ZION - Zions Is Unlikely To Benefit From Fed Rate Cuts (Rating Downgrade)

2024-01-11 13:30:57 ET

Summary

- Zions Bancorporation's stock has recovered sharply in the past three months, but it is still lower than a year ago.

- The decline in interest rates has helped alleviate concerns about unrealized losses on bank balance sheets, but lower rates will also reduce bank profits.

- Zions Bancorporation may struggle to generate sequential earnings growth and its shares have reached fair value, so investors should consider rotating exposure elsewhere.

Shares of Zions Bancorporation ( ZION ) are still lower than a year ago, significantly lagging the market; however, they have recovered sharply. In just the three months since I rated ZION a “ strong buy ,” its stock has returned one-third, moving above my $40 price target. Given the strength of this move and the fact the business is not without challenges, I would use this strong move to take profits and am moving my recommendation down to a “hold.”

{kind=link}

Bank shares have recovered meaningfully in recent months as interest rates have fallen. Currently, the market is pricing is in six rate cuts by the Federal Reserve this year. This has helped to alleviate concerns about the unrealized losses sitting on bank balance sheets in accumulated other comprehensive income (AOCI). Additionally, declining interest rates should over time reduce funding costs for deposits. However, lower rates will also reduce the yields banks earn on their floating rate loans, meaning that a Fed that is cutting rates is not entirely good news for bank profits.

Additionally, ZION benefits less from declining unrealized losses on it securities portfolio. Because the bank has under $100 billion in assets (it had $87 billion in Q3), it does not need to phase-in AOCI into its capital calculations, like bigger peers will. Now, management certainly pays attention to its economic capital position, but firms like PNC ( PNC ) will see greater regulatory relief from declining unrealized losses and lower bond yields than ZION. As a consequence, investors hoping for meaningful share repurchases to be discussed when it reports Q4 earnings on January 22 nd are likely to be disappointed, and given ongoing economic uncertainty and rate volatility, I expect management to remain cautious with significant buybacks more of a 2025 possibility.

The decline in rates has increased optimism about banks’ earnings power because they were enjoying wider net interest margins before the last several Fed rate hikes. Looking at ZION, its net interest income of $585 million in Q3 was down from $663 million a year ago. Net interest margin stabilized at 2.93% sequentially but was down 60bps from Q4. That is why in the bank’s third quarter, ZION earned $1.13 down from $1.40 last year.

A key focus for investors this earnings season should be on the trajectory of NIM and net interest income in 2024. If they revert to 2022 levels, bank shares have more upside; if they are going to hold nearer H2 2023 levels, shares are more fully valued. In Zion’s case (as with most of the industry), I expect profits to remain below 2022 levels, and I continue to expect ~$4.50 in earnings power in 2024. If that is the direction of management guidance, I expect shares to pause after their significant rally.

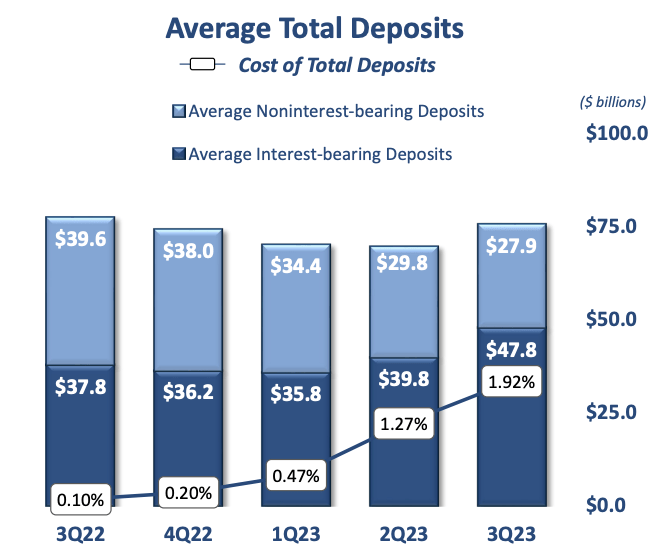

In an effort to restore liquidity after the deposit flight in early 2023, ZION has pulled back on lending. Last quarter, period-end loans were held flat sequentially while period-end deposits rose by 1.4%, bringing its loan to deposit ratio down to 75%. This is a more sustainable level, and I would expect loan growth to match or slightly lag deposit growth in 2024. The challenge will be that I expect deposit costs to remain somewhat elevated. As you can see below, while ZION grew deposits last quarter, there was a significant cost with its deposit cost up 65bp sequentially.

{kind=link}

A reason for this is that noninterest-bearing ((NIB)) deposits fell another $1.9 billion. While its deposits are essentially flat from a year ago, NIB balances are nearly $12 billion lower. I expect this to be a permanent shift. After years of near-zero rates, some depositors may have grown complacent to earning nothing, keeping excess cash in NIB accounts. But having moved into 5+% yielding products, even if the Fed funds rate falls to 3%, I expect some permanence to this behavior shift as they are unlikely to move out of 3% products into 0% deposits. This mix shift to more interest-bearing deposits means even at the same Fed funds rate, deposit costs are likely to be higher than in the past.

This is also true because deposits are scarcer today than 18 months ago, and when something is scarcer, it is typically costlier. The Federal Reserve has been steadily reducing its balance sheet, and this reduction is likely to continue over the coming year. As the Fed withdraws excess liquidity from the system, deposit rates may not fall as quickly as the fed funds rate, limiting the scope for NIM expansion.

{kind=link}

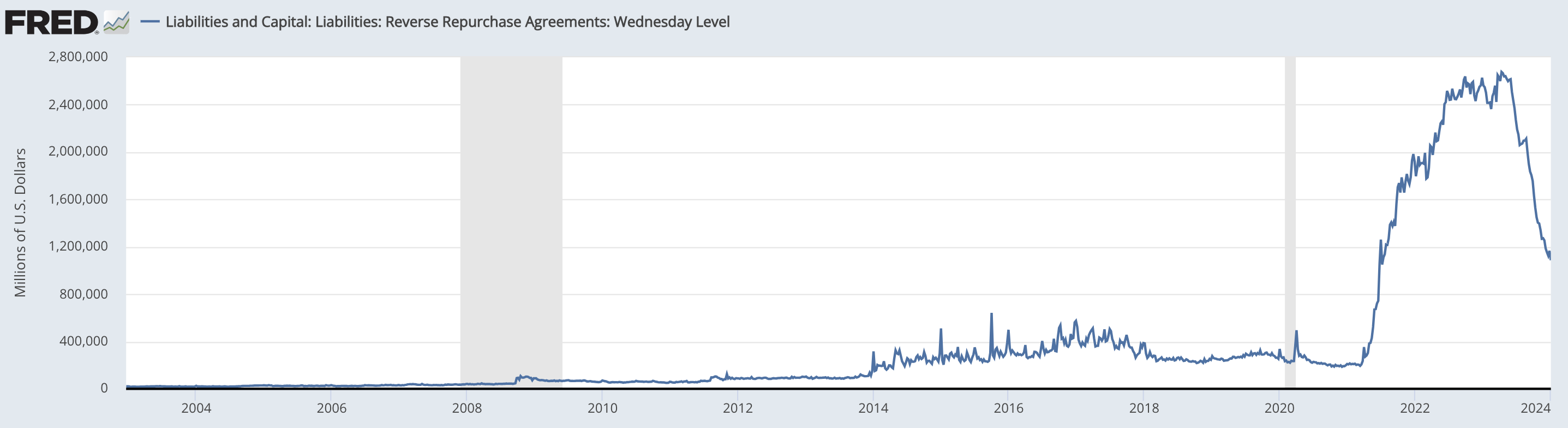

Indeed, I like to track reverse repo agreements to the Federal Reserve. This facility is essentially where the Fed sucks up excess liquidity from money market funds, paying roughly in-line with the fed funds rate. As you can see, as the Fed has withdrawn liquidity and as the treasury has continued to run a deficit, excess cash has steadily fallen from over $2.5 trillion to less than $1.2 trillion. As this continues to dwindle with Fed balance sheet reductions, it may be difficult for banks to cut deposit rates as quickly as they raised them.

{kind=link}

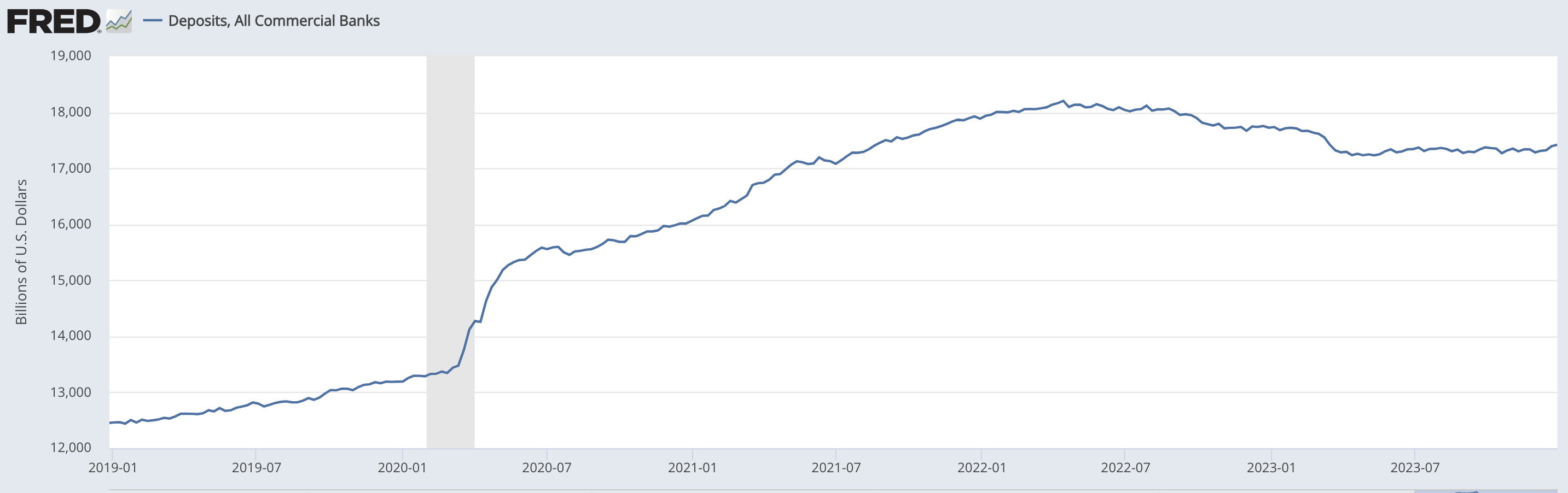

To be clear, I am not arguing deposits rates will not fall at all. Just that they are unlikely to fall as quickly as the fed funds rate. On the bright side, we have seen deposit levels across the industry stabilize, a positive from the declines seen in March and April of 2023. Banks are no longer fighting over a shrinking pie. However, deposits are now flattish; they are not growing. With ongoing Fed balance sheet reductions, they are unlikely to meaningfully grow either. As banks fight over a static pie, that can pressure deposit pricing as industry loans continues to rise, increasing some banks’ needs for deposit funding.

{kind=link}

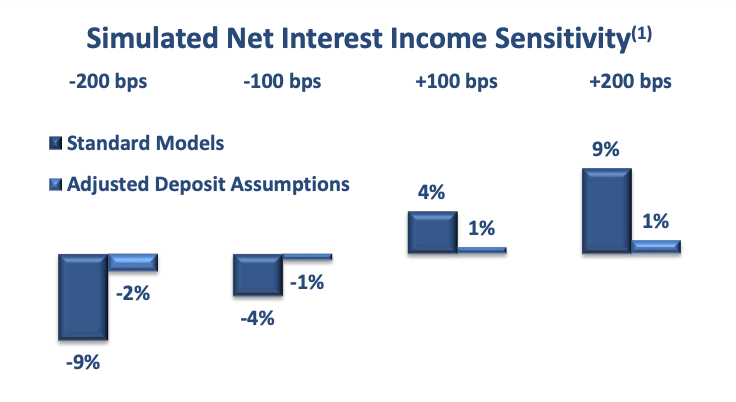

This analysis brings me to Zions’ own projections. As you can see below, it expects its interest income to decline as interest rates fall. Now, its adjusted model essentially assumes that the higher deposit beta we have seen in recent months continues. This is why higher rates do not boost income as much as its “standard” model as higher funding costs offset increased loan income. By the same token, if deposit rates fall as quickly as they rose, ZION is relatively immune to rate cuts.

{kind=link}

My concern is that while the “adjusted model” may be right in a higher-rate environment; the standard model of low-deposit betas could occur during 2024 because while the Fed is cutting rates, it is also reducing its balance sheet, draining more liquidity from the system and keeping bank competition for funding fiercer than it otherwise would be. In that environment, it will be difficult for ZION to increase earnings meaningfully. Now, there will be some modest tailwinds, like increased fee income. Additionally, its securities portfolio is down to $20.7 billion from $24.2 billion last year. With a 3.5 duration, it will continue to generate substantial liquidity with which ZION can reinvest or lend at higher yields.

Lastly, one of Zion’s strengths is its solid underwriting with a 0.1% long-term charge-off rate. It is quite well reserved. Its 1.3% allowance for losses to loans ratio more than 3x its 0.41% nonperforming asset rate. That is better than my 250% healthy level, and so we should see provision costs decline in 2024 somewhat, especially as lower rates should help borrowers refinance and roll over debt.

While these efforts can help keep earnings around its recent run-rate, Fed rate cuts are more likely to be a headwind for income than a tailwind, which is why I see its Q3 annualized earnings rate of ~$4.50 likely to be about as strong as ZION can generate in 2024. At nearly 10x earnings, this is now fully priced. Moreover, ZION has a tangible book value of $25.75. This is $46 excluding unrealized losses on its securities portfolio. I expect book value to rise above $28 in Q4 as securities are marked higher, but this will not impact its ex-AOCI book value. There also is still some economic cost to having bought bonds at lower yields, and so I expect shares to remain below $46.

In a market that has rallied so much, it can be tempting to look for stocks still lower than a year ago. In Zions’s case, its shares should trade lower than 12 months ago because the deposit funding environment is fundamentally different. Even as the Fed cuts rates, we are unlikely to see NIM return to its lofty 2022 levels as a result, and ZION will struggle to generate sequential earnings growth. It does pay a secure dividend, but trading up against book value ex-AOCI, markets have grown too optimistic on what rate cuts will do for the business. I see shares having reached fair value and would look to rotate exposure elsewhere.

For further details see:

Zions Is Unlikely To Benefit From Fed Rate Cuts (Rating Downgrade)