ZUO - Zuora: Confidently Buy The Dip At 2x Revenue (Rating Upgrade)

2023-08-24 16:46:41 ET

Summary

- Zuora stock presents a buying opportunity after a significant pullback, with strong growth potential and a unique product catering to fellow subscription companies.

- Operating margins and cash flow are also expanding sharply.

- Especially with positive pro forma operating income and a low valuation, Zuora could be an acquisition target.

- The stock trades at just ~2x consensus revenue estimates for next year.

It's a tough time to be an equity investor right now. The key story is interest rates: it's difficult to see valuations expanding much further when short-term treasury bills are yielding 5%, risk free. The core strategy investors should deploy is to rotate more allocation toward high-yielding cash: but on the equity side, favor "growth at a reasonable price" stocks that won't be subject to sharp downside if rates remain persistently high.

Zuora ( ZUO ) is one stock I've constantly championed in this regard, and I think there is a tremendous buying opportunity here after a massive pullback since the start of the month. Zuora is still up more than 30% year to date, but the lion's share of gains this year were wiped out in the month of August, despite reasonably strong Q2 results.

Given the sharp decline in the share price over the past few months, alongside the company's ability to maintain double-digit growth rates, I'm leaning in on my Zuora position. Previously bullish on the stock with a $14 price target, I am retaining my price target and upgrading the stock to very bullish , as my confidence in Zuora hitting the mid-teens is unchanged coupled with a lower-risk entry price.

For investors who are newer to Zuora: the company is an enterprise software solution designed to help fellow subscription businesses manage their recurring revenue. The company has over 1,000 customers and counts some of the most recognizable brands among its customer base, including Zoom ( ZM ), Nutanix ( NTNX ), as well as several media brands like The Atlantic and The Seattle Times.

My long-term bull case and upside catalysts for Zuora include the following:

- Subscription-based business models are becoming dominant. Given the fact that more and more businesses are adopting this type of model, Zuora's base of potential customers has widened significantly. Zuora's uniqueness in this regard is also important to point out: companies can choose a regular ERP, but Zuora's subscription-focused solutions help to address common pain points.

- Even newer industries are adopting subscriptions. News broke that Pret-A-Manger, the fast-casual coffee-and-snack chain, is bringing its widely popular UK subscription model to the U.S. for the first time. Rideshare companies like Uber ( UBER ) have also rolled out premium membership programs. As subscriptions become mainstream, Zuora's opportunity set grows.

- Net retention rates above 100% as Zuora grows along with its customers. As Zuora's clients grow their subscriber bases, so does Zuora's opportunity to monetize and grow alongside its customers. The company has noted that upsells have hit a "record pace", and highlighted several key milestones like GoPro's subscription-based storage and insurance program (a key feature of the company's planned turnaround) hitting one million subscribers.

- Ripe for a takeover, especially at low valuations. While I never like to base any investment decision based on high hopes that the company will get acquired, Zuora checks off a lot of boxes for being acquired: it's small with just a ~$1.2 billion market cap; it offers a very unique product that many larger software companies may want to get their hands on, especially during times when organic growth is fading; and it has positive pro forma operating margins.

From a valuation perspective, at current share prices just under $9, Zuora trades at a market cap of $1.21 billion. After netting off the $406.8 million of cash and investments on the company's most recent balance sheet against $214.4 million of debt, the company's resulting enterprise value is $1.02 billion.

For FY25 (the fiscal year for Zuora ending in January 2025), Wall Street analysts have a consensus revenue target of $489.4 million for the company, representing 12% y/y growth (data from Yahoo Finance ). This puts Zuora's valuation at just 2.1x EV/FY25 revenue, which I'd consider to be a very de-risked entry point in this stock. My $14 price target still represents a modest 3.5x EV/FY25 revenue multiple: and though I'm not certain the company can hit that threshold by year-end 2023, consistent quarterly performance should help Zuora inch up to that level by early/mid 2024.

The bottom line here: I'd apply the oft-quoted market adage here of buying while the rest of the market is fearful. We'll discuss Zuora's latest earnings in the next section, but my overall take is that the company is sliding despite solid results - creating a great buying window.

Q2 download

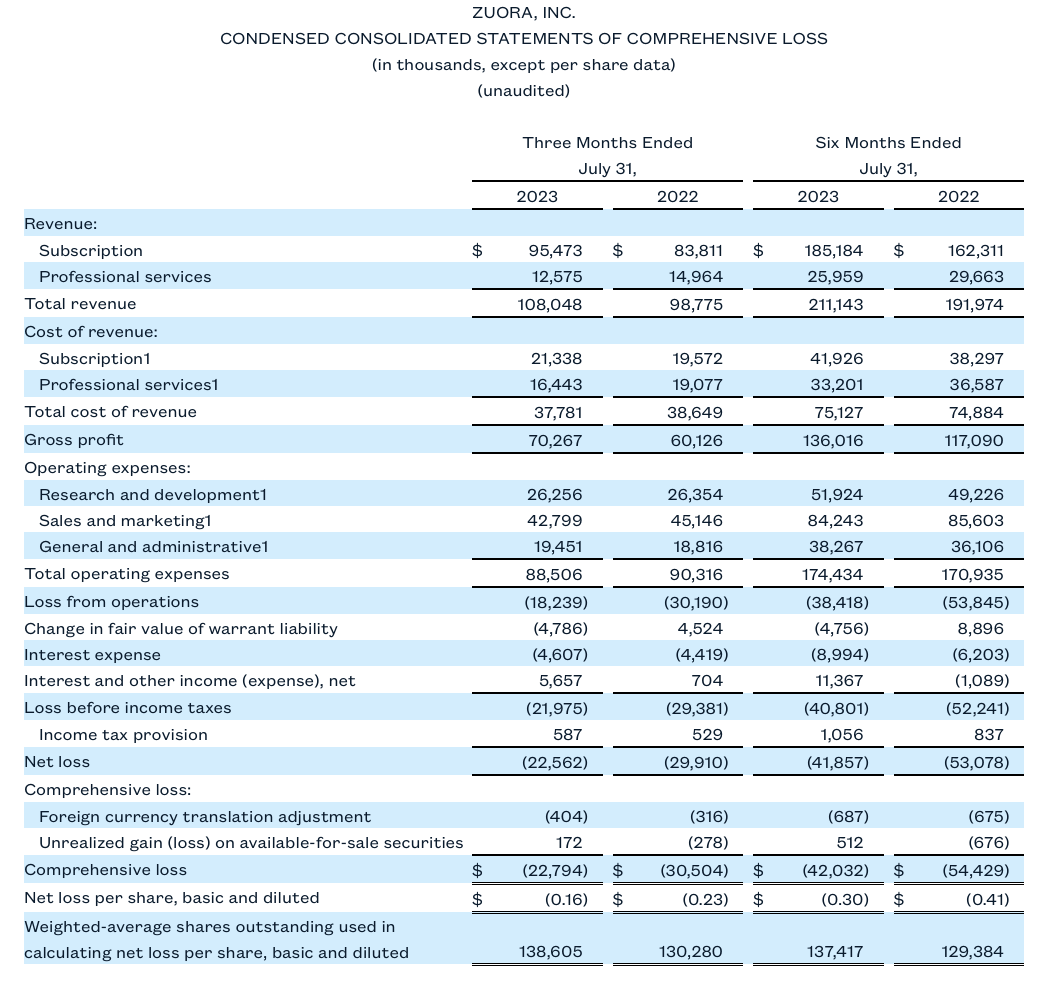

Let's now go through Zuora's Q2 results, released in mid-August, in greater detail. The Q2 earnings summary is shown below:

{kind=link}

Zuora Q2 results (Zuora Q2 earnings release)

Zuora's total revenue grew 9% y/y to $108.0 million, essentially in-line with Wall Street's expectations of $108.8 million. We note, however, two encouraging facts: first, FX continues to be a sharp headwind for Zuora. On a constant-currency basis, Zuora's revenue would have grown 11% y/y. Second, the drag to revenue was on professional services, which is a positive for Zuora as services are performed below cost. Underlying subscription revenue, meanwhile, grew 14% y/y - in line with Q1's growth rate.

Note as well that Zuora raised the lower end of its full-year subscription guidance for the year by $3 million (roughly one point of y/y growth), while simultaneously lowering services revenue expectations by $6 million, which is a favorable mix shift from a margin perspective. The midpoint of the company's pro forma operating income guidance for FY24 is now $35 million, up 13% from a prior view of $31 million.

From a sales execution perspective, cognizant of the difficult landscape particularly among larger enterprises, Zuora has found success in pivoting its sales team to closing smaller deals with a faster path through the pipeline. Per CEO Tien Tzuo's remarks on the Q2 earnings call:

But the adjustments we made to focus on smaller, faster lands continues to pay dividends. We continue to demonstrate the durability of our enterprise segment. And finally, our innovation train continues to roll forward and take hold within a customer base that most companies would be envious of.

Let me go through each point with examples of what we saw in Q2. On our last earnings call, we said that buyer behavior has settled into a consistent pattern and this extended into Q2. There continues to be good demand for what we do [...]

On our last earnings call, we talked about how we displayed agility, by adjusting to the macro and we're targeting smaller, faster lands with a single Zuora product versus starting customers with the full suite. And that strategy continued to pay-off this quarter as it did in Q1. This quarter, we closed over 35% more new logos compared to Q2 of last year, and our average sales cycles improved by over 30% year-over-year."

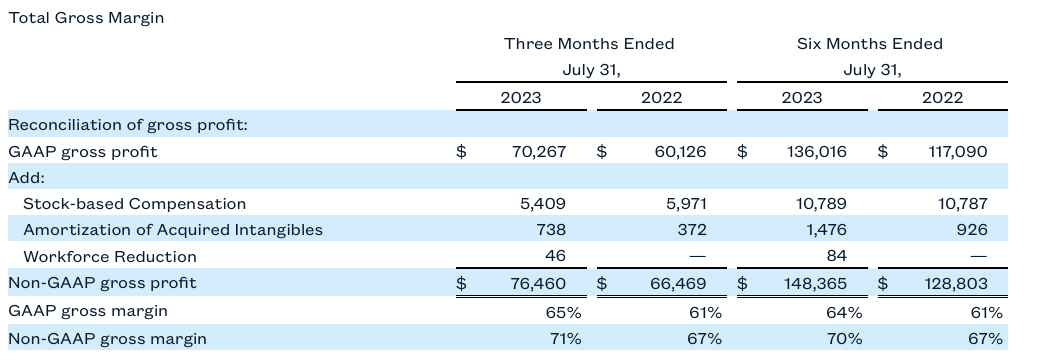

Zuora's pivot toward subscription revenue and away from services, meanwhile, has lifted its gross margin profile to 71% on a pro forma basis, up four points y/y:

{kind=link}

Zuora gross margins (Zuora Q2 earnings release)

Zuora used to have a gross margin deficit versus other SaaS peers thanks to a higher concentration of services revenue, and that was a partial reason behind its undervaluation relative to peers (lower-margin revenue streams should be valued less, of course) - but now, with margins in the 70s, there's no reason for Zuora's ultra-low valuation profile.

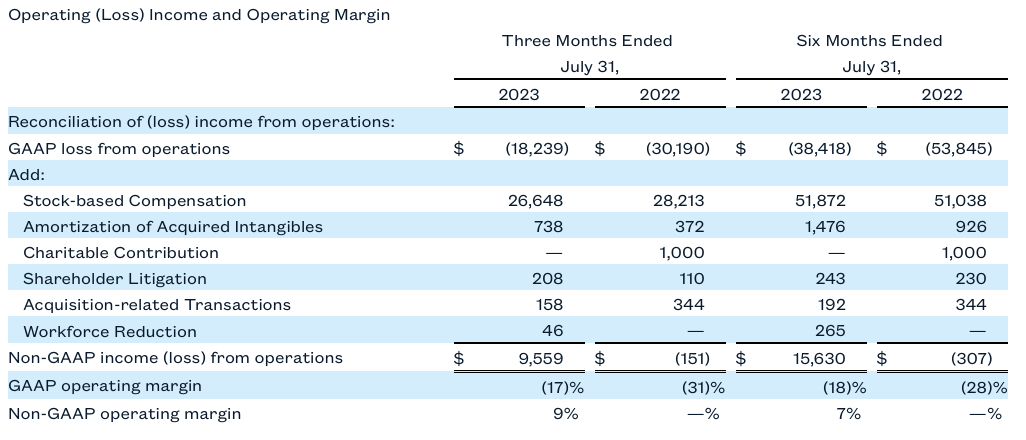

Pro forma operating margins, meanwhile, shot up to 9%, versus flat (slightly below zero) in the year-ago Q2:

{kind=link}

Zuora operating margins (Zuora Q2 earnings release)

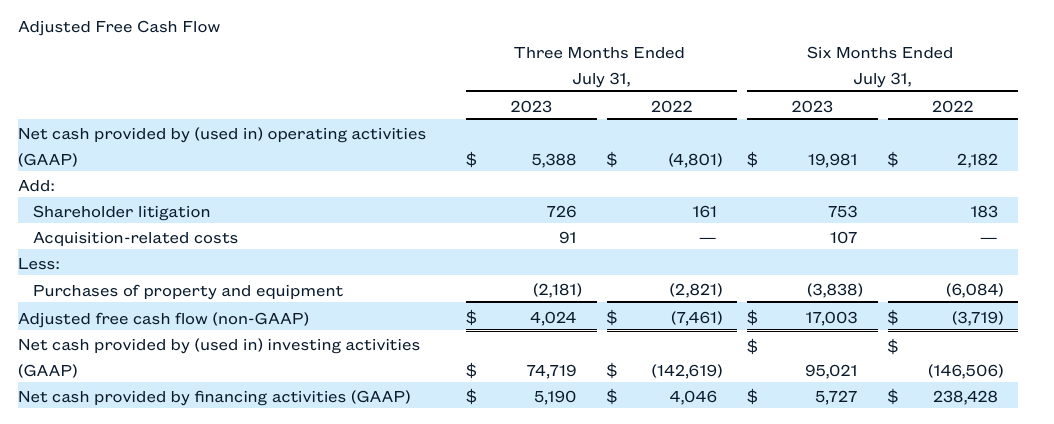

And from a free cash flow basis, year to date the company has delivered $17.0 million of FCF, or an 8.1% margin - versus a cash burn of -$3.7 million, or ten points worse on margin at -1.9%, in the year-ago period.

{kind=link}

Zuora cash flow (Zuora Q2 earnings release)

Key takeaways

Consistent sales execution and mid-teens subscription revenue growth; sharp operating margin gains, and an ultra-low valuation: these are all compelling reasons to buy into Zuora now after a sharp dip over the past few months. Stay long here and wait patiently for the rebound.

For further details see:

Zuora: Confidently Buy The Dip At 2x Revenue (Rating Upgrade)