CA - 2 Fast-Growing Dividend Stocks That Will Soar

Summary

- There are two dueling visions of the future of energy. Will it be clean and green or all of the above? Answer: Yes.

- We think the world is starved for energy, and countries will accept whatever forms of energy they have to in order to keep lights on, homes heated, and factories running.

- Renewables are undoubtedly an exciting growth story, but natural gas has a long growth runway as well.

- We present two of our favorite opportunities right now to generate high and growing dividend income while helping to meet the world's need for energy.

Co-produced by Austin Rogers

Dueling Visions Of The Future Of Energy

Today, we are living in the midst of an unprecedented level of uncertainty about the future of energy in the world. Two dueling visions of the future present very different outlooks.

The Paris Climate Accord calls for drastic reductions in carbon emissions across the world in order to prevent global average temperatures from rising more than 2 degrees Celsius. Advancements in renewable energy technologies in recent decades have dramatically lowered costs for these sources of energy, allowing countries to massively ramp up wind and solar installations.

But critics of the "net zero by 2050" plan that would seek to cap global temperature increases at 2 degrees Celsius say that it's simply not possible to achieve with current technologies and supplies of critical materials. As such, demand for oil, natural gas, and probably also nuclear power will continue to grow along with the world population over the next several decades.

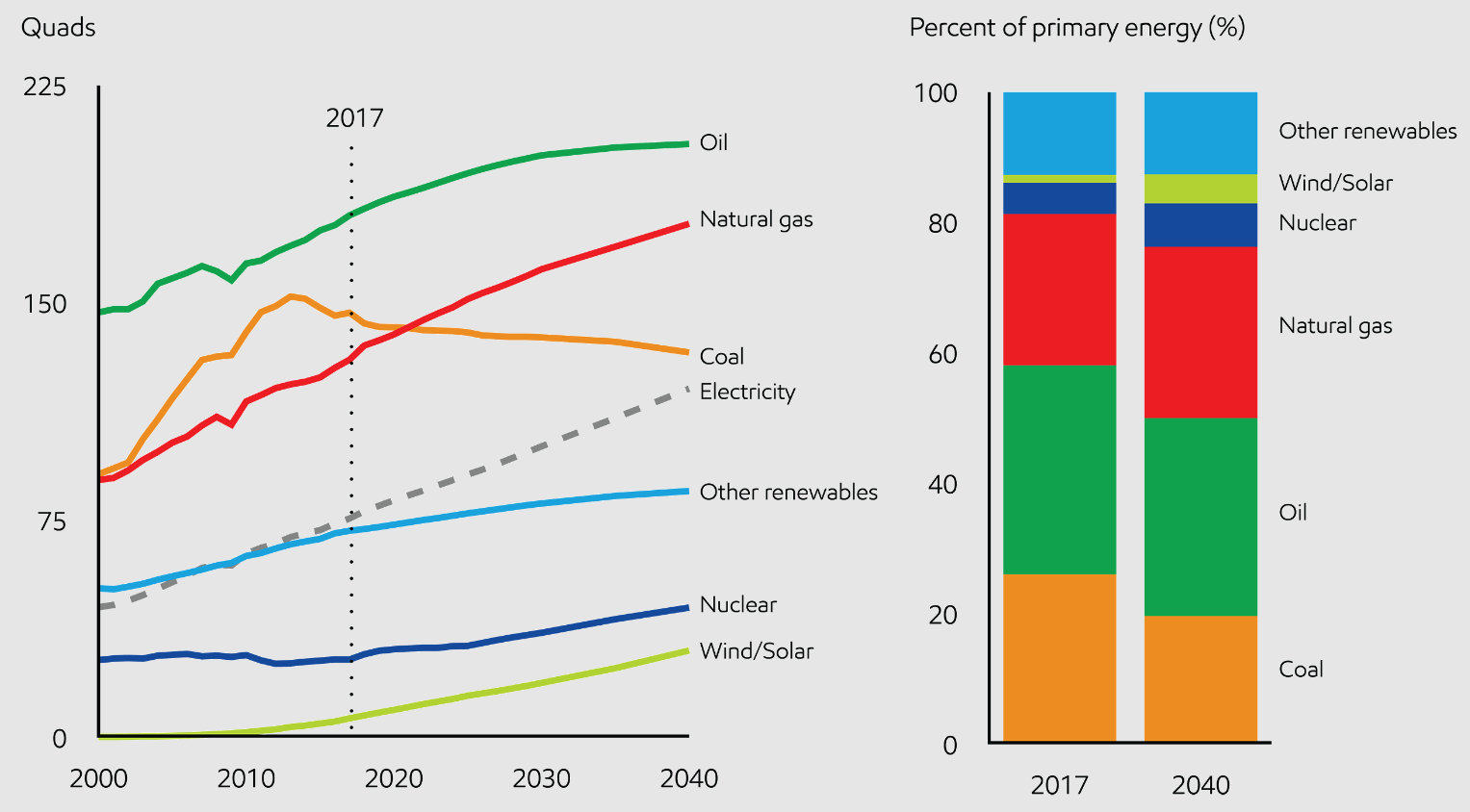

Representing this latter view, you have Exxon Mobil's ( XOM ) recent energy outlook, projecting that through 2040 energy usage will grow not only for renewables but also for oil, natural gas, and nuclear power.

{kind=link}

Is Exxon Mobil's energy outlook clear-eyed and realistic? Or is it overly optimistic in favor of the oil & gas giant's own specialization?

While we do think oil and gas demand should continue to grow for a long time to come, we think Exxon Mobil's forecast probably underestimates the lengths governments will be willing to go to decarbonize in the future.

On the other end of the spectrum, you've got McKinsey Global Institute's 2022 Global Energy Perspective, showing a very different trajectory for energy demand into the future.

{kind=link}

The McKinsey forecast has global oil demand peaking in 2025, natural gas demand peaking in 2035, and coal having already seen peak demand back in 2013, while Exxon Mobile's forecast shows oil and gas demand continuing to grow through at least 2040.

Already, we are skeptical of McKinsey's projection for a few reasons.

- As we highlighted in " 2 High-Yield Stocks For A Lifetime of Passive Income ," demand for coal has retouched its peak level this year as European countries scramble to secure energy sources to replace Russian gas.

- As Europe is learning now, it is dangerous for countries to become overly reliant on an adversarial nation for critical materials or intermediate products related to energy. The Western world remains overly reliant on China for the raw materials and solar PV panels necessary to continue ramping up renewables production.

So, which vision of the future of energy will prove accurate? Or will the truth ultimately end up somewhere in the middle?

Frankly, we don't know. We don't think anyone really knows. Exogenous shocks, such as a major energy producer invading a neighboring country, could always throw off one's well-thought-out projection.

Rather than pick a side, we at High Yield Investor believe that the future of energy will necessarily be an "all of the above" scenario, involving rapid growth in renewables but also natural gas, oil, and perhaps hydrogen.

Given that fundamental view, here are a few of our top picks in the energy/utilities space.

1. Brookfield Renewable Partners L.P. ( BEP , BEPC )

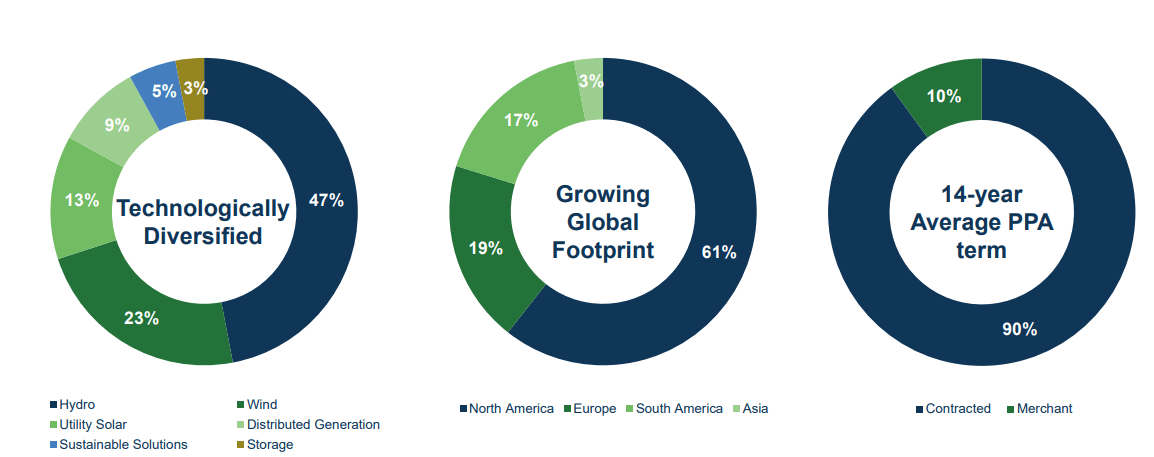

BEP is the industry leader in the ownership, management, and development of pure-play renewable power production assets. One of the most exciting aspects of BEP is its massive growth runway ahead, illustrated by its ~100-gigawatt pipeline of future development projects, around four times larger than its currently operational portfolio.

BEP is technologically diversified, with a little under half of its portfolio in hydropower dams, 23% in wind, and most of the remainder in various forms of solar energy.

{kind=link}

As you can see in the illustration above, BEP is also geographically diversified, with 80% of its assets located in North America or Europe, 17% in South America, and a small but growing 3% in Asia.

The overwhelming majority of BEP's cash flows come from long-term contracted power purchase agreements ("PPAs") with an average remaining term of 14 years. These contracts create a high degree of stability in BEP's income streams, and over 70% of them include inflation-adjustments that provide additional revenue boosts from elevated inflation.

Another best-in-class feature of BEP is the company's strong balance sheet that has earned a BBB+ credit rating. Though BEP does carry a lot of debt as part of its financing strategy, it also keeps a substantial buffer of liquidity on hand at all times. Currently, the company enjoys about $4 billion of liquidity (~30% of market cap).

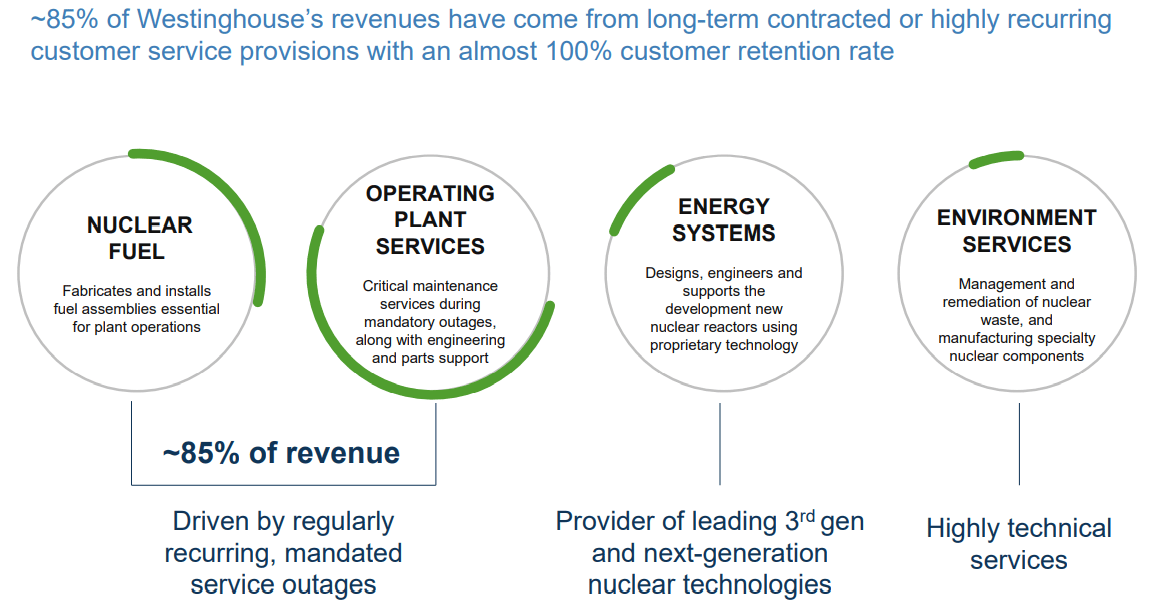

Recently, BEP agreed along with uranium producer Cameco ( CCJ ) to purchase Westinghouse, a business that provides maintenance and servicing to nuclear power plants.

{kind=link}

It makes sense that BEP would enter the nuclear power sector with this acquisition, as it is highly complementary to the rest of its clean energy portfolio.

Many countries that had previously been on a course to wind down their use of nuclear power have recently reversed course and chosen to extend the life of those nuclear plants and, in some cases, even to expand use of nuclear. Germany, France, and Belgium are all examples on the European continent, but the recently passed Inflation Reduction Act also contains some incentives for nuclear power production in the United States.

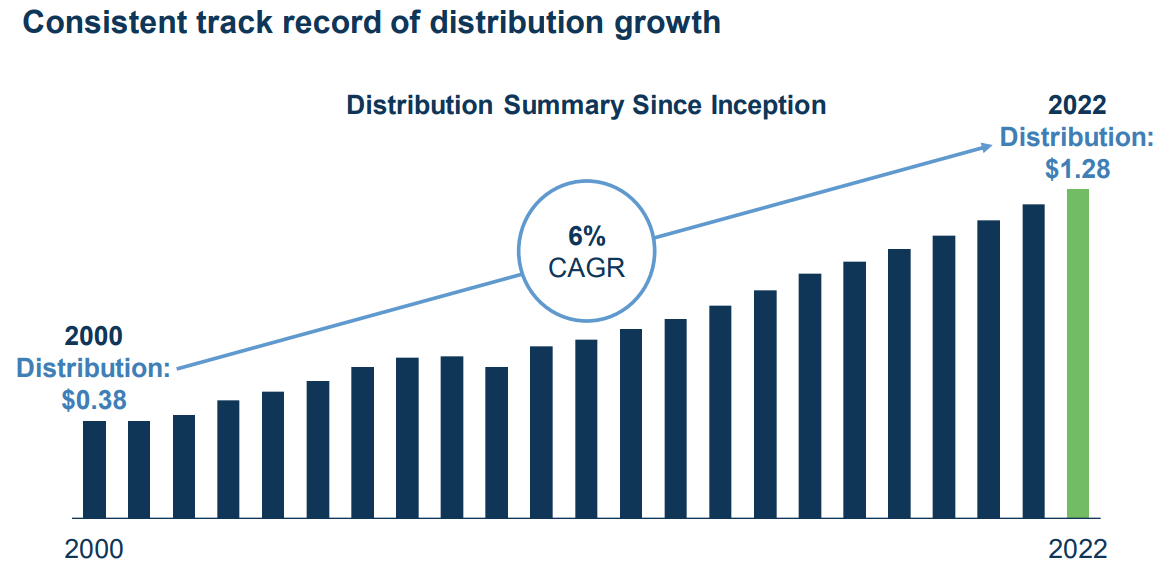

These and other investments should fuel BEP's continued strong funds from operations ("FFO") per unit growth, which has been around 10% annually for the past decade. And, in turn, this strong profit growth should fuel further distribution growth as well, which has likewise been strong and consistent for over two decades now.

{kind=link}

Combining BEP's 4.55% dividend yield and 6% dividend growth gets one to 10%+ total returns on its own. But consider also that BEP likely has significant price upside from here (at least 35%) when renewables come back into favor with investors.

2. ATCO Ltd. ( ACLLF )

ATCO is a Canadian holding company of various businesses, the primary of which being Canadian Utilities ( CDUAF ) accounting for around 80% of earnings.

While CU is a slow-growing regulated utility company operating mainly in Alberta, Canada, ATCO owns a handful of faster-growing businesses as well. Notably, ATCO has long been an industry leader in Canada's niche modular construction market. This business builds and operates temporary workforce housing for various projects like pipeline construction, typically located in remote areas.

ATCO Presentation

ATCO also owns a minority stake in Neltume Ports, an owner/operator of port facilities in South America.

Though ATCO's total earnings were rangebound from 2013 through 2021, this year seems to have broken that streak of weak performance.

Total adjusted earnings were up about 13.5% year-over-year in the first half of 2022, and adjusted EPS was up 13.8% because of a slight decrease in shares outstanding. Meanwhile, in Q2 2022, adjusted EPS surged 15.7%, indicating that ATCO's earnings resurgence this year may have just been getting started in the first half.

This impressive performance was largely driven by earnings growth at Canadian Utilities (up 18.2% in the second quarter), which could mean that CU's long streak of underperformance may have come to an end.

Bolstering this view that earnings growth momentum will carry on into future quarters is this comment from management in the Q2 conference call :

The drive of our leaders to deliver top tier performance, our operating expertise and our historical track record, all support a view that outperformance above allowed ROEs [returns on equity] will be attainable for 2023.

Supporting further earnings growth is the fact that CU recently announced the $730 million acquisition of renewable energy assets and the associated development pipeline of Suncor Energy Inc. ( SU ).

ATCO Presentation

These assets are mainly concentrated in Alberta, which makes them a great bolt-on addition to CU's existing power production portfolio. They also give a big boost to CU's long-term decarbonization efforts, which have thus far been fairly minimal.

And both CU and ATCO should have plenty of relatively low-cost financing to make attractive investments in the future, thanks to their investment grade credit ratings of A- and BBB+, respectively.

Proof of ATCO's ability to generate long-term value for shareholders is in the pudding, or rather, the 29-year dividend growth streak.

{kind=link}

ATCO's 4.5% dividend yield also remains very well-protected by earnings, with a payout ratio of only 46.6% in the first half of 2022.

We believe ATCO has 20% upside to fair value. Combining that with dividends and growth, this Canadian gem should enjoy strong, double-digit returns from here.

Bottom Line

The world needs energy. And though we all have preferences about what sources should provide that energy, almost all of us would rather keep the lights on and our house warm than to achieve all of our energy preferences. That virtually ensures that the world will continue to take an "all of the above" energy sourcing strategy for the foreseeable future.

As such, great opportunities exist for high-yield investors all across the energy space, from oil & gas to renewables to utilities.

For long-term investors, we at High Yield Investor believe BEP and ATCO are two phenomenal ways to generate high dividend income while participating in the provision of badly needed energy across the globe.

For further details see:

2 Fast-Growing Dividend Stocks That Will Soar