XOS - Xos Makes A Killer Shelf Deal And I Am Buying More Shares

2023-08-03 18:26:25 ET

Summary

- XOS registered $125 million through a shelf offering, providing much needed cash.

- XOS has some big name customers with the potential to be volume buyers.

- XOS focuses on the stepvan market, and is now working to reach profitability.

Xos Inc. (XOS) raised a potential $125 million through a shelf registration ; the Shelf has a single purchaser YA Li PN Ltd, and XOS has the right but not the obligation to sell shares to Ya Li PN at any time until 2026. These shares will carry the weighted average price of XOS shares in the preceding days minus 3%-5%. YA Li PN has the right to sell the shares on the market or hold on to them at their discretion. XOS will not receive any income beyond the initial sale price.

It is an excellent deal for XOS; they have a guarantee of up to $125 million of cash, available when needed, that they intend to use for general business purposes, including work in progress and operating costs.

The shelf names YA Li PN Ltd as the buying shareholder. YA Li PN is a Cayman Island registered Hedge fund managed by Yorkville Advisors Global Lp with almost $10 billion of assets under management. The terms of the deal imply Yorkville likely intends to become a long-term investor rather than to sell the shares immediately; the discount of 3%-5% does not seem large enough to warrant the cost of a quick sale. (They are legally bound by the agreement not to take a short position in XOS.) Yorkville is putting $125 million on the line. It is both a vote of confidence and an excellent boost to XOS liquidity but very dilutive.

Total dilution could be very significant; the Shelf is for 100,000,000 shares. Before the deal, XOS had 176,018,525 shares outstanding, so potential dilution is as much as 57%, which is a big hit to current shareholders (me included). Before the Shelf, I had estimated that XOS needed around $160 million to make it to profit; the Shelf covers almost all of it. The effect of the dilution will only be felt if Yorkville decides to sell.

With the necessary funding now mostly in place, I think XOS is an excellent investment and hope to explain why by looking at its history and how it got to this point.

What does XOS do?

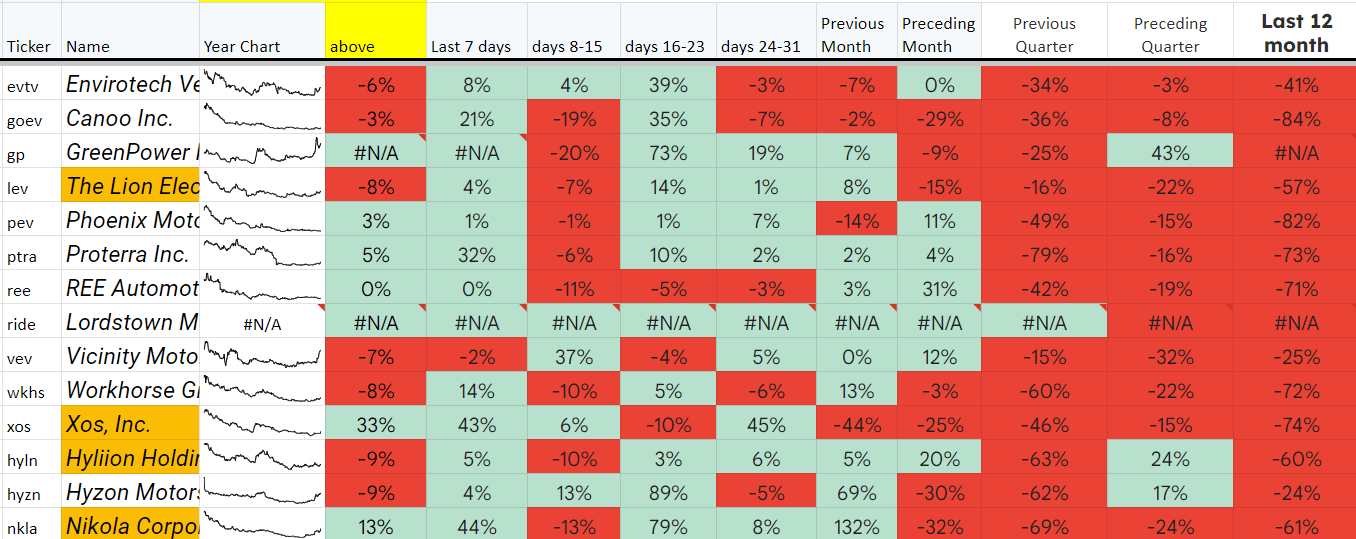

I track 45 Battery Electric Vehicle Companies; most have been public for less than five years and launched during the SPAC craze. XOS was one of these and, like the others, launched with great fanfare, spouting unrealistic timelines, overly optimistic sales forecasts, and some very dubious financial forecasts. Many of these companies are now in serious financial difficulty, taking Tesla ( TSLA ) and the Chinese-based manufacturers from the list. The remaining companies show an average decline of 87% in the last three years, a terrible return for the whole sector. I have holdings in 4 of the companies marked in yellow on this graphic.

{kind=link}

There are probably still too many companies, but some of those that remain are beginning to look like solid investments. Many have ditched the unrealistic timeframes, and most now have a product for sale; the ones I like the look of have found their niche. They no longer claim to be able to produce everything for everyone but offer a specific product to a particular set of customers and are aiming to deliver that product profitably. They could be excellent investments if their target market niche is big enough and their product good enough.

I hope to explain why I think XOS has grown into an investable company with a reasonable probability of success.

The Growth Story

The Initial XOS Business Plan Circa 2020

Xos completed its SPAC deal in 2021 and presented its plans , including 2,000 sales in 2022, rising to 33,674 by 2025. Xos intended to sell medium and heavy-duty last-mile delivery trucks on its X-platform.

XOS products (original prospectus)

The key parts of the plans at the launch were

- Manufacture and sell class 5-8 trucks to the worldwide trucking industry.

- Develop its proprietary battery technology that will deliver best in class range.

- Deliver a fleet as a service platform that would double revenue compared to legacy manufacturers.

- Develop XOS flex, a flexible asset-light manufacturing model that would deliver below-average costs. Plans were to manufacture in Canada, the US, Mexico, Europe, and Asia.

By the end of 2021, with the SPAC deal completed and the plan unchanged. In the Q4 2021 earnings call , the CEO said Xos focused on establishing relationships with key customers, building its manufacturing team, and ramping manufacturing capacity.

In the earnings call, XOS had two XOS FLEX manufacturing sites with 5,000-vehicle capacity.

The second generation of the proprietary battery offering a 50% improved battery density was discussed.

The only major change was the delay in the launch of the class 6/7 and 7/8 vehicles, and they did not make it to market in 2021.

The Plan Circa 2022

Twelve months is a long time for these companies; by the end of 2022 ( FY 2022 earnings ), a very different XOS was presented.

The three focus areas had become growing demand, improving gross margins, and maintaining access to capital.

A diversified battery strategy complemented the proprietary battery tech.

Manufacturing has moved to one site in Tennessee. The traditional factory model replaced the XOS flex manufacturing.

While still part of the XOS plan, the fleet as a service idea had not taken off, and most sales were going through a traditional dealer and direct sales channel.

The international expansion has been sidelined.

XOS was now about the Class 5/6 stepvan, their only product, as the larger trucks had not made it to market, and they intended to grow demand for this product, increase gross margin by cutting costs, and arrive at positive cash flow by building volume.

Stepvans the Market

Stepvans are uniquely North American vehicles; I have rarely seen them in Europe or Asia. I have never seen one outside the UK, where UPS is the sole user of the vehicle type.

An estimated 4.2 million step vans in North America make it a significant market niche. The range issues associated with BEVs are irrelevant for step vans as they are used for last-mile delivery and typically do less than 92 miles per shift ( North American Council for Freight Efficiency P6 ). The NACFF document estimated that an additional 18,000 StepVans would be needed each year due to growing e-commerce demands, increased regulation is likely to mean more and more companies will look at choosing BEV over diesel the entire fleet could become BEV by 2033 when the current fleet will all be more than ten years old. That represents an enormous market; if XOS can capture even a tiny share of it, they will be a large and profitable.

Step vans the competition

Step vans typically have two OEMS- one builds the chassis and drive train the other builds the body. Ford ( F ) and Freightliner are the market leaders for the chassis, with Morgan Olson and Utilimaster dominating the design and installation of the body.

Stepvans are highly customizable; some users require a platform to service postal delivery, others hold cash securely, and others reinforce floors to cope with heavy items. The large end-users have worked with Morgan Olson and Utilimaster to design the needed body. It would be a hard sell to get large-scale users to change the body supplier as well as the chassis and engine supplier.

The New Entrants

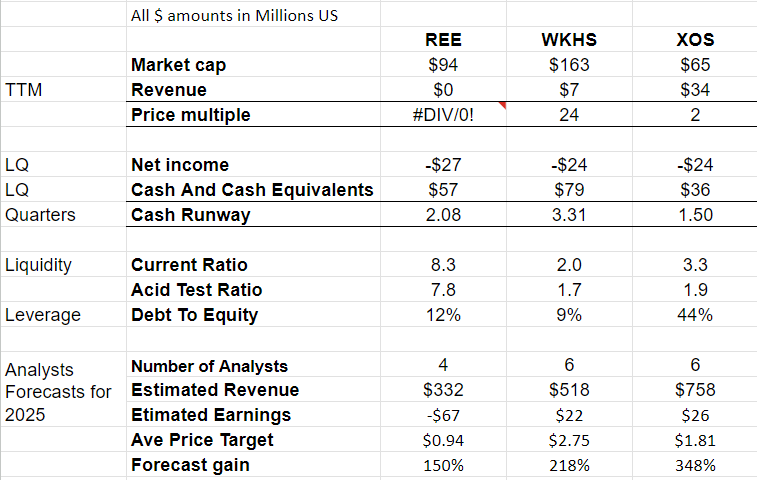

The initial flood of BEV competitors has thinned over the last few years. Lion Electric ( LEV ) appears to focus on school buses, and Greenpower Motor ( GP ) has a focus on its cab and chassis which it sells to Workhorse ( WKHS ) to build into a stepvan. XOS has three main competitors: Ree Automotive ( REE ), WKHS and the private company Motiv. (Here, I am ignoring the large incumbent diesel and gas-powered manufacturers who may develop electric versions)

Ree is an outlier, and its four-wheel drive four-wheel steer platform has many advantages. It has a lower step for the driver, a smaller turning circle, and a flat base for OEMs,s to build on. This video shows the product in action.

Motiv is focused on a smaller class 4 vehicle. It has 105 miles of range and a GVWR of 14,500lbs; however, 175 vehicles sold in 2022 are worth watching if they come to the markets in the future. Motiv also uses Morgan Olsen to build the body and also has a relationship with Utilimaster.

That leaves three horses in this particular race.

{kind=link}

I will discount REE at this point. It currently has no sales, so its product does not have the commercial validation I demand before investing, and with estimated earnings still negative in 2025, it is just too risky. Xos is currently outselling WKHS with a price multiple of only 2 against 30; it seems undervalued. A 350% forecast increase makes it very interesting.

Comparing the products of Xos and WKHS is interesting but not enormously illuminating.

step van comparison (Author)

The only noticeable difference is under the category OEM. Workhorse was working with Morgan Olsen on the C1000 stepvan product, discontinued in 2022 . The current WKHS vehicle is based on the Greenpower Motor ( GP ) EV Star. The EV Star is developing into a monster in the electric van industry; WKHS placed an order in the thousands and is already taking delivery. (I wrote about this deal in my article on GP last month)

XOS and competitive advantage

I think the agreement with Morgan Olsen is almost a guarantee of volume. It is the basis of Xos's largest customer, the FedEx contractor agreement, a repeat order funnel that looks set to grow significantly.

FedEx has an independent contractor supplies operation . On the FedEx contractor business site, the Xos step van is described as

{kind=link}

The FedEx independent contractor must get the Morgan Olson P100 with a Xos drive train. They are not choosing which truck, just how it is powered. Options are available to buy the P1000 with other drive trains, but the only electric one is Xos. The complete list of P1000 trucks available to FedEx contractors is on the link.

FedEx ISP has been a customer since 2021 and has increased its orders annually. Xos is the only electric stepvan on the ISP site and serves the 35,000 independent contractors that keep the FedEx system running. The latest order was for an additional 120 units.

Other Customers

In the 2022 earnings call the CEO said

While step vans are most associated with parcel delivery, with Xos serving independent service providers of two of the largest parcel delivery companies in the world, we also now serve four of the top uniform rental fleets as well as two of the largest US-based beverage fleets in the country.

It is difficult to identify customers of OEMs; names are often not released for commercial purposes. With Morgan Olson step vans, it is even more difficult as even if you saw one, you could not be sure which chassis and drive train it was on as they all look identical.

XOS claim to have two of the world's largest parcel delivery companies as customers. We know one is FedEx, but the other remains undisclosed. I think I may have found evidence that the second customer is Amazon ( AMZN )

Amazon signed a deal to take 10,000 Rivian trucks , I assumed this meant they would not be buying electric vans elsewhere; however, searching through the Morgan Olson Parts website site (looking for lidar/radar for my recent article on ARBE ), I found The Amazon Xos Delivery vehicle (from Sept 2022).

Other major customers

Xos has gained some traction. In February 2023, Loomis (LOOM) ordered 150 Armoured vehicles from XOS; Loomis stated that the 20 vehicles they had at the end of 2022 had outperformed expectations in terms of range, safety, and weight. The 150 new vehicles will operate during the second half of 2023. Loomis stated that they will continue to invest in electric and hybrid vehicles as they renew their global fleet. In the US, Loomis has a fleet of around 3,000 vehicles .

Global uniform and linen delivery service Alsco has ordered 30 vehicles

UniFirst initially bought 3 trucks on a test basis, but with 260 service locations and 300,000 customers, they are a high-potential customer.

Merchants Fleet , a fleet management company, has received 120 Xos stepvans and intends to electrify 50% of their fleet by 2025. Merchant's fleet work with several BEV suppliers, and as yet, no indication of future Xos business has been made public.

XOS received orders for 800 Stepvans in 2022 (earnings call), an increase of more than 500% over 2021.

The Plan 2023

In the shelf prospectus, XOS provided further updates and insight into its plans; the money from the Shelf takes the pressure off the cost-cutting elements of the 2022 plan, and XOS appears to be moving forward with a more rounded product lineup.

Xos as a service, the fleet management package, is again under development. The prospectus does say it has very few customers.

The class 7/8 HD X platform has been launched, and XOS targets vehicles that do less than 200 miles daily. It is a product of the future. The prospectus contained this line.

We plan to continue to develop the HD X-Platforms for future customer use in regional haul fleets with body configurations to include box trucks, refrigerated units, and flatbeds.

Profits?

We heard in the earnings call that moving the business to a profitable operation is one of the three focus points for the next 12 months. The 2023 Stepvan was presented as an example of how changes to the vehicle's design have saved $15,000 per unit (prepared remarks Giordano Sordoni) and how manufacturing has been streamlined to the Tennessee facility. More cost reductions are related to the change in battery strategy.

During Q1 2023, GP came in at -19%; it was -85% in Q4 2022. Kingsley Afemike (CFO now resigned) said they were on track to deliver positive GP by mid-2023 with a combination of cost reductions and price increases, and he quoted 4% as the price increase.

Kingsley promised to share plans on how the company will move from positive GP to positive cash flow in the next earnings call.

Financials and forecasts

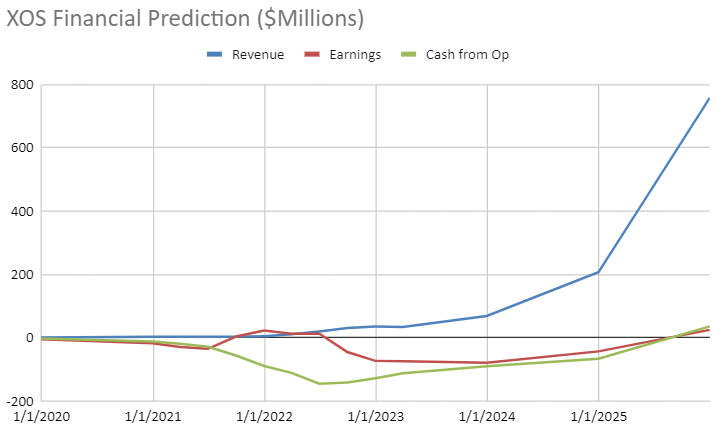

Xos gave unchanged 2023 revenue forecasts suggesting that their manufacturing operation will become GP positive later this year and cash flow positive next. Using information from the analyst's forecasts in the earlier table and averaging with Xos forward guidance, I got.

{kind=link}

It is a significant ramp-up in the year 2025-2026. It is possible with the customers identified and the manufacturing capacity in place. The cumulative loss from today to the cash flow positive forecasted in 2025-2026 is $290 million.

{kind=link}

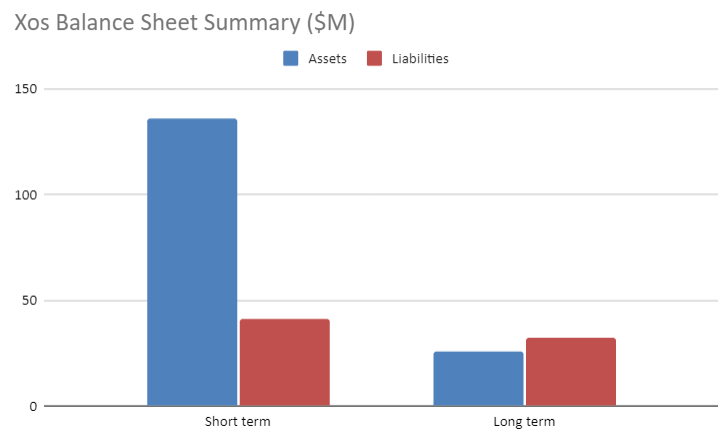

I estimate that Xos is short of around $150 million to reach its profit date. Debt is about $44 million, and equity is $90 million. It was a stated aim in the latest earnings call to manage the company in a way that keeps access to capital markets open. In the past 12 months, dilution was around 4%, but we should expect a larger figure in the coming years.

The Shelf deal makes these plans a reality, the next earnings call scheduled for Aug 10th will be

Conclusion

XOS has focussed on the Stepvan market, a large segment that looks well suited to electrification. I have looked at several customers, all of whom have the potential to order many thousands of vehicles.

The North American stepvan market is growing and might need millions of new trucks over the next decade. Stepvans typically operate in urban areas where regulation forces fleets to electrify while providing financial incentives for them to do so.

Staying with Morgan Olsen for body design means the big fleets get the truck body they want. As long as the XOS part holds up the orders should continue to flow in.

Xos is short of cash and is working hard to improve GP by reducing production costs and increasing selling prices. The plans here will be essential in the upcoming earnings call.

The new shelf prospectus probably means XOS has enough cash to reach profitability. The Shelf is very dilutive, but its effect will depend on what the buyer does with its shares; if it sells, the price will suffer. If the buyer plans to hold onto the shares as an investment, it will likely not be as negative.

The next earnings call is due August 10th. Hopefully, we will get an update on plans and the future.

For further details see:

Xos Makes A Killer Shelf Deal, And I Am Buying More Shares