ZUO - Zuora: Great Buy With Strong Trends

2023-12-16 09:54:23 ET

Summary

- Zuora, a subscription-software company, has the potential for appreciation in the stock market due to accelerating trends and strong Q3 results.

- The company's unique subscription-focused solutions address common pain points for businesses adopting subscription-based models.

- Zuora's low valuation, recovering growth rates, and improving margins make it an attractive investment option for 2024.

The stock market is rallying on the expectation of lower interest rates next year, but that doesn’t mean it’s still not a great time to invest in “growth at a reasonable price” stocks. In fact, as valuations flex up in response to lower rates, I think these are the stocks that have the most room to appreciate next year.

Zuora ( ZUO ) is a stock that bears close examination on this front. The subscription-software company, which provides revenue and billing management systems for other subscription businesses, has struggled to find direction for years. It’s been part of the tech rally this year, up nearly 40% year to date - but coming off a very depressed base in 2022. I think there’s a lot going for Zuora this year, especially as the company is enjoying accelerating trends.

A great bull case for Zuora at an excellent price

I last wrote a bullish note on Zuora in August, when the stock was trading closer to ~$8.50 per share. Since then, the stock market has rallied tremendously - while Zuora has barely budged. At the same time, the company has issued incredibly strong Q3 results that featured both a re-acceleration in growth rates to the mid-teens, while also showing significant margin expansion. That, in my view, forms a perfect buying formula - when we're able to catch Zuora on a fundamental upswing, before the stock has had a chance to react.

As a refresher to investors who are newer to this stock, here is my long-term bull case on Zuora:

- Subscription-based business models are becoming dominant. Given the fact that more and more businesses are adopting this type of model, Zuora's base of potential customers has widened significantly. Zuora's uniqueness in this regard is also important to point out: companies can choose a regular ERP, but Zuora's subscription-focused solutions help to address common pain points.

- Net retention rates above 100% as Zuora grows along with its customers. As Zuora's clients grow their subscriber bases, so does Zuora's opportunity to monetize and grow alongside its customers. The company has noted that upsells have hit a "record pace", and highlighted several key milestones like GoPro's subscription-based storage and insurance program (a key feature of the company's planned turnaround) hitting one million subscribers.

- Gross margin leverage. A better subscription versus professional services revenue mix has helped Zuora lift its gross margin profile to life-to-date highs, reversing a common concern investors had with this stock at the time of its IPO.

- Ripe for a takeover, especially at low valuations. While I never like to base any investment decision based on high hopes that the company will get acquired, Zuora checks off a lot of boxes for being acquired: it's small with just a ~$1.3 billion market cap; it offers a very unique product that many larger software companies may want to get their hands on, especially during times when organic growth is fading; and it has positive pro forma operating margins.

In spite of these strengths, and the fact that recent quarterly results demonstrate further upside, Zuora remains quite cheap. At current share prices just under $9, Zuora trades at a market cap of $1.29 billion. After we net off the $493.7 million of cash and $356.6 million of debt on Zuora's most recent balance sheet, the company's resulting enterprise value is $1.15 billion.

Meanwhile, for next fiscal year FY25 (the year for Zuora ending in January 2025), Wall Street analysts are expecting Zuora to generate $475.0 million in revenue, representing 10% y/y growth. This puts Zuora's valuation multiple at just 2.4x EV/FY25 revenue.

I'm still holding firm to my very bullish position on Zuora and a $14 price target for mid-year 2024 (representing a 3.5x multiple on 2024 revenue). Stay long here and wait for the market to re-value Zuora shares.

Q3 download

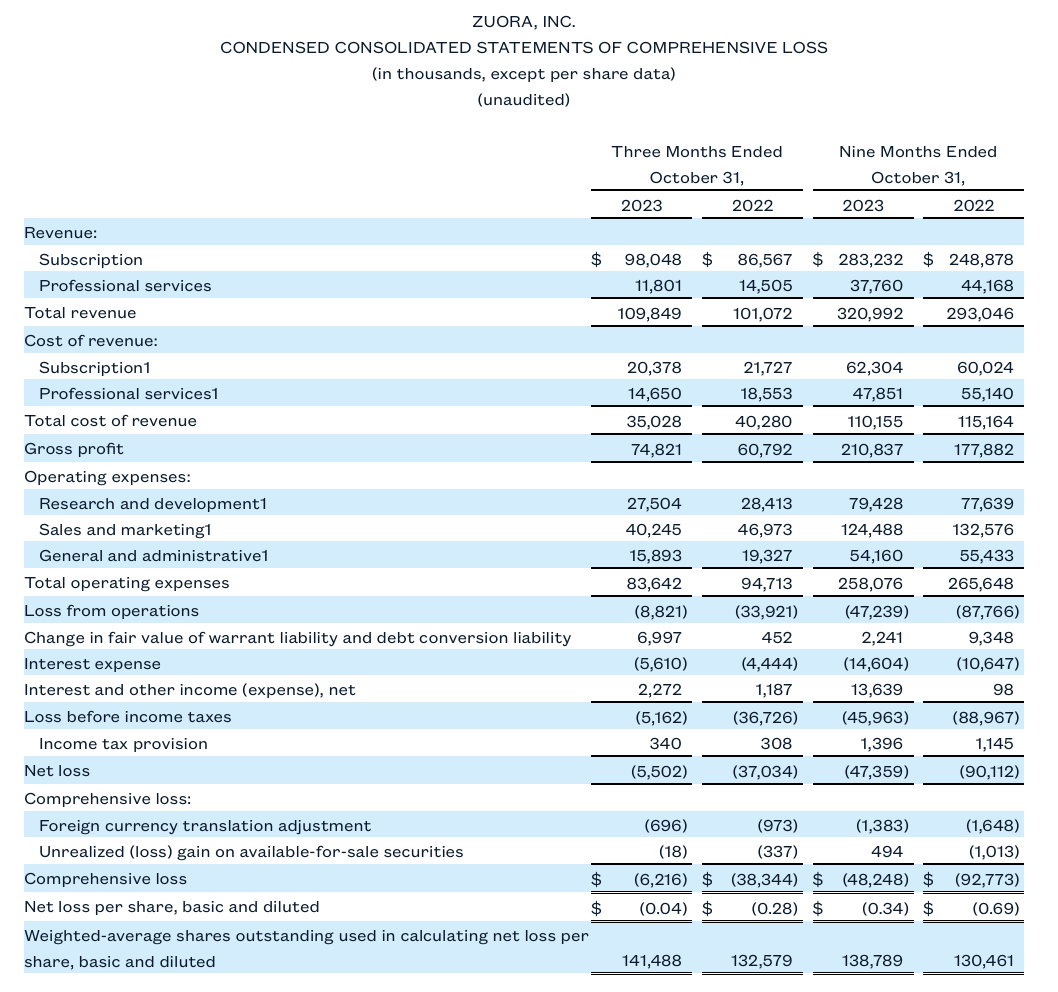

Let's now go through Zuora's latest quarterly results in greater detail. The Q3 earnings summary is shown below:

{kind=link}

Zuora's revenue grew 9% y/y to $109.8 million, ahead of Wall Street's expectations of $108.7 million (+8% y/y). Meanwhile, on a constant-currency basis, Zuora's subscription revenue grew 14% y/y - marking several quarters of a return to mid-teens subscription growth after several years of lag. Zuora's ARR also grew at a strong 13% y/y pace to $396.0 million - and we note that its existing ARR base already covers 83% of Wall Street's $475 million revenue target for next year (and note that the company typically has a 10-11% mix accruing to professional services).

And, in spite of pressure on seat counts and constrained IT budgets in this environment, Zuora continued to notch a net upsell, with net revenue retention rates of 108% in the quarter. The company also signed a number of notable new customers in the quarter, including and especially LinkedIn, now a division of Microsoft ( MSFT ).

Here are some helpful remarks from CEO Tien Tzuo's remarks on the Q3 earnings call , detailing the company's top-line performance:

We've done this while building a durable business that delivers a double-digit growth even in this macro-environment where budgets are scrutinized and deal cycles are taking longer. I would say there are two things that have allowed us to accomplish this. Our enterprise customers and our mission-critical technology.

As you know, we chose to focus on the world's largest and fastest-growing companies across industries and all around the world. This gives us a customer base that many would be envious of. And in Q3, many of these companies are recommitted to Zuora. We saw several expansions with multi-year commitments that drove a 20% year-over-year increase in our total RPO or Remaining Performance Obligations. This also helped drive our dollar-based retention rate to 108% in Q3, up one point quarter-over-quarter.

Let me give you some examples. In Q3, we expanded our work with Google, Google Fiber, Alphabet's high-speed broadband Internet service that spans 15 states and counting. Now Zuora will power GFiber's full order-to-revenue process as they continue to grow. Or, you all know we power 12 of the top 15 automobile companies around the world.

Well, in Q3, one of them, which is also one of our top five customers, renewed their commitment to Zuora for another five years. Not only that, in one of the world's largest telecommunications and entertainment companies, we expanded to yet another business unit, signing a five-year, seven-digit deal, which also was a competitive replacement."

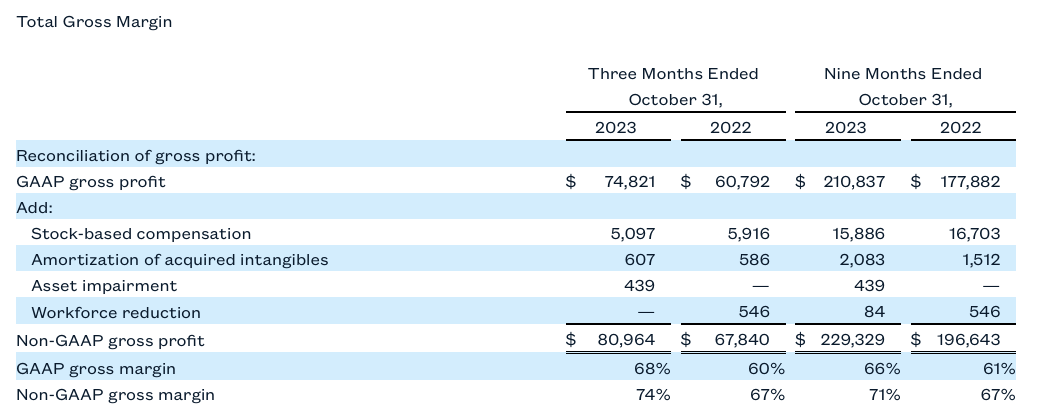

Top-line strength also flowed nicely through to the bottom line. Zuora's pro forma gross margins hit 74% in the quarter, a seven-point bump from the year-ago Q3 - which is largely a function of better subscription revenue mix versus the prior year, as the company's unprofitable professional services revenue stream is winding down.

{kind=link}

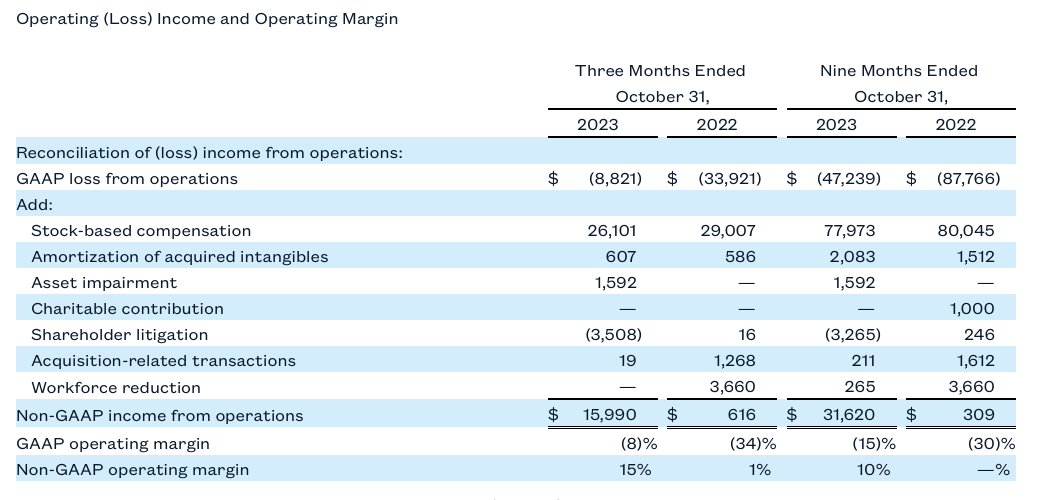

Pro forma operating margins, meanwhile, soared 14 points y/y to 15%, which was also a nine-point sequential improvement versus Q2:

{kind=link}

The company has also delivered $30 million in free cash flow in the three year-to-date quarters (at a 9% margin), versus an -$11 million loss in the prior year-period. It's targeting $37 million in FCF for the year, which is a $65 million improvement versus FY22.

Key takeaways

With a low valuation, recovering growth rates, and rapidly ramping margins, there's a lot to like about Zuora as we head into 2024 - especially at its low valuation multiple. Stay long here and wait on the rebound.

For further details see:

Zuora: Great Buy With Strong Trends