ET - 2 Champs 1 Winner: Energy Transfer's 9% Yield Beats Enterprise Products' 7% Yield

2023-10-22 09:10:28 ET

Summary

- Energy Transfer and Enterprise Products Partners are two prominent Master Limited Partnerships in the energy industry, offering stable income and potential for capital gains for investors.

- EPD is akin to a reliable Toyota Corolla, boasting a strong track record of dividend growth, financial stability, and an undervalued status, making it a compelling investment choice.

- ET, despite its turbulent history, has transformed into a more robust investment, offering a well-protected dividend yield, favorable valuation, and an impressive business outlook with a 9% yield.

Introduction

Energy Transfer ( ET ) and Enterprise Products Partners ( EPD ) are two of the best Master Limited Partnerships on the market. The two giants are the backbone of America's energy infrastructure and valuable sources of income and capital gains for millions of investors.

I have covered both in the past (EPD in this co-produced article and ET in this article ) and like both as long-term investments.

However, given recent developments, EPD is yielding "only" 7%, while ET can still be bought at a 9% yield.

In this article, I'll share my thoughts on two similar yet different stocks and explain which one I would be buying if I could only own one.

So, let's get to it!

A Quick Note

On a side note, please note that both companies operate in the midstream energy industry, which means they connect producers of fossil fuels (and related products) to customers. Although they are energy stocks, they do not produce oil and gas.

Both EPD and ET benefit from throughput fees, which makes cash flows reliable and both stocks good income tools. MLPs are not necessarily a bet on higher energy prices. That's what upstream companies are for.

Eland Cables

Both ET and EPD issue K-1 forms, which means taxes are shifted from the corporation to its unitholders.

Please make sure to be aware of what this could mean for your portfolio before buying.

Also, bear in mind that shares are called units. Dividends are called distributions.

In this article, I may use both, although it's not technically correct.

The Toyota Corolla Of MLPs

Enterprise Products Partners always makes me think of a Toyota Corolla. According to multiple sources , it's one of the most reliable cars ever built. It's not fancy, and it's not fast, but it sure gets the job done, which is to get its owners from A to B (and back) without unexpected costs, annoying breakdowns, and whatnot.

A few years ago, people got a good laugh out of a Toyota Corolla ad from Craigslist.

{kind=link}

So, why does this remind me of EPD?

Like the average car, EPD and its peers are dealing with many uncertainties and costs. In the Midstream industry, that's mainly demand fears and high investment requirements.

For example, over the past ten years, the Alerian MLP ETF ( AMLP ) has returned just 10% - including dividends!

This poor performance is due to a number of steep sell-offs that were caused by demand fears hitting sky-high investment requirements.

Since the Great Financial Crisis, the American energy industry has required a ton of new pipelines to facilitate rapidly rising oil and gas production, export facilities, and the production of related chemicals.

As building pipelines is expensive, most MLPs and C-Corp midstream companies used debt to fill funding gaps, as operating cash flows were often not enough to deal with capital expenditures - let alone dividends.

Energy Transfer is one of these companies, but more on that in a bit.

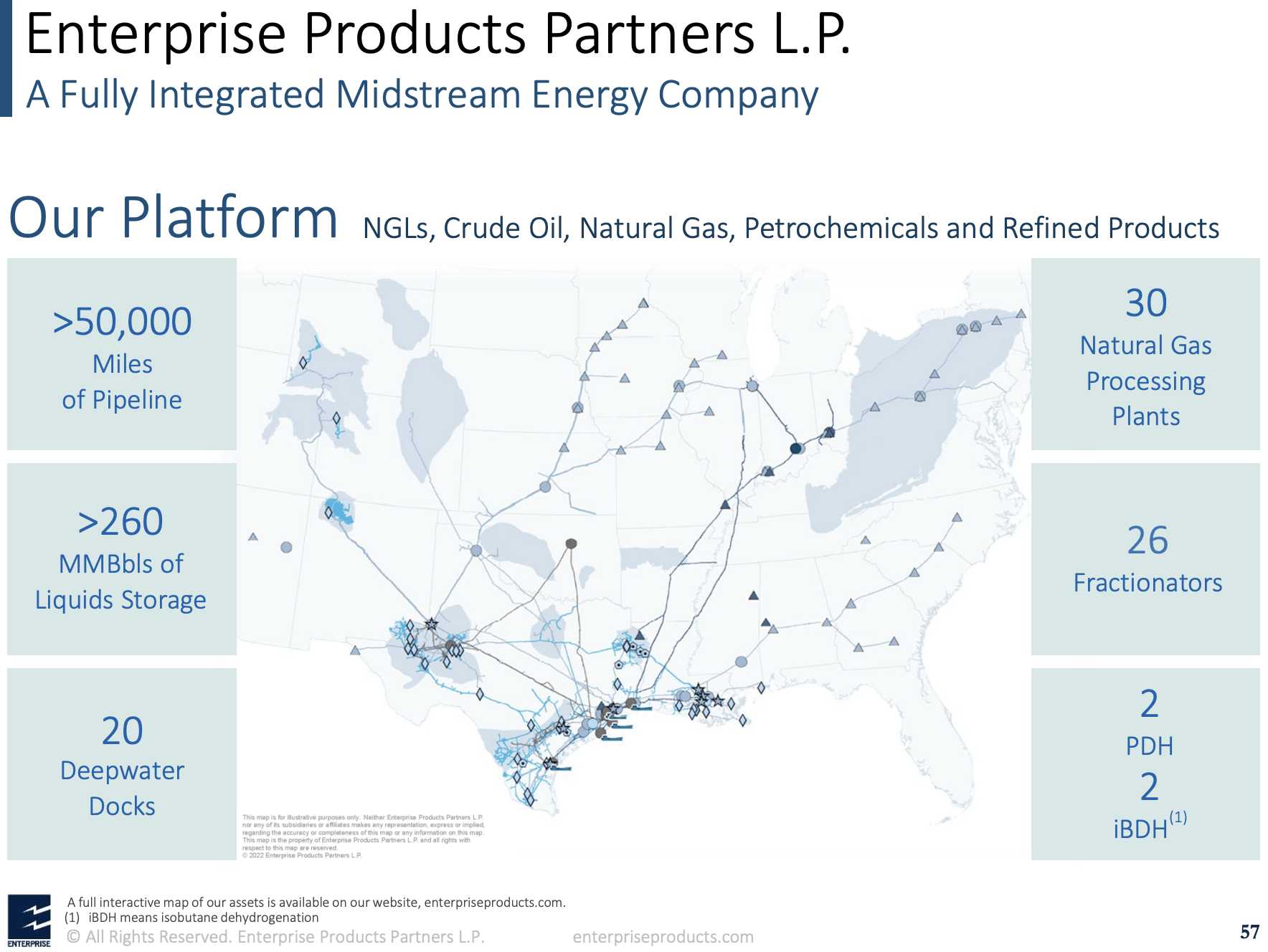

Enterprise Products Partners has a large network consisting of more than 50 thousand miles of pipelines, more than 260 million barrels of liquids storage, 20 deepwater docks, 30 natural gas processing plants, and 26 fractionators.

{kind=link}

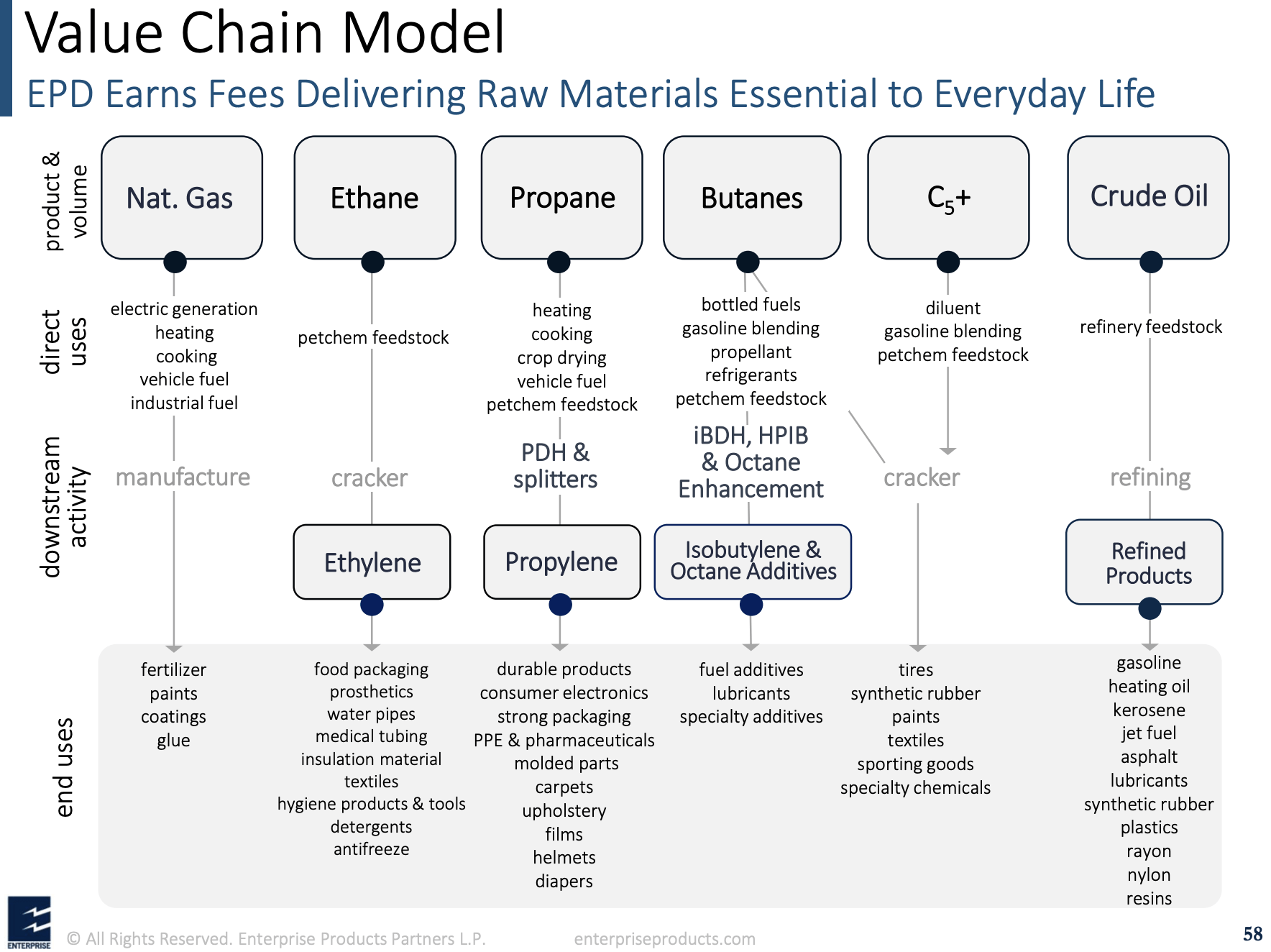

These assets connect producers of fossil fuels to buyers and turn these products into value-added products. They also facilitate exports, which is increasingly important in a world where the U.S. allies rely on its energy exports (for example, caused by the war in Ukraine).

{kind=link}

On top of that, there are a number of things that make EPD very special:

- Close to a fifth of its units/shares are owned by management.

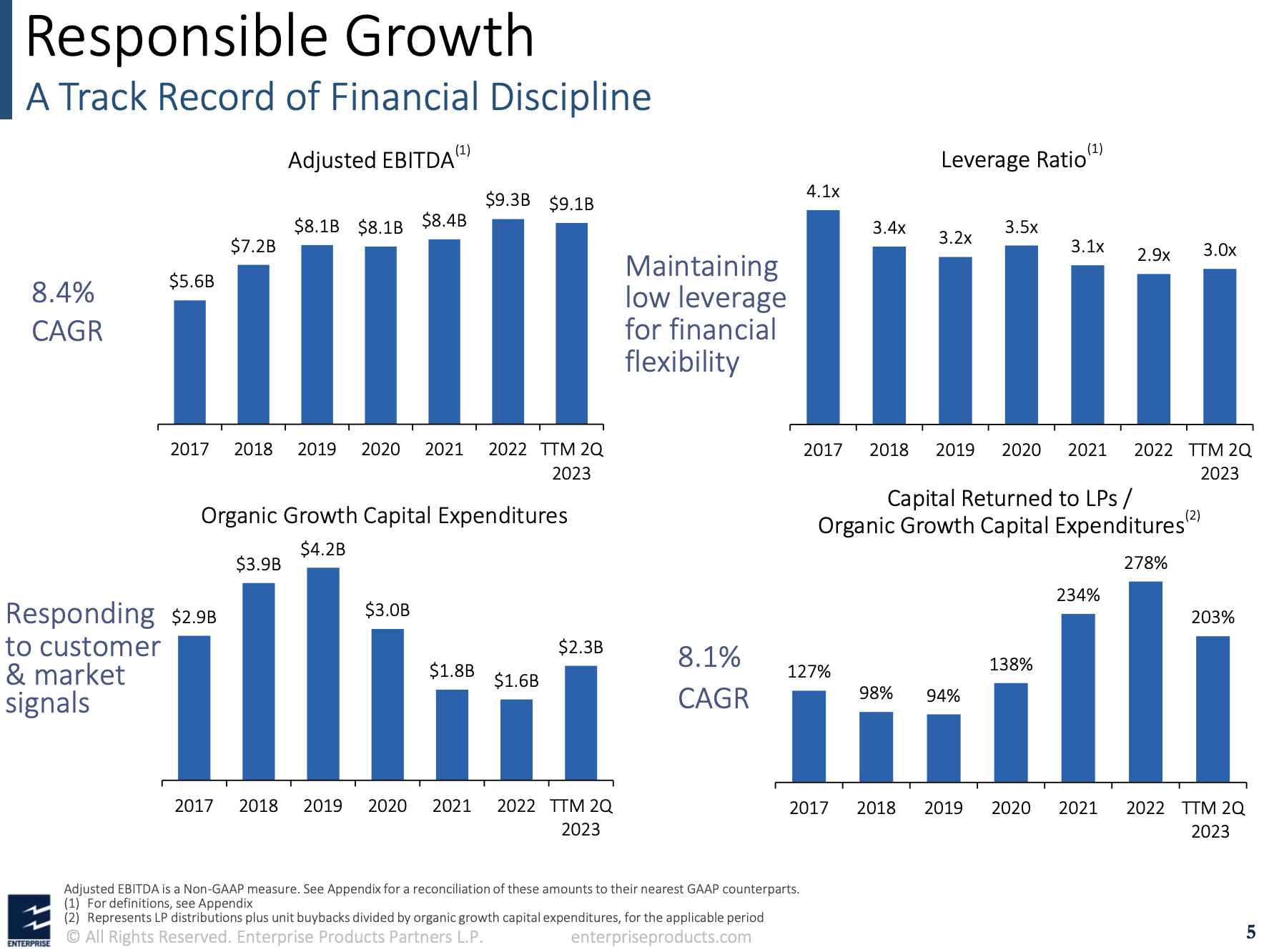

- The company has a leverage ratio of just 3.0x (EBITDA) and an A-minus credit rating, making it one of the financially healthiest companies in its sector.

As of 2Q23, the company has a total debt principal outstanding of approximately $28.9 billion, with a weighted average life of the debt portfolio at 20 years and a weighted average cost of debt at 4.6%.

Around 97% of the debt is fixed-rate. The consolidated liquidity at quarter-end was approximately $4 billion, which includes both availability under credit facilities and unrestricted cash.

The aforementioned leverage ratio of 3.0x aligns with their target range of 2.75x to 3.25x.

- It has grown its EBITDA by 8.4% per year since 2017.

- The company's capital expenditures have peaked, allowing the company to reduce leverage and boost shareholder returns.

{kind=link}

As a result, in the past four quarters, the company has distributed 57% of its operating cash flow to shareholders. CapEx accounted for less than 40%.

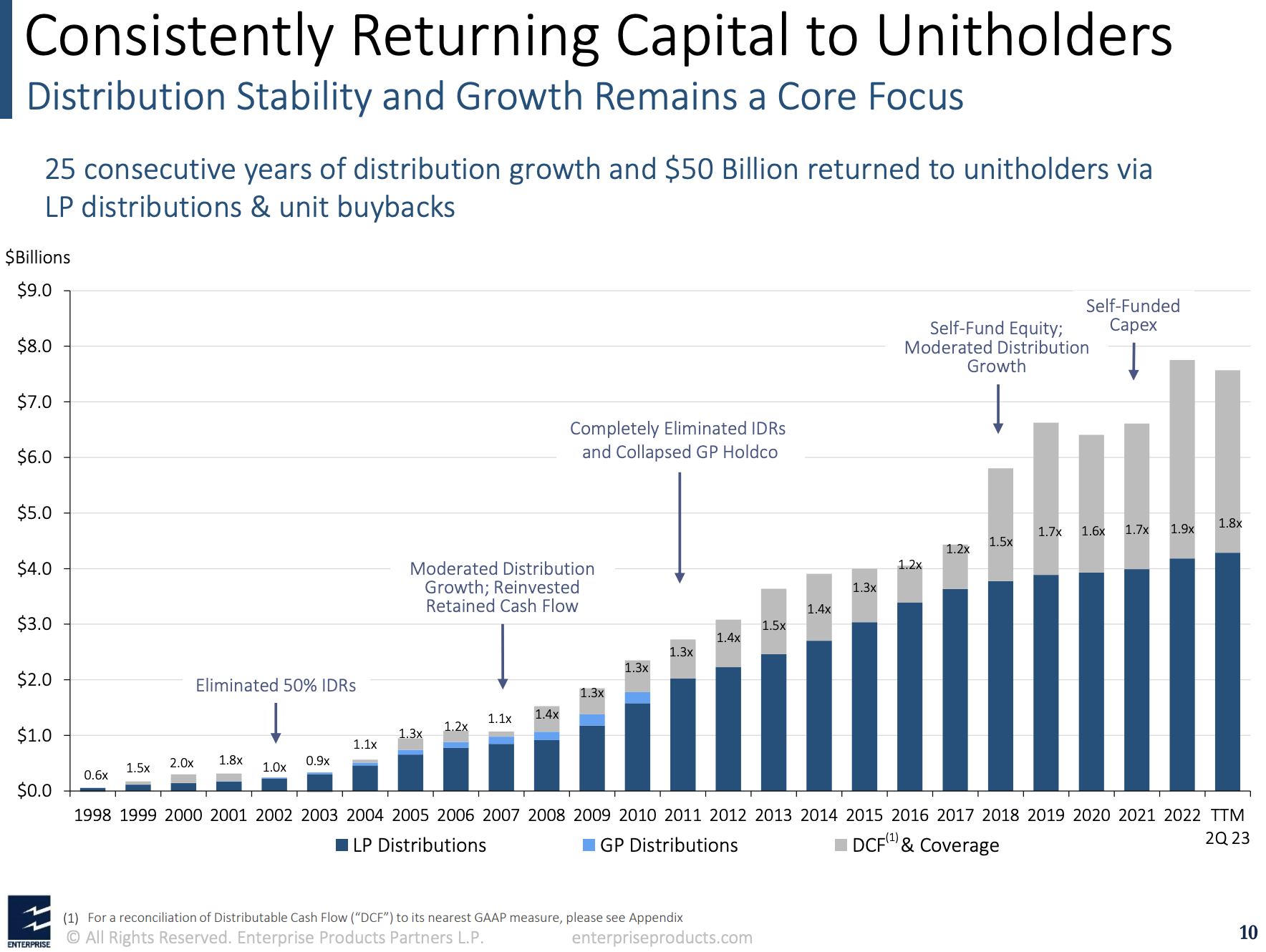

EPD also has a track record of consistent dividend/distribution growth. The company has hiked its dividend for 25 consecutive years, making it the only MLP with a dividend aristocrat track record.

Even better, the dividend has consistently been covered by distributable cash flows, allowing the company to hike its dividend even in 2015/2016 and during the pandemic, when most of its peers were cutting dividends.

{kind=link}

Just like the Corolla of the Craigslist ad, it didn't matter to EPD how much trouble its industry was in. Oil price crashes, demand fears, a major pandemic, political fears, wars, and more didn't keep EPD from sustainably raising its dividend.

This has allowed EPD to consistently outperform its peers, as shown by the YCharts chart earlier in this article.

Currently, EPD yields 7.3%. The 5-year distribution CAGR is 2.8%, which means that dividend growth is barely above the Fed's 2% inflation target.

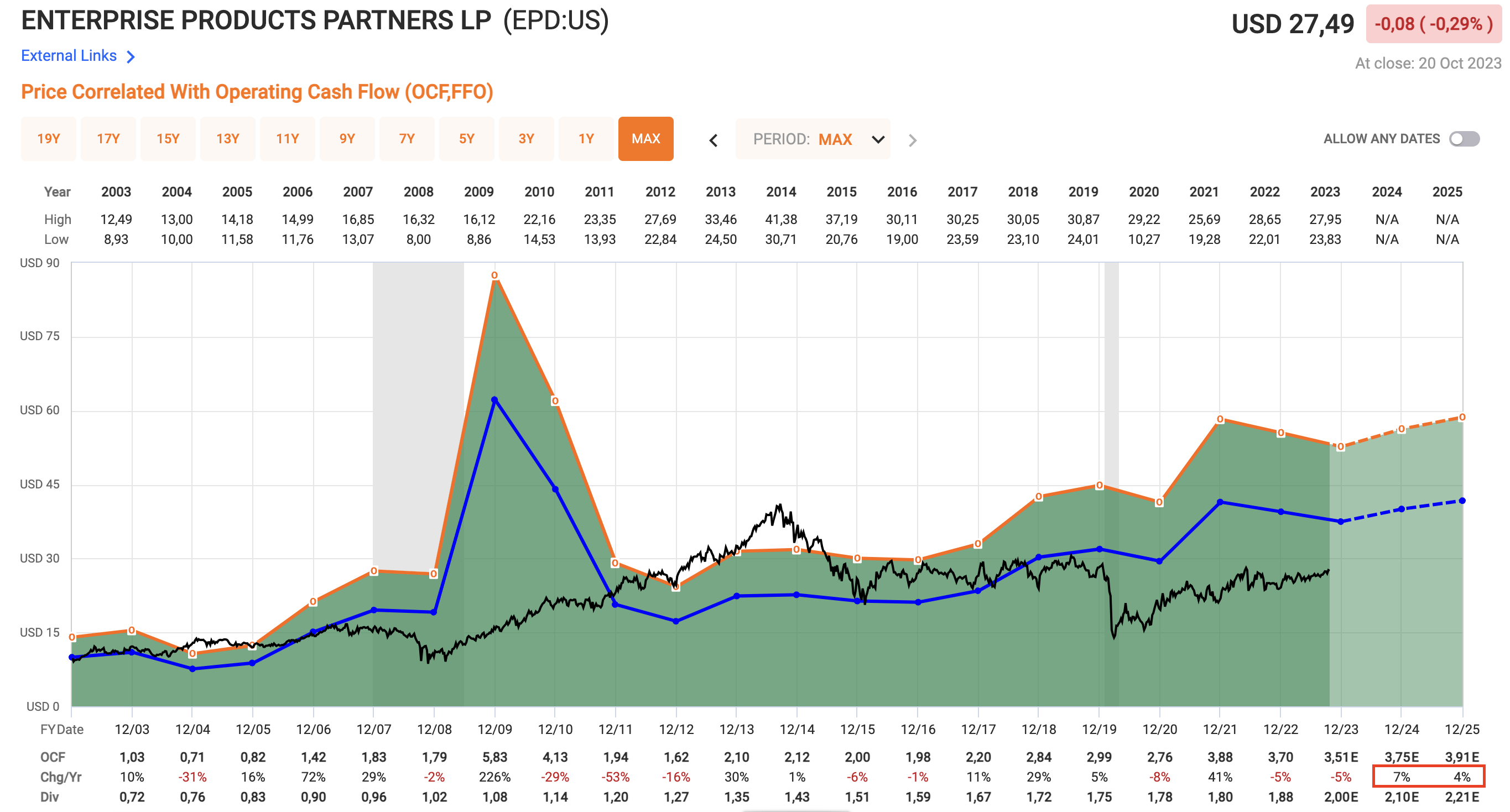

Valuation-wise, the stock is trading at 7.7x operating cash flow, which is below its normalized valuation of 10.7x OCF. Next year, OCF is expected to grow by 2%, followed by 4% growth in 2025.

{kind=link}

This paves the road for consistent low-single-digit dividend growth, and it's backed by $4.1 billion in projects under construction.

These projects include a natural gas pipeline expansion, a cryogenic natural gas processing plant, an NGL fractionator, and the PDH 2 plant in Chambers County.

The company also announced plans for three new natural gas processing plants in the Permian Basin and the first phase of the Texas Western products pipeline.

These projects will significantly expand their capacity and value-added services.

The current consensus price target is $32, which is 16% above its current price. I believe it's a fair target.

In general, I really like EPD. It's reliable, a source of elevated income, and undervalued.

However, it may not be the best play on the market.

The Comeback Kid

If EPD is a Corolla, ET is that car you almost totaled but managed to fix a few times. As the chart below shows, excluding dividends/distributions, ET lost 90% of its value during the 2016 commodity crash. It revisited these lows during the pandemic.

It also cut its dividend during the pandemic.

Overall, ET wasn't a great place to be.

That has changed.

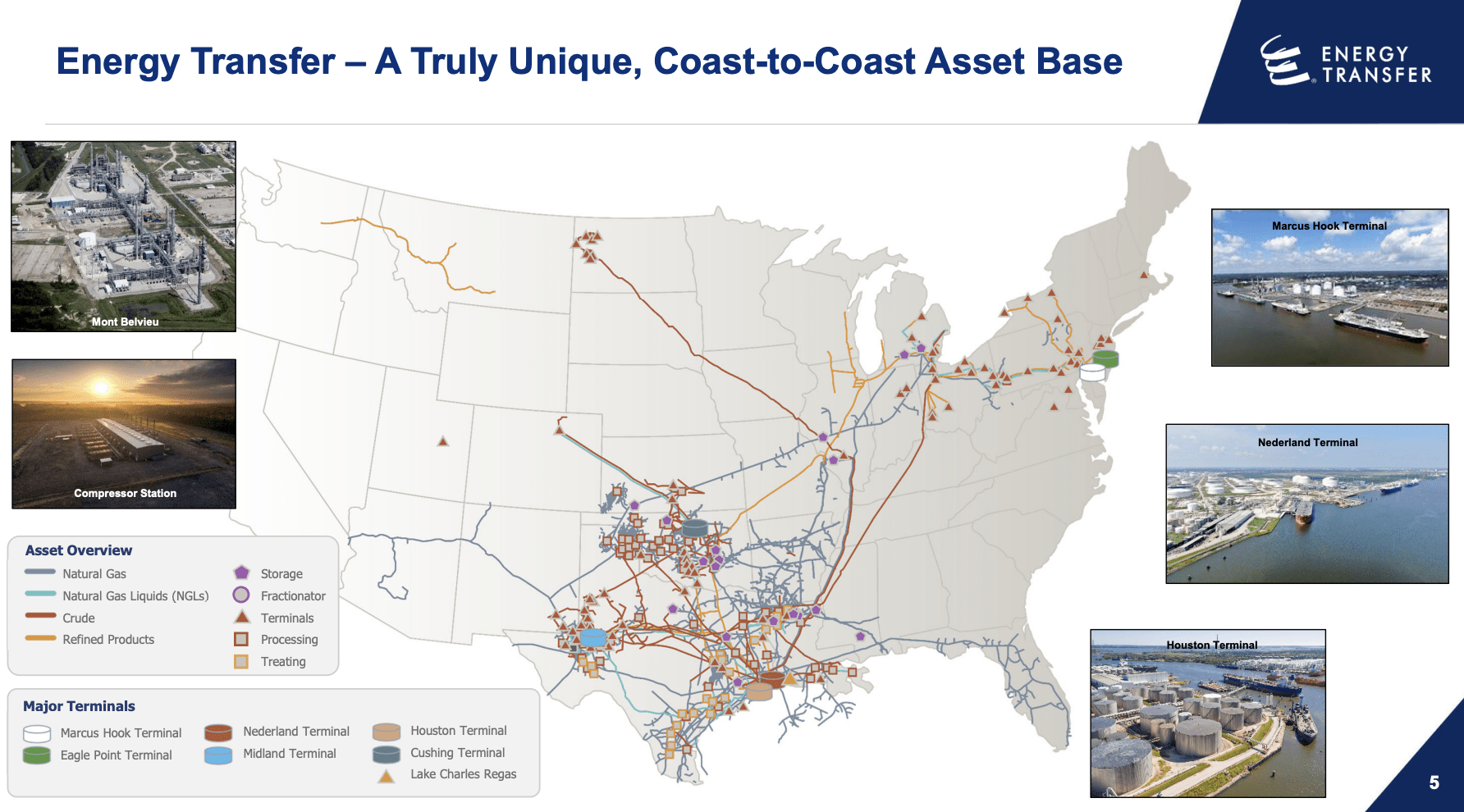

Excluding the Crestwood merger, the company has a massive footprint in the United States, which includes 14,300 miles of crude oil pipelines, a million barrels of daily Permian crude oil takeaway capacity, and pipelines to other major basins, like Bakken.

The company also has eight fractionators, close to 6,000 miles of NGL pipelines, and more than 54 thousand miles of gathering pipelines with almost 12 billion cubic feet per day of processing capacity, making it a giant in the natural gas industry.

{kind=link}

Now, ET is a much healthier, more mature corporation.

It could be a future Corolla.

In August, the company's credit rating was upgraded to BBB, which means it's now an investment-grade rating. Its leverage ratio is expected to be at the lower end of the 4-4.5x target range, and its CapEx requirements are dropping, allowing the company to boost free cash flow.

Looking at the table below, we see that the company is expected to generate $6.2 billion in free cash flow this year, which would translate to 14% of the company's market cap!

| $ in Millions |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 2023E |

| 2024E |

| 2025E |

| Free Cash Flow |

| 2 043 |

| 2 231 |

| 8 340 |

| 5 670 |

| 6 160 |

| 6 220 |

| 6 417 |

Bear in mind that free cash flow is operating cash flow after all capital expenditures.

This would mean that there's a path to double-digit dividends down the road.

In the second quarter, Energy Transfer announced a quarterly cash distribution of $0.31 per common unit, an increase from the $0.23 paid in 2Q22.

The company maintains its goal of achieving a 3% to 5% annual distribution growth rate while managing leverage reduction, enhancing equity returns, and ensuring sufficient cash flow for investment in its growth opportunities.

This month, the company hiked by 0.8% to $0.3125, which translates to a yield of 8.9%.

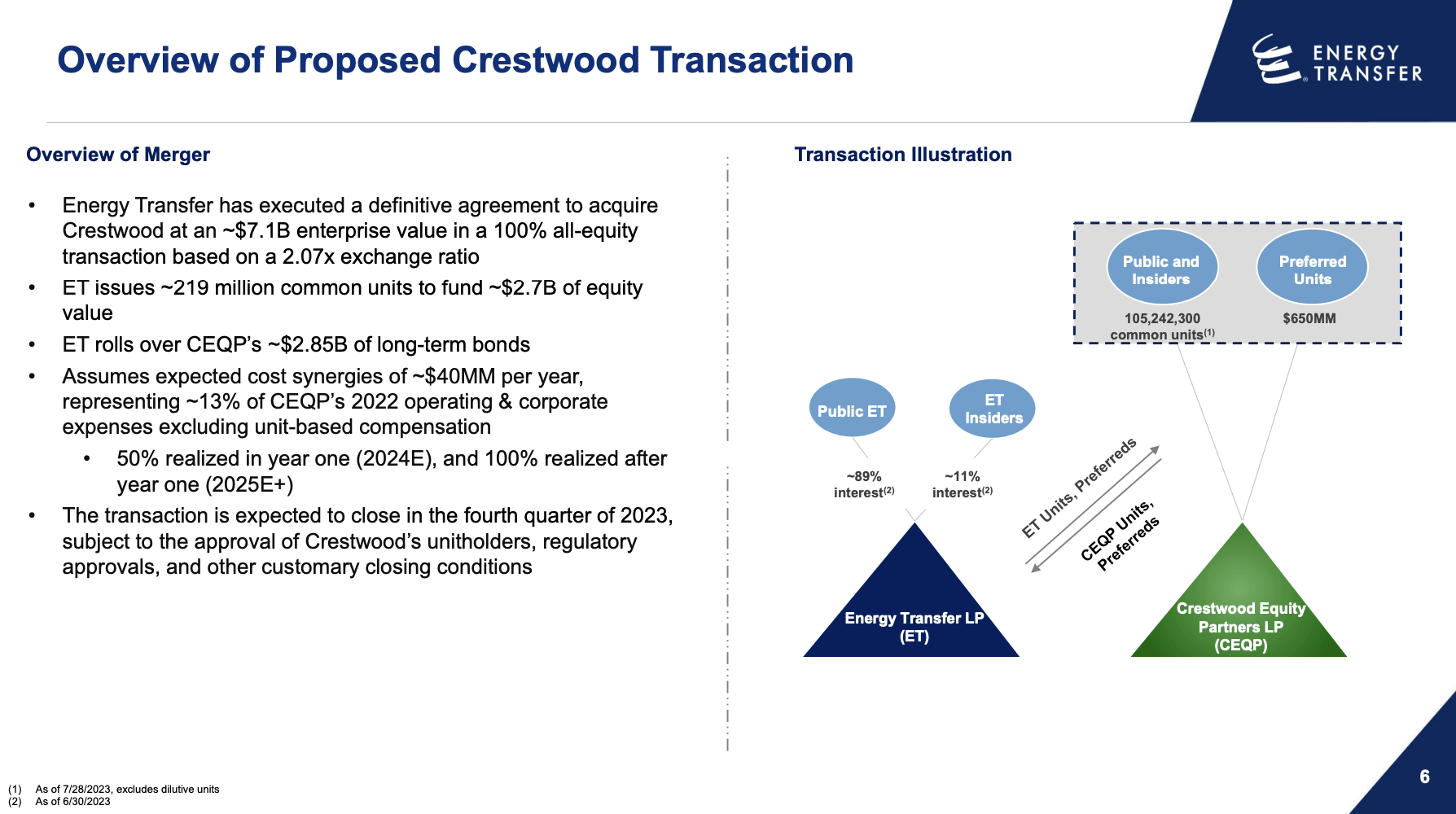

Going forward, the company is acquiring Crestwood Equity Partners in a $7.1 billion deal that wouldn't affect its credit and add a business with more than 85% fee-based income to its portfolio.

{kind=link}

Meanwhile, the company's Nederland and Marcus Hook export terminals continue to benefit from the increasing demand for ethane and LPG products, with plans to expand NGL export capacity at Nederland.

Additionally, the company is considering an optimization project at the Marcus Hook terminal.

In the Delaware Basin, several processing plants have been placed into service, supported by customer commitments.

The Gulf Run pipeline, connecting gas-producing regions to LNG export markets, is nearing full subscription, causing discussions about capacity expansion.

All of this supports low-to-mid-single-digit long-term operating cash flow growth, which makes the company attractive.

Due to past troubles, the company has a more attractive valuation than most peers.

ET is trading at just 7.5x forward EBITDA.

The current consensus price target is $17.30, which is 24% above its current price.

Thanks to the mix of a strong business, a juicy, well-protected dividend yield, and an attractive valuation, ET has turned into an outperformer.

Since 2011, ET has consistently outperformed the AMLP ETF and the dividend aristocrat EPD!

Given the attractive valuation and massively improved business, I expect that ET will continue to outperform, which is why I would rather buy it than EPD.

Needless to say, this is not a call to get people out of EPD. I respect EPD's business a lot. I just have to say that the risk/reward of ET is still better, even after two years of outperformance.

Takeaway

When comparing Energy Transfer and Enterprise Products Partners, I find myself leaning toward ET as the more attractive investment choice.

While EPD is like the reliable Toyota Corolla of the MLP world, offering a steady 7.3% yield and consistent dividend growth, ET has transformed from a troubled past to a more mature, promising option.

ET boasts a healthier financial profile, with an investment-grade rating and a path to double-digit dividends.

With a current yield of 8.9% and strong business growth prospects, it has consistently outperformed its peers since the pandemic, which I expect to last.

This is not to downplay the merits of EPD, which is reliable, income-generating, and undervalued. However, the risk-reward balance seems to tilt in favor of ET, making it my preferred choice in this comparison.

For further details see:

2 Champs, 1 Winner: Energy Transfer's 9% Yield Beats Enterprise Products' 7% Yield