CA - Yields Up To 10%: My Top 10 High Dividend Yield Companies For November

2023-11-15 16:00:00 ET

Summary

- While investing in companies that pay relatively high dividends provides you with several benefits, it often comes attached to an elevated risk-level.

- A careful selection process is essential for identifying high yield companies that pay sustainable dividends, have significant competitive advantages, are financially healthy, and have an attractive valuation.

- In today’s article, I will present you with 10 high dividend yield companies which I believe are presently appealing for investors, and worth considering investing in.

Investment Thesis

When searching for high dividend yield companies for potential inclusion in your investment portfolio, there are a number of factors to consider. In the following, I will list some of them for you:

- Strong Competitive Advantages and Financial Health: The company should have strong competitive advantages and be financially healthy to stand out against the competition. This criterion is important for you as an investor, since it helps to safeguard your investment. Should the company be unable to distinguish itself from competitors, the likelihood of losing your investment in the future would significantly increase. My investment approach (reflected through The Dividend Income Accelerator Portfolio ), puts the preservation of your capital in first place.

- Attractive Valuation for a Margin of Safety: The Valuation of the company should be attractive. This helps us to achieve rewarding investment outcomes over time. At the same time, it helps you as an investor to establish a margin of safety when investing.

- Sustainability of the Dividends: Selecting companies that pay sustainable dividends also ensures that you can invest with a margin of safety. Such companies tend to offer a lower risk of dividend reduction, which would negatively affect the company’s stock price. Companies that pay sustainable dividends are typically characterized by a relatively low Payout Ratio, a historical track record of dividend growth, and attractive growth prospects.

During the selection process for the incorporation of companies into The Dividend Income Accelerator Portfolio, I am carefully considering these factors before deciding to add additional companies. The Dividend Income Accelerator Portfolio specifically targets companies that can maintain sustainable dividends, thereby enhancing the likelihood of rewarding investment outcomes, and producing robust income streams with a low risk-profile. These are the principal characteristics of The Dividend Income Accelerator Portfolio.

The focus of this article is to present you with a carefully selected list of high dividend yield companies that are presently worth considering investing in.

Since I have already described the detailed selection process in a previous article , if you are already familiar with it you can skip the following section written in italics.

First Step of the Selection Process: Analysis of the Financial Ratios

In order to identify companies with a relatively high Dividend Yield [FWD], I use a filter process to make a pre-selection. From this pre-selection, I will later choose my top 10 high Dividend Yield companies of the month. To be part of this pre-selection of high Dividend Yield stocks, the companies should fulfil the following requirements:

- Market Capitalization > $10B

- Dividend Yield [FWD] > 2.5%

- P/E [FWD] Ratio < 30

In the following, I would like to specify why I have chosen the metrics mentioned above in order to select my top 10 high Dividend Yield stocks of the month.

A Market Capitalization of more than $10B contributes to the fact that the risks attached to your investments are lower, since companies with a higher Market Capitalization tend to have a lower volatility than companies with a low Market Capitalization.

A P/E [FWD] Ratio of less than 30 implies that the price you pay for the company is not extraordinarily high, thus filtering out those that have stock prices in which high growth expectations are priced in. High growth expectations imply strong risks for investors, since the stock price could drop significantly. Again, the filtering process helps us to reduce the risk so that we are more likely to make an excellent investment decision.

Second Step of the Selection Process: Analysis of the Competitive Advantages

In a second step, the companies’ competitive advantages (for example: brand image, innovation, technology, economies of scale, etc.) are analyzed in order to make an even narrower selection. I consider it to be particularly important for companies to have strong competitive advantages in order to stand out against the competition in the long term. Companies without strong competitive advantages have a higher probability of going bankrupt one day, thus representing a strong risk for investors to lose their invested money.

Third Step of the Selection Process: The Valuation of the Companies

In the third step of the selection process, I will dive deeper into the Valuation of the companies.

In order to conduct the Valuation process, I use different methods and criteria, for example, the companies’ current Valuation as according to my DCF Model, the expected compound annual rate of return as according to my DCF Model and/or a deeper analysis of the companies’ P/E [FWD] Ratio. These metrics should serve as an additional filter to only select companies that currently have an attractive Valuation, which helps you to identify companies that are at least fairly valued.

The Fourth and Final Step of the Selection Process: Diversification Over Industries and Countries

In the fourth and final step of the selection process, I have established the following rules for choosing my top picks: in order to help you diversify your investment portfolio, a maximum of two companies should be from the same industry. In addition to that, there should be at least one pick that is from a company that is based outside of the United States, serving as an additional geographical diversification.

My Top 10 High Dividend Yield Companies to Consider Investing in for November 2023:

- Altria Group (MO)

- United Parcel Service (UPS)

- Verizon Communications (VZ)

- Pfizer (PFE)

- Canadian Imperial Bank of Commerce (CM)

- Axa (AXAHY) (AXAHF)

- Morgan Stanley (MS)

- Iberdrola (IBDSF)

- Ares Capital (ARCC)

- Suncor Energy (SU)

Overview of the 10 Selected High Dividend Yield Companies to Consider Investing in for November 2023

| PFE |

| VZ |

| UPS |

| MO |

| CM |

| AXAHY |

| MS |

| IBDSF |

| ARCC |

| SU |

| Company Name |

| Pfizer |

| Verizon |

| United Parcel Service |

| Altria |

| Canadian Imperial Bank of Commerce |

| AXA |

| Morgan Stanley |

| Iberdrola |

| Ares Capital |

| Suncor Energy |

| Sector |

| Health Care |

| Communication Services |

| Industrials |

| Consumer Staples |

| Financials |

| Financials |

| Financials |

| Utilities |

| Financials |

| Energy |

| Industry |

| Pharmaceuticals |

| Integrated Telecommunication Services |

| Air Freight and Logistics |

| Tobacco |

| Diversified Banks |

| Multi-line Insurance |

| Investment Banking and Brokerage |

| Electric Utilities |

| Asset Management and Custody Banks |

| Integrated Oil and Gas |

| Market Cap |

| 166.46B |

| 150.13B |

| 117.66B |

| 70.78B |

| 34.83B |

| 64.73B |

| 123.64B |

| 71.00B |

| $11.17B |

| 42.97B |

| Dividend Yield [FWD] |

| 5.56% |

| 7.45% |

| 4.69% |

| 9.80% |

| 6.83% |

| 6.25% |

| 4.51% |

| 3.72% |

| 9.79% |

| 4.63% |

| Dividend Yield [TTM] |

| 5.56% |

| 7.34% |

| 4.69% |

| 9.50% |

| 6.78% |

| 6.25% |

| 4.31% |

| 4.68% |

| 9.79% |

| 4.64% |

| Payout Ratio |

| 56.79% |

| 54.41% |

| 64.25% |

| 76.77% |

| 53.36% |

| - |

| 55.11% |

| - |

| 80.67% |

| 36.58% |

| Dividend Growth 3 Yr [CAGR] |

| 4.43% |

| 1.98% |

| 17.06% |

| 3.98% |

| 5.99% |

| 7.47% |

| 32.41% |

| 40.06% |

| 6.27% |

| 16.27% |

| Dividend Growth 5 Yr [CAGR] |

| 4.95% |

| 2.02% |

| 12.23% |

| 5.85% |

| 4.48% |

| 8.03% |

| 24.19% |

| - |

| 4.65% |

| 7.33% |

| P/E [FWD] |

| 18.85 |

| 7.98 |

| 16.37 |

| 8.69 |

| 9.67 |

| - |

| 13.37 |

| 15.53 |

| 7.66 |

| 8.25 |

| Net Income Margin |

| 15.29% |

| 15.58% |

| 9.19% |

| 42.60% |

| 22.51% |

| 6.52% |

| 18.37% |

| 8.58% |

| 50.37% |

| 16.26% |

| 24M Beta |

| 0.53 |

| 0.37 |

| 1.01 |

| 0.41 |

| 0.96 |

| 0.89 |

| 1.03 |

| 0.52 |

| 0.83 |

| 1.1 |

Source: The Author, data from Seeking Alpha

Morgan Stanley

I consider Morgan Stanley to be a compelling choice for investors due to its combination of dividend yield and dividend growth. This positions the U.S. bank as a promising candidate for inclusion into The Dividend Income Accelerator Portfolio.

Morgan Stanley’s current Dividend Yield [FWD] stands at 4.51%, being 9.96% above the Sector Median. At the same time, its current Dividend Yield stands 49.40% above its five-year average, suggesting that the bank is currently undervalued.

It is further worth noting that Morgan Stanley has shown excellent metrics in terms of dividend growth: its 5 Year Dividend Growth Rate [CAGR] stands at 24.19%. The same is at 32.16% when considering the past 10 years.

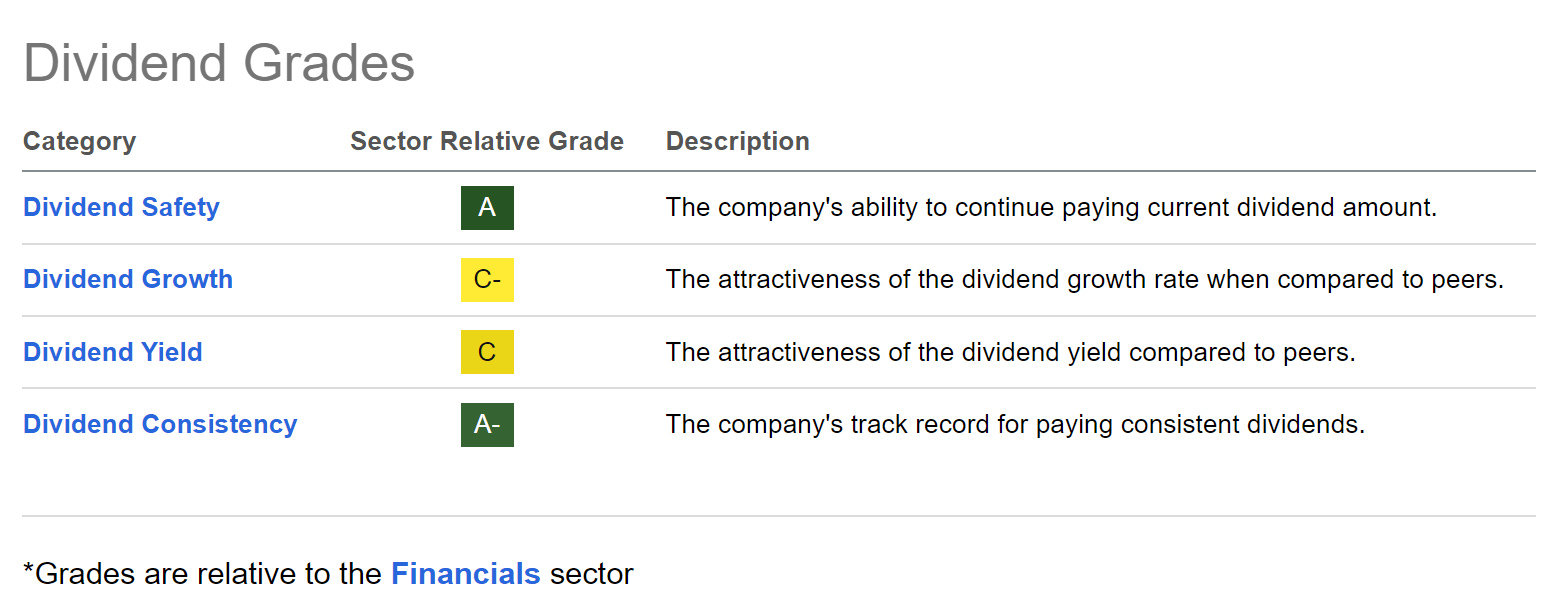

The Seeking Alpha Dividend Grades further confirm Morgan Stanley’s robust Dividend. The U.S. investment bank gets an A rating for Dividend Safety, an A- for Dividend Consistency, a C for Dividend Yield, and a C- for Dividend Growth.

{kind=link}

Axa

The French company from the Multi-Line Insurance Industry, offers its clients insurance, asset management, and banking services . The company was founded in 1852, is headquartered in Paris, and currently has a Market Capitalization of $64.73B.

Axa presently has a P/E GAAP [TTM] Ratio of 9.46, which is only slightly above the Sector Median of 9.25, suggesting that the company is at least fairly valued. The same is confirmed when looking at its Dividend Yield [TTM] of 6.25%, which is in line with its average from the past 5 years (which is 6.52%).

At this moment of writing, the French insurance company has a Free Cash Flow Yield [TTM] of 14.79%, which shows that its current price is not based on high growth prospects. Moreover, this suggests that it is an attractive investment choice for investors seeking companies with a favorable risk/reward ratio.

Not only does the French insurance company pay an attractive Dividend Yield [FWD] of 6.25%, it also shows appealing metrics when it comes to dividend growth. The company has a 5 Year Dividend Growth Rate [CAGR] of 8.03%. These metrics make Axa a candidate for potential inclusion into The Dividend Income Accelerator Portfolio.

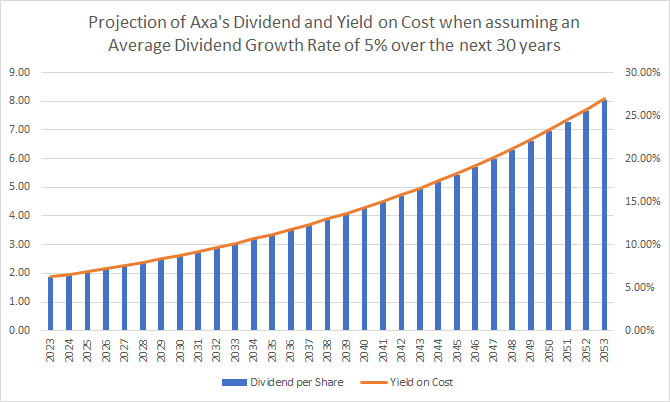

Below you can find a projection of Axa’s Dividend and Yield on Cost when assuming that the company was able to raise its Dividend by 5% per year on average for the following 30 years.

{kind=link}

The graphic indicates that Axa is a promising pick for investors aiming to blend dividend income and dividend growth. This further bolsters my belief that it is a strong candidate for future inclusion into The Dividend Income Accelerator Portfolio.

Ares Capital

Ares Capital has been among my latest acquisitions for The Dividend Income Accelerator Portfolio . I am convinced that this business development company [BDC] is presently an appealing pick for investors, particularly due to its high Dividend Yield [FWD] of 9.79%, its 3 Year Dividend Growth Rate [CAGR] of 6.27%, and its current Valuation. At this moment in time, Ares Capital’s Market Price of $19.61 is only 3.26% above its NAV, suggesting that it is currently fairly valued.

These metrics played a major role in the inclusion of Ares Capital into The Dividend Income Accelerator Portfolio, and its selection in this list of high dividend yield companies to consider investing in during the month of November 2023.

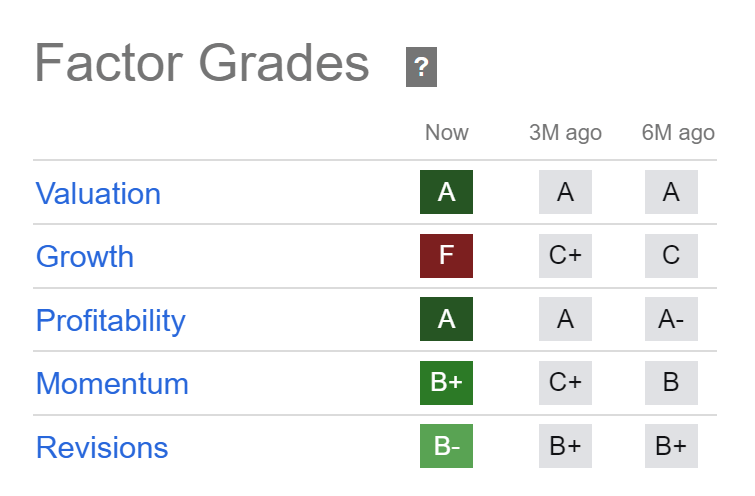

The Seeking Alpha Factor Grades underscore my theory that Ares Capital is an attractive option to consider investing in. The company receives an A rating for Valuation and Profitability, a B+ for Momentum, and a B- for Revisions.

{kind=link}

Canadian Imperial Bank of Commerce

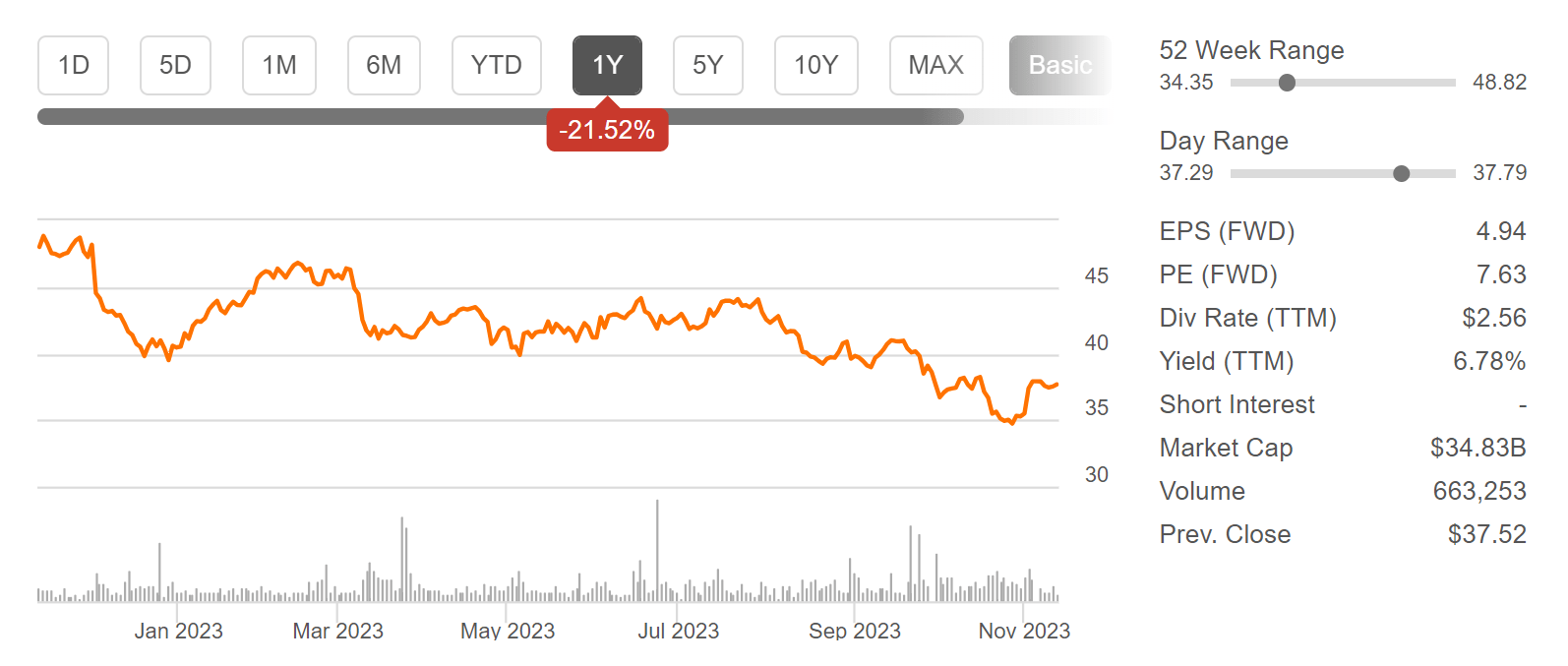

The Canadian Imperial Bank of Commerce has shown a negative performance of -21.52% over the past 12-month period.

{kind=link}

At the bank’s current stock price of $37.68, it pays shareholders a Dividend Yield [FWD] of 6.83%. This metric is even more compelling for investors when considering its Payout Ratio of 53.36%, which suggests potential for future dividend enhancements, in combination with its 5 Year Dividend Growth Rate [CAGR] of 4.48%.

These numbers have also influenced me placing the Canadian Imperial Bank of Commerce on my watchlist for potential incorporation into The Dividend Income Accelerator Portfolio. This is due to it closely aligning with the portfolio’s investment approach: it combines dividend income with dividend growth, and contributes to reducing the risk level of a portfolio (due to its 24M Beta Factor of 0.96). At the same time, it would increase the geographical diversification of The Dividend Income Accelerator Portfolio.

It is further worth highlighting that the bank’s Valuation is currently attractive, attributed to its P/E [FWD] Ratio of 9.67, which is 2.60% below its average from the past 5 years, indicating that the Canadian bank is presently at least fairly valued.

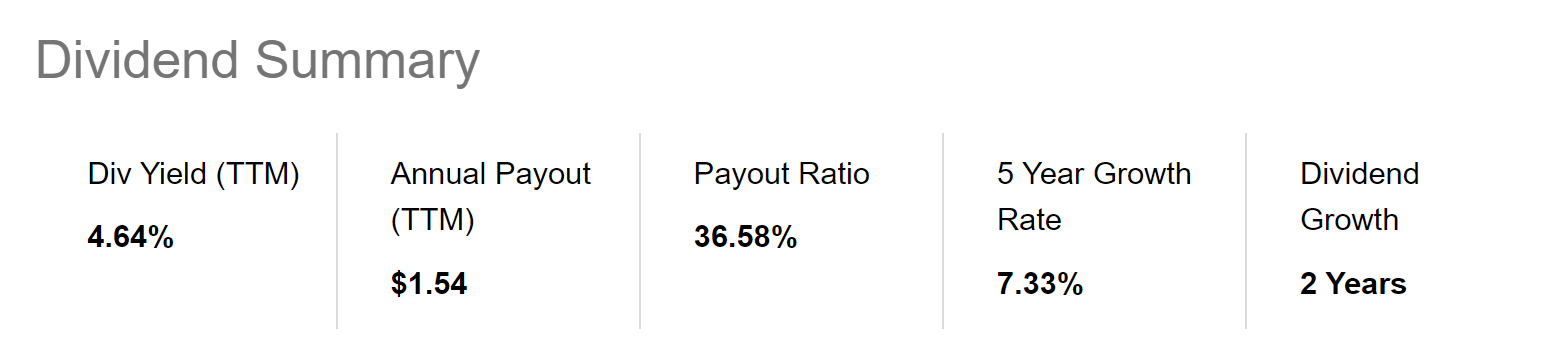

Suncor Energy

Suncor Energy has had a negative performance of -7.29% within the past 12-month period.

{kind=link}

Presently, Suncor Energy pays shareholders a Dividend Yield [FWD] of 4.63%. Moreover, it is worth noting that the company’s Free Cash Flow Yield [TTM] stands at an attractive level (10.45%), indicating that it is an appealing risk/reward choice for investors.

Moreover, I am convinced that Suncor Energy’s Valuation is presently attractive, which is underscored by the company’s P/E [FWD] Ratio of 8.24, being 22.55% below the Sector Median (10.64).

In addition to the above, it is worth highlighting that Suncor Energy’s Payout Ratio of 36.58% and its 5 Year Dividend Growth Rate [CAGR] of 7.33% underscore that the company is not only attractive for those seeking dividend income, but also dividend growth.

{kind=link}

When compared to Exxon Mobil (NYSE: XOM ), it can be highlighted that Suncor Energy has a slightly lower Valuation (P/E [FWD] Ratio of 8.24 when compared to 11.16), pays a higher Dividend Yield (Dividend Yield [FWD] of 4.63% when compared to 3.66%), and has shown more dividend growth (5 Year Dividend Growth Rate [CAGR] of 7.33% when compared to 2.74%). It also seems to be the slightly more appealing choice in terms of Profitability: the company’s EBIT Margin [TTM] of 21.93% is slightly above Exxon Mobil’s (EBIT Margin [TTM] of 15.05%).

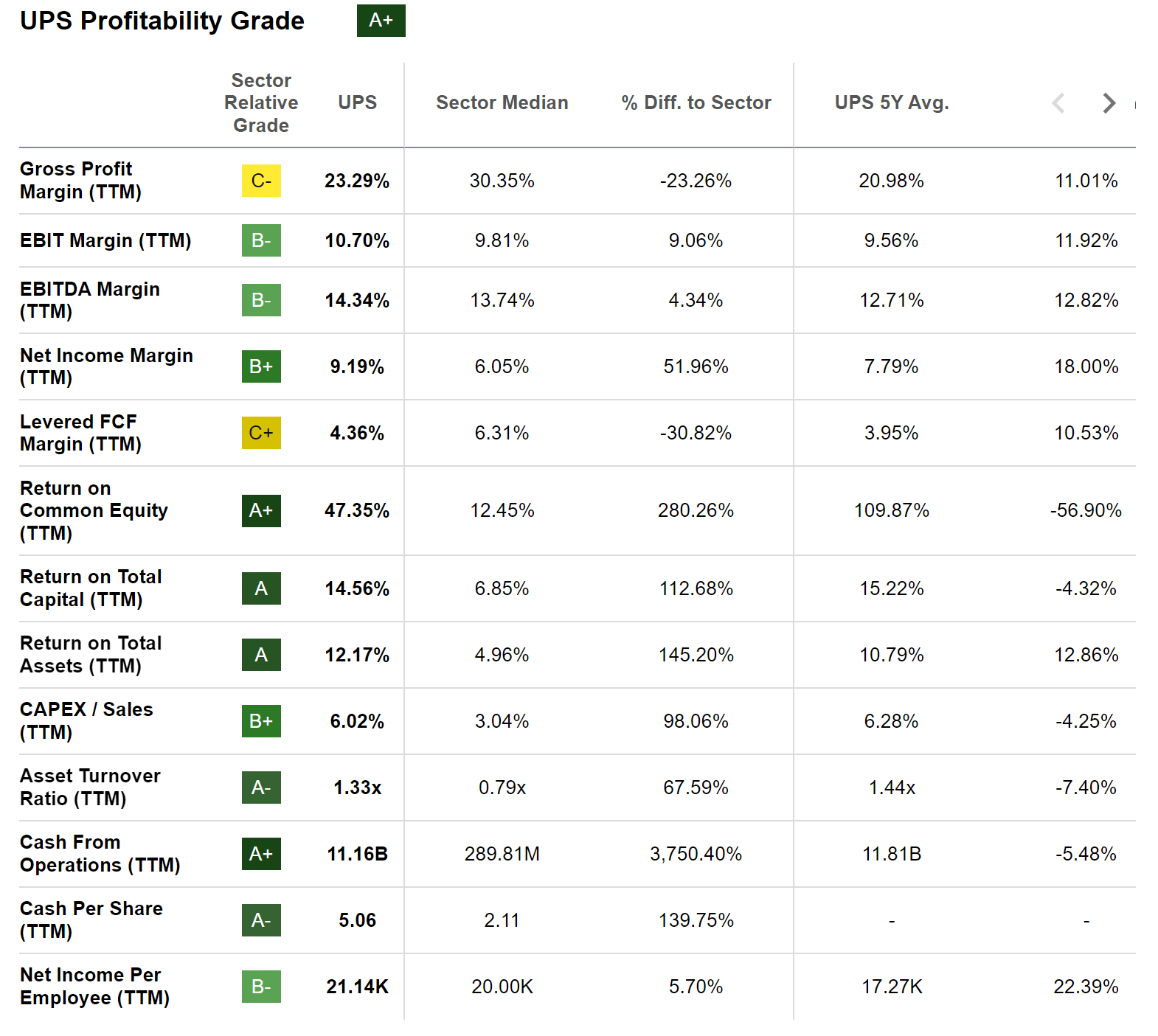

United Parcel Service

UPS hasn’t performed well when considering the past 12-month period, showing a performance of -19.85%.

{kind=link}

Given UPS’s weak performance within the past months, the company is now available for a compelling price: its P/E [TTM] Ratio of 13.93 is 30.74% below the Sector Median and 44.53% below its average from the past 5 years, suggesting that UPS is presently undervalued.

I further believe that UPS shows attractive metrics when it comes to Profitability: this is underscored by the company’s EBIT Margin [TTM] of 10.70% (9.06% above the Sector Median), and its Return on Equity of 47.35% (which is 280.26% above the Sector Median). The Seeking Alpha Profitability Grade, which you can find below, confirms this theory.

{kind=link}

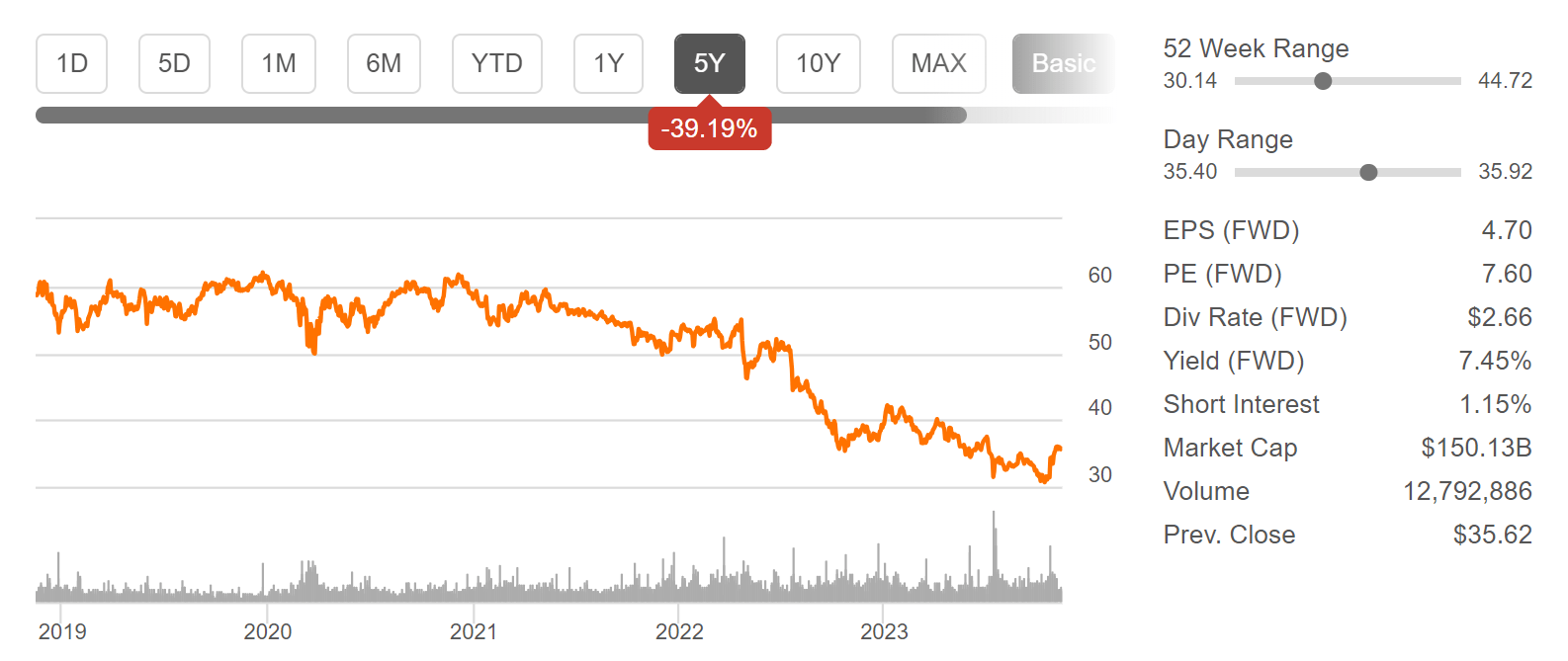

Verizon

Considering the past 5 years, Verizon’s stock price has declined by 39.19%, as you can see in the illustration below.

{kind=link}

Today, Verizon is available for a P/E [FWD] Ratio of 7.98. The company’s present P/E [FWD] Ratio is 25.60% below its average from the past 5 years, and it is 49.14% below the Sector Median.

When compared to its main opponent AT&T (NYSE: T ), it is worth highlighting that Verizon currently pays the slightly higher Dividend Yield [FWD] (7.45% compared to 7.10%), has shown significantly more dividend growth (3 Year Dividend Growth Rate [CAGR] of 1.98% when compared to -10.93%), and has produced slightly better results when it comes to growth (Revenue 5 Year [CAGR] of 0.54% when compared to -5.83%), suggesting that Verizon is the superior pick for dividend income and dividend growth investors when compared to its rival AT&T.

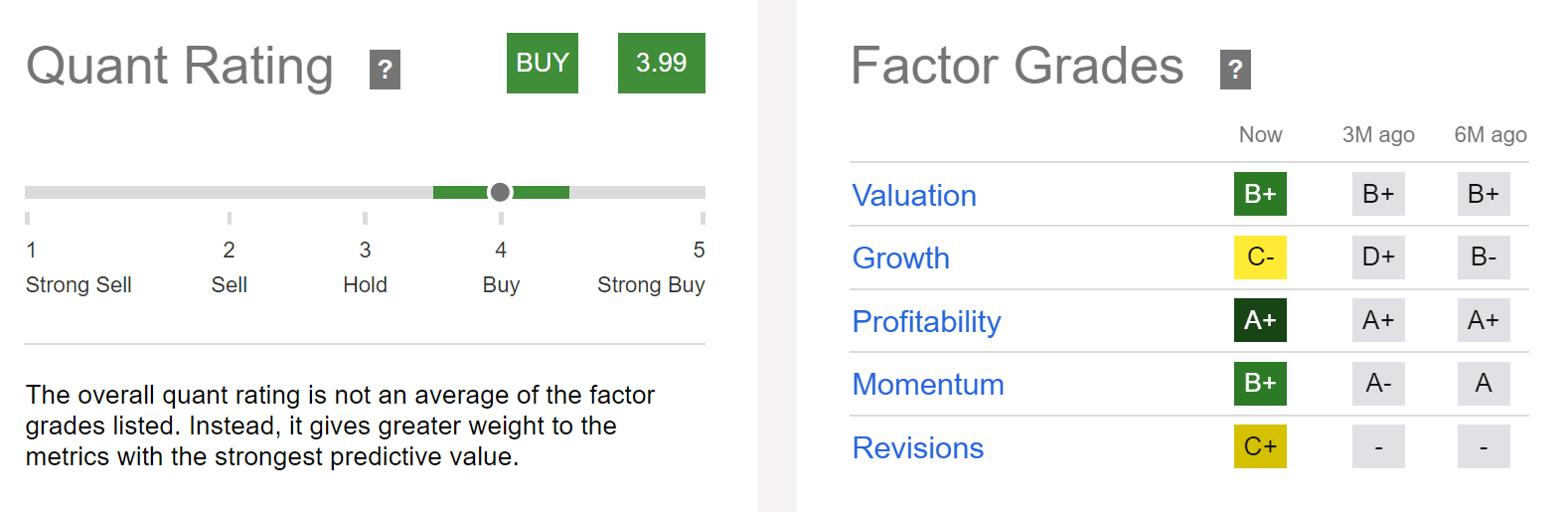

Iberdrola

Headquartered in Bilbao, Spain, Iberdrola is a company from the Electric Utilities Industry that was founded in 1840.

From my perspective, Iberdrola currently has an attractive Valuation. This is evidenced by the company’s P/E [FWD] Ratio of 15.53, which is 3.41% below the Sector Median of 16.08.

The undervaluation of Iberdrola is further shown by its Dividend Yield [TTM] of 4.68%, which is 57.92% above its average from the past 5 years (which is 2.97%).

Different metrics further demonstrate that the company’s Dividend Yield is attractive. Both its Dividend Yield [TTM] of 4.68% and Free Cash Flow Yield of 6.55% stand above the Sector Median (which are 4.23% and 6.14% respectively).

Iberdrola’s strength in terms of Profitability is reflected in its EBIT Margin [TTM] of 16.04%, and its Return on Equity of 10.66% (which is 17.84% above the Sector Median).

Both the Seeking Alpha Quant Rating and the Seeking Alpha Factor Grades underline that Iberdrola is worth taking a closer look at: the company receives a buy rating from the Seeking Alpha Quant Rating, and, according to the Seeking Alpha Factor Grades, the company gets an A+ rating for Profitability, and a B+ for Momentum and Valuation. For Revisions, it gets a C+, and for Growth, a C-.

{kind=link}

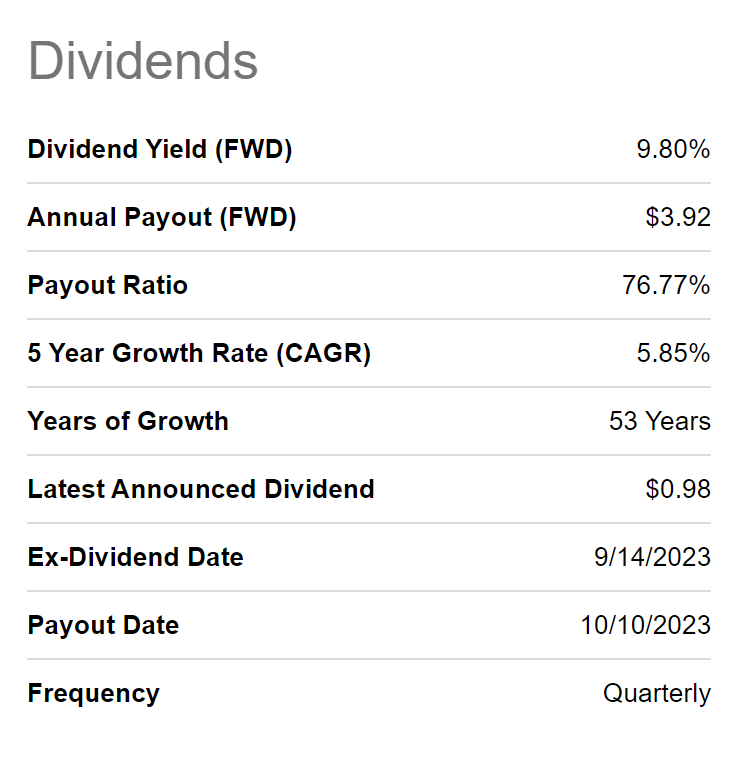

Altria

Numerous indicators highlight that Altria is an exceptional choice for investors seeking a high and sustainable Dividend Yield. At Altria’s present Annual Payout [FWD] of $3.92, it offers shareholders a Dividend Yield [FWD] of 9.80%.

Altria pays its Dividend quarterly, and the company has already shown 53 Years of Dividend Growth. Altria’s Payout Ratio of 76.77%, its 5 Year Dividend Growth Rate [CAGR] of 5.85%, and its EPS Diluted Growth [FWD] of 3.58% raise my confidence that the company’s Dividend should be sustainable.

{kind=link}

The sustainability of Altria’s Dividend in combination with its current Valuation (P/E [FWD] Ratio of 8.69) make it not only a potential candidate for future incorporation into The Dividend Income Accelerator Portfolio, but also an excellent pick to consider investing in during this month of November.

When compared to opponents such as British American Tobacco (NYSE: BTI ) ( OTCPK:BTAFF ) and Philip Morris (NYSE: PM ), I see Altria slightly ahead in terms of Profitability (while Altria has an EBIT Margin [TTM] of 59.67%, British American Tobacco’s is 48.10%, and Philip Morris’ is 35.34%), and in terms of Dividend Growth (Altria has a 5 Year Dividend Growth Rate [CAGR] of 5.85%, while British American Tobacco’s is 2.45%, and Philip Morris’ is 2.94%).

In addition to that, it can be highlighted that Altria’s current P/E [FWD] Ratio of 8.69 is significantly lower than Philip Morris’ (P/E [FWD] Ratio of 17.63), underscoring my theory that Altria is presently undervalued.

Pfizer

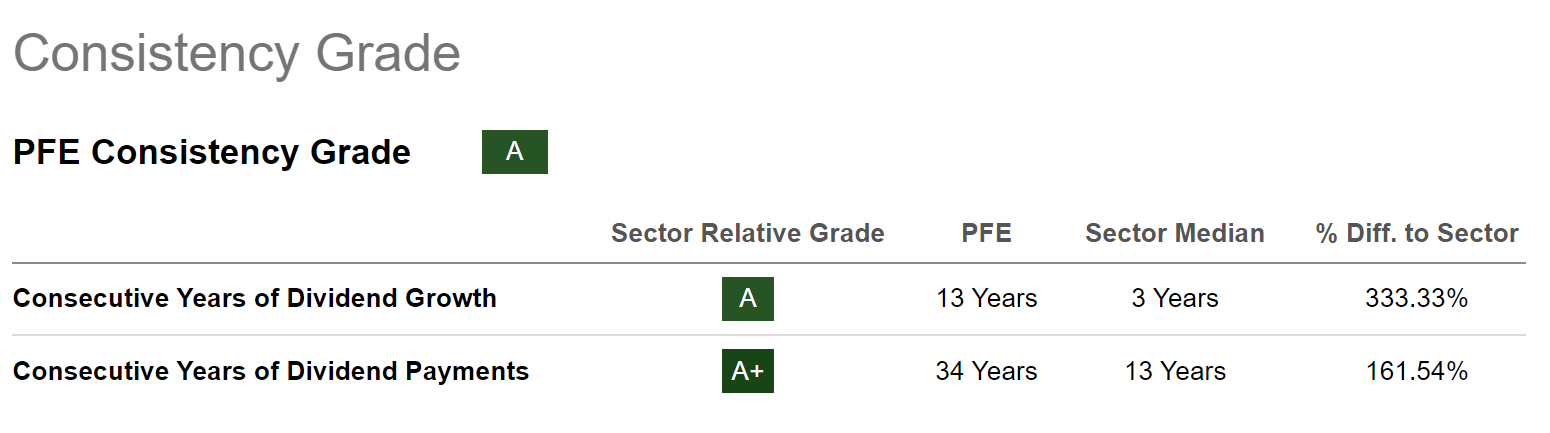

Pfizer currently presents a Dividend Yield [FWD] of 5.56%. The company has shown 13 consecutive years of dividend growth as well as 34 years of dividend payments. These metrics underscore Pfizer’s attractiveness for dividend income investors.

{kind=link}

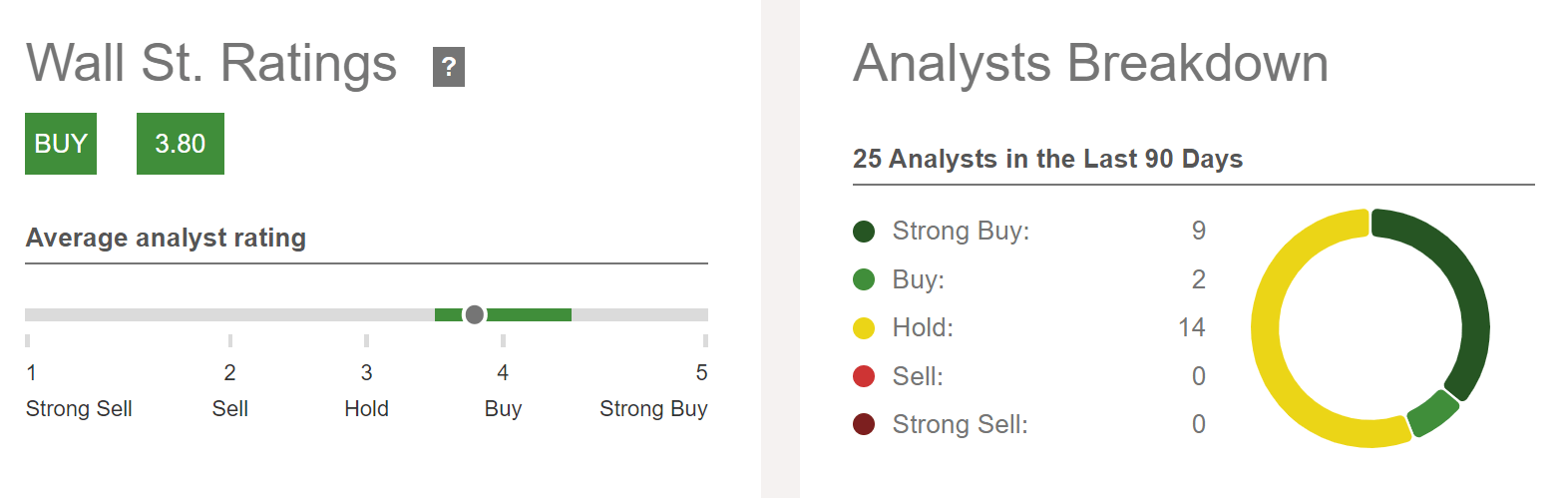

According to the Wall Street, Pfizer is currently a buy: from 9 analysts, the company receives a strong buy rating, from 2 analysts a buy rating, and from 14 analysts, it gets a hold rating.

{kind=link}

In addition to the above, it can be noted that Pfizer currently has a P/E GAAP [TTM] Ratio of 16.06, which is only 4.11% above its 5-year average, and which indicates that Pfizer is currently fairly valued.

Conclusion

The identification of competitive advantages, the companies’ financial health, their attractive Valuation, and the existence of sustainable dividends are key factors when seeking high dividend yield companies that could be incorporated into your investment portfolio.

I am following this careful selection criteria process with the construction of The Dividend Income Accelerator Portfolio. From today’s list of 10 high dividend yield companies, Ares Capital has already been incorporated into The Dividend Income Accelerator Portfolio. The remaining companies are on my watchlist for future incorporation, aligning with the investment approach of The Dividend Income Accelerator Portfolio.

I strongly believe that it is important to include companies that pay sustainable dividends in your investment portfolio. The reason for this is that they can offer you a platform for financial independence, providing you with an income stream that can be raised on an annual basis.

I believe that each of the selected picks I have presented in today’s article could help you generate extra income through the production of a reliable income stream via dividends, which have the potential to grow annually, thus bolstering your financial security.

Envision the benefits of receiving attractive dividend payments from the companies you invest in: a dream vacation to Europe or any other place in the world with your best friends or family, paid with by the dividends from companies such as Morgan Stanley, UPS, Verizon, or Pfizer. Simultaneously, you can enjoy the advantages of an extensively diversified portfolio with a lowered risk level that contributes to the continuous growth of your wealth! With the construction of The Dividend Income Accelerator Portfolio, my aim is to guide you toward these goals.

Author’s Note: I would appreciate hearing your opinion on my selection of high dividend yield companies to consider buying in November 2023. Do you already own or plan to acquire any of the picks? Which are currently your favorite high dividend yield companies?

For further details see:

Yields Up To 10%: My Top 10 High Dividend Yield Companies For November