ET - 10% Yield And Outperformance - Has Energy Transfer Become Unbeatable?

2023-06-20 09:00:00 ET

Summary

- Energy Transfer LP has evolved into a strong income play with a well-covered 10% dividend and plans to hike it by 3-5% annually.

- Energy Transfer has improved its financial position, with decreasing capital investment needs, a healthier balance sheet, and increasing free cash flow.

- Despite past downturns and a complex tax structure as a Master Limited Partnership, ET stock presents an attractive investment opportunity with growth potential and attractive valuation.

Introduction

I'm currently sitting next to a whole stack of energy research, a big part of it consisting of midstream companies. In the past few quarters and years, we have discussed a wide variety of midstream companies. One puzzle piece that was missing was Energy Transfer LP ( ET ) , the star of this article.

While the company has struggled in the past with underperformance and dividend cuts, it has now evolved into a company with subdued CapEx requirements, strong EBITDA growth, a well-covered 10% dividend, and goals to sustainably hike this dividend (above the rate of inflation).

Not only has ET become a fantastic income vehicle in the energy sector, but it has also turned into an outperformer. The company has outperformed the ALPS Alerian MLP ETF ( AMLP ) and all major midstream companies on my watchlist over the past 12 months.

In this article, we'll assess what makes ET such a quality income play.

So, let's get to it!

Not A C-Corp

I need to start this article by explaining that ET is not a traditional C-Corp. The company is a Master Limited Partnership, which are tax-advantaged entities that connect producers of oil and gas to their customers. This includes storing products, shipping byproducts, and everything else with regard to managing the flow of energy products.

Energy Education

According to PIMCO :

Their core midstream oil and gas pipelines typically employ “toll-road-like” fee-based business models to handle, process and transport oil, natural gas, natural gas liquids (NGLs) and refined products from the point of production to distribution. The structure of the MLP business model combined with their critical asset base contributes to the industry’s high barriers to entry, generally predictable revenues and limited direct commodity price exposure, offering a number of potential benefits for investors.

MLPs are structured as pass-through companies, which means they do not pay corporate taxes. These taxes are borne by unitholders (shares are called units). Hence, investors have to deal with K-1 forms, and a wide range of foreign investors may not be able to invest in ET.

So, please keep that in mind and assess how this may impact your tax situation.

What's Energy Transfer?

With a market cap of $40 billion, Dallas-based Energy Transfer is the fourth-largest midstream company in North America.

The company is involved in various activities related to natural gas and related fossil fuels, including natural gas operations, midstream services, and intrastate transportation and storage.

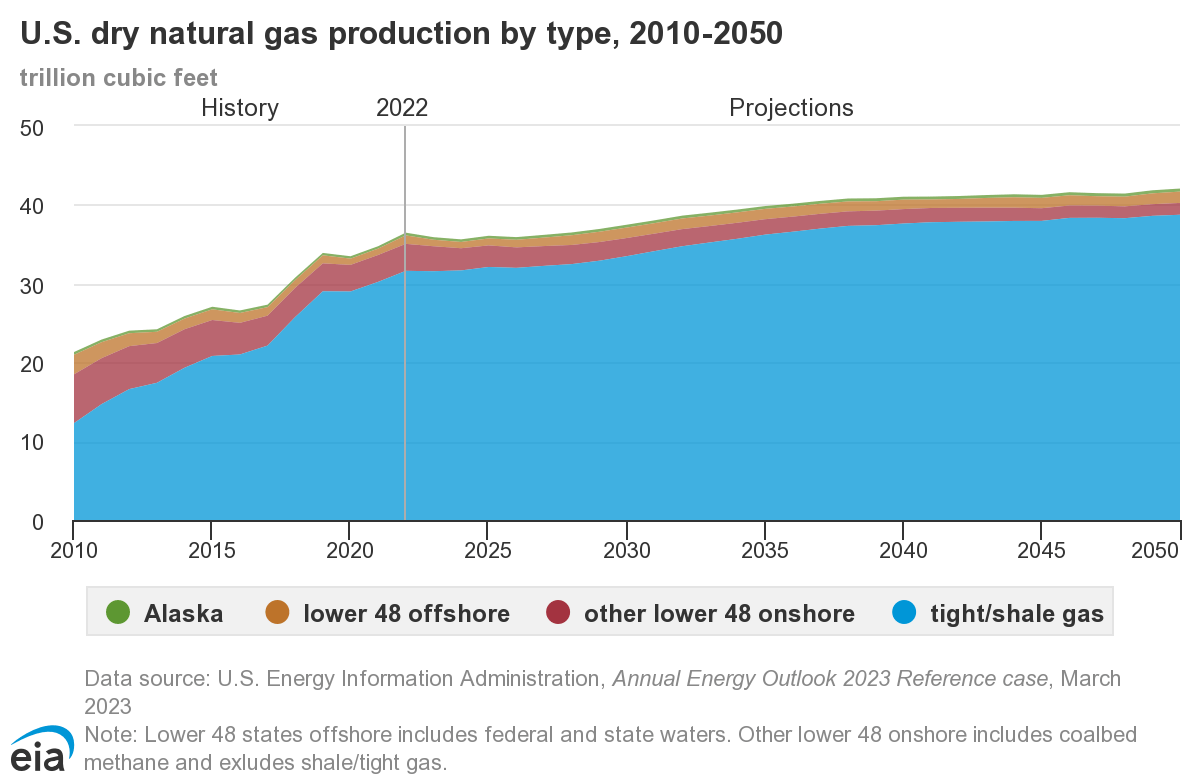

The intrastate transportation and storage segment, as well as the interstate transportation and storage segment, primarily handle the transportation of natural gas, which is the cleanest fossil fuel that is expected to enjoy long-term production growth in the United States. In this case, midstream demand is also fueled by export operations of natural gas and other value-adding operations.

Energy Information Administration

{kind=link}

The company also transports oil and owns 34% of Sunoco LP ( SUN ), a publicly traded LP engaged in the distribution of motor fuels to independent dealers. Sunoco also operates 76 retail stores in Hawaii and New Jersey.

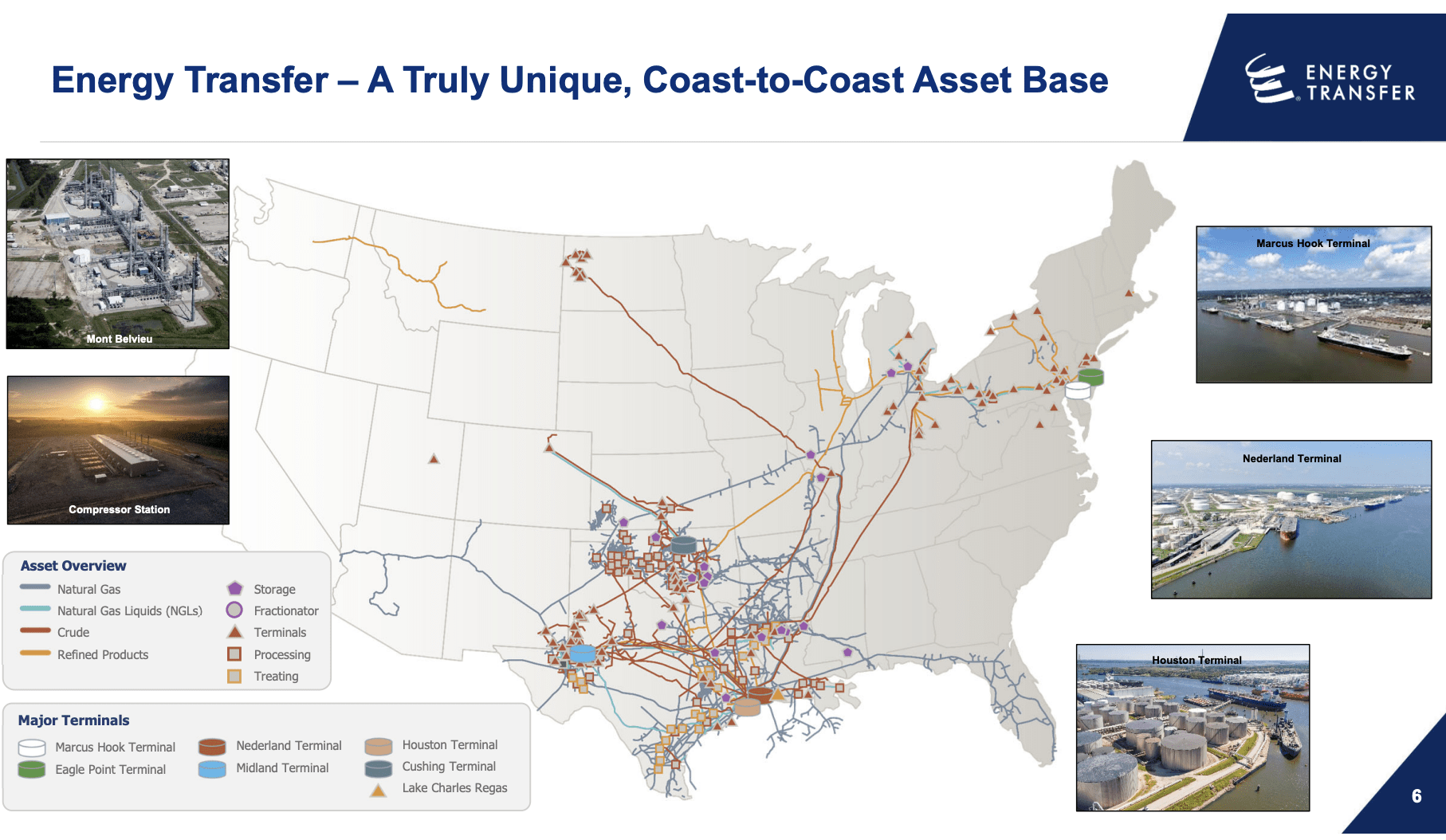

As the map below shows, the company has major operations in the South's biggest basins, the natural gas-rich Northeast, multiple export ports, and the massive Dakota Access Pipeline.

{kind=link}

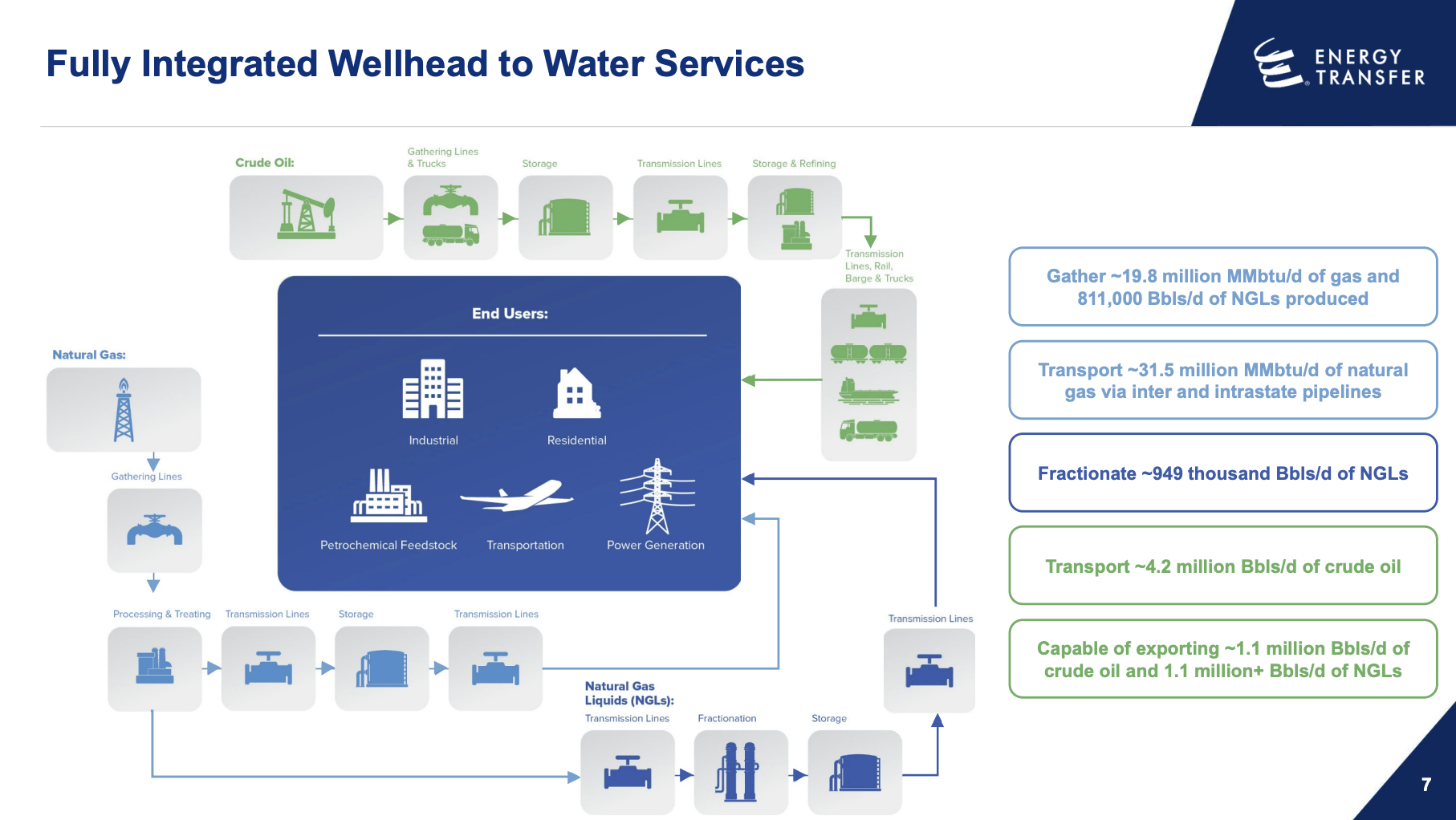

While its market cap is a pretty good indicator of its size, there are a few impressive numbers I want to share with you. For example, the company gathers roughly 20 million MMbtu of gas per day and transports more than 4 million barrels of crude oil per day. It is capable of exporting roughly a quarter of that in its own facilities.

{kind=link}

With that in mind, the company is dependent on fees.

Fee-based contracts involve the payment of fixed fees or tolls for the use of Energy Transfer's infrastructure and services.

These contracts are typically long-term agreements with customers and are generally determined based on factors such as the volume of products transported or stored, the distance traveled, or the duration of service provided.

While the company does have commodity-based contracts, it is far less dependent on commodity prices than its customers. The biggest commodity risks are that prices fall so much that producers reduce output. Or, demand weakness could cause final demand to suffer, which is a bit related to low commodity prices.

Speaking of economic risks, ET shares have been through a number of steep downturns.

Past Downturns (What Caused Them?)

Since the Great Financial Crisis, ET shares (like all of its peers) have been through two major downturns. In 2015, commodity prices crashed due to oversupply and imploding demand. In 2020, supply was also an issue. However, back then, lockdowns caused demand to vanish almost overnight.

Furthermore, it needs to be said that ET was a different company back then.

As one can imagine, building a massive network of pipelines and related infrastructure is expensive - very expensive.

As the chart below shows, the company went into the 2015 downturn with annual CapEx requirements of more than $8 billion. This caused free cash flow to drop to almost negative $8 billion due to low operating cash flows. You can imagine why investors were eager to drop shares back then when commodity prices started to plunge.

This funding gap also resulted in a steep surge in debt. Between 2014 and 2020, net financial debt rose from roughly $20 billion to more than $50 billion. One can imagine why this caused another panic when the pandemic did a number on demand.

As a result, the company had to cut its dividend in 2020, as the chart below displays.

Now, the company is back on track.

- Capital investment needs have come down significantly.

- Net financial debt has peaked.

- The company is in a good spot to use its assets (and strategic M&A) to grow on a long-term basis.

Energy Transfer Is Back On Track

Energy Transfer is a stock that displays a lot of conviction from its management. Not only does it have one of the highest insider ownership rates in the country (>12%), but it is also mainly owned by retail investors, who own roughly 50% of all units.

Since January 2021, insiders and independent board members have bought units worth more than $340 million.

This is no surprise, as ET is back on track.

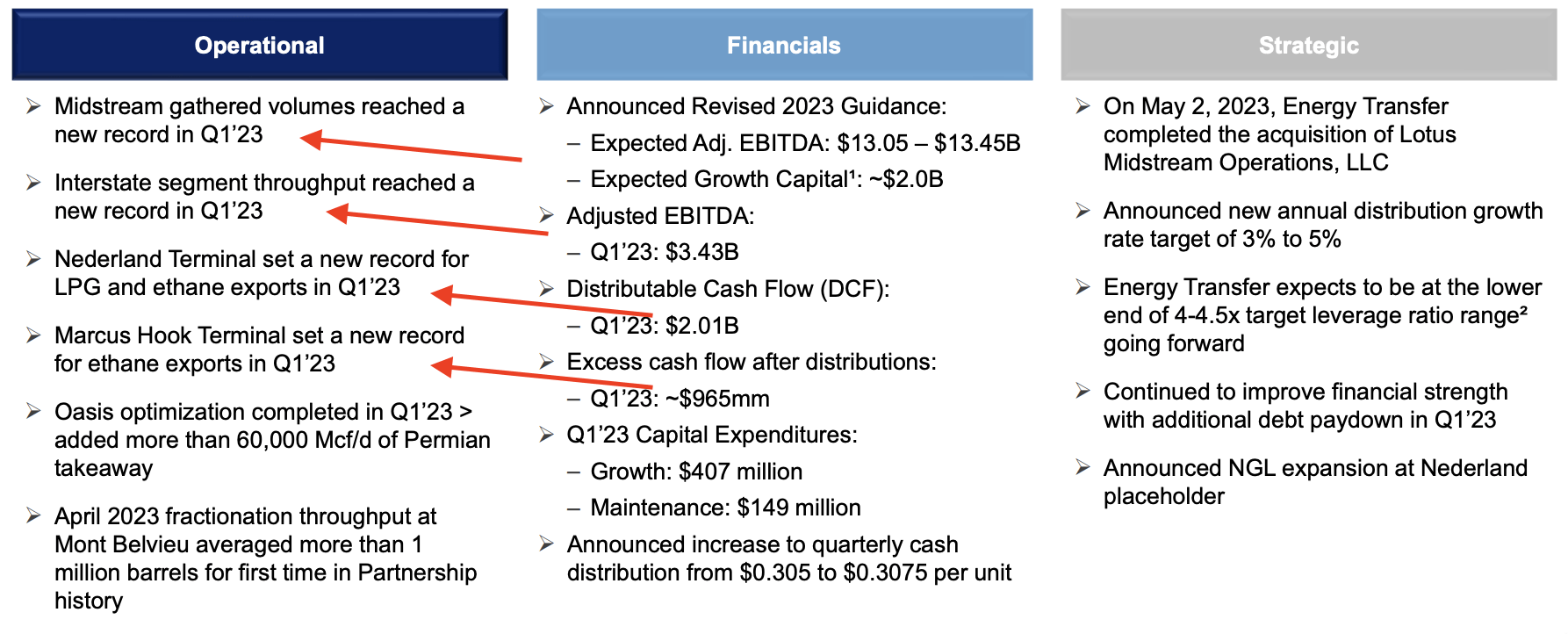

For example, in the overview below, I point at four operational records in its Midstream, Interstate, Nederland Terminal, and Marcus Hook Terminal businesses.

{kind=link}

In the first quarter, the company reported positive financial results, with an adjusted EBITDA of $3.43 billion, representing an increase from $3.34 billion in the prior-year quarter.

The company also reported distributable cash flow ("DCF") attributable to Energy Transfer partners of $2.01 billion, compared to $2.08 billion in the first quarter of 2022.

Essentially, DCF is cash available for dividends.

The excess cash flow after distributions came in at $1.04 billion, which shows that the dividend was fully covered.

In light of these developments, Energy Transfer announced a quarterly cash distribution of $0.3075 per common unit, representing a 0.8% increase compared to the prior hike. The hike prior to that was 15.1% in January of this year.

Going forward, the company expects to continue increasing its common unit distribution on a quarterly basis and targets a 3% to 5% annual distribution growth rate, which is a huge deal for a company that currently yields 9.6%!

The best - and most important - news is that the company is now in a good spot to reward shareholders and execute its plan to hike its dividend by 3% to 5% per year.

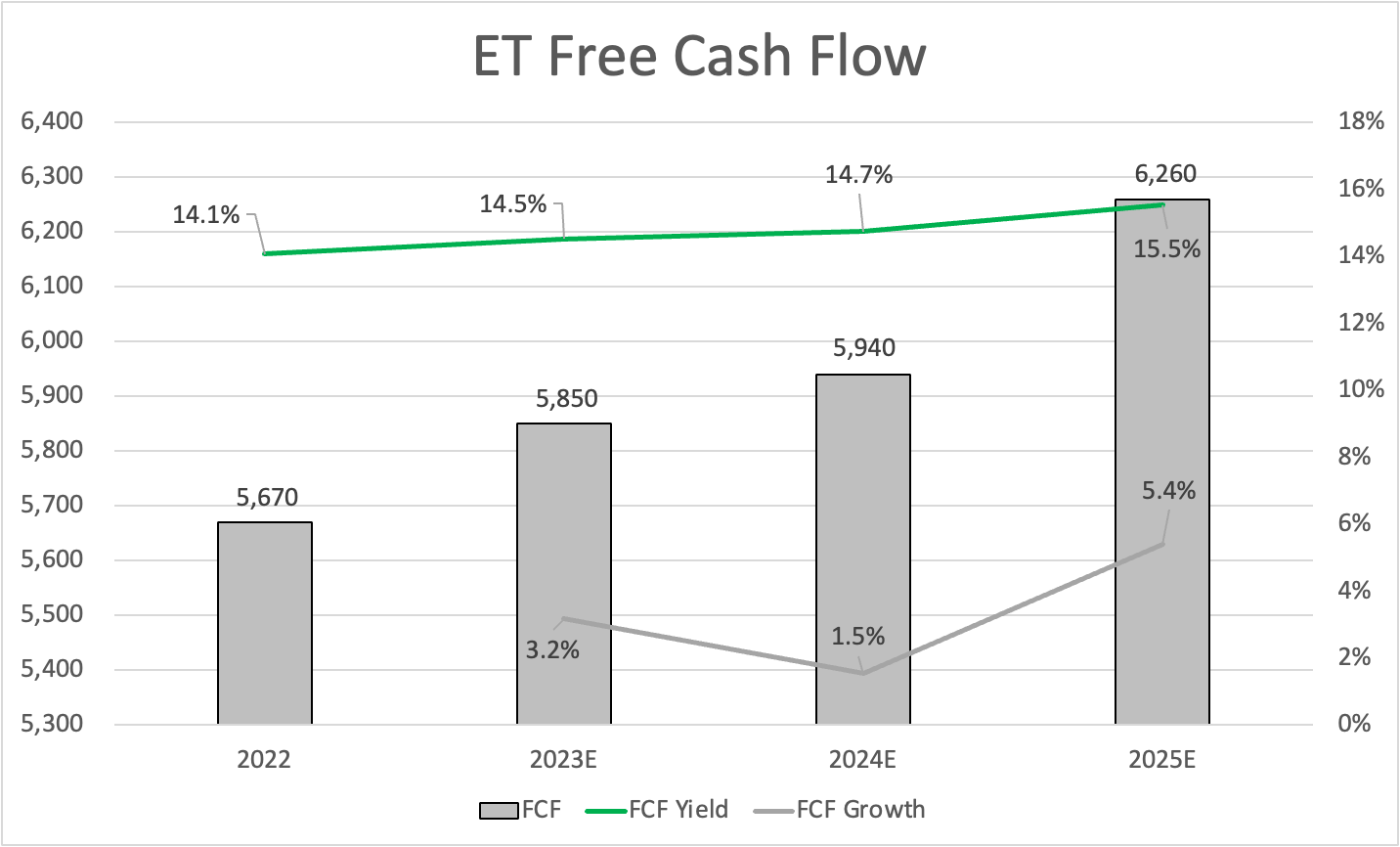

- Free cash flow is rising . In this article, we already briefly discussed that the company is now boosting operating income while CapEx needs are falling. This year, the company is expected to do $5.9 billion in free cash flow, which implies a 14.5% free cash flow yield. This is enough to satisfy the 10% dividend and reduce debt. In the years ahead, free cash flow is expected to gradually improve.

{kind=link}

- CapEx has plateaued . This reason is related to free cash flow. However, I still wanted to highlight a few things. While the company is still using CapEx to grow, its CapEx is not expected to exceed $3 billion until at least 2026. Note that the company had more than $5 billion in CapEx in 2020.

The company expects growth capital expenditures for the full year to be approximately $2 billion, primarily allocated to the midstream, NGL and refined products, and interstate segments.

Furthermore, the company anticipates increased utilization in all core segments and continues to seek opportunities for optimization and expansion driven by domestic and international demand.

The capital allocation strategy focuses on balancing annual distribution growth, leverage targets, and free cash flow for growth.

In other words, the company doesn't need to boost CapEx to grow its core business, which allows it to protect the dividend and reduce debt.

- The balance sheet is healthier . At the end of this year, net debt is expected to be $50.3 billion. Analysts believe that ET will lower that number gradually to $46 billion in 2025. Incorporating gradual EBITDA growth, we're dealing with an implied 2025 net leverage ratio of 3.4x EBITDA. The company's current credit rating is BBB-, which is one step below the company's first target (BBB-flat). As Fitch has given the company a positive outlook, we're likely close to a rating upgrade.

The next reason is also a bit related to the other reasons.

- ET is seeing growth opportunities . In its 1Q23 earning call , the company said that it anticipates widening spreads across Texas due to the construction of a new pipeline. Growth in natural gas demand is expected to continue, supporting spread expansion in the coming years. In the crude sector, despite industry overbuilding, the acquisition of Lotus was seen as beneficial for ET. The company is also excited about the potential to bring additional barrels into its system, which could boost revenue. Additionally, ET mentioned an increase in the sensitivity range related to spreads, indicating an improved outlook.

Based on this context, I believe that ET isn't what it was when it cut its dividend in 2020 or was sold off in 2015. It's healthier, its balance sheet is being repaired, free cash flow is rapidly rising, and there are plenty of growth opportunities that can be achieved with subdued increases in growth CapEx.

Valuation

I also believe that the company is attractively valued, as it is trading at less than 7x free cash flow with a rising trend in free cash flow. Based on that calculation, ET is among the cheapest players in its industry.

This is also reflected in its consensus price target, which is currently $17. This price target is 33% above its current price, which makes ET one of the analyst's favorites. After everything that has been said in this article, I agree with that.

Pros & Cons

Pros:

- Strong dividend yield of 10%.

- Outperformed major midstream companies and Alerian MLP ETF, which I expect to continue.

- Transformation towards a healthier financial position.

- Increasing free cash flow and plans for dividend growth.

- A very fair valuation.

Cons:

- Complex tax structure as a Master Limited Partnership.

- Potential limitations for certain foreign investors.

- ET tends to sell off during recessions, although it's less prone to severe sell-offs, given its improved business.

- It's an income play, which may make it unsuitable for total-return-focused investors.

On a side note, please let me know if you want to see a pros and cons list in future articles!

Takeaway

Despite past struggles, ET has transformed into a remarkable income play. It offers a well-covered 10% dividend and has outperformed major midstream companies, including the Alerian MLP ETF.

While it faced downturns in the past, ET has made significant improvements. Its capital investment needs have decreased, its balance sheet is healthier, and it is generating increasing free cash flow.

Now, ET is focused on rewarding shareholders and plans to hike its dividend by 3% to 5% annually, which is a big deal given its 10% yield.

With a fair valuation, growth opportunities, and positive analyst sentiment, ET presents an attractive investment opportunity.

For further details see:

10% Yield And Outperformance - Has Energy Transfer Become Unbeatable?