ZUO - Zuora: Richly Priced At 31x FCF Even Though It Carries A Lot Of Cash

2023-10-06 07:30:18 ET

Summary

- Zuora's valuation, currently at 30x next year's free cash flow, appears relatively high for a business experiencing single-digit revenue growth rates.

- The rich price tag of Zuora's stock raises concerns about its investment value, particularly when compared to its growth potential.

- The company's strong balance sheet, boasting over $180 million of net cash, offsets the uncertainty surrounding its valuation.

Investment Thesis

Zuora ( ZUO ) specializes in providing cloud-based subscription management solutions for businesses. They offer tools and platforms to help companies operate and scale subscription-based business models efficiently.

There's a lot to like about its business model plus its very strong balance sheet . However, I believe that having to pay 30x next year's free cash flow is a rich price tag for this business.

Zuora's Near-Term Prospects

Zuora is a cloud-based subscription management platform designed to assist companies in monetizing new services and operating recurring revenue business models efficiently.

This platform enables businesses across various industries to launch, manage, and scale subscription-based operations, automating essential processes such as quoting, billing, collections, and revenue recognition.

With Zuora, companies can adapt pricing and packaging, comply with revenue recognition standards, analyze customer data for optimization, and establish meaningful relationships with subscribers. It addresses the limitations of traditional transaction-based software, making it valuable for businesses with ongoing customer relationships and recurring revenue models. Zuora's has a suite of products including Zuora Platform and Zuora Billing, that offer features like automated processes and data-driven decision-making. Many companies across various industries, including Fortune 100 firms and top auto manufacturers, use Zuora to thrive in the Subscription Economy.

This is the bull case, Zuora has positioned itself to leverage the increasing adoption of recurring revenue models in the business landscape.

That being said, Zuora also acknowledges that it has encountered growing scrutiny in deal-making processes, reflecting the evolving landscape of technology spending and customer decision-making. This increased scrutiny stems from a heightened emphasis on cost control and ROI evaluation within customer organizations.

To adapt to this environment, Zuora is pursuing smaller, swifter deals. The company's proficiency in offering distinct technology solutions, which cater to diverse industries such as 5G network providers like DISH Wireless ( DISH ) and prominent media publishers like The Atlantic, underscores its adaptability and relevance within the market. Furthermore, Zuora's recent product innovations, including Zuora for consumption capabilities and Zuora Command Center, hold some potential to fuel future growth.

Customer examples serve as compelling evidence of Zuora's pivotal role in enabling businesses to flourish via recurring revenue models.

To this point, here's a quote from the earnings call describing its customer success with DISH,

The DISH Wireless, a subsidiary of DISH Network and a 5G network provider that reaches more than 240 million Americans. They purchased Zuora Revenue in Q2. Zuora has the unparalleled functionality DISH needs to automate their revenue recognition as they grow their subscriber base.

One aspect of Zuora's business model that I like is that they position themselves to win alongside their customers. For instance, DISH Wireless's selection of Zuora Revenue for automating revenue recognition underscores the functionality and capabilities that Zuora brings to the table, essential for supporting the expansion of its subscriber base.

Given this context, let's now discuss Zuora's financials.

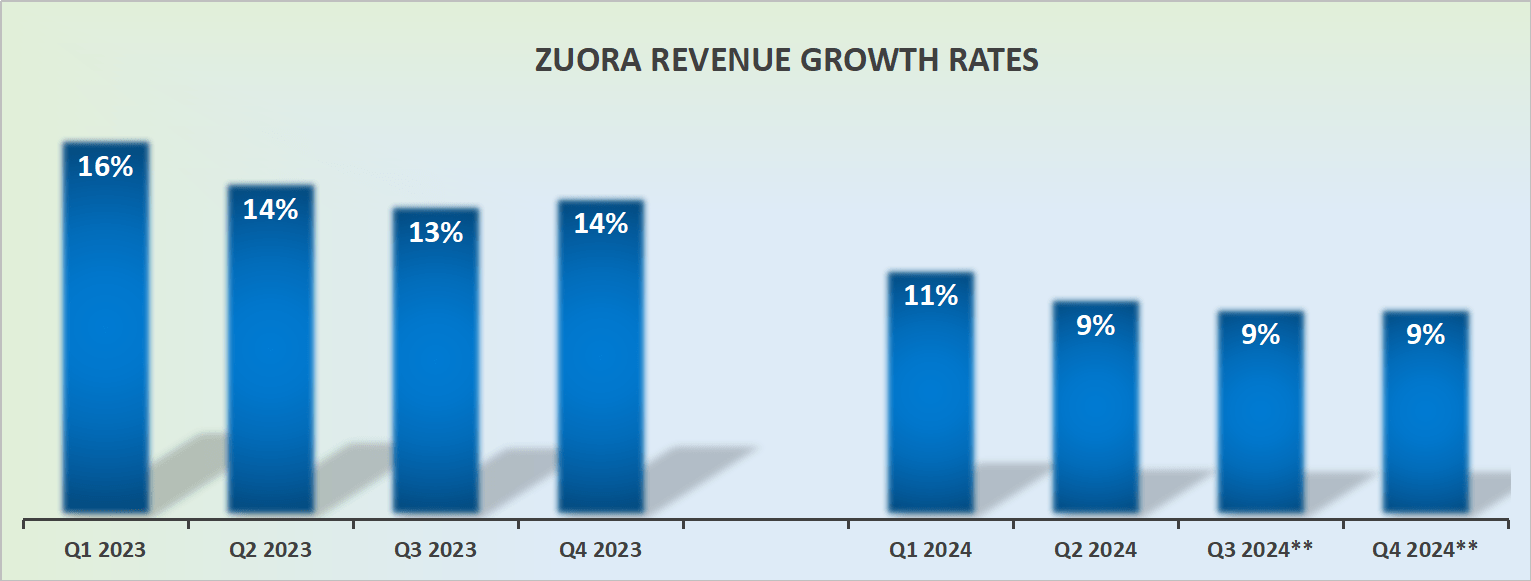

Revenue Growth Rates Drop to Single Digits

{kind=link}

Up until fiscal Q1 2024 (the previous quarter), investors would have still had some hopes that Zuora could deliver a 10% CAGR in the near term. But after Zuora provided its updated guidance for fiscal 2024 and took out the high end of its guidance, investors were forced to come to terms that Zuora would no longer be delivering solid double-digit growth rates.

Consequently, investors are now left with a business that's still able to eke out some growth, but hardly enough to get anyone particularly excited about Zuora's prospects.

Accordingly, as we look out to fiscal 2025, I believe that with a somewhat weak economic outlook, this aspect largely cements the fact that the days when this business could be counted on for high double-digit growth rates are now in the rearview mirror.

Naturally, this will impact the sort of valuation that investors will be willing to pay for Zuora.

ZUO Stock Valuation -- Priced at 31x Forward Free Cash Flow

Let's assume that Zuora's free cash flow reaches $30 million this fiscal year. And then, let's assume that as Zuora's growth rates start to slow down next year, its eagerness to aggressively invest in its operations will be curtailed.

Consequently, this implies that although its top line is growing at single digits, this sees Zuora's free cash flow grow by 15% y/y into fiscal 2025 (next year) leading Zuora's free cash flow to reach $35 million.

This leaves Zuora priced at 31x next year's free cash flows. Does anyone truly think that paying 31x next year's free cash flow for a business that's growing single digits makes sense?

With that sort of multiple, investors might as well pay for the biggest and best of the blue chips. After all, they too are able to grow in the high-single digits to low double digits.

The main difference is that those blue chips have substantial market share and dominance. In comparison, Zuora operates in a highly competitive environment against Chargee and Recurly on one side and Salesforce ( CRM ) on the other, as well as SAP ( SAP ) and others.

To be clear, it's not that I believe the stock is overpriced. It's not. In fact, Zuora's balance sheet is very strong with more than $180 million of net cash. The point I'm making here is that this stock is richly valued for what's on offer.

The Bottom Line

As I analyze Zuora's current situation, there appears to be much to appreciate about its business model and robust financial standing.

However, I can't help but feel uncertain about the hefty price tag of 30x next year's free cash flow, which raises doubts about the investment's value.

Zuora's strengths lie in its cloud-based subscription management platform, catering to a wide range of industries and enabling businesses to navigate the subscription-based landscape effectively.

Still, challenges loom as it grapples with heightened scrutiny in deal-making processes, reflective of changing technology spending dynamics and customer evaluation criteria focused on cost control and ROI. The company's pivot towards smaller, faster deals and innovative products may offer a glimmer of hope, but as revenue growth rates taper off to single digits, it's unclear whether Zuora can recapture its previous high double-digit growth trajectory.

This uncertainty surrounding its valuation and growth prospects keeps me on the sidelines.

For further details see:

Zuora: Richly Priced At 31x FCF, Even Though It Carries A Lot Of Cash