ZION - Zions Bank: From A Great Buy To A Good Buy On The Rally

2023-07-24 11:53:24 ET

Summary

- Zions Bank's stock has risen by 25% to $36. My price target of $45 is up another 25%, plus the 4.6% dividend yield.

- Despite rising deposit costs, possible increased capital requirements, and office loan risks, Zions Bank expects its EPS to remain stable over the next year at its Q2 $1.11 level.

- I expect Zions to eventually return to loan portfolio growth and to revive its share repurchase program, so EPS will eventually start growing again.

This is my fourth article on Zions Bank ( ZION ) for Seeking Alpha. The first three were written when the stock was in the $28-$30 range. Now it's at $36, so up about 25%. The stock is no longer a steal, but I continue to believe that it's worth $45, or up another 25%. So still a good buy. And you get a 4.6% dividend yield while you wait.

Zions' stock got cheap because emotions overwhelmed reality. Now those negative emotions are fading and reality is resurfacing. So yes , Zions is dealing with some issues at present. But Zions has a number of offsets and protections against those issues, as it displayed in its Q2 earnings it reported last week. This article reviews these "Yes, but…" issues:

- Yes, three big banks failed, causing a deposit safety panic. But…

- Yes, deposit costs are sharply rising. But…

- Yes, office mortgage loans have gotten a lot riskier. But…

- Yes, bank regulators are considering increased capital requirements. But…

- Yes, EPS declined from a year ago. But…

Yes, three big banks failed, causing a deposit safety panic. But…

Four months ago, Silicon Valley went bust, setting off a panic that uninsured bank depositors were going to lose their money due to widespread bank failures. But since then, two realities made themselves evident:

- SIVB, First Republic and Signature uniquely mismanaged their interest rate risk.

- The federal government simply cannot let uninsured depositors lose money in a bank failure. They never have, and never will; it would cause an unacceptable economic crisis.

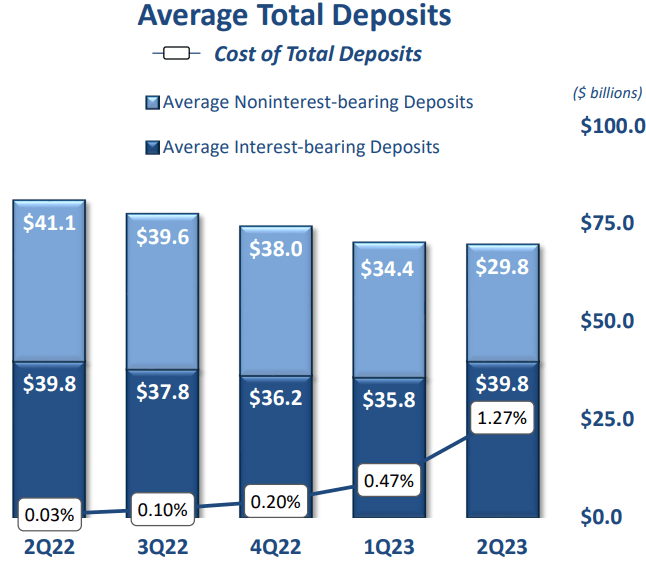

So yes, Zions lost a lot of customer deposits during Q1 due to the panic, and for several quarters prior as COVID cash was spent. But customer deposits stabilized during Q2, as the chart below shows. And the public panic has pretty much faded without a trace.

{kind=link}

Source: Zions Bank Q2 earnings presentation

Yes, deposit costs have been sharply rising. But…

As the fleeing-depositor panic started to subside, the media worry about regional banks shifted to "Rising deposit costs are going to eat up regional bank earnings." Yes, I am excited that I can park money safely at 5%, and I'm sure you are too. And yes, Zions' deposit costs rose from a measly 0.03% a year ago to 0.47% during Q1, to 1.27% during Q2. And yes, Zions' deposit costs are going a lot higher.

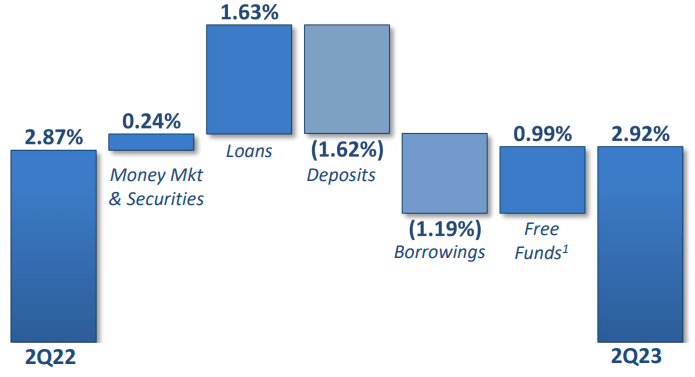

But… Zions' interest margin of 2.92% this past Q2 was actually higher than the 2.87% a year earlier. And Zions forecasts that its net interest income will be " Stable to slightly decreasing " over the next year. How? This is how:

{kind=link}

Source: Zions Bank Q2 earnings presentation

Versus a year ago:

- Rising deposit costs reduced Zions' interest margin by 1.63%

- Rising borrowing costs reduced the margin by 1.19%

But…

- The bulk of Zions' loans are variable rate, so rising loan yields added back 1.63%

- The yield on its securities rose and added 0.24%

- Zions still has $30 billion of non-interest-bearing deposits - checking accounts, etc. As interest rates rise, they get more valuable. That added 0.99% to Zions interest margin.

Zions management expects these trends to roughly remain in place over the next year. The bottom line is that, unlike SIVB and First Republic, Zions carefully manages its interest rate risk exposure.

Yes, office mortgage loans have gotten a lot riskier. But…

The media is all over the theme of hollowing out of office buildings due to work-at-home, and the serious risk that creates for office mortgage lenders like Zions. But how do you explain these facts:

- Zions' charge-offs on its $57 billion loan portfolio were a measly $13 million during Q2. Annualized, that is less than 0.10% of loans.

- None of the charge-offs were commercial real estate loans.

- Both delinquent and worrisome loans declined during Q2, and steadily over the past year.

Oddly enough, Zions knows that loans can go bad. It therefore carefully underwrites its loans. For example, only $2 billion of Zions' $57 billion of loans are on office buildings. The average office loan is only $4.6 million, and the average loan-to-value ratio is less than 60%.

Yes, bank regulators are considering increased capital requirements. But…

The federal government - meaning you the taxpayer - covers the losses when a bank fails. As a result, the government, over time, has added more and more regulations on banks to limit the costs of bank failures.

Talk is that more regulation is coming. Bank regulators may require banks (maybe just large banks) to hold more shareholders' capital as a percent of assets. My editorial comment is that this is a misguided idea. SIVB and First Republic went bust because of poor interest rate risk strategies that were discredited back in the 1970s. Lax regulation of individual banks' interest rate risk was the problem. Increasing capital requirements will just discourage bank lending and therefore hurt the economy.

With more capital requirements being discussed, Zions is restraining its asset growth - it expects earning assets to be flat to down over the next year. And Zions' share repurchase program, which reduced shares outstanding by 29% over the past six years, is on hold for at least the next few quarters. Earning asset growth and share repurchases are the drivers of Zions' EPS growth.

But… (You knew that "but" was coming!) But:

- Zions has plenty of capital and has no reason to raise any to support its current balance sheet.

- Zions has started an expense control program which kept Q2 expenses flat with Q1, and management expects to keep expenses flat over the next year.

- Zions is maintaining its $1.64 dividend.

Yes, EPS declined from a year ago. But…

Here is Zions' EPS over the past five quarters:

Zions Bank Q2 earnings presentation

Source: Zions Bank Q2 earnings presentation

Looks bad, right? But:

- Zions added $0.18 per share to its loan loss reserve, so Q2 cash earnings were $1.29 per share.

- Zions' EPS, similar to other banks, has been buffeted up and down since 2020 by COVID credit risk issues and the Federal Reserve's roller coaster interest rate policies. The Q2 $1.11 EPS compares favorably to Q2 2019's $0.99 EPS.

- Zions forecasts roughly flat EPS over the next year.

- Most importantly, think about how the $1.11 compares to expectations. Zions' low stock price this year was $18, and it traded at $34 right before it announced Q2 earnings. The $1.11 means way-below market average P/E ratios of 4.1 times the bottom and 7.8 times last Wednesday's close.

Wrapping up- The stock is no longer a steal, but it remains cheap

Zions' current 8.1 P/E multiple implies that its EPS will trend down over time. To help visualize my conclusion, consider that Zions' "earnings yield" - the flip of the P/E ratio - is 12%. That would be an awesome return if Zions never grew EPS again. My target price of $45 takes the earnings yield to a still-conservative 10%.

For further details see:

Zions Bank: From A Great Buy To A Good Buy On The Rally