IIPR - 10% Yielding REIT Buying Opportunities

2024-01-15 08:05:00 ET

Summary

- REITs have crashed and dividend yields have soared.

- Some REITs yield as much as 10% right now.

- We highlight two of our favorite 10% yielding opportunities.

Today, REITs ( VNQ ) are offering historically high dividend yields.

That's because over the past two years, their share prices have dropped significantly even as they kept growing their dividend payments:

NAREIT

{kind=link}

Higher dividend payments coupled with lower share prices result in higher dividend yields, and in some cases, the yields have reached up to 10%.

In today's article, we will look at two such high-yielding opportunities that we are buying for our Portfolio. Keep in mind that both of these REITs are somewhat riskier than the average REIT. We would only hold small positions as part of a well-diversified portfolio.

NewLake Capital Partners

NewLake Capital Partners (NLCP) is our Top Pick among REITs specializing in cannabis cultivation facilities:

NewLake Capital Partners

It has risen quite a bit lately, but it has still massively underperformed its larger peer, Innovative Industrial Properties ( IIPR ). We think that this is because NLCP is not listed on a major exchange and it leads to slower flows of capital:

- No debt: NLCP is one of just a few REITs that have zero debt. It is sitting on a significant net cash position (~10% of its market cap), which puts it in a strong position to play offense if opportunities present themselves, and defense in case some risk factors play out.

- Limited license: NLCP invests exclusively in cannabis cultivation facilities that are located in limited license jurisdictions. This is a crucial risk mitigator because occasional tenant issues are inevitable in this space. However, since the supply of these properties is limited by licenses even as the demand for cannabis keeps on growing, we believe that the existing properties should remain needed and even grow in value over time.

- Size advantage: NLCP is about 8x smaller than IIPR and we think that this should be a major advantage in the long run. Right now, NLCP cannot tap into the equity market to grow externally, but if that opportunity presents itself in the future, it should be able to grow far faster than IIPR because each new acquisition will have a much larger impact on its bottom line. Moreover, NLCP could start using some debt and this would make new investments even accretive to its FFO per share.

- Lower valuation: Despite owning better properties on average, having no debt, and enjoying better long-term growth prospects, NLCP is today a lot cheaper, trading at 8x FFO, 10% dividend yield, and an estimated 20% discount to its NAV. In comparison, IIPR is priced at 12x FFO, a 7.5% dividend yield, and an estimated 20% premium to NAV. The reason for this has nothing to do with the fundamentals of the company. It is simply because IIPR has a listing on a major exchange and as a result, its shares enjoy a much larger pool of buyers.

- Buybacks: The company already completed one $10 million buyback authorization, and it has authorized another one to keep buying more shares while they remain discounted. This is a great use of capital that should create significant value given that the implied cap rate of its shares is about 15%. I believe that the management and the board are very well aligned with shareholders. The Chairman is the former CEO of GPT, another REIT that did very well for us in the past.

- Catalyst: IIPR has a better listing than NLCP because it came public when such companies were still allowed on the NYSE. Eventually, as laws change, I expect NLCP to also obtain a similar listing, resulting in greater demand for its shares and a higher valuation that's in line with or higher than that of IIPR. In the meantime, we are buying NLCP on the OTC market and getting a nice discount for it.

Best of all, I think that the downside should be limited even in a worst-case scenario. For most REITs that use debt, a worst-case scenario would be bankruptcy and a complete wipeout of the equity. This is a real risk for speculative REITs like MPW, CORR, or even Branicks. However, since NLCP has no debt, a big cash position, and its valuation is so heavily discounted, I think that the downside is much more limited.

Even if NLCP had to cut its rents across the board by 30%, it would still trade at a high implied cap rate, a relatively low FFO multiple, and be able to pay out a decent dividend yield.

And that's of course highly improbable. The management has a great track record and significant skin in the game, they focus on limited license states, and it is very hard to believe that their underwriting could have been so off. Moreover, the fact that they are today aggressively buying back shares tells you loud and clear that they think that the downside is more than priced into their stock.

Finally, I would note that despite facing some tenant issues in 2023, the company was still able to grow its FFO thanks to its strong 2.7% escalations in their leases and the highly accretive share buybacks.

The REIT also just recently hiked its dividend, which currently yields 9.6%. I believe that the dividend is sustainable and in fact, the payout ratio is currently at the bottom of their target range of 80-90% of AFFO.

Therefore, I think that the risk-to-reward is very compelling, especially after the recent underperformance relative to IIPR and the broader REIT market.

Just a few years ago, cannabis REITs were loved by the market and priced at large premiums to their NAVs as the market saw them as a way to participate in the rapid growth of the cannabis sector with lower risk by owning the critical infrastructure. Now they are hated, but things could change again.

Uniti Group ( UNIT )

Uniti Group is an infrastructure REIT that owns a portfolio of fiber networks and it is today offering a 10% dividend yield.

The reason why its yield is so high is that its share price has crashed in recent years:

It crashed because of two main reasons:

- Too much debt: Firstly, the company is a bit more leveraged than your typical REIT. Its debt-to-EBITDA is 6x and this has caused the market to worry given the recent surge in interest rates.

- Tenant concentration: UNIT generates a very big chunk of its cash flow from one tenant called Windstream and they are alleging that their rent is too high and should come down when their lease expires.

Those are significant risks and there's no sugarcoating it.

But here is the good news.

Firstly, UNIT has no major debt maturities until 2027, and by then, the REIT's leverage should be a lot more reasonable and interest rates should have also returned to lower levels. Already this year, interest rates are expected to be cut at least 3 times and additional cuts are expected in 2025.

Secondly, the lease with Windstream is long and won't expire before 2030. Moreover, at a recent REIT conference, UNIT's CEO seemed confident that their current market rent is fair and should stay more or less at these levels. Their fiber network is essential to the communities they serve, they are growing in demand, and their replacement cost has only gone up with the recent inflation. Therefore, it seems that Windstream is simply making these allegations as a negotiation strategy.

In any case, UNIT now has plenty of time to diversify its business, grow new revenue sources, and deleverage its balance sheet to put it in a stronger position to negotiate with Windstream.

{kind=link}

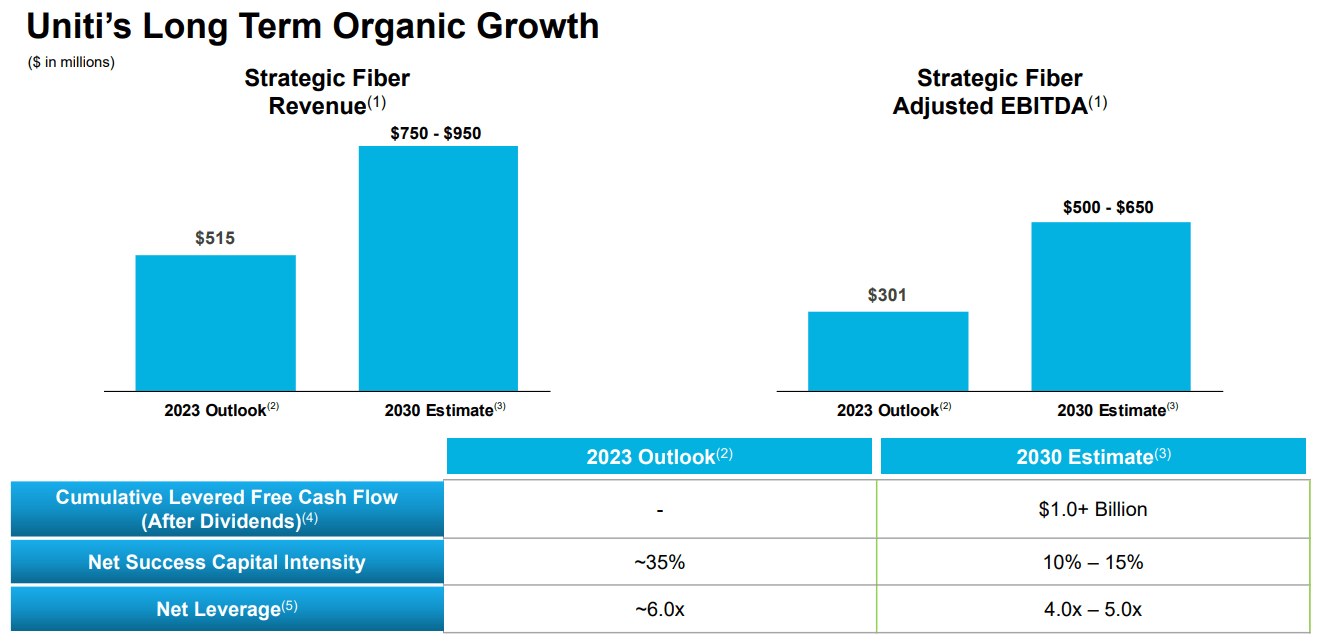

Right now, the company has $6.5 billion of revenue under contract and it is expected to generate over $1 billion of free cash flow after its dividend by 2030.

Despite that, its market cap is just $1.39 billion, it trades at 4x FFO, and its dividend yield is over 10%.

UNIT is so cheap because the market is pricing the Windstream master lease at a 19% implied yield. But if you valued it at a more reasonable yield, this would imply that UNIT has 100-200% upside potential from today's share price.

Uniti Group

So how I see it is that the risks are more than priced in, and the risk-to-reward is very compelling given how low the valuation has become, the lack of debt maturities in the coming years, and the long remaining lease term.

I would add that the CEO bought over $1 million worth of shares last year, he knows best what's the fair value of these assets, and he clearly thinks that the market has gotten it wrong.

{kind=link}

The 10.5% dividend yield is well covered, but it would not surprise me if they decided to cut it in order to accelerate their plans to deleverage the balance sheet and diversify the business. I would welcome such a cut as it would make the bear thesis even weaker. The market is not giving them any credit for the dividend anyway.

It also wouldn't surprise me if they simply sold parts or all of the business to another company. There were rumors of a potential buyout back in 2022 and the rumor was that UNIT was offered $15 per share. Today, they trade at just 1/3 of that, they are currently undergoing a strategic review, and the CEO is buying shares.

There are many infrastructure funds that have a lot of capital that's waiting to be invested and private markets would likely give these assets a much higher valuation.

Closing Note

There are many REITs that are offering high dividend yields right now, but for how much longer is the question?

Valuations are today still discounted but as interest rates return to lower levels in the coming months, I expect a lot of investors to rush back into REITs to secure these attractive yields.

This will then push their share prices higher and lead to lower dividend yields so don't miss this chance to secure these high yields while they still exist.

For further details see:

10% Yielding REIT Buying Opportunities