ZION - Zions Bancorporation: Upbeat Q2 Earnings Shares Remain Undervalued

2023-07-20 11:43:03 ET

Summary

- Zions Bancorporation has rallied sharply in recent weeks and shares moved up again following a better-than-expected Q2 earnings report.

- While figures were largely down year-over-year, the drop was much less than the bears were expecting.

- Shares remain cheap, especially as it seems analyst expectations may be too low.

- I expect many regional banks, including Zions, to rally as investors realize that most firms face a near-term dip in profits rather than a solvency crisis.

Bank earnings season is here, and it's off to a strong start. The money center banks have delivered generally upbeat results with healthy lending activity, decent credit performance, and resilient profit margins.

And this week, we've seen a number of the leading regional banks report. The focus with the regionals has been more around deposits. Could the smaller banks hold onto their customer deposits in an increasingly competitive world especially after the failures of Silicon Valley and other banks which highlighted deposit flight as a risk?

So far, the answer appears to be a resounding yes. This brings us to the matter of Zions Bancorporation ( ZION ), which has been a controversial bank in 2023. It has one of the higher ratios of non-interest bearing deposits in the industry, which led the bears to assume there would be massive deposit flight from the bank given the current industry storm. Short interest was at an elevated 14.9% of the float coming into the bank's Q2 earnings report:

ZION stock information (Seeking Alpha)

Needless to say, Zions' Q2 earnings report did not shape up as the bears had been anticipating. Instead of a deposit flight, the company actually reported a rise in its deposit base. Earnings also beat expectations and the stock rallied significantly in after-hours trading Wednesday.

Q2 Earnings: The Sky Isn't Falling

Zions' Q2 earnings report is a classic example of what happens when a company beats low expectations. Because, on the whole of it, there were some negative points in Zions' earnings report. EPS fell to $1.11, down meaningfully from $1.29 from the same quarter of 2022. The bank's efficiency ratio went in the wrong direction, allowance for credit losses was up noticeably, and the bank's net interest income was down more than 10% sequentially from Q1 of this year.

Anyone nitpicking the Q2 release can find some issues to worry about. However, this is where the expectations game comes into play. Zions stock was down 38% over the past year heading into this report. Not too long ago, ZION stock was off by two-thirds from its prior peak. In other words, a lot of investors were acting like Zions might be the next Silicon Valley or First Republic (FRCB).

This earnings report showed that those worries were not well-founded. The most important figure of all was customer deposits. Zions reported $65.9 billion for that item, which was actually up 3% from the prior quarter. For all the talk about bank runs and people moving cash to get more yield, there's simply not much evidence of this occurring at any great scale at Zions or most other major regional banks.

From my perspective, the banking industry is facing a profitability issue, not a solvency issue. Until the inverted yield curve clears up, and more normal lending conditions return, banks will see their profit margins face pressure. But there's a huge difference between a short-term drop in profitability and potential insolvency. Regional banks stocks were priced for the latter, whereas, in my opinion, the banks that failed this spring largely did so due to unique challenges and bad decisions on the part of those management teams rather than a broader systemic crisis.

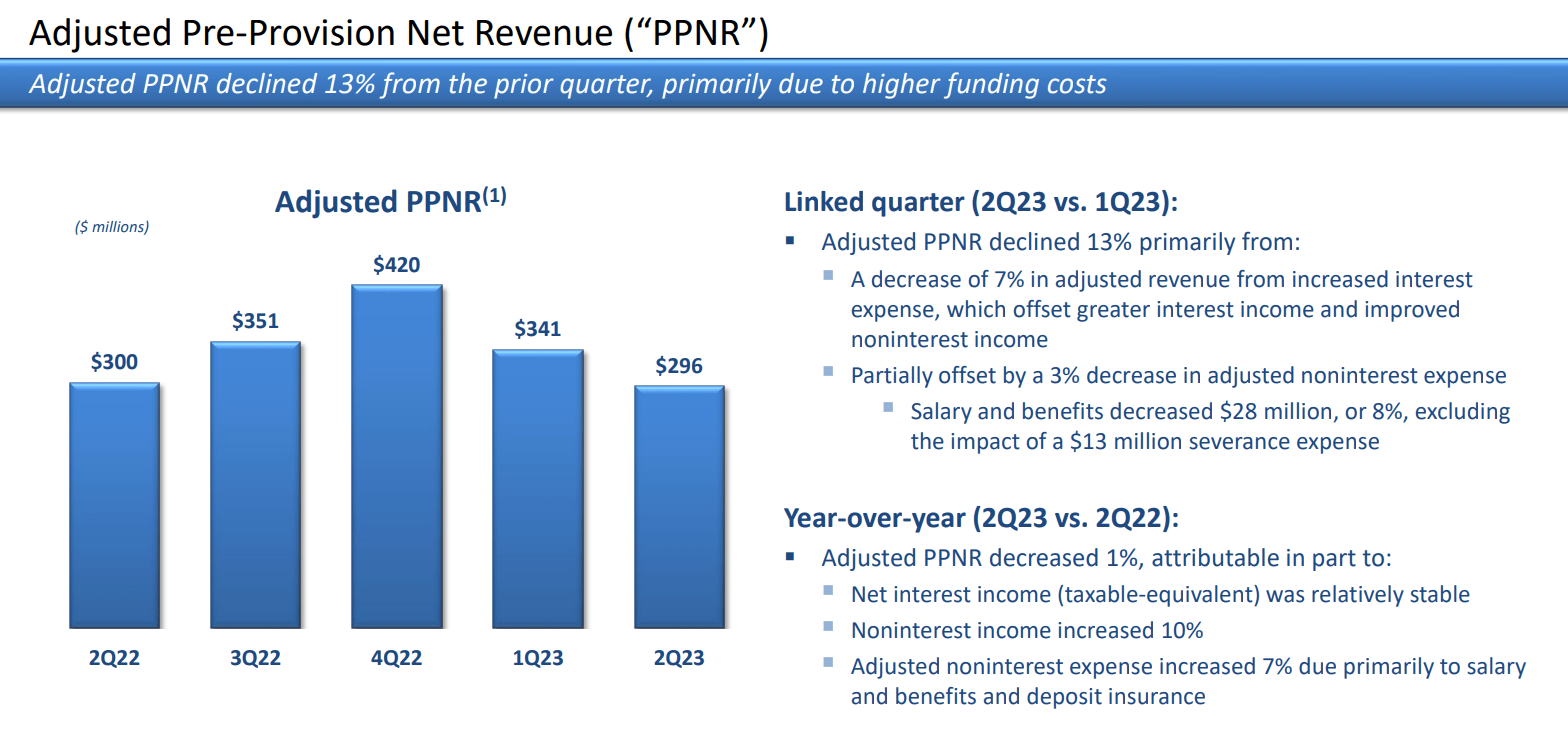

To the profitability point, here's Zions' pre-provision net revenue:

Zions PPNR (Corporate presentation)

{kind=link}

The company saw PPNR fall 1% year-over-year and 13% sequentially from Q1. That's not good -- it's a drag on earnings. But we're talking about a stock that lost as much as two-thirds of its value in a short period of time. A small decline in profitability doesn't justify anything like the sorts of collapses that we saw in Zions and other leading regional banking shares.

That's why we're seeing the sorts of vigorous rebounds now in the regional banking sector as these Q2 earnings roll in. Profits are facing significant headwinds for now, and that is likely to persist for a few quarters at least and perhaps longer if we see a meaningful recession in 2024. But there's a big difference between a 10% or 20% drop in EPS and a run on a bank's deposit book. As long as deposits are flat or even up, the industry will come out of the current volatility in fine shape.

To that point, Zions gave an outlook for the next year on its conference call, with CFO Paul Burdiss stating that:

"Our outlook for net interest income in the second quarter of 2024 is stable to slightly decreasing relative to the second quarter of 2023. Risks and opportunities associated with this outlook include realized loan growth, competition for deposits and the path of interest rates across the yield curve."

As per that statement, it seems Zions may already be near its trough net interest income for this interest rate cycle, with the outlook being flat to a slight decrease over the next 12 months. That, in turn, suggests that analysts may have been too bearish coming into this quarter as they were looking for an 18% drop in earnings in 2023 and another 9% decline on top of that next year:

Zions earnings outlook (Seeking Alpha)

Even with the prior analyst projections, Zions was trading at less than 8x projected 2024 earnings, and that moved back to 6.4x the 2025 outlook. If and when analysts raise their projections following this quarterly earnings beat, shares will look even cheaper on a forward earnings basis.

ZION Stock Verdict

I'm not the only one sharing a bullish view on Zion's. Morningstar's Eric Compton came into this quarter with an audacious $58 price target on ZION stock, saying that shares were "materially undervalued". I'd further note that even in Compton's bear case for ZION, he still reached a fair value of $44 per share, and that assumed a material degradation in the firm's operating results.

I'd argue that the $20 share price we saw on Zions earlier this year was irrational and entirely driven by market panic rather than any informed assessment of fundamentals. The stock has bounced a long way off the low, to be sure, but shares are still down sharply year-to-date. That's in stark contrast to the overall stock market, which is up considerably.

I believe that well-run banks with healthy deposit bases, like Zions, will suffer little-to-no material damage from the banking industry scare we saw earlier this year. As such, I expect all the losses suffered by these sorts of banks to be recouped as the fear continues to let up and investors return to the regional banking sector. ZION stock started off the year trading around $48/share. Don't be surprised if we see that price again in the not-too-distant future.

For further details see:

Zions Bancorporation: Upbeat Q2 Earnings, Shares Remain Undervalued