APO - Zelikovic Investments Annual Letter 2022 (Updated Q1 2023)

2023-05-02 18:31:13 ET

Summary

- Summary of fiscal year 2022 and positions for 2023.

- A discussion of our Owner Operated Compounder stocks.

- Micro-Cap Value Strategy - Based on Greenblatt's Magic Formula and Jim O'Shaughnessy's Composite Score.

- Special Situation Investments and International Net Nets.

"The two most powerful warriors are patience and time"

Leo Tolstoy ("War and Peace")

Dear Investors,

I have the privilege to write to you in this annual letter for the past fiscal year of 2022.

General review:

As usual, first I wish to welcome the new clients who have joined our financial path this past year. Together with our new clients, we currently have over 600 investors involved in our activities. It is my great honor to provide you with the service you deserve.

The year of 2022 will be remembered as a tumultuous year for most investors all around the world. The invasion of Ukraine by Russia, rising inflation, and the increase of the Federal Funds Rates in the U.S., all had a negative influence on the markets. As a result, most of the stock indexes in the world suffered a double-digit decrease in 2022, including the NASDAQ, which decreased in value by 33% in 2022, the S&P 500 index, which dropped by 18%, and the Russell 2000 index was also down by approximately 22%. The MSCI WORLD index also fell by almost 20% last year. These paled in comparison to the decrease in the value of Bitcoin (BTC-USD) in 2022 (-64%), in the price of the Tesla (TSLA) stock (-65%) (despite an impressive recovery YTD), and in the value of Cathie Wood's popular fund, ARK (-69%) (see the reference to ARK funds in my last year's letter). The global crisis did not skip the stock indexes in Israel as well. Last year, the Tel Aviv 125 index dropped by about 12%, while the Tel Aviv 35 index fell more than 9%.

In my letter last year, I discussed the potential influence of an increase in interest rates on the stock market. The analysis included a detailed reference to the three investments in the stock market, i.e., short-term deposits, bonds, and different kinds of stocks. I summarized this subject in the following words:

"It is clear how a change in interest rates may affect financial assets in the world, and why an increase in the interest rates may decrease the price of most of our investments in the short term ."

Well, this increase in interest rates indeed occurred last year and its results were very well felt in the global markets. And as expected, what exacerbated the crisis in 2022 is the fact that the value of "risk-off" assets (specifically bonds) also decreased sharply, in some cases even more than the stock indexes. For example, the ETF which tracks long-term US government bonds (TLT) decreased by 31% last year! In contrast to the popular opinion held by many investors, that these investments are immune to losses, in the scenario of interest rate increases, it is possible to lose a lot of money by investing in these assets. Despite the sharp deciles in these assets, which make them even more tempting for investors currently, I still recommend drawing away from most bonds which in "real prices" (after deducting inflation) continue to generate negative yields.

In order to slightly "sweeten the pill" from last year, I wish to add a historical fact which provides a reason to be an optimist for those who believe that history repeats itself (or at least, in the words of Mark Twain, rhymes…). Reviewing the history of the US stock exchange teaches us that after a year of drops of over 20% in the main US indexes, almost in all cases (excluding the Great Depression in the 1930s), the following year was always a positive year for the markets (and indeed 2023 has begun with positive returns across most markets). Another encouraging fact is that a calendar year, in which all the main US stock indexes as well as the Aggregate Bond Index dropped, is a very rare event which happened only three times since 1926 (in 1931, 1969 and last year).

Despite the negative occurrences detailed above, I am happy to tell you that the returns in our Funds/SMA's were barely negative. We believe this is mainly thanks to: 1. Active stock picking of financially stable companies, while staying away from the "shiny" popular stocks; 2. International diversification- i.e., investing in stock markets of countries outside of Israel and the U.S. markets; 3. A substantial strengthening of the Dollar and the Euro last year versus our home currency - the New Shekel. Specifically:

- Stock Picking: We continue the same financial pathway we initiated over six years ago on your behalf, and which you are well-aware of. Our approach does not include focusing on the gyrations of stock prices, rather on the careful selection of companies with impressive economic performances, in which we intend to invest as partners for many years. We do not engage in a daily, monthly, or yearly comparison of our stocks' performances to the stock market indexes, or in vain attempts to predict the behavior of the stock market. We base our investment recommendations on solid, managerial and economic data of public companies. In this spirit, we made sure to stay away from the expensive tech stocks, from various "Cathie-Wood" like popular stocks, and from additional securities prices at "bubble" prices. We remained invested in "non-popular", boring, profitable companies within the oil industry as well as the insurance industry; companies whose value increased even in a year like 2022. These investments soundly protected our portfolios from the sharp drops of last year (see my elaboration below).

- Investments in foreign stocks: An additional tactic we have adopted, which continues to serve us well, is investing in stock markets of countries outside Israel and US, such as Europe, Canada, England, and Japan. Seemingly, adapting this policy is "going against the flow", especially considering that until recently the US Nasdaq index was almost the "only game in town". But in fact, in these countries around the world, we have found (and continue to find) many high-quality companies, which trade at a discount of 50% or more, compared to parallel companies in the US. In this respect, we rely on the words of Professor Robert Shiller (winner of the Nobel Prize in Economic Sciences for the year of 2013), who recently stated that the US stock market is approaching "bubble" prices and that there is much logic in shifting funds to markets outside the US. For example, the U.K. stock market served as an excellent ground for this strategy last year. England had to deal with difficult national crises, including, among other things, the frequent changes of prime ministers and other officials, the death of the Queen, and coping with the withdrawal from the European Union, which drove many investors away from this market. Nonetheless, there, of all places, we invested in the stocks of thriving companies at particularly low prices, and despite the Macro headwinds, the U.K. stock market was one of the best performing markets during 2022.

- Strengthening of foreign currencies (versus the Shekel) : Another important factor influencing our stock portfolios, which mostly consist of foreign stocks, is of course the foreign currency rate. The increase in the rates of the dollar and the euro last year (and leading into 2023) led to a positive increase in our portfolios (when we invest our shekels in foreign stocks quoted in foreign currencies and translate this return back to shekels, the portfolio shows a positive return even if the stock prices remain unchanged in foreign currency terms). Yet, we are well-aware of the volatility of the exchange rates, which sometimes generate profits for the investor and sometimes contradict them. Therefore, we believe that what will determine the yield of our portfolios for the long term is primarily the economic performances of the companies we invest in globally, combined with the tremendous power of compound interest, rather than fluctuations in the rate of exchange in the short term.

Looking Forward:

"You make most of your money in a bear market, you just don't realize it at the time "

Shelby Cullom Davis

Whoever hoped that 2022 would finally end and for 2023 to begin with a flurry of positive economic news, was much disappointed. Despite a strong January, this year continued with several occurrences that badly shook the stock market in Israel and the entire world, including the social/political fermentation in our country, the hawkish statements made by the US central bank, the collapsing of banks in the US and in other countries, and a considerable decrease in the profits of many public companies. And indeed, the average investor finds himself very much confused, wondering what the right investment strategy in this current market is. Many investors choose to reduce their exposure to this "sizzling and bubbling" stock market, assuming and feeling that the decreases in value of stocks will continue in the visible future. We think that this reaction is wrong. First, we must remember that the stock market has always been, and always will be, volatile; that there is no proven correlation between the market behavior in a certain year and its behavior in the year after; and that nobody can predict the market behavior in the short term. Moreover, investors must remember that the Capital Markets, are distinguished by a highly sophisticated mechanism summarized in a theory, called in the professional language " The Efficient Market Theory " (for the development of which Professor Fama from the University of Chicago won a Nobel Prize in Economics in 2013). The theory determines that once information about the market or a certain company is made public, including evaluations regarding the future of the market or the company, this information is immediately embodied in the prices of the corresponding securities in the market. In other words, the company's value is derived directly from its present profits along with the expectations of the investors for its future profits. If so, a decision to buy or sell a stock based on consensus evaluations for the stock's future does not make sense, because these future earnings (or expected changes thereof) are already embodied in its present value (making the market very difficult to "beat").

In this context, we should emphasize that last year's decreases in the stock markets are a direct result of the investors' anticipation for future inflation, an upcoming recession, or future increases in interest rates, thus even if these events will indeed occur in the future, they won't necessarily be accompanied by additional decreases in the stock markets (these are already reflected in the present stock price). Furthermore, it is very difficult to evaluate what expectations are already reflected in the current stock prices in the markets, and thus it is also so difficult to invest according to macro-economic forecasts. The graph below, properly illustrates the relationship between stock prices and the economic performance of companies in previous bear markets. The graph shows how in previous crises, the prices of the stocks (blue line) start to rise 6-9 months before the profits of the companies (green line) hit a low point.

{kind=link}

We should point out the fact that despite the negative financial developments of the beginning of this year, as specified above, the world stock markets started the new year with strong increases in almost all investment channels (except for the markets in Turkey and Israel, the former due to a natural disaster, and the latter due to a self-inflicted conflict).

All the data above demonstrates the futility in trying to predict the occurrences in the stock market. We believe that "time in market", and not "market timing", is the key to success in the world of investments. Investors who stand for long-term investments are not supposed to fear the current stock market drops. On the contrary, today it is possible to buy stocks of prime companies at sale prices. In this regard, I have adopted John F. Kennedy's saying about the shape used for writing the word "crisis" in Chinese. The Chinese use two strokes of a pen to write this word, while one stroke symbolizes "danger", and the other - "opportunity". Beware of the danger but recognize the opportunity! In line with this, I proceed with our same investment strategy, according to which even in times of turmoil and high volatility, I recommend investing in carefully selected profitable companies. I will continue to recommend investing in stocks of these companies over time and in this manner we will be able to compound our investments over time.

Price Earnings (P/E) ratio - an Essential Tool for Intelligent Investors:

"The habit of relating what is paid to what is offered is an invaluable trait in investment"

Benjamin Graham ("The Intelligent Investor")

This year, as in each year, I will dedicate part of this letter to discussing an essential investing tool, which guides us in our portfolio selection. After discussing in last year's letter the "economic mass" and interest rates in the stock market, in this letter I will analyze the "price earnings ratio" (or its inverse- "The Earnings Yield"). This index expresses the ratio between the quoted purchase price of a financial asset and its economic value, and constitutes an essential index in the "tool box" of value investors around the world.

Before I introduce our analysis of the "price earnings ratio" in the stock market, I would like to mention an example from the world of real estate, in which an extensive use of a similar ratio is used. This example will help us understand the importance of the "price earnings ratio" in the stock market. Let us assume that an investor wishes to invest in an apartment (without the use of leverage) and rent it to a rentee. How will he evaluate such an investment? After considering the neighborhood, he will evaluate the monthly rent paid for such a property. Assuming he buys this apartment for one million NIS, and it will generate a monthly rent of 8,333 NIS - in this case, we are talking about a yearly rent of 100K NIS (8,333 times 12). How will the said investor evaluate the profitability of this deal? He will divide the price of the apartment (1 million NIS) by the rent he will be receiving for the apartment in a specified year (100,000 NIS), thus receiving the number: 10. In other words, in this deal the investor will purchase an apartment in a price earnings ratio of 10, indicating a good real estate deal. What is the importance of calculating the "price earnings ratio" in the real estate businesses? First, it indicates how long it takes for the investor to earn back his investments - in our case, 10 years, which is a relatively short period of time in most established real estate markets. Second, the price earnings ratio helps us calculate the yield from the investment. How? By calculating the inverse of the price earnings ratio. In this example, the investor can determine the yield on his money by dividing the yearly rent (100,000 NIS) by the price of the apartment (1 million NIS) resulting in a yield of 10%, which is also an attractive yield in the real estate market.

Similar to its use in the real estate market, the "price earnings ratio" is an essential index for determining the price of an investment in the stock market too. In the stock market, this important tool, which as aforesaid, provides information on a stock's price in relation to its economic value, is expressed by the following financial equation:

The price earnings ratio = The Company's market cap / Net profit per year

or by reversing the ratio:

The Earnings Yield = Net profit per year / the Company's market cap

Which data will we use to calculate the price earnings ratio? "The Company's market cap ", placed in the numerator of the equation, is the value of the market cap of any public company (this number is stated for each company in every financial portal and is equal to the number of shares issued by the company multiplied by their market price). The denominator represents the accounting profits of the company during the last calendar year (every public company publishes its accounting profits in the past year, revenues minus all expenses, in its audited financial reports). As seen in the second equation, the expected yield of the investor will be received by reversing this ratio.

Both equations demonstrate that the less we pay for a stock, the lower its price earnings ratio will be and the higher its expected future yield will be. And vice versa, a high stock price will increase its price earnings ratio and decrease the expected yield for the investor. Correspondingly, a company's high profit per year will lead to a low price earnings ratio and a high future yield, whereas a low net profit will be expressed by a high price earnings ratio and a low future yield. The current average price earnings ratio in the US stock market is around 18, and the yield to the average investor is a little over 5% (not including dividends).

The price earnings ratio is a convenient index for estimating the value of a company, and together with additional price to value ratios (see my article on the topic, published in my blog on The Marker), it serves the wise investor well, when having to decide whether to purchase the stock of a certain company. Many investors, who buy stocks for any price, without considering the economic value of a public company, justified by a "promising" investment story they believe in, are not taking an investment action; they are taking an action which is more like gambling. Following the above example from the real estate market, what does this resemble? It is like a real estate investor, who is willing to buy an apartment in a good neighborhood at any price. Each apartment has an estimated economic value, and no reasonable person will pay a price completely disconnected from this economic value, even in the best neighborhoods.

In general terms, the stocks of public companies can be divided into two categories: growth stocks and value stocks. Growth stocks are the popular stocks; stocks of companies which the investing public expects to grow at above average rates, and therefore price these companies at a premium price (and a high price earnings ratio). Inversely, value stocks are stocks of companies within less "shiny" industries; companies which the investing public often stay away from and as such their prices are much lower, as expressed by a low price earnings ratio. As you very well know, our investment recommendations focus on these value stocks, while carefully selecting these companies after determining their economic value (see below).

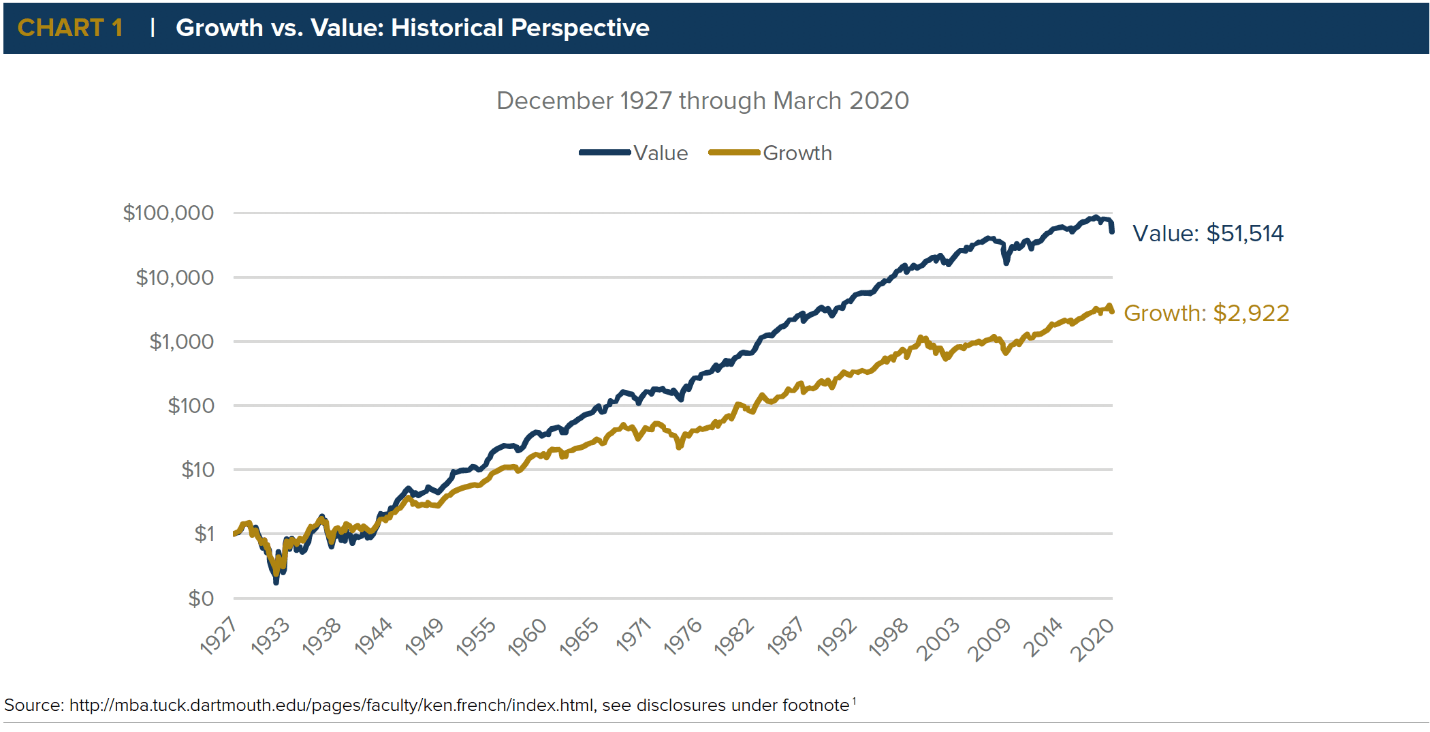

Professors Fama and French from the Faculty of Economics at the University of Chicago divided the stocks traded in the US stock exchange between value stocks and growth stocks (here according to price to book ratio) and examined their historic performances over the last 100 years. As clearly demonstrated in the graph below, the value stocks (blue line) generated higher profits on average compared to the growth stocks (brown line) and the difference is quite sizable. From a historical perspective, it is evident that the value investor who invested in the cheapest stocks made over 20 times more on his money than the one who invested in the growth stocks.

{kind=link}

This data is based on average values, and certainly does not apply to every company, however this supports the idea that in building an investment portfolio, it is recommended "on average" to invest in the "cheaper" stocks.

In my opinion, investors who chose the growth stocks are misled by wrong assumptions and forecasts about these stocks. The common mistake of these investors is their belief that companies which grew at above average in the past will continue to grow at the same rate also in the future, and that companies with a low growth rate will continue this trend. A rigorous research performed by Brian Chingono and Greg Obenshain from the Verdad Investment House in the US (extending previous research by Chan, Karceski and Lakonishik in their 2001 paper, The Level and Persistence of Growth Rates ), examined and analyzed the performances of companies in the US, Europe and Japan over the last decades. They showed that there is no reliable way, and it is basically impossible, to predict the growth rate of a company over time based on its past growth rate. Additionally, very few, seemingly random companies succeed to grow at above average rates over time.

The inability of companies to grow at above average rates over time can be explained, among other things, by one of the well-known, dominant phenomena in the world of free economy, called "reversion to the mean". The profit/growth rates of every company, successful as it may be, will usually align with the average rate of the market, whether due to a competitive forces, changing market conditions or various other reasons. Many investors are not aware of this phenomenon and are willing to pay too high a price for companies with above average growth rates in the past, even though in the future they will probably slow down to an average growth rate. And vice versa, companies with a growth that is below average may surprise the market in the future and their future profits will rise above the investors' expectations. The value stocks belong to this latter group.

On this matter, I should point out another phenomenon directly related to the price earnings ratio, called "multiple expansion". I will explain it through two hypothetical investment portfolios: the first with the "popular" stocks priced to grow in a rate above average over time by a P/E ratio of 40, and the second with "weak" stocks trading at a P/E ratio of 5. As said above, most of the "popular" public companies will not grow at above average rates, therefore the market forces will bring down their P/E back to the average ratio today (about 20), which will necessarily lead to a 50% decrease in the stock's price (assuming no changes in the profits). In the second portfolio on the other hand, a substantial part of the weak companies traded in a P/E ratio of 5 will remain profitable, which will earn them a market pricing with a P/E ratio of 20. This will lead to a 300% increase in the stock's price (even if their profits of the company did not grow). It will be correct to assume that some of the companies in the second portfolio will not recover, and some will even go bankrupt, but there is no doubt that the financial experience and the compelling studies back up "on average" investing in the lower priced stocks.

In summary, it is important to emphasize again that what will determine our returns over time will be first and foremost be the profitability of the companies in which we invest, rather than other macro conditions, such as foreign exchange rates (see above) or the interest rate environment.

Henceforth we will set forth a specific description of our investment policy:

Our Portfolios:

Our portfolios are divided into three parts (with the exception of those of you invested additional fund, which is concentrated mainly in Net-Net stocks worldwide):

- "Micro- Cap Value Stocks" rebalanced monthly.

- "Compounder" stocks.

- "Special Situations".

I should emphasize that the Individual Retirement Account (I.R.A.) option also allows us to rebalance our portfolio without incurring taxes.

1. Micro-Cap Value Stocks

This investment strategy is based on one of the best strategies in the book "What Works on Wall Street" by James P. O'Shaughnessy. This strategy selects a basket of 25 stocks whose market cap at the time of purchase is under 500 million dollars (stocks which are usually excluded from the major indexes in the U.S.A.). These stocks are selected only if they fulfill a number of criteria (including value, momentum and financial stability) which have been proven by empirical studies to be a source of alpha.

As we have witnessed in the first years, some of these stocks and this strategy do not outperform the market every year. Nevertheless, this instability per se (which may cause other investors to abandon the strategy at exactly the wrong time) is the key for its success over time as it involves "going against the herd". As Prof. Joel Greenblatt, the author of the book "The Little Book that Beats the Market"), once stated:

"If I wrote a book about a strategy that worked every month, or even every year, everyone would start using it, and it would stop working."

2. Compounders

Compounder stocks are stocks of profitable companies which operate in various fields (including many owner-operated stocks of public insurance companies around the world), led by honest, reliable Outsider-like CEOs with a proven track record. We prefer to purchase these at a healthy discount to their economic value, so that even in the worst-case scenario our investment can still be profitable (Margin of Safety). However, once we purchase these, we plan to never sell them unless they undergo a dramatic change or a de-listing (much like the Coffee-can Portfolio).

Before I introduce our Compounders, I wish to share a short story I read (thank you to Morgan Housel) about Warren Buffett which I think encapsulates the common attributes of our Compounder Stocks. It is told that a neighbor of Warren Buffett from Omaha approached him during the depths of the 2008-2009 financial crisis and asked could the American economy ever recover from such a calamity and how does an individual investor invest during such a period. According to the story Buffett answered him - "Do you know what was the best selling candy in the U.S during the 60's? Buffett answered- it was the Snickers bar. And do you know what the best selling candy bar is today? The Snickers bar". With this answer their conversation was over.

From this story we can better understand the investment philosophy we adapted. We invest in the stocks of companies which operate in predictable and stable industries which should be around for me years. The average investor would be better suited investing in what is knowable and stable rather than guessing as to what will be different and growing into the future. The track record of many great investors proves that the most profitable investments were buying and holding companies which have been doing the same thing for many years.

So how did our companies perform in 2022?

Let's start off with the Italian holding company EXOR (EXO.AS), an old family-owned company which historically has excelled in a very successful investment and acquisition policy. The market value of the company remains about 16 billion euros, despite a very challenging year with much volatility. As you recall, among the holdings of EXOR you can find Fiat-Chrysler (which merged in 2021 together with the French auto manufacturer, Peugeot into a new company- Stellantis), CNH Industrial (CNHI) (the manufacturer of agricultural equipment), Ferrari (RACE), Juventus Football Club, and the newspaper The Economist. The Net Asset Value of the company, as published in its financial reports, dropped 7.5% in 2022. During the year Exor also established a new Investing arm (Lingotto) to be managed by Matteo Solari, a reputable investor from the Insurance world. There is no doubt that this leading company (led by the Agnelli family) is financially solid and meets all the criteria I look for in a long-term investment (see my article about EXOR in my blog on The Marker).

An additional player in our "team" is Brookfield Asset Management ( BAM ), a Canadian holding company which owns and manages over 720 billion dollars worth of real estate around the world. Last year the group decided to spin off part of its asset management business to shareholders, thereby each shareholder received shares in the new entity ( BAM ) a 13 billion dollar market cap company and also remained with shares in the parent company ( BN ) a 51 billion dollar company (which also continues to own part of BAM). We plan to hold both for many years to come. During 2022 the shares of both companies dropped significantly, despite growth in AUM.

Another company we own is InterActiveGroup ( IAC ). IAC is a highly successful holding company in the technology sector which is managed by the renowned investor, Barry Diller. The company lost more than 50% of its value in 2022 (similar to many shares in the Tech industry). During the year, the CEO of IAC, Joey Levine, also took over as CEO of the subsidiary, Angi Home Services ( ANGI ) in an effort to turn things around. Together with IAC's investments in MGM, Meredith and Dotdash and numerous other promising ventures we continued adding to our position in IAC during the selloff.

We also increased our stake in the giant global-American asset management company, Kohlberg Kravis Roberts (KKR), which manages today over 400 billion dollars (23% CAGR growth rate in the past decade). The company's stock dropped over 30% last year. However, we believe that the asset management industry is one of the best and most profitable ones in the economy (and KKR has one of the best management teams in the industry), and that the company's stock is still trading at a discount to its true value. Many insiders in the company, as well as several successful investment managers in the world, invest alongside us in this wonderful company.

We remind you this year again that we believe that one of the most promising pathways for investing in the stock market is investing in insurance companies. A well-managed insurance company has two sources of profitability: 1. Insurance activity, and 2 . Investment of its "float" (see my previous article on Seeking Alpha). Accordingly and after careful examination, we have increased our stake in a number of insurance companies, including Fairfax Financial Holdings, which has compounded book value at an almost 18% rate for the past 30 years, Assured Guarantee (AGO), and Markel Corporation ( MKL ) managed by the exemplary Thomas Gayner, and the Norwegian insurance company, Protector Insurance ( PSKRF ), which is a rising star in the European insurance field. These companies continued to demonstrate excellent performances in the year of 2022 and their stock prices stood up well during the sell off last year. We also established a new position in Apollo Global Management ( APO ) which is also a great asset management firm (over 380 Billion USD AUM) and owns a profitable insurer (Athene).

Another stock we plan to own for many years is Texas Pacific Land Trust (TPL). TPL is an trust company which was founded in 1888, when it received through a legal settlement, a valuable piece of real estate (packed with oil fields) in the state of Texas. This is a royalty company which profits from royalties paid to it by oil drilling companies that operate in the area. The big advantage of this business model is that the company has almost no expenses, which significantly increases its profitability (the profit margins of TPL are even higher than those of Microsoft (MSFT)). Add to this the rights that the company possesses for many water resources discovered on its lands, a good management team which has excelled in efficient capital allocation (for example, by buying back its own stocks instead of distributing large dividends). Thanks to the increase in the price of oil in 2022 the Company increased its annual earnings by over 100% (30% CAGR over the last decade).

During the temporary crash in the global airline industry because of the COVID crisis, we also took advantage of the crisis to buy the stocks of HEICO (HEI.A/HEI), a Florida-based company which designs and manufacturers parts for the aircraft and aerospace industries. This is a company with great economic attributes and financial stability. They have proven themselves to be very skilled acquirers of companies while allowing the acquired companies to continue to grow autonomously over time under the Heico name. The price of its stocks dropped during the crisis, but its economic value dropped more moderately (Heico maintains a positive cash-flow throughout the year), and they seem to be overcoming the crisis with much success. We bought the company's stock when they were "on sale" during the pandemic and they are likely to yield significant profits in the long term.

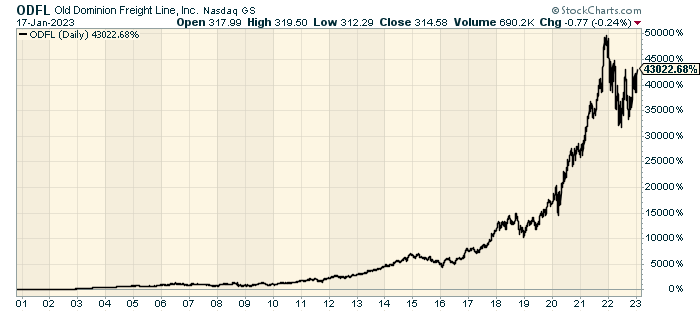

A New Compounder I recommended buying in 2022

In 2022, we have also added to our portfolio the successful American transport company Old Dominion Freight Line (ODFL). Notice the stock's price (see graph below) since the beginning of the current century in spite of its slightly "boring" area of activity (the company is in the transportation business for nearly 100 years), the company's stock generated an overall return of 43,000% (a CAGR of almost 29% since 2000). And this is while the S&P 500 index increased by about 350% (less than 7% a year). As a result, its market cap today is over 35 billion dollars.

{kind=link}

Thanks to the unusual profitability of the company and its position in the industry, and mainly thanks to its remarkable management, I have started recommending buying its stock, with an anticipation to keep it for many years to come (I would like to express my gratitude to my educated colleague Shree Viswanathan from the SVN Capital fund, who brought to my attention this outstanding company). This company's stocks are an excellent example for "winning" stocks which may belong to "boring" industries. The stock is not cheap today, its P/E ratio is above 25, but it increases its value by a double-digit rate yearly for many years already, thanks to the consistent organic growth of the company. Despite a challenging economic environment, the value of the stock increased by over 10% in 2022 and in almost 20% since the beginning of 2023.

3. Special Situations and Cash

The role of this category is to serve as a more "conservative" backdrop in our portfolios. In order to diversify our stock-focused portfolios, we use the cash that has accumulated in the investor's portfolio and invest it in a more "conservative" fashion. To this end, we search the global markets for special situations such as tender offers, re-organizations, delisting, mergers and acquisitions that can provide us with opportunities to make lower risk investments with a target date of return. These investments may yield low returns over short-term periods of time but become very profitable over long-term periods.

Due to the many opportunities we find today in the first two categories detailed above, at this time we have a smaller allocation to this category.

4. Net Net Stocks

We recently added another investment strategy to our portfolios. While this strategy is similar to the investment strategy I described above, in this strategy we adhere specifically to a policy of investing in specific stocks called "net-net" stocks. This strategy was first applied by Benjamin Graham (the author of "The Intelligent Investor"), and it involves investing in stocks that trade at a price which is less than the company's net asset value. The market cap of "Net-Net" companies' is lower than the value of all the company's cash and current assets after deducting all of the company's liabilities. Companies that trade at such low prices, usually operate in "out of favor" industries. Due to their small market value most of the shares of the companies that meet this criterion will be out of the investment radar of most investors in the world. These days we find many ''Net-Net'' stocks in Asia (especially Japan), Europe and other countries. This strategy has been back-tested in many countries and has so far been proven to yield an excess return to market indexes of about 10% per year on average over time (there is of course no guarantee for the future). Graham himself used this strategy and managed to yield an annual return of almost 20% net for his investors.

On the personal level, as your portfolio manager, I am pleased to share with you some of my activities in the year:

- My colleague Gilad Slonim (Financial Planner) and I began a weekly podcast in Hebrew ("Investing in Value") where we discuss the careers and strategies of the Great value investors. The podcast can be found on YouTube and Spotify.

- I was invited by our Legal Advisor, Oded Ofek, to give an additional lecture to graduate students at the Hebrew University in which I talked to them about the teachings of the great value investors.

- I was selected to teach a Value Investing Course, administered by Interactive Brokers Israel. A big thank you to Lior and Meirav Shemesh from Interactive Israel and their team. We just finished our fourth placement for this course.

- I was interviewed by the renowned financial mentor. Thanks to this interview and the exposure it gave us, many of you joined our financial journey.

- I gave a talk at the yearly gathering of Epoch Israel- a link to the talk can be found on YouTube.

- My partner and friend, Matan Guetta, published two articles this year in the prestigious local economic paper- "The Marker".

- I published over the last five years thirteen articles in leading financial portals in Israel and abroad, including The Marker, BizPortal, Globes, Forbes and Seeking Alpha.

- Since early 2019, I have been regularly writing an investment blog on the website of The Marker, where I have already published 15 chapters.

- In light of the high demand for our I.R.A. services, we continued working with Meitav Dash, a leading broker in Israel. A big thanks is due to Mr. Ilia Shirshov from Meitav Dash who assisted us and gave our clients the personal attention they deserved. We also wish to thank Miri Shmueli from Meitav Dash for her assistance.

- I still enjoy the warm environment and cooperative work with the staff of IB Israel. This cooperation is very beneficial for us and for our clients. Special thanks go out to Meirav and Lior Shemesh and their staff, David Shem Tov, Itzik Shemesh and Liran Younger.

In conclusion, I wish to summarize again and share with you our "Ten Commandments" which underlie and direct us in our investment activities:

- Focus on high quality micro-cap value stocks which have a well-documented track record of achieving alpha and not on high-flying popular stocks.

- Identify and analyze the best Compounders in the world and invest in them as partners for the long term.

- Set a long-term goal of at least a 5-year to achieve investment returns.

- Utilize the powerful effect of compound interest on long-term investments on behalf of our investors.

- Refrain from any speculation and short-term trading.

- Not allow "noisy" headlines and catchy newsflashes about the stock market dictate our activity in this market.

- Stay away from any investment fads, the long-term economic value of which is highly questionable.

- Carefully analyze the past and present investment strategies of the world's best investors who are renowned for excellent financial performance.

- Continuously read and study professional/academic papers, reports and research in the area of investments/finances published around the world.

- Finally - rehash to our investors the message - "Patience is gold".

As usual I wish to thank for friend and Partner, Matan Guetta without whom this path we have set off would not have been possible and definitely not as enjoyable!

We wish to thank again our investors for the pleasure we get from working with you and for the trust you grant us. On our part, we will continue to work on your behalf in a fair, diligent, professional and trustworthy manner, while utilizing our investing strategy outlined above.

On a more personal note, this past year my precious wife Revital and I welcomed a baby girl to our life, beautiful Libbie, who joins her adorable brother Johanathan in our small and growing family.

Finally, I wish to also thank and send my love and admiration to my father, Prof. Israel Zelikovic, who edited and revised this Annual Letter, and of course, to my loving and devoted mother, Orly Zelikovic, both of whom continue to be role models for me and for our whole family. G-d willing may they be healthy for many years!

For further details see:

Zelikovic Investments Annual Letter 2022 (Updated Q1 2023)