ZION - Zions Bancorporation: A Strong Buy After Q2

2023-07-25 22:57:21 ET

Summary

- Zions Bancorporation reported strong Q2 earnings, with a growing book value and return of deposits.

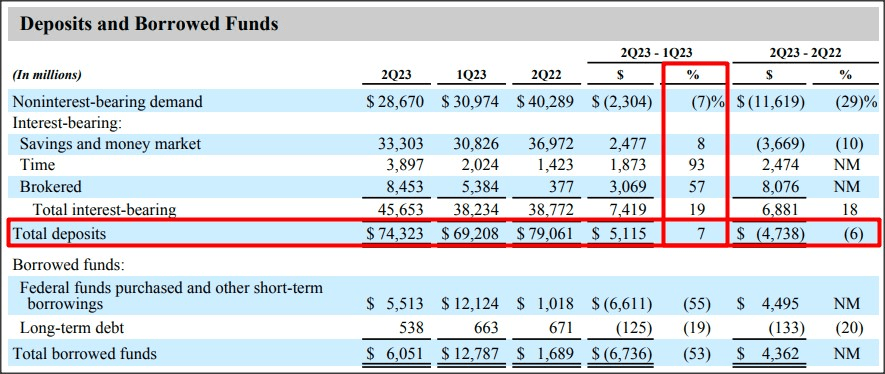

- Despite a 3.4% decline in deposits in Q1 due to growing fears in the system, ZION restored its deposit base in Q2. Total deposits increased $5.1B, or 7.4% Q/Q.

- ZION's net interest income declined due to rising deposit costs, but its book value nonetheless increased 2% in Q2'23 to $32.69 per-share.

- Shares are still trading at a discount to the historical 1-year average P/B ratio.

Zions Bancorporation, National Association ( ZION ) reported solid second-quarter earnings that showed a growing book value as well as an impressive return of deposits to the regional bank. While shares of Zions Bancorporation have already revalued to the upside in recent weeks and are now selling at a premium to book value, I continue to see revaluation potential going forward. Given ZION's pre-crisis valuation of $50, I see approximately 35% upside for shares of ZION as investor confidence In the regional banking market gets fully restored!

Previous rating

I recommended Zions Bancorporation at the end of June -- Zions: Strong Recovery Potential -- due to the bank's improving liquidity profile and significant discount to its 1-year average P/B ratio. If you acted on my last recommendation, you are up 19.67%.

Regional bank deposit flows have stabilized

ZION, like so many other small and vulnerable regional banks, saw a decline in its deposit base in the first-quarter: its average deposit balance declined 5.5% quarter over quarter to $70.2B while end-of-period deposits fell 3.4% to $69.2B. The negative trend in Q1’23 was made possible by the failure of Silicon Valley Bank and the resulting panic it caused in the financial system.

In the second-quarter, however, confidence in regional banks, especially those that hold a large amount of deposits for commercial customers, was slowly restored, in part because of the Fed’s emergency liquidity window that allowed banks to receive short-term liquidity in exchange for the pledging of high-quality collateral (such as Treasuries or mortgage-backed bonds).

In Q2’23, ZION’s deposit based (based off of end-of-period values) increased more than 7% to $74.3B. The regional bank, therefore, more than fully restored its deposit base in the second-quarter: in Q4’22, ZION had $71.7B in total period-end deposits on its balance sheet, meaning Q2’23 deposits surpassed the bank’s pre-crisis deposits by approximately $2.7B.

The restoration of ZION’s deposit base is a key reason why I continue to recommend the regional bank to investors.

{kind=link}

Source: Zions Bancorporation

Net interest income decline

What offset the positive news was the decline in the bank’s net interest income… which is something all banks have suffered from in the second-quarter. As deposit costs rise, banks are making less profit on their operations, resulting in a compressing net interest margin. In Q2’23, ZION reported a net interest margin of 2.92% compared to 3.33% in Q1’23. Going forward, the pressure on banks’ net interest margin should be expected to build until the Fed enters a new interest rate down cycle.

Source: Zions Bancorporation

Office real estate exposure

ZION is a regional lender and therefore has exposure to the commercial real estate market, but the exposure to offices is fairly limited... meaning investors don't have a good enough reason to avoid ZION's shares for fears of rising office loan defaults. At the end of the second-quarter, the regional bank had $12.9B in total outstanding commercial real estate loans, which represented a loan share of only 23%. For context, offices only accounted for $2.2B of loans, or 17% of total CRE exposure. According to ZION's Q2'23 earnings presentation, there were 0% delinquencies in the office loan portfolio in the second-quarter ( Source ).

Source: Zions Bancorporation

ZION is now trading at a premium to book value, but the risk profile is still favorable

ZION traded at a significant premium to book value before Silicon Valley and two other banks went out of business in Q1'23. Now, the discount to book value is no longer available, but ZION's shares are still trading significantly below their pre-crisis level.

ZION is now trading at a 13% premium to book value, well below their 1-year average P/B ratio. The current discount to book value is approximately 20% which I consider to be undeserved. ZION's book value grew 2% in Q2'23 to $32.69 per-share. If ZION revalues back to its pre-crisis valuation of approximately $50, then shares could have approximately 35% upside potential.

ZION’s risk profile and potential headwinds

ZION’s risk profile has fundamentally improved since the regional bank has been able to more than restore its deposit base in the second quarter. Other regional banks have also seen a stabilization of their deposit bases, and sentiment in the sector has profoundly improved as well. A compressing net interest margin is possibly the biggest risk for ZION at this point. What I don't see as a risk is ZION's commercial real estate exposure, which remained limited in the second-quarter and all office loans were performing.

Closing thoughts

Despite a major revaluation taking place over the last month or so, I still like ZION and I believe the regional bank made a convincing case for itself by reporting a strong sequential increase in its deposit base. Although ZION’s net interest margin declined, the bank’s book value was up a solid 2% quarter over quarter in Q2’23. Shares are no longer a bargain at 1.13X book value, but I see no reason why ZION’s pre-crisis valuation could not also be restored, although it may take a while for this to happen. ZION traded at $50 before the Q1’23 scare in the regional banking market and if ZION climbs back to this valuation range, shares could have a solid 35% upside potential!

For further details see:

Zions Bancorporation: A Strong Buy After Q2