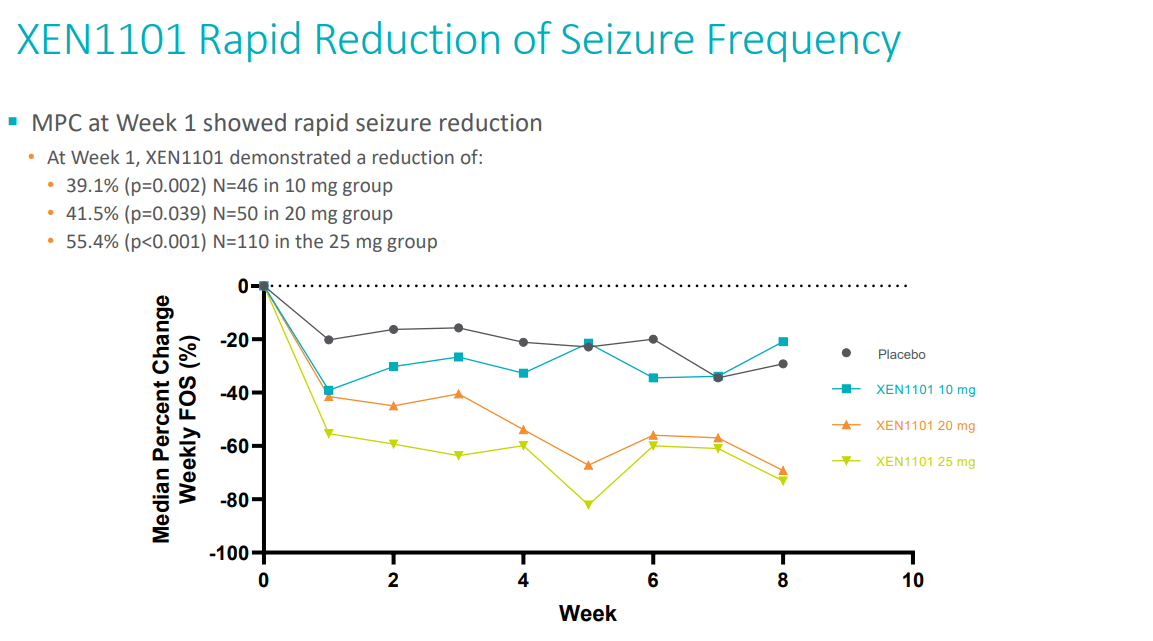

- Rapid onset of action across all treatment arms at week 1

- Durable response during the OLE portion of the trial. The company noted that i) patients who remained in the X-TOLE OLE for at least 3 months and 12 months experienced >70% and 80% reduction of MPC compared to the baseline and ii) >=6 and >12 months of consecutive months of seizure freedom was reached in 19.6% and 9.5% of subjects in the OLE population. The company noted that the X-TOLE OLE is expected to continue for 3-5 years for assessing long-term data.

- According to the OLE safety data published as of June 22, the safety data was consistent with the data shown during the double-blinded period. A few that we highlight are i) similar CNS side-effects, ii) no TEAEs related to pigmentation.

In the primary efficacy endpoint of change from baseline in monthly focal seizure frequency, XEN1101 provided median percentage reductions of 33.2%, 46.4%, and 52.8% in the 10mg, 20mg, and 25mg groups, respectively, versus a placebo response of 18.2%. The monotonic dose response of XEN1101 compared to placebo was statistically significant at all doses (p<0.001). Additionally, there was a marked improvement and dose-response in a responder analysis, which measured patients with a ?50% reduction in monthly focal seizures versus placebo. Achievement of the responder analysis threshold was seen in 28.3% of patients at 10mg, 43.1% of patients at 20mg, and 54.5% of patients at 25mg, compared to 14.9% in the placebo group. This secondary endpoint was statistically significant across all doses (p=0.037 at 10mg; p<0.001 at 20mg and 25mg).

There was a trend toward increased treatment-emergent adverse events (TEAEs) in the 25mg treatment arm, where 85.1% of patients experienced at least one TEAE (compared to 62.3% in the placebo arm, 67.4% in the 10mg arm, and 68.6% in the 20mg arm). A similar trend was seen in the number of patients that discontinued treatment due to an adverse event, with a notable increase seen in the 20mg and 25mg XEN1101 arms. Despite these increases, tolerability was actually quite good in relation to other ASMs available, especially given the strength of the efficacy seen for XEN1101 to date. Furthermore, the incidence of treatment-emergent serious adverse events (SAEs) was similar in all four groups, with the placebo group and the 25mg XEN1101 group both having 2.6% of patients with at least one treatment-emergent SAE. Company IR Presentation and press release

Valuation

Using peak sales from Guggenheim of $1.5Bn , and a probability of success of 85% (which is a statistical figure to adjust for the potential clinical risk of the compound), we get risk-adjusted peak sales of $1.27Bn. Using a conservative peak sales multiple of 2.5 (lower than the commonly used 3), we get around $3.15Bn. Considering that the current EV is 1.71Bn (as of Feb 07, 2023), we see around an 80% upside from the stock. Furthermore, the company has around $600M cash on hand, which is enough cash runway for more than 2 years from today. We see anything beyond 1 year of cash runway investible.

Risks

The key risks to our thesis are i) clinical failure of any phase 3 can plague the stock, ii) the company has ~$600M of cash reserve; however, considering that the company is yet cashflow positive if the company runs out of cash reserves and they may have to issue more shares and dilute more, iv) commercial risk, considering that the company does not have an approved candidate, commercial performance is not proven yet and represent as a key risk moving forward, and v) XEN1101 has limited composition of matter patent protection (expires in 2028), which may lead to lower than expected commercial performance due to generic entry.

Conclusion

We initiate Xenon Pharmaceuticals with a BUY rating; even with the meteoric rise in stock price, we see XENE as one of the most de-risked and compelling SMID-cap biotech companies with multiple ongoing phases 3 studies. Once approved, we see the platform has a tremendous opportunity to expand into multiple other CNS indications, as we have seen with many other CNS blockbuster drugs, as many CNS indications share the pathophysiology. We are positive for several catalysts during the next 6-12 months (i.e., X-NOVA MDD study expected to readout in 3Q 2023), and we are a big fan of XEN1101 based on the robust clinical data that showed durable efficacy, safety, and convenience advantages. Furthermore, the company has close to $600M in cash, where we think the company has a sufficient cash runway for more than 2 years based on its current cash burn, which gives us a lot of confidence moving forward.

For further details see:

Xenon Pharmaceuticals: De-Risked Late-Stage Neurology Biotech, Buy