XPEV - XPeng: The Risk/Reward Has Now Become Favorable

Summary

- XPeng could be well positioned to capture an attractive share of the fast-growing and large market for EVs.

- Especially given the company's focus on innovation and cost competitiveness.

- XPeng missed its 2022 delivery target due to COVID-19 restrictions in China.

- With reset expectations, the company may now deliver upside as compared to sentiment.

- Personally, I value XPeng stock based on a residual earnings model and calculate a fair value for XPEV stock of $14.23/share.

Thesis

In May 2022, I argued that XPeng ( XPEV ) was overvalued and I advised against investing in the Chinese EV maker at levels above a $9.04/share target price. Now, with the glamour of electric vehicles under pressure, and XPEV stock trading close to my previously guided target price, I feel it is an excellent time to revisit the investment thesis for XPeng.

Reflecting on a more reasonable valuation, paired with a positive outlook for China's EV market through 2030 and likely also beyond, I update my valuation model for XPEV; and I now calculate a fair implied target price of $14.23/share. I assign a 'speculative Buy'.

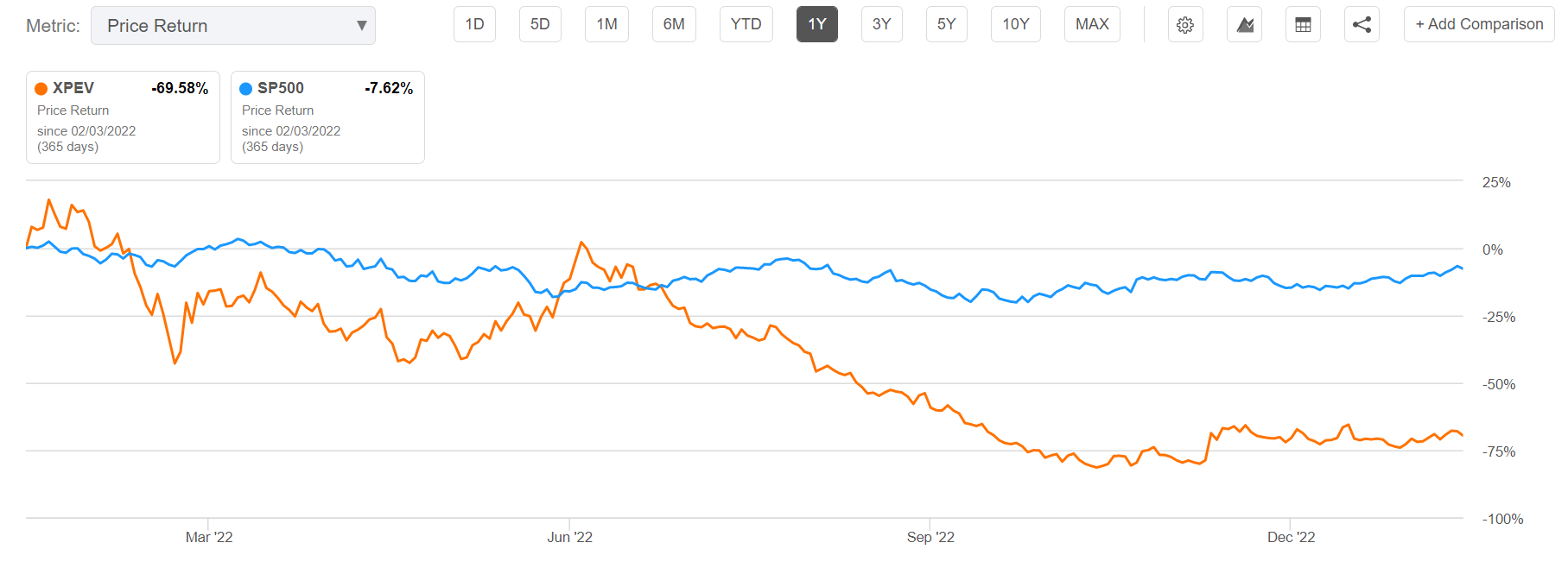

For reference, XPEV stock is down approximately 70% for the past twelve months, as compared to a loss of about 8% for the S&P 500 ( SPY ).

{kind=link}

Favorable Market Tailwind

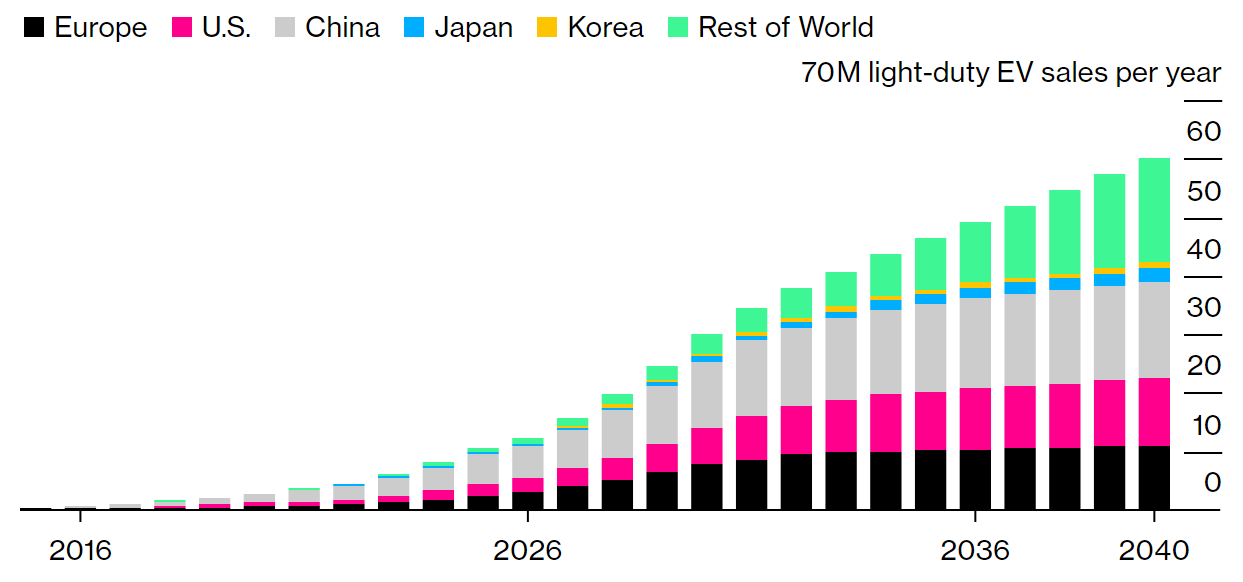

The EV market has lost lots of its glamour, after the stock prices of leading EV makers lost between 50% and 80% of their market capitalization, and after Tesla (TSLA) started to cut prices of model 3 and Y--which could be seen as the start of a potential price war. However, judged from a structural perspective, the market for electric vehicles continues to enjoy a strong growth tailwind, as governments around the world introduce regulations aimed at reducing carbon emissions, and consumers become more environmentally conscious. Furthermore, with advancements in battery technology and the decreasing cost of EVs, the growth of the market is likely to continue, making EVs increasingly accessible to a wider range of consumers. Notably, according to Bloomberg estimates, the EV market could support close to 30 million EVs by 2030, and likely as much as 70 million by 2040.

{kind=link}

While XPeng is a relatively young brand in the automotive industry, the company is, in my opinion, well positioned to capture an attractive opportunity in the fast-growing EV market. Innovation is a major argument for my optimism, as XPeng continues to push towards connected and autonomous mobility--searching for opportunities also beyond automobiles (see here , and here). In addition, cost competitiveness is certainly also an advantage that favors Xpeng. The costs of producing EVs in China are reportedly much lower than in other countries, due to cheap labor costs, a favorable manufacturing environment, and government incentives to encourage the development of the EV industry (for reference, it is no secret how supportive Gigafactory 3/ Shanghai is to Tesla's profitability margins).

Despite the positive market tailwind, investors should consider, however, that the EV market remains highly competitive. And many potential customers, including customers located in China, still tend to prefer western and established brands such as Tesla, Volkswagen, and BMW. As of 2022, XPeng's P7 ranked only as the country's 10th best-selling EV, while Tesla's Model 3 and Model Y ranking 2nd and 3rd, respectively.

Estimates Now More Reasonable

XPeng missed delivery estimates in 2022, shipping only 120,757 cars, as compared to a target of 250,000. Investors should consider, however, that XPeng was greatly impacted by the restrictions and lockdowns imposed due to the COVID-19 pandemic in China, as the company's sole factory and many critical suppliers are located in Guangdong and Shanghai. These regions were among the most affected by the restrictions. According to a recent interview , XPeng's Chief Executive Officer He Xiaopeng pushed back the company's profitability goal of breaking even to 2025, as compared to early 2024 prior.

XPeng's deliveries miss and break-even push back are not necessarily bearish. In fact, I argue the company was too ambitious in expanding production and supporting investor sentiment with stretched targets. Now, with expectations reset to more reasonable expectations, XPeng could be well positioned to deliver upside.

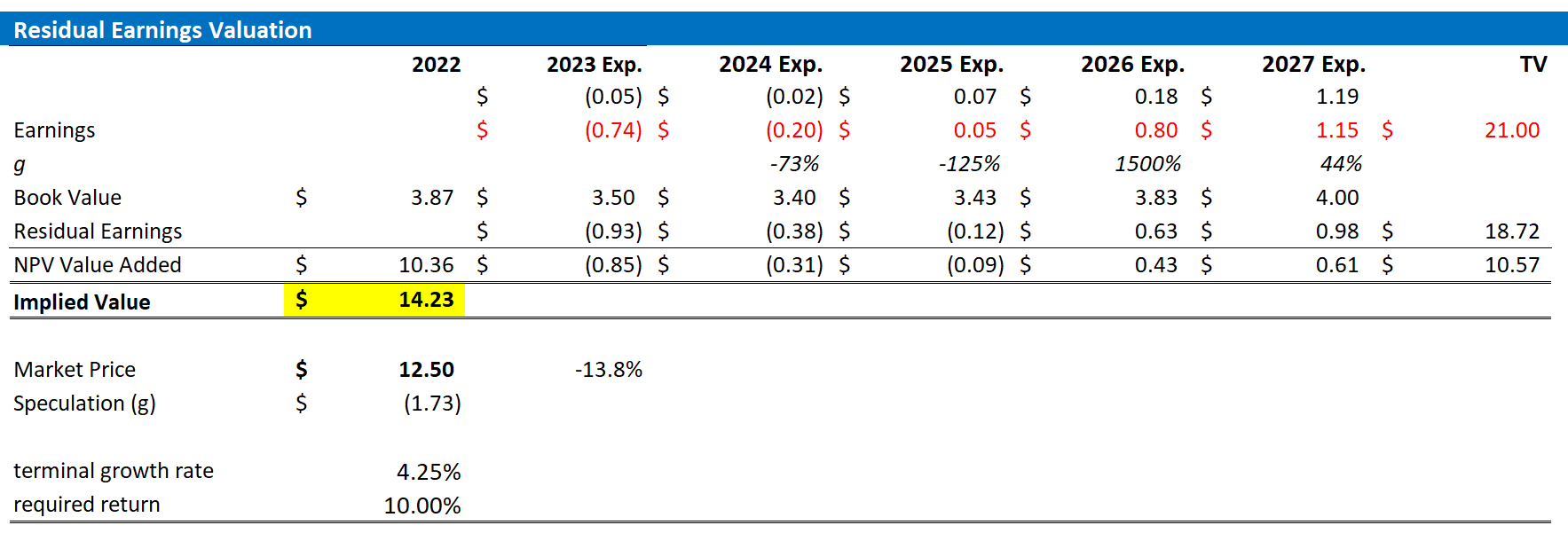

Valuation Update: Raise Target To $14.23

I now estimate that XPEV's EPS in 2023 will likely fall to somewhere between $-0.9 and $-0.6. In addition, I slightly lower my EPS expectations for 2024 to $-0.20. I now model that XPeng will likely achieve operating profitability in 2025, generating EPS of approximately $0.05, with accelerating profitability thereafter.

Reflecting on a positive outlook for China's EV market through 2030, which is not fully captured in my EPS estimates until 2027, I raise my expectations for a reasonable terminal growth rate to 4.25% (about two percentage point higher than estimated nominal global GDP growth, but still well below the past cyclical adjusted GDP growth in China). I continue to anchor on a 10.5% cost of capital.

Given the model updates as highlighted below, I now calculate a fair implied share price of $14.23.

(topline numbers highlight my post-Q2 2022 assumptions)

Author's EPS estimates; Author's calculation

{kind=link}

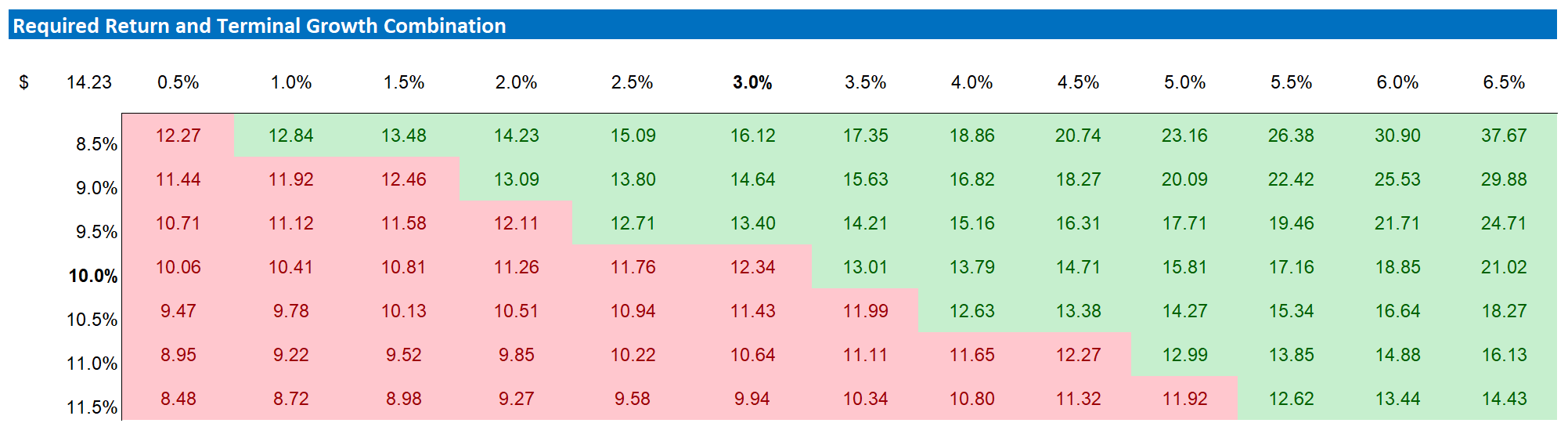

Below is also the updated sensitivity table.

Author's EPS estimates; Author's calculation

{kind=link}

Downside Risks

As I see it, there has been no major risk-updated since I have last covered XPEV stock. Thus, I would like to highlight what I have written before :

First, XPeng is a loss-making company and there is no guarantee the company will reach profitability in 2024, if ever. Second, as the company is investing heavily in R&D, there is no guarantee that the company's innovation efforts - e.g., autonomous driving and flying cars--will ever materialize. Third, XPeng is based in China. Although the CCP currently acts favorably towards EV companies, this may change in the future. Investors should keep in mind that XPeng collects and operates with lots of customer data, which is a dimension that both the CCP and the EU are looking to regulate more effectively. Finally, the ongoing economic challenges in China such as inflation, the real estate crisis and low consumer confidence will definitely add a transitory headwind to XPeng's short-/medium-term operations.

Conclusion

XPeng could be well positioned to capture an attractive share of the fast-growing and large market for EVs, given the company's focus on innovation and cost competitiveness. XPeng missed its 2022 delivery target due to COVID-19 restrictions in China, but with reset expectations, the company may now deliver upside as compared to sentiment. The company is estimated to reach operating profitability in 2025.

Personally, I value XPeng stock based on a residual earnings model and my calculation indicates that the fair value for XPEV stock is likely somewhere around $14.23 /share. I upgrade XPEV to a 'speculative Buy'.

For further details see:

XPeng: The Risk/Reward Has Now Become Favorable