ZUO - Zuora: Valuation To Rerate As Growth Reaccelerates

2023-10-04 06:02:10 ET

Summary

- I expect growth acceleration driven by a sales strategy pivot and the potential for reversion to higher valuation multiples.

- Zuora offers a product that supports subscription and usage-based businesses in managing their order-to-cash cycles, filling a gap in the market.

- ZUO's shift to targeting smaller markets with a single product is expected to help mitigate near-term weaknesses and provide long-term growth opportunities.

Summary

This post is to provide my thoughts on the Zuora ( ZUO ) business and stock. I am recommending a buy rating as I expect growth to accelerate from here, driven by the ZUO pivot in its sales strategy, which allows ZUO to better acquire new customer logos in the current tough macro environment. Historically, ZUO has pretty much traded in line with peers; hence, I believe as growth reaccelerates, valuation multiples should revert back to the same trend.

Business overview

ZUO offers a product that helps subscription and usage-based businesses manage their order-to-cash cycles. ZUO has found a niche because traditional ERP providers have been slow to adopt and support subscription-based business models. The development of ZUO's market is still in its infancy because it is dependent on the maturation of subscription business models.

Investment thesis

The nature of ZUO business is inherently tied to the health of the general business environment, as it is a large-ticket implementation that typically requires major business transformation. As such, growth has been weak over the past 2 quarters, dipping into single-digit percentage growth (in 2Q24, total revenue grew only 9%) vs. mid-teens previously. While gross margins did expand to 70.8% as the revenue mix shifted toward subscriptions (now 88.4% of total 2Q24 revenue), I believe the focus is on growth, as the narrative for ZUO was that the addressable market for businesses demand for offering subscription models is huge. This is true both in the technology sector and outside of it. In the broader enterprise segment, there are new subscription businesses launched in sectors like industrials (Autodesk, Procore, etc.). Within technology, software companies such as ADBE have been transitioning to subscription business models.

As one can imagine, it takes a lot of effort to roll out a subscription model given all the factors that need to be considered (pricing, cash collection, inventory updates, go-to-market strategy, customer-facing website, customer services, etc.). On top of this, a lot of financial resources are needed as well. As such, a lot of businesses are likely to delay such implementation until there is a clearer line of sight for demand recovery (consumers and businesses confidence level) and also a cheaper cost of capital.

In my opinion, ZUO's move to pivot its sales strategy to target smaller markets with a single product versus a platform sale will help cushion near-term weakness as it is relatively easier for customers to adopt one module rather than transform their entire business operations. Not only will this help to grow the business in the near term, but I believe there are long-term benefits from this. The way I view this pivotal strategy is by looking at it as a cheap cost of customer acquisition. If we were to compare the cost of convincing a customer to adopt an entire platform, it is likely going to take months and a lot of resources, although the payoff is worth it. On the other hand, adopting a single module is a lot faster and cheaper, but the payoff is weaker. But note that the latter approach gives ZUO a direct channel to upsell or cross-sell other modules to the customer over time, eventually leading to a platform transition. As ZUO continues to grow its base of logos, it will mean there are more opportunities to grow, providing further visibility into the growth profile of the business.

On our last earnings call, we talked about how we displayed agility by adjusting to the macro through targeting smaller, faster lands with a single Zuora product versus starting customers with a full suite. 2Q234 earnings results call

Notably, this strategy is likely to work better for industries outside of the technology sector, as it is easier to convince. These industries are early adopters of subscription-based business models and are likely to be unaware of the full benefits right from the onset. It takes time for them to learn, adapt, and realize how beneficial ZUO's product offerings are. As such, I am very positive about the management shift to this go-to-market strategy and believe that ZUO should be able to re-accelerate growth when the macro recovers.

During a recent conference where ZUO was present, the management team pointed out that despite facing certain short-term obstacles in the broader economic landscape and the pace at which longer ROI products are adopted, management maintains a positive outlook regarding the long-term prospects. They are particularly optimistic about the enduring impact of structural shifts in business models within the industries they cater to. Long-term, ZUO is a stock I'm bullish on because of its solid fundamental growth driver. There is a growing need for products like ZUO because businesses and consumers are gravitating toward more flexible pricing and collection models, which can strain preexisting ERP systems and their ancillary components.

Valuation

Own calculation

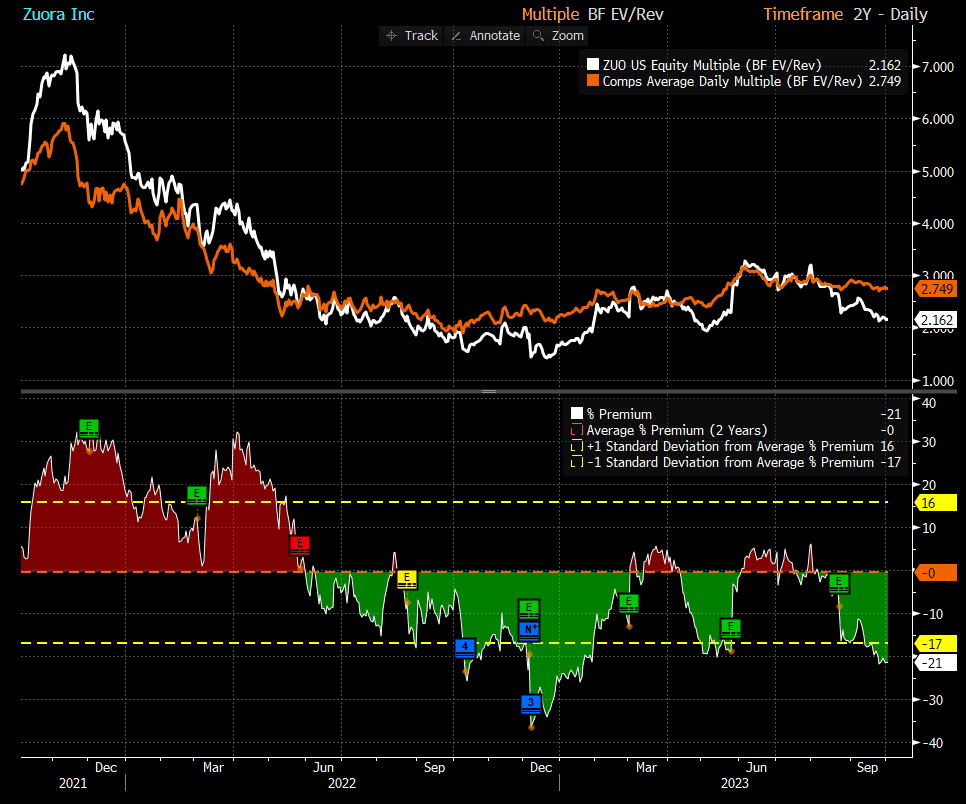

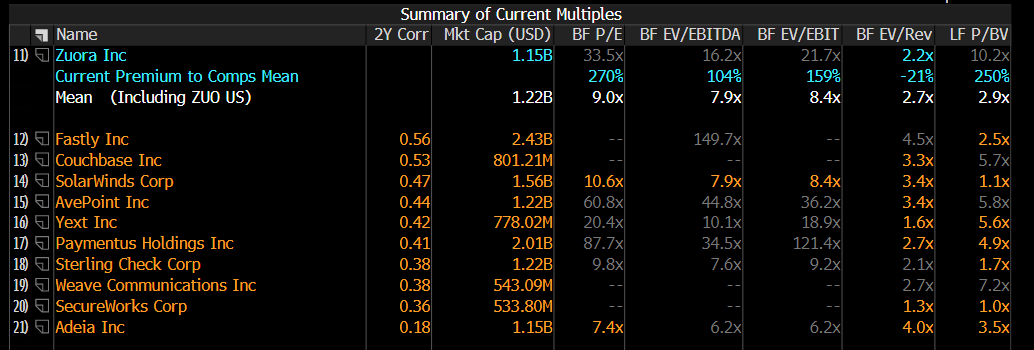

I believe the fair value for ZUO based on my model is $11.61. My model assumptions are that ZUO's growth will accelerate from the 9% growth in FY24 to 12% in FY25 and 15% in FY26, recovering to the previous mid-teens growth profile. With this growth profile, I believe the market will rerate the stocks' valuation upwards back towards other infrastructure software players multiples of ~2.7x forward revenue (refer to screenshot below for peers and their multiples). Over the past 2 years, ZUO has traded pretty much in line with these peers, and I believe it should continue to do so as growth reaccelerates.

{kind=link}

{kind=link}

Risk

The change in go-to-market strategy is certainly positive; however, the fact is that ZUO is still heavily dependent on macro recovery so that its growth can reaccelerate. Further deterioration of the economy will likely cause growth to come down further, which is bad for the business and the stock's narrative.

Conclusion

I recommend a buy rating for ZUO as I anticipate an acceleration in growth, driven by the company's pivot in its sales strategy. This shift allows ZUO to more effectively acquire new customer logos, particularly in the current challenging macroeconomic environment. ZUO's strategy to target smaller markets with a single product rather than a platform sale is expected to cushion near-term weaknesses and serve as a cost-effective means of customer acquisition. This approach not only aids short-term growth but also sets the stage for long-term benefits by opening opportunities for upselling and cross-selling additional modules. Additionally, ZUO's shift in its go-to-market strategy is likely to resonate well with industries outside of the technology sector, which are increasingly adopting subscription-based models.

However, it's essential to acknowledge that ZUO's growth is still reliant on macroeconomic recovery, and any further economic deterioration could impact both the business and the stock's narrative. Nevertheless, the strategic shift and the company's positioning in a changing business landscape make it an intriguing prospect for investors.

For further details see:

Zuora: Valuation To Rerate As Growth Reaccelerates