XPEV - XPeng: EV Slowdown Is Taking A Toll (Rating Downgrade)

2023-07-03 23:12:08 ET

Summary

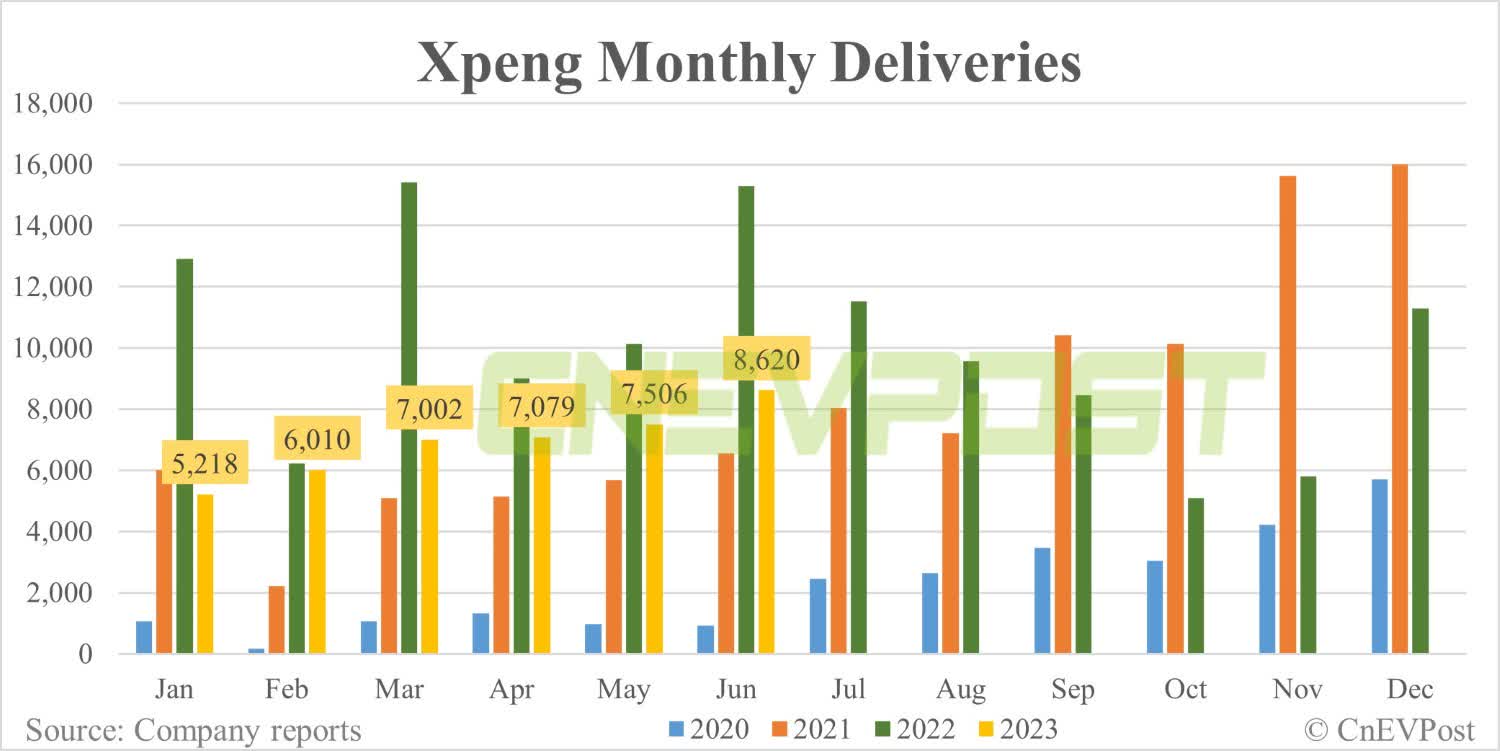

- Chinese EV start-up XPeng has seen a significant downturn in its delivery prospects, with June deliveries down 43% Y/Y due to rising pricing pressure, increased competition and weakening demand.

- The company's Q2'23 outlook is also weak, with expected deliveries between 21,000 and 22,000, a potential Y/Y decline of up to 39%.

- Despite the launch of a new EV, the G6, XPeng's delivery prospects should be expected to remain weak in an increasingly competitive market.

XPeng ( XPEV ) has seen a rather dramatic downturn in its delivery growth rates in the Chinese electric vehicle market this year. The Chinese EV start-up delivered only 8,620 electric vehicles in the month of June, showing a decline of 43% year over year, in part due to rising pricing pressure as well as waning demand for electric vehicles. Although XPeng launched a new electric vehicle product in June, the G6, a Tesla ( TSLA ) Model Y competitor, I believe XPeng’s delivery prospects will continue to remain weak in a market that is seeing much more EV competition than just a year ago. Since XPeng's delivery Q2 delivery outlook disappointed and the company also failed to recharge its delivery growth after the Chinese holiday period, I am down-grading my rating from buy to hold!

XPeng: a new delivery reality

XPeng has seen a sharp deceleration of its delivery growth rates in 2023, in large part because Tesla ignited a price war in the Chinese EV market by lowering prices six times in a bid to spur demand . Tesla has been able to grow its deliveries as a result, but it came at the cost of increasing pricing pressure in the EV market which, combined with a glut of new electric vehicle models, have resulted in a serious deterioration of XPeng’s delivery prospects: in June, XPeng delivered only 8,620 electric vehicles , showing a decline of 43% year over year. However, XPeng saw a 15% month over month increase in deliveries. Although delivery volumes have been rising on a month over month basis in June, XPeng’s monthly delivery volumes in FY 2023 are still far below those of FY 2022.

{kind=link}

XPeng deliveries relative to other EV rivals

XPeng has also performed far worse than its competitors in the industry, Li Auto ( LI ) and NIO ( NIO ).

Li Auto, for the first time ever, broke through the 30,000-electric vehicle delivery barrier in June and saw 150.1% year over year delivery growth. NIO reclaimed the 10,000 delivery threshold in June, while still reporting a delivery decline of 17.4% year over year. XPeng has been the worst performing EV company in the industry group for a while, resulting in XPeng reporting a 50% decline in revenues from vehicle sales to 3.51B Chinese Yuan in the second-quarter. XPeng also submitted a very weak outlook for the second-quarter: the company expects only 21,000 and 22,000 deliveries in Q2'23, showing a potential year over year decline of up to 39%. Li Auto, as shown in the following table, has been by far the best-executing EV company in the industry group.

| Deliveries |

| Apr-23 |

| Apr Y/Y Growth |

| May-23 |

| May Y/Y Growth |

| Jun-23 |

| June Y/Y Growth |

| NIO |

| 6,658 |

| 31.2% |

| 6,155 |

| -12.4% |

| 10,707 |

| -17.4% |

| XPEV |

| 7,079 |

| -21.4% |

| 7,506 |

| -25.9% |

| 8,620 |

| -43.0% |

| LI |

| 25,681 |

| 516.3% |

| 28,277 |

| 146.0% |

| 32,575 |

| 150.1% |

(Source: Author)

Revenue and delivery headwinds, XPeng's officially launches G6 SUV

XPeng has seen a slowdown in revenues just like other EV manufacturers have after the pandemic, and the company’s outlook for the second-quarter strongly suggests that operating conditions will remain challenging for the second half of the year as well. All three EV companies have seen a deceleration of their top lines since the pandemic although Li Auto is faring much better than the competition.

I believe the introduction of XPeng’s latest EV product last month, the G6 sport utility vehicle that is marketed as a Tesla’s Model Y rival, could have a positive impact on the company’s delivery prospects going forward, but the latest EV model is nonetheless getting released into an overall weak market.

XPeng’s G6 is competitively priced, however, costs less than $30,000 and is thereby 20% cheaper than Tesla’s Model Y, China's top-selling EV. A strong reception of XPeng's G6 product could lead to a reacceleration of XPeng’s delivery prospects, but only after mass production starts later in September.

{kind=link}

XPeng officially launched the G6 at the end of June and it is the first EV built on XPeng’s new SEPA 2.0 modular EV architecture. This architecture will be used in future XPeng models as well and allow the company to save money on R&D as well as reduce the launch time it takes to bring new electric vehicles to market. Nonetheless, investors should expect XPeng's delivery picture overall remain challenged in the second half of the year as slowing demand should be expected to remain a consistent headwind for delivery growth rates of EV start-ups.

XPeng’s valuation relative to rivals

XPeng’s delivery potential is currently valued at a price-to-revenue ratio of 1.65X which makes XPeng the most expensive of the three top Chinese EV start-ups. Li Auto, which is currently crushing it, is valued at 1.42X FY 2024 revenues and is currently the best deal in the industry group, in my opinion.

NIO is valued at a P/S ratio of 1.21X and the company recently announced that Abu Dhabi became a strategic investor in the EV company... which I believe is a game-changer . From a valuation perspective, I like Li Auto the most as the EV firm delivers by far the fastest top line and delivery growth. Li Auto is also the only EV company (of the top three mentioned here) that is projected to be profitable in FY 2023 .

Risks with XPeng

Obviously the biggest short term risk is the firm’s execution on the production and delivery front. The second-quarter delivery outlook is not great and neither was the company’s second-quarter earnings release. However, XPeng still has an ace up its sleeve due to the launch of the G6 SUV which could help XPeng achieve a re-acceleration of its delivery growth in the fourth-quarter. Given the aggressive pricing of the G6, however, I would expect continual margin headwinds for XPeng as well as for the sector in general.

Closing thoughts

Considering XPeng’s significant slowdown in delivery growth rates, I can no longer maintain the firm’s buy rating. While I still like XPeng and the company’s delivery potential in the Chinese electric vehicle market, especially regarding the newly launched Tesla rival G6, the overall slowdown in deliveries and the weak outlook for Q2'23 deliveries justify a rating down-grade. XPeng’s G6 does have a lot of potential in the market, in my opinion, but the real impact on the company's financial will not be felt before the fourth-quarter which is when mass production is expected to start!

For further details see:

XPeng: EV Slowdown Is Taking A Toll (Rating Downgrade)