ELAN - Zoetis: High-Quality Compounder With A Reasonable Price After Earnings

2023-11-09 12:58:30 ET

Summary

- Zoetis is the largest player in the animal health industry, with high returns on capital and steadily growing margins.

- The company operates in two main categories: livestock, which is growing slowly, and the faster-growing companion market for pets.

- Management incentives align with shareholders.

- Pricing power is great and is one of the main strategies.

- Reasonable price for a high-quality company.

My Thesis

Zoetis ( ZTS ) is a niche company operating in the animal health industry. It is the largest player in this field, and I appreciate several aspects of this company. Zoetis boasts high returns on capital, steadily growing margins, a stable source of recurring revenue, good management incentives, and operates in a growing industry. One of its goals is to continue expanding within this industry.

Furthermore, I believe it is currently trading at a reasonable price. While it may not be heavily discounted, the price is positioned for good potential results.

The Business

Zoetis operates in the animal health segment, where it is the largest player. The company divides its business into two main categories: the livestock category, which is growing slower, experiencing a 2% decrease in the last report. However, the long-term guidance suggests a CAGR between 2-4%. This category encompasses health solutions for Ruminants, Swine, Poultry, and fish.

The lion's share of Zoetis' business, and the fastest-growing one, belongs to the companion market. This segment experienced an impressive 11% growth in the last quarter, contributing 78% to the revenue (Q3). It is projected to be a least 70% by 2027. The companion market focuses on health solutions for pets, primarily catering to dogs and cats. This is an exciting market with significant growth potential ahead.

Zoetis primarily sells its products to veterinarians, who, in turn, offer them to their customers. With a product line boasting 300 items, Zoetis covers a range of categories, including parasiticides, vaccines, dermatology products, anti-infectives, other pharmaceutical products, medicated feed additives, and animal health diagnostics.

The company highlights segments such as OA pain, renal, cardiology, and oncology as its innovative and high-growth areas.

Zoetis stands out as the market leader in a growing market, currently commanding approximately 27% market share and still expanding. A noteworthy goal set by the management is to achieve revenue growth surpassing industry standards—an ambition I find commendable.

As a successful spinoff of Pfizer ( PFE ), Zoetis faces competition from major players. However, unlike its competitors, all of whom are subsidiaries of large pharmaceutical companies, Zoetis is a dedicated leader in animal health. Key competitors include Merck Animal Health ( MRK ), Boehringer Ingelheim, and Elanco ( ELAN ), formerly a subsidiary of Eli Lilly.

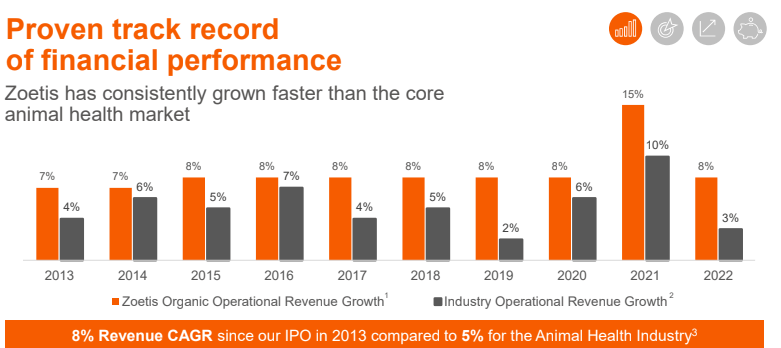

Before we explore the avenues of growth, let's appreciate Zoetis's pricing power. One of the primary drivers of top-line growth for Zoetis is its ability to increase prices. In Q3 , out of the 8% operational revenue growth, 5% is attributed to price increases, while 3% is from volume.

Zoetis can continue to raise its prices for a straightforward reason—people deeply care about their pets and are willing to go to great lengths for them, including paying higher prices. Consider these compelling facts from Zoetis's investor presentation :

86% of pet owners would pay whatever it takes if their pet needed extensive veterinary care.

When faced with a 20% decrease in budget, pet owners will not spend less on their pets.

High income households often have more than one pet and are more willing to spend during a down economy

Furthermore, Forbes has discovered that pet owners are willing to make personal sacrifices to meet their pets' needs. A significant majority, 85% of dog owners and 76% of cat owners consider their pets to be integral members of their family. A Forbes Advisor survey of 10,000 dog owners revealed that these individuals willingly make professional, financial, and lifestyle sacrifices for the well-being of their canine companions.

Pricing power (zoetis ir)

These facts alleviate my concerns about the viability of price increases as a long-term strategy. People go to great lengths for their pets, treating them as integral family members. Much like caring for their own children, individuals are dedicated to ensuring the health and well-being of their furry companions.

Where Will The Growth Come From?

The long-term growth drivers in the companion market are multifaceted. Firstly, there's a surge in pet ownership in the U.S., with 66% of households (86.9 million homes) owning a pet as of 2023—up from 56% in 1988, according to pet ownership statistics. Furthermore, higher-income families, known to adopt more pets, coupled with the economic growth in emerging markets, are expected to boost pet adoption rates. This, in turn, will lead to increased demand for medical care, a niche that Zoetis expertly fills. Additionally, the rising trend of Gen Z and millennials humanizing their pets bodes well for Zoetis. As these demographics earn more over time, there's an optimistic outlook for increased spending on their beloved pets.

For the slower-growing livestock segment, Zoetis emphasizes population and GDP growth as key drivers for demand. With the world population expected to grow and an anticipated need for 2 billion more mouths to feed by 2050 , the demand for protein will rise, necessitating the raising of more animals. It's worth noting that while plant-based solutions have gained traction in recent years, their efficacy is wavering.

Meat consumption will rise (zoetis ir)

Furthermore, as highlighted in both segments above, the strategy of implementing price increases is poised to drive top-line growth.

Mergers and acquisitions (M&A) serve as another avenue for growth, allowing Zoetis to enter new markets. A notable example is the acquisition of Jurox, an Australia-based livestock company.

Zoetis emphasizes a long-term industry growth projection of 4-6%, primarily driven by the companion market. A key management goal is to surpass market growth, a feat they have achieved since the IPO, with a consistent annual increase of 3%. Based on this, one can anticipate a robust 7-9% top-line growth in the long term.

higher revenue growth than the market (zoetis ir)

{kind=link}

Important Figures

In addition to top-line growth, there are several crucial ratios that I find impressive about Zoetis.

Firstly, the consistently high, stable, and growing linear margins are indicative of pricing power and ongoing efficiency. This outstanding margin expansion has allowed Zoetis to achieve higher growth in earnings per share than in revenue, showcasing operational leverage with a remarkable 15% CAGR since its inception. Notably, this growth occurred without significant buybacks, further enhancing the EPS.

These elevated margins also contribute to the impressive returns on capital that Zoetis consistently achieves, which, in my perspective, are as crucial as top-line growth. I appreciate that the management team places a focus on maintaining a high return on invested capital as one of their objectives. Recent research by Morgan Stanley indicates that high and growing ROIC contributes to outperformance among companies. Zoetis not only demonstrates impressive figures in this regard but also maintains stability, adding to its overall appeal.

Debt

Zoetis appears financially robust in my assessment. With a net debt of $4.8 billion and 70% of its $6.5 billion debt maturing after 2027, the company's debt structure seems well-managed. I find it reassuring that it could cover its net debt within 3 years based on free cash flow. Zoetis boasts an interest coverage ratio of 11, surpassing the recommended level of 3. Additionally, its current ratio stands at a healthy 3, and the debt-to-equity ratio is a solid 1.2. The Altman Z score, exceeding 7, further supports the company's financial strength. Considering its predictability and recurring revenue, Zoetis appears perfectly healthy in my view.

Return To Shareholders

Zoetis offers a modest dividend of 0.9% , but what's truly remarkable is its impressive growth rate—20% CAGR for ten consecutive years. The company aims to boost its dividend at a faster pace than net income, a goal it has successfully achieved thus far.

While Zoetis may not have reduced its outstanding shares as dramatically as some other companies I've covered in the past, the 8% reduction since inception is still noteworthy. It contributes to the long-term growth of earnings per share. The management's systematic approach to buybacks aligns with one of their goals, a strategy I appreciate for its proven ability to create compounding effects.

Management

CEO Kristin Peck has skin in the game, holding 263,824 (2022) shares valued at about $40 million. What's even more appealing is that over 70% of her annual compensation, totaling around $14 million, comes from long-term equity incentives. I appreciate this alignment, as I believe it ensures the CEO's interests are in sync with those of the shareholders.

Additionally, the company extends this alignment to the rest of the management team, ensuring their interests are closely tied to those of the shareholders:

Emphasize pay for performance— our executive compensation program emphasizes variable pay over fixed pay, with more than three-quarters of our executives’ target compensation tied to our financial results and stock performance.

Furthermore, the alignment of interests extends to the directors, where more than 70% of their compensations are in the form of equity.

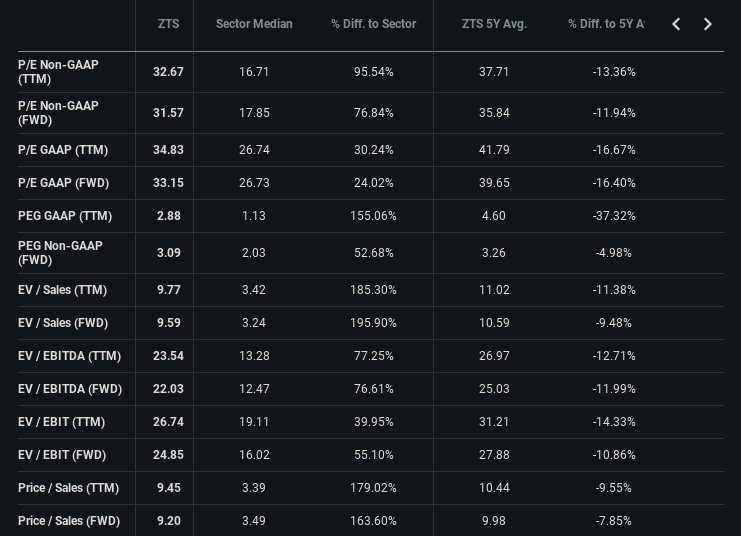

Valuations

I prefer to invest in companies when their trading multiples are below their historical averages, indicating potential for margin expansion. Zoetis aligns with this strategy, and it's not common for high-quality companies to reach these levels. Additionally, I have a preference for companies with free cash flow yield approaching 5%, although this condition may not always be met by quality companies.

{kind=link}

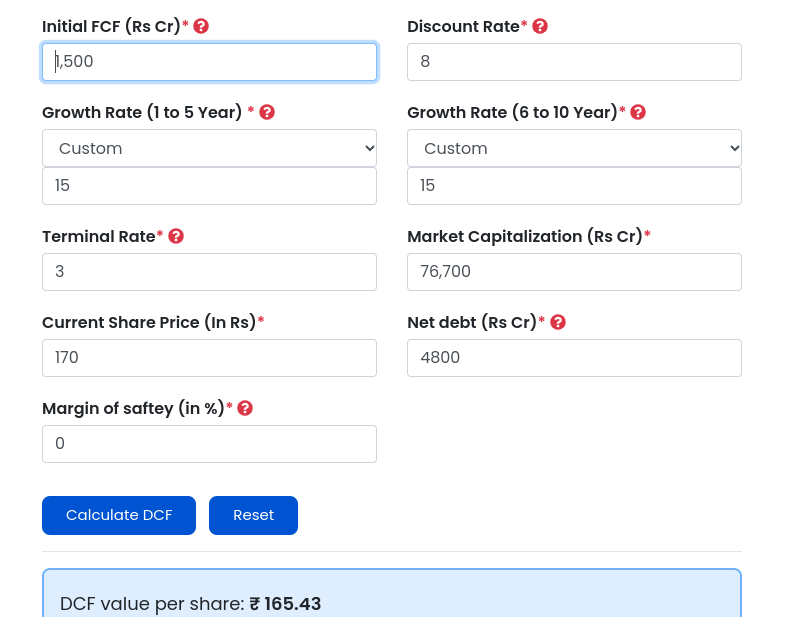

In my discounted cash flow analysis, I'll explore two scenarios: the bear case and the bull case.

For the bull case, I assume Zoetis will maintain a performance similar to its historical trend. I use a projected revenue of 2023 with an 18% free cash flow margin, consistent with the five-year average . The discount rate is set at an 8% WACC, and the terminal growth is 3% to account for global expansion. The FCF growth rate aligns with the last 10 years' EPS CAGR at 15%. The result suggests Zoetis is a perfectly valued company, with an intrinsic value of $165. While it may not be significantly undervalued, I believe its quality, akin to other high-quality companies, is challenging to capture entirely in a DCF calculation.

{kind=link}

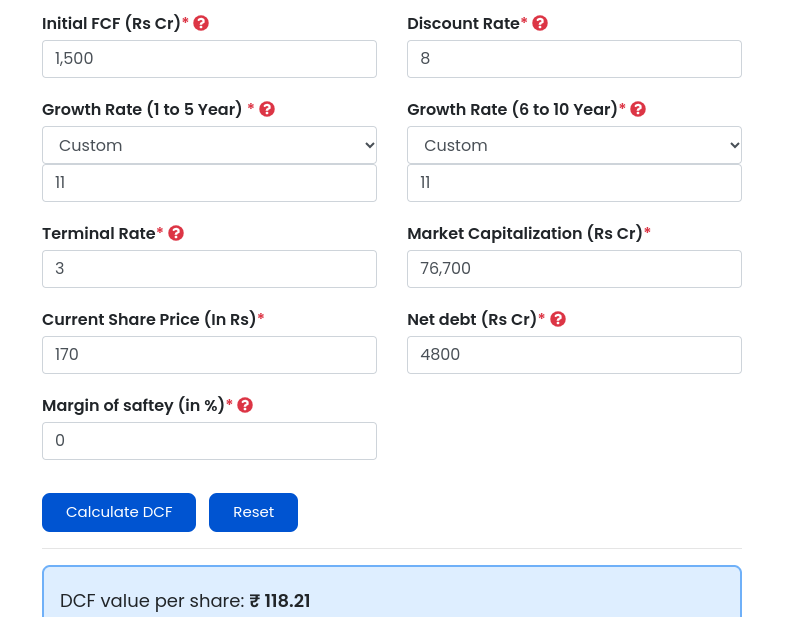

On the flip side, the bear case retains the same inputs but with a more conservative growth estimate of 11%, in line with analysts' projections for the next three years of EPS growth. This scenario paints a different picture, indicating a significantly overvalued company with an intrinsic value of $118, reflecting a 44% overvaluation. It's worth noting that Zoetis has consistently outperformed analysts' expectations, making these projections potentially less accurate.

{kind=link}

Indeed, an interesting anecdote underscores the robust performance of Zoetis. Even if you purchased Zoetis with a P/E ratio of 40 in March 2018, the subsequent performance has proven to outpace the market significantly. This serves as a testament to the company's strength and potential for rewarding investments.

Risks

While Zoetis's business seems relatively low-risk, a few factors warrant consideration. One concern is the global effort to combat carbon pollution, with cattle being a significant contributor. Innovations like lab-grown meat or alternative solutions could potentially impact the livestock business, although I perceive the likelihood of this happening as low.

Another potential risk lies in the failure to innovate and competition for patents in emerging markets.

Additionally, there's uncertainty surrounding the sustainability of price increases over the long term.

However, the most prominent risk, in my opinion, is the valuation, which currently lacks a margin of safety. This presents the greatest challenge and should be carefully monitored.

Conclusion

Taking into account the risk-reward balance and the array of quality attributes that Zoetis possesses—such as linearity, high return on capital, sustained growth, and pricing power—I perceive Zoetis as a compounder capable of maintaining its track record of outperforming the S&P. Additionally, I believe Zoetis has the potential to deliver solid returns with relatively low risk, a combination that can often be more impressive than high returns with high risks.

Overall, the favorable risk-reward profile leads me to rate the company as a BUY.

For further details see:

Zoetis: High-Quality Compounder With A Reasonable Price After Earnings