DDOG - Zscaler: Positioned For Success In The Evolving Cloud Security Market

2023-07-20 05:24:03 ET

Summary

- Zscaler is well-positioned to capitalize on the ongoing trend toward cloud-based security solutions.

- The company's strong position in secure web gateway and VPN/ZTNA, along with its product capabilities and ease of deployment, are key differentiators against competitors.

- I view ZS stock as a buy and have an end-of-year price target of $194 on the stock.

Thesis

I believe Zscaler, Inc. ( ZS ) provides a unique investment opportunity with significant long-term value potential. ZS excels in both security and network transformation, positioning it as a major player in the market. ZS's cloud security advantage, along with its product capabilities and ease of deployment, allows it to gain traction in workload security. As more companies migrate to the cloud, I believe Zscaler's leadership in this area will likely drive its growth further. I expect significant growth in applications. Zscaler is well-positioned to play a critical role in connecting users to applications and facilitating application-to-application connectivity in the cloud environment. I view the stock as a buy and have an end-of-year price target of $194 on the stock, based on EV/S multiples of 13.5x applied to the CY24 revenue estimate.

Company Overview

Zscaler is a cloud-based provider of Enterprise and Network Security, delivered over a distributed proxy network of over 150 Data Centers. Zscaler offers Zscaler Internet Access (ZIA) for secure access to internet and SaaS applications, and Zscaler Private Access (ZPA) for secure access to internal applications. The company has additional solutions in Zscaler B2B (ZB2B) for secure access to B2B applications, Zscaler Cloud Protection (ZCP) for cloud workload security, and Zscaler Digital Experience (ZDX) for management, analysis and remediation of user experience issues. Zscaler also has CASB, browser isolation, and DLP products which only recently ramped. Longer-term, Zscaler intends to get into application security in East/West cross domain traffic. Zscaler is a crucial enabler of secure SD-WAN and helps enterprises move to cloud-direct network architecture.

Q3 Review and Outlook

Zscaler reported strong 3Q23 results, exceeding the original guidance across metrics by wide margin , despite facing the same macro headwinds and longer sales cycles that all other vendors are seeing. Zscaler's higher orders in fiscal 3Q suggest that its exposure to large enterprises and government customers drove the better-than-expected 40% billings growth, in stark contrast with cloud peer Okta, Inc. ( OKTA ), which was hurt by lower upselling and a slowdown in IT spending at small and midsized customers. ZS's new products, such as ZPA continue to aid Zscaler's upselling and retention at existing customers, while the company's pivot to workload security from a seat-based model has improved its positioning vs. other security providers. I believe the company's data loss prevention product may see increased interest from companies seeking to protect against risks tied to the use of large language models like ChatGPT.

Workload Migration to Cloud Helps Adoption

Zscaler's leadership position in secure web gateway and VPN/ZTNA puts it in a strong position to expand lead over on-premise providers such as Broadcom ( AVGO ), Cisco Systems, Inc. ( CSCO ) and Forcepoint, which still makeup a significant of the market. Traction with companywide deployments remains key to faster share gains against appliance-based vendors that are still in the process of pivoting to cloud and trail Zscaler in terms of product capabilities. Zscaler has a strong advantage in cloud security, in my view, even with increased competition from firewall providers such as Palo Alto Networks, Inc. ( PANW ) and Fortinet ( FTNT ) that have also launched their cloud access security brokers ((CASB)) offerings.

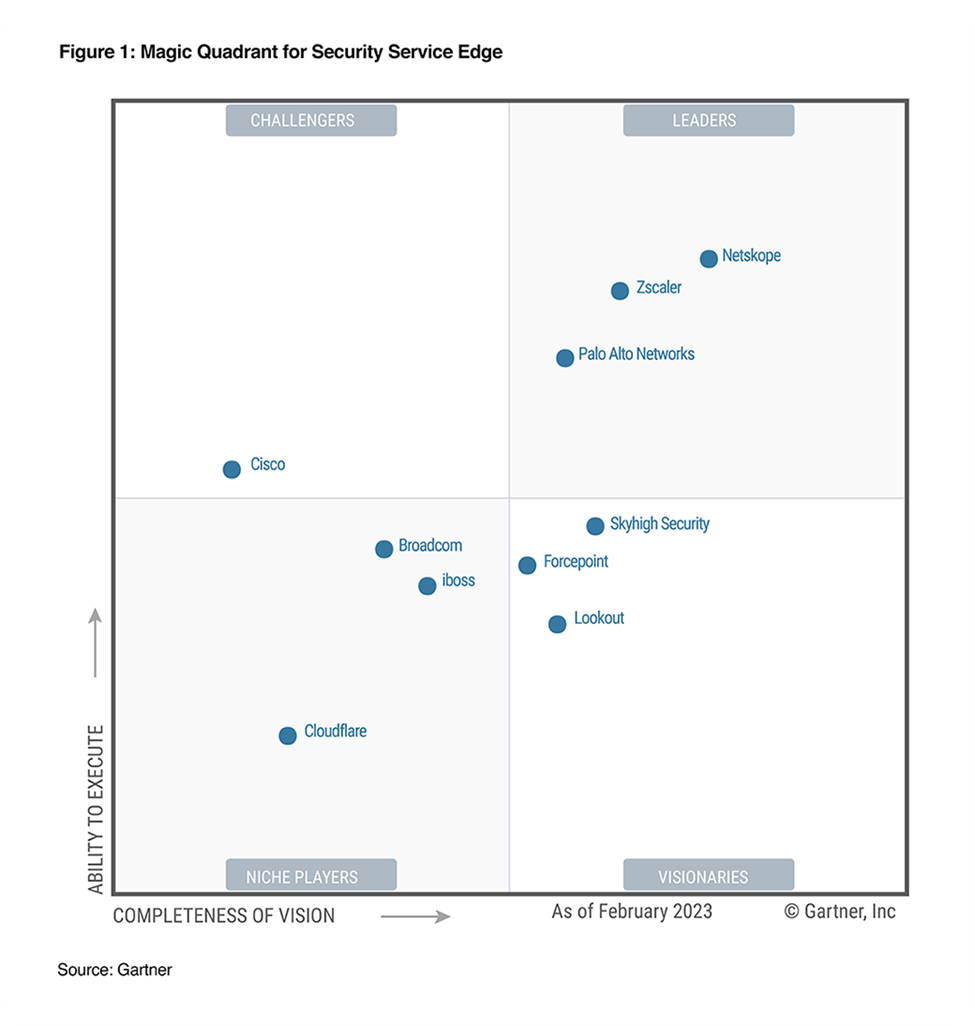

Zscaler's product capabilities, native integrations and ease of deployment continue to be differentiators vs. competing products from legacy providers such as Broadcom and Cisco. This is visible in Zscaler's strong position as a leader in the Gartner Magic Quadrant for security service edge. The company has much higher adoption at corporations that have migrated their workloads to the public cloud and lowered their reliance on traditional data centers. Workload migration from on-premise to cloud will likely be a multiyear growth driver for Zscaler, in my view, if the company can maintain its product lead on the cloud vs. incumbent firewall providers.

Zscaler is seeking to expand its total addressable market by extending its cloud-based deployment for web gateways to other large security segments, such as workload security. The company's category leadership position is allowing it to expand faster than the low-double-digit expectations in its combined secure web gateway and VPN/ZTNA segments. I believe it could continue to take share from legacy web-security providers such as Broadcom and Cisco as corporations look to move to cloud offerings from appliance-based products.

{kind=link}

Gross-Margins Expansion To Be Limited

Though Zscaler's use of its own data centers for deploying generative AI models on its own data and deploying software lets the company add new features and potentially expand into other areas of security, it will likely limit any improvement in gross margin over the near to medium term. Its approach is in contrast with other cloud-security peers, such as Okta and CrowdStrike Holdings, Inc. ( CRWD ), which deploy their services on a hyperscale cloud like Amazon AWS, Microsoft Azure or Google Cloud. I believe data-center investments and multicloud support could help Zscaler's positioning against traditional network-security providers as the company looks to expand product suites and boost capacity to support enterprise deployments, though I believe margin could improve in the long term with scale and customer expansion. Moreover, a boost in Zscaler's order sizes amid tailwinds for remote work could help lower the company's sales and marketing expenses, which historically have been about 45-50% of sales.

{kind=link}

Valuation

I have a strong conviction in ZS's strategic positioning and growth potential. I believe Zscaler can play the critical role of connecting users directly to applications while also facilitating application-to-application connectivity as apps simply become points in the cloud. The company's operating margin expanded by 580bps in the last quarter, and I believe that a rise in referral business from partners may reduce ZS's sales and marketing intensity, further boosting near-term operating margin. New products such as ZPA continue to aid Zscaler's upselling and retention at existing customers, while the company's pivot to workload security from a seat-based model has improved its positioning vs. other security providers.

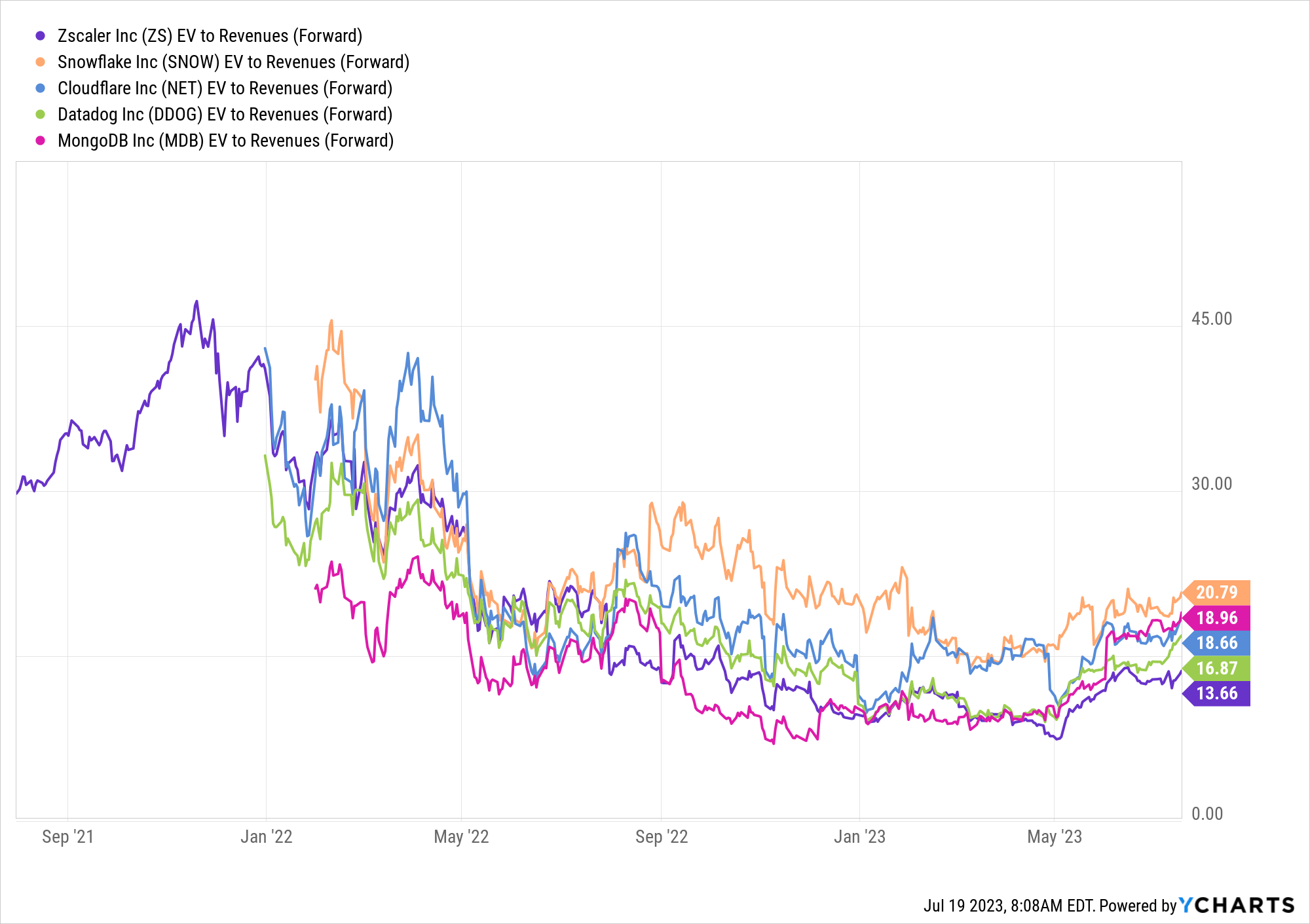

I believe Zscaler is driving the future of security to a Cloud Direct model, and should be able to beat and raise consistently over the next several years. Zscaler currently trades at a discount to Hyper-Growth SaaS Names like Datadog, Inc. ( DDOG ), MongoDB, Inc. ( MDB ), and Snowflake Inc. ( SNOW ), and I expect the valuation gap to close as the company continues to post strong results.

During the past eight years, ZS has traded at a median EV/Sales multiple of 24x , however, the stock's EV/Sales multiple has shrunk from a peak of 47x in 2021 to 13.6x currently. The multiple shrinkage is not unique to ZS as valuations of most growth stocks across the board have suffered in a rising rate environment. However, the stock has performed well in 2023 and I expect the multiple to continue to creep up to trade in-line with other high-growth SaaS peers. ZS currently trades at EV/Sales multiples of 13.6x to the CY23 estimate. My $194 price target is based on a EV/Sales multiple of 13.5x applied to the CY24 revenue estimate of $2.05 billion. During the last quarter, ZS exceeded the original guidance across metrics by wide margin, despite facing the same macro headwinds and longer sales cycles that all other vendors are seeing. I believe if the company continues to post strong results with outperformance in billings growth/better margins, the multiple can re-rate significantly higher than my forward estimate of 13.5x.

{kind=link}

Risks

Zscaler is currently in the early stages of profitability and has not yet achieved its long-term target for operating margin. Therefore, the valuation of the company is based on its enterprise value-to-sales ratio. While Zscaler is growing faster than many other security companies, it will require several years of growth, operational efficiency, and careful cash management to justify its current valuation. If Zscaler's growth slows down or fails to continue to improve its operating margins, the valuation could take a significant hit which poses a risk to investing in ZS at this stage. Moreover, ZS needs to achieve substantial growth in order to benefit from economies of scale in its operations. The market for Zscaler's cloud platform is rapidly changing, and the adoption of cloud solutions, especially cloud security, is not yet widespread. To drive growth, Zscaler plans to invest resources in increasing its operating expenses.

Conclusion

Zscaler is in a favorable position to take advantage of the ongoing trend towards cloud-based security solutions, as businesses are replacing their outdated VPN and data-center firewalls with Zscaler's offerings. I believe that the continuous migration of workloads to the cloud, along with Zscaler's expansion of its product suite, strengthens its competitive position. I view the stock as a buy and have an end-of-year price target of $194 on the stock.

For further details see:

Zscaler: Positioned For Success In The Evolving Cloud Security Market