XPEV - XPeng: Time To Sell

2023-07-21 09:29:40 ET

Summary

- XPeng's stock price has almost doubled since early June due to above guidance Q2 deliveries and a launch of a new model G6.

- At the same time, Chinese EV market is cooling down and too optimistic growth expectations are priced in.

- My valuation analysis suggests that the recent massive rally gives investors an excellent opportunity to sell this overvalued stock.

Investment thesis

XPeng's (XPEV) stock price has almost doubled since the early June lows. There were two significant catalysts: introducing a G6 SUV , and above-the-guidance Q2 deliveries. But, as reasonable investors, we should not forget that the company is still burning cash, and its delivery numbers suggest that the company is losing competition to its closest rivals represented by hot Chinese EV startups like NIO (NIO) and Li Auto (LI). Moreover, very aggressive revenue growth assumptions are already priced in, and my valuation analysis suggests the stock is overvalued. All in all, I assign the stock a "Sell" rating

Company information

XPeng is a Chinese EV company that designs, develops, manufactures, and markets Smart EVs. The company currently offers six models: SUVs of different sizes, sports sedans, and a family sedan.

The company's fiscal year ends on December 31 with a sole operating and reportable segment.

Financials

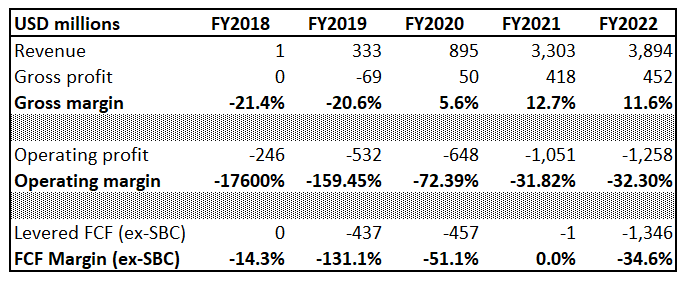

The company went public relatively recently , so we do not have a long horizon for the financial analysis. Revenue demonstrated a staggering growth with a more than ten-fold increase between 2019 and 2022. As the business scaled up, profitability metrics expanded significantly. Though the operating loss is still substantial, and the gross margin is razor-thin.

{kind=link}

The company invests heavily in R&D. Last year, these expenses represented about 20% of the total sales, which is substantial. The company is still burning cash, with negative cash from operations of about $1.2 billion in FY 2022. The balance sheet looks solid, with a $1.47 billion net cash position and decent liquidity metrics. But if the company will have one more year with above $1 billion in negative cash from operations, it will face the need to raise additional capital. This will weigh on the company's future earnings or might dilute shareholders, which is bad for investors.

Seeking Alpha

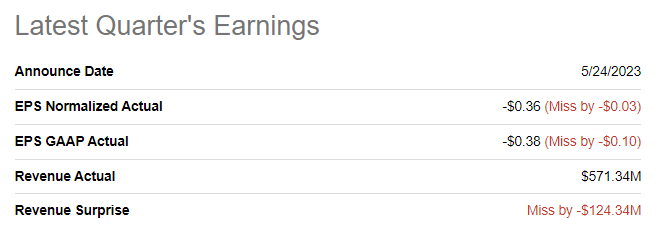

The latest quarterly earnings were released on May 24, and the company significantly missed consensus estimates. Revenue almost halved on a YoY basis and the EPS also decreased. In Q1 the company delivered 18,230 cars which was 47% below YoY.

{kind=link}

The upcoming earnings release is scheduled on August 23. The quarterly revenue is expected at $758 million, which is about 30% lower than the same quarter last year. On the other hand, the EPS is expected to improve slightly. The company is likely to miss consensus revenue estimates again because its deliveries YoY decline was slightly higher than 30% with a 33% decrease in the number of cars delivered during Q2.

Valuation

The stock significantly outperformed the broader U.S. market and iShares MSCI China ETF ( MCHI ) with a 45% year-to-date rally. Seeking Alpha Quant assigns the stock a "C-" valuation grade due to the high valuation multiple compared to the sector median. The stock might look overvalued based on multiples, but it is a growth stock that is rather far from generating profits. Therefore, multiples analysis might not be the best option and I need to run a discounted cash flow [DCF] simulation.

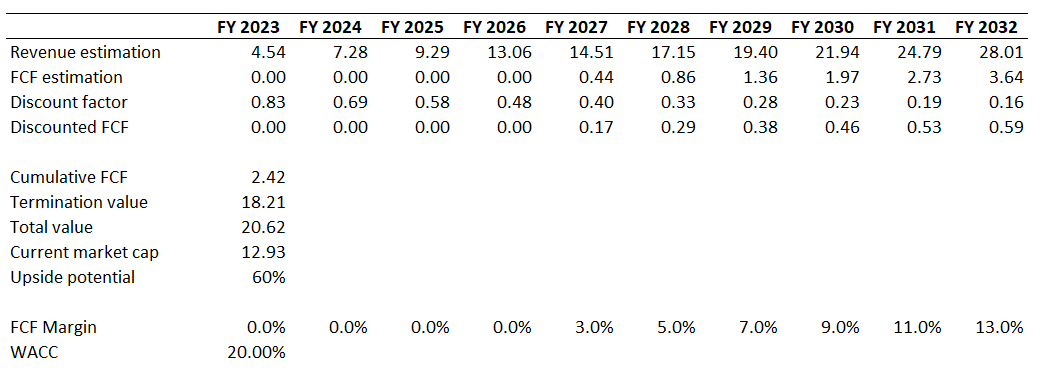

I use a massive 20% WACC due to two reasons. First, the company is very far from a break-even and the cash-burn rate is massive. Second, investing in Chinese companies is riskier due to substantial political risks. I have very ambitious earnings consensus estimates projecting a 20% revenue CAGR for the next decade. The FCF margin is very tricky for companies far from profitable. I expect FY 2027 to be the first year with a positive FCF margin and expect it to expand by two percentage points yearly.

{kind=link}

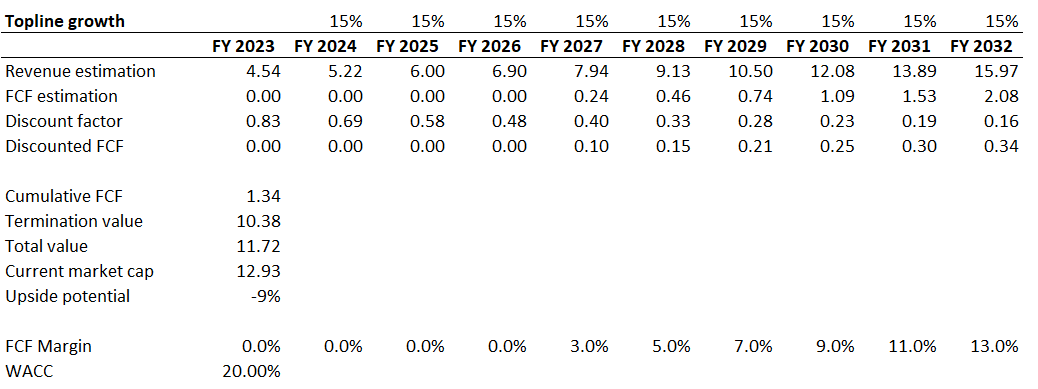

The DCF model suggests the stock is about 60% undervalued, but consensus revenue estimates are too optimistic. I think so because the projected 20% revenue CAGR is higher than the growth expectations for the overall Chinese EV market. For example, fortunebusinessinsights.com forecast an 18.4% CAGR for the Chinese EV market. The competition in the Chinese EV market and I expect it to intensify. XPeng's delivery numbers are much lower than his closest rivals, NIO and Li Auto, demonstrate. There are also two EV giants with a massive presence in China. The local giant is BYD (BYDDF), and the undisputed global EV leader is Tesla ( TSLA ). European giants like Volkswagen and Volvo also have their plants or joint ventures in China. That said, it is highly unlikely that XPeng's revenue will grow in line with the total EV market of China. Therefore, I think that a 15% revenue CAGR would be more fair for my DCF simulation. A 15% revenue growth rate over a decade is still an aggressive assumption. Other assumptions will be untouched for the second scenario.

{kind=link}

The stock now looks overvalued, with a 15% annual revenue compounding. Based on the overall Chinese EV market growth projections, I believe that the second DCF scenario is closer to reality than the first one. Thus, I think that the stock is not attractively valued.

Risks for XPeng investors

XPeng is a growth company, and massive revenue growth expectations are priced in. There is also a very high level of uncertainty regarding when the company will start generating sustainable positive free cash flow. Any signs of a substantial revenue growth deceleration are highly likely to lead to investors' disappointment which could result in a massive sell-off.

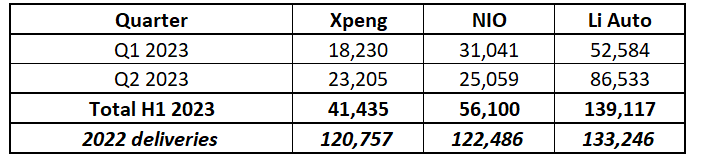

The company faces fierce competition. The Chinese EV market is one of the most competitive in the world. Tesla and many other Global legacy automotive giants either have their plants in China or have strategic partnerships with local plants to produce EVs. I think that the best metric to demonstrate that XPeng is losing market share to its closest competitors, NIO and Li Auto, is delivery numbers. During the first half of this year, XPeng delivered 35% fewer vehicles than NIO, and more than three times fewer than Li Auto. Please also pay attention that during the full 2022, the gap between the three companies was not as wide as it is in the first half of 2023.

{kind=link}

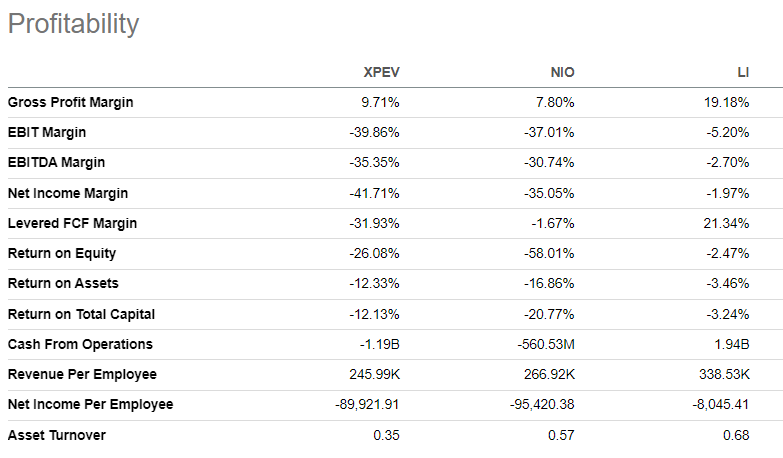

The second important criterion which I would like to demonstrate XPeng's weakness compared to NIO and Li Auto is profitability. As you can see below, Li Auto is much more profitable, since it enjoys economies of scale effect. XPeng's and NIO's profitability metrics are close to each other, but please pay attention that XPeng loses two times more cash on operations than NIO does.

{kind=link}

To conclude, I believe that there is a very high risk that, over the long-run XPEV will not be able to resist competition even from local Chinese EV startups.

Risks to my bearish opinion

Markets are not always rational, and it is common when the stock continues to demonstrate growth despite weak fundamentals, usually based either on hype or investors' fear of missing out [FOMO]. But, over the long term, fundamentals are the main driver for the long-term stock price movement. The company's new G6 SUV indeed might be an absolute hit for the Chinese EV market, and the company might rapidly close the gap in delivery numbers. But I think that this risk is low because sales of cars heavily depend on the broader economy's health, and the Chinese economy recovers substantially slower than it was expected. We also should not forget that XPEV loses substantial amounts of money on each car it sells. That said, the company will face the need to balance production ramping up and the available financial reserves. Otherwise, additional financing will be needed, which will also weigh on the costs side.

Another risk to my thesis relates to some hard-to-predict good news for XPeng. For example, in June, I also had a bearish call about NIO , due to weak fundamentals as well. And just a few days after my article went live, the news regarding a billion-dollar investment in NIO from the Abu Dhabi fund was a big catalyst for the stock's short-term bull run. I am still bearish on NIO, but from a short-term perspective, it looks like my thesis was wrong. That is also a substantial risk to my bearish opinion about XPeng.

Bottom line

Overall, I think that the stock is a "Sell" after a massive rally, which started in early June. The company is still far from turning profitable, and delivery numbers are weaker than the ones its closest competitors demonstrate. The demand growth for EVs in China is decelerating due to the challenging macro environment. I think that a pullback, especially after XPeng's stock's massive rally, is highly likely. Last, based on my DCF analysis, the stock is overvalued.

For further details see:

XPeng: Time To Sell