XPEV - XPeng: Ignore The Noise

2023-10-07 01:43:14 ET

Summary

- XPEV's stock price surged recently after the announcement of the strategic partnership with Volkswagen, but it was an overreaction and indicated desperation from investors.

- The company's latest earnings showed a decline in revenue and negative gross margin, raising big concerns about future profitability.

- My valuation analysis suggests the stock is overvalued.

Investment thesis

Despite aging not very well, recent Q3 vehicles deliveries data suggests that my first bearish call about XPeng ( XPEV ) was sound. The stock price surged just a couple of days after my first article went live due to the news related to a strategic partnership with the world's largest car manufacturer, Volkswagen. The German giant invested $700 million in XPEV, which might seem like a big amount of money if we ignore the context that the company burned about a billion dollars between June 2022 to June 2023. I am highly convinced that the spike in the stock price was a huge overreaction and indicates that XPEV's investors are desperate. The decline of above 20% from late July's peak says a lot to me. As a long-term investor, I prefer to ignore the noise. It is better to assess stocks from a fundamental perspective and look at trends instead of separate breaking news. Moreover, my valuation analysis suggests the stock is overvalued. All in all, I assign the stock a "Strong sell" rating.

Recent developments

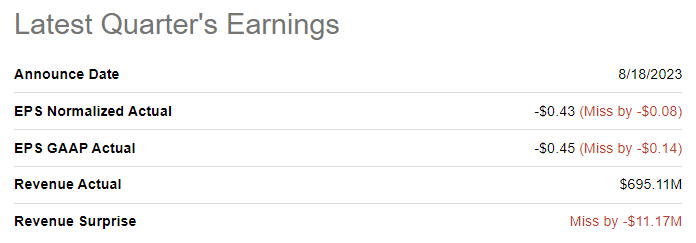

The latest quarterly earnings were released on August 18, when the company missed consensus estimates. Revenue dropped 36% YoY, while the adjusted EPS was almost flat. XPEV's profitability metrics deteriorated dramatically, and the gross margin even went negative. Having a negative operating margin might seem okay, considering the company's early stage of development. Still, a negative gross margin is a huge red flag to me, meaning that vehicle selling prices do not even cover direct costs.

{kind=link}

XPEV's balance sheet might look solid with a $1.7 billion net cash position and a moderate level of debt-to-equity ratio. Near-term liquidity also does not look like a problem. But let me add a little bit of context here. The company's net cash position as of the 2022 year-end was about a billion dollars higher, meaning a massive cash burn rate. If cash burn continues at the same rate, the company is likely to face the need to raise additional finance in 2024. And there will not be good options for equity investors. Either the company will need to obtain debt financing and bear additional costs of servicing the incremental debt amount or it will dilute shareholders by the emission of additional stocks.

Seeking Alpha

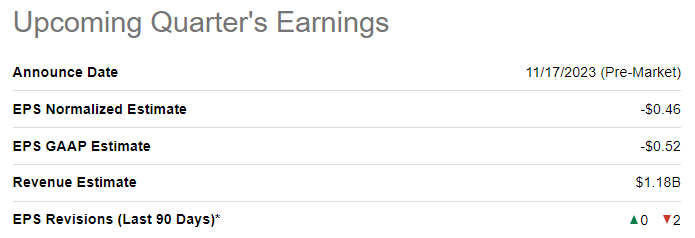

The upcoming quarter's earnings are scheduled for release on November 17. Quarterly revenue is expected by consensus at $1.18 billion, indicating a 23% YoY growth. However, there is little evidence that profitability will improve as the adjusted EPS is expected by consensus to decline both sequentially and YoY.

{kind=link}

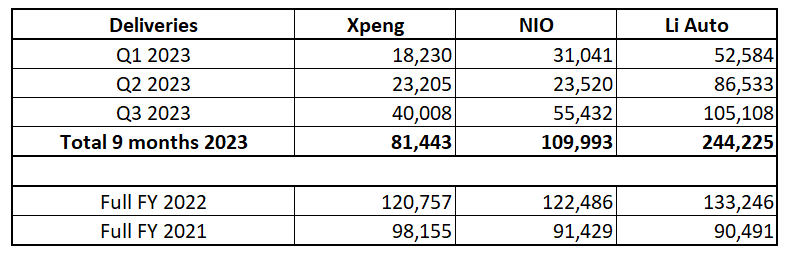

The revenue rebound projected by consensus should not mislead investors. XPeng is significantly lagging behind its closest Chinese peers, NIO ( NIO ) and Li Auto ( LI ). In my latest article about NIO , I revealed its weaknesses, but XPeng's deliveries dynamics are even weaker. It is crucial to underline that two years ago, in 2021, XPeng was leading by a solid margin among these three EV companies. The company lost its leadership compared to its closest rivals and in the first nine months of 2023 delivered three times fewer cars than Li Auto and about 25% less than NIO. XPEV is losing its market share for the benefit of its closest rivals, meaning that its offerings are inferior to competitors.

{kind=link}

And I see no good options for XPEV to boost its sales and make a comeback. The company theoretically could have offered discounts for its vehicles but the probability of it is close to zero given that its profitability metrics are by far worse than the ones of NIO and LI. Providing discounts will further deepen the company's losses and will rapidly drain its balance sheet. As Tesla continues its price war and its closest Chinese rivals ramp up much faster, I think that XPEV is highly unlikely to demonstrate a turnaround in these circumstances.

Valuation update

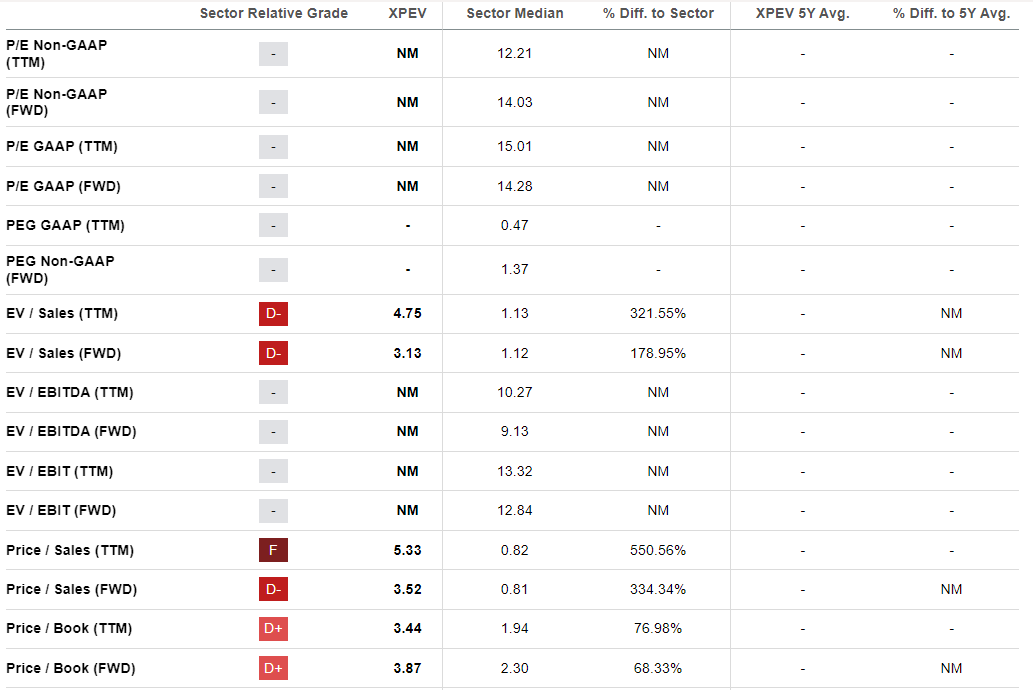

The stock rallied 76% year-to-date, significantly outperforming the broader U.S. stock market. Seeking Alpha Quant assigns the stock a low "D" valuation grade because its valuation ratios are multiple times higher than the sector median. A substantial portion of valuation ratios are inapplicable because the company is far from achieving profitability.

{kind=link}

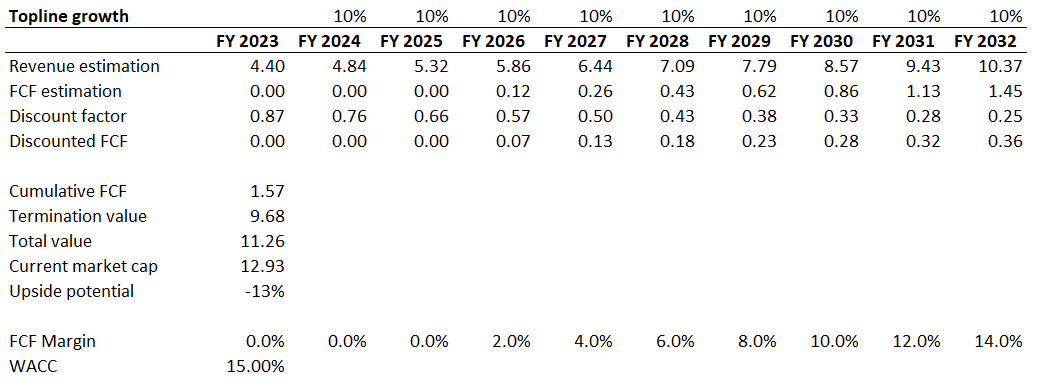

For a young growth company like XPEV multiple, only analysis is insufficient to make judgments regarding the attractiveness of the valuation. That said, I must simulate a discounted cash flow [DCF] model to get more conviction. I use an elevated 15% WACC for discounting, considering country risks and a high level of uncertainty regarding the timing for XPEV achieving profitability. I expect a 10% revenue CAGR for the next decade, which is relatively positive considering the company's weak fundamentals. I expect the FCF margin to turn positive in FY 2026, which is in line with consensus EPS estimates . I project a two percentage point yearly FCF margin expansion.

{kind=link}

According to my DCF simulation, the business's fair value is about $11.3 billion, which is 13% below the current market cap. I ignore the company's current solid net cash position because XPEV is still burning cash, and the outstanding amount will be utilized in the next quarters.

The big risk to my bearish thesis

I am highly convinced that XPeng is fundamentally weak, and its long-term prospects are very cloudy. However, my high conviction does not guarantee that unexpected stock price spikes will never happen. I was unlucky to share my first thesis just a few days before the stock price spike after news regarding the strategic partnership with Volkswagen was released. Market overreactions work on both sides, and sudden good news might lead to another short-term rally. But it is also essential to understand that the weaker the company is from a fundamental perspective, the less likely the stock price rally will be sustainable.

Bottom line

To conclude, XPEV is a "Strong sell". The company's financial performance is poor with revenues hardly covering the cost of goods sold, which is draining XPeng's balance sheet rapidly. The company lost its solid leadership among the three popular Chinese EV startups and is now lagging by a wide margin, softly speaking. XPEV is likely to face liquidity problems as early as next year and it will be choosing between two bad options to continue as a going concern. Moreover, my valuation analysis suggests that the stock is overvalued.

For further details see:

XPeng: Ignore The Noise