CA - 2 High-Yield Blue Chips At 52-Week Lows Worth Buying

2023-08-22 07:00:00 ET

Summary

- Even in challenging and overvalued markets, something great is always on sale. That includes high-yield blue chips at 52-week lows.

- Of course, the key is to separate the trash from the treasure to avoid unsafe dividends and yield traps.

- Here are two high-yield dividend legends trading at 52-week lows that are potentially wonderful ways to safely earn income ahead of the 2024 recession.

- One is a thriving consumer staples giant that can't keep up with demand for its high-margin products, and that's the main reason it's down 22% in a few weeks.

- The other is one of the fastest-growing telecoms in the world, with a yield of 6.5%, the highest in 14 years. It's a bit more speculative, but if it can deliver on its expected 28% annual growth in free cash flow, it could be a 5X return within a decade.

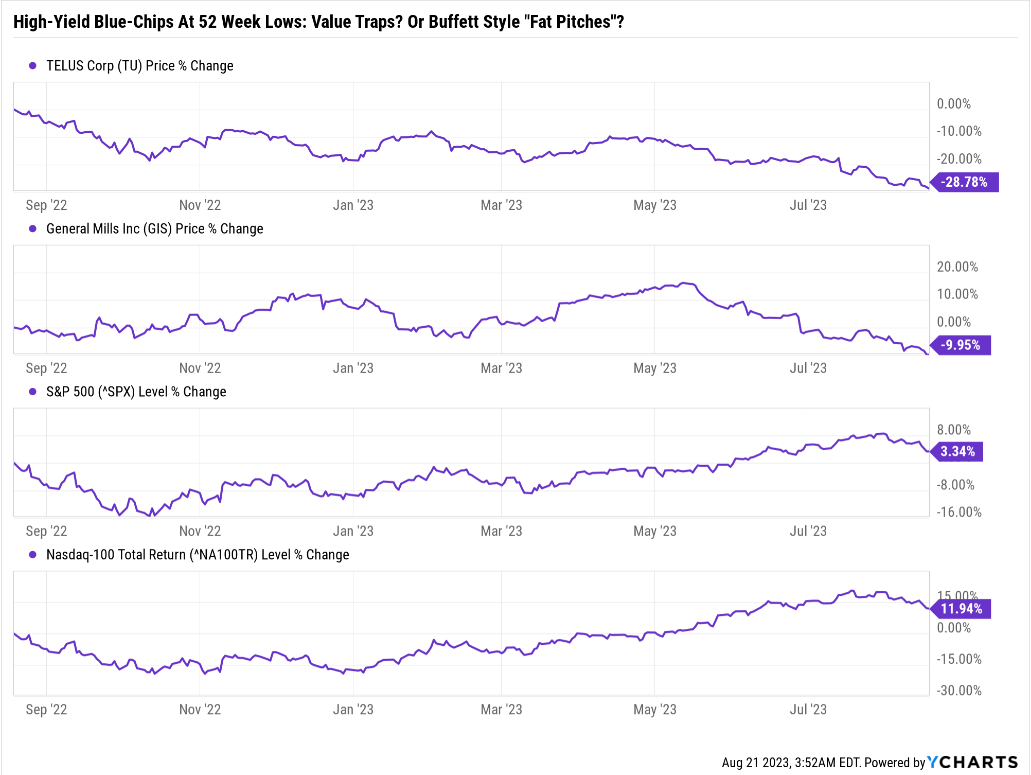

I've often said that it's always and forever a market of stocks, not a stock market. So even in highly overvalued and speculative market bubbles, as we've recently found ourselves in, you can always find wonderful blue-chip bargains.

Companies that are world beaters that have been thrown out with the bathwater.

I've been asked to update two famous high-yield blue-chips that have been pummeled and are trading at 52-week lows. Are these value traps set for further slides into the abyss? Or deep value "fat pitches" that can generate medium-term Buffett-like gains?

Consider General Mills (GIS) and TELUS (TU), two famous names that have been around for 157 years. These are companies the bond market thinks will likely outlive us all.

{kind=link}

YCharts

Of course, there's more to good high-yield dividend investing than just buying beaten-down big-name companies.

{kind=link}

JPMorgan Asset Management

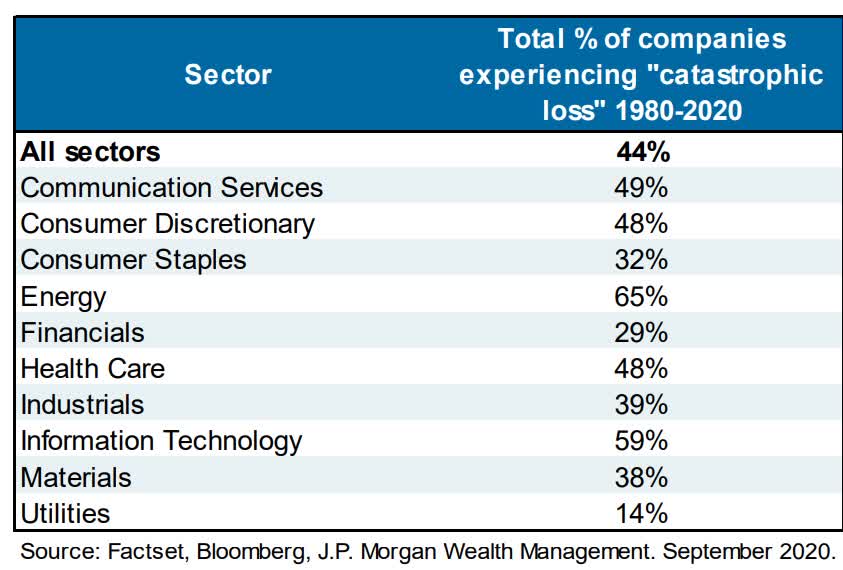

If 44% of all companies suffer permanent 70%-plus crashes, it's very important to distinguish the value traps from the Buffett-style bargains.

Note that 50% of telecom companies suffer catastrophic declines, while for consumer staples, it's still 32%.

The stability of a business model doesn't necessarily protect you from the risk of a catastrophic permanent decline.

So let's consider why the market hates General Mills and Telus and whether you should avoid these legendary dividend growers, back up the truck, or something in between.

Why The Market Likely Hates General Mills

There are many reasons for a stock to be at a 52-week low.

- it may have started in a bubble that has now popped

- it may be seeing a collapse in earnings

- it may have just made a big debt-funded acquisition

- it may have an unsafe balance sheet and is facing credit rating downgrades

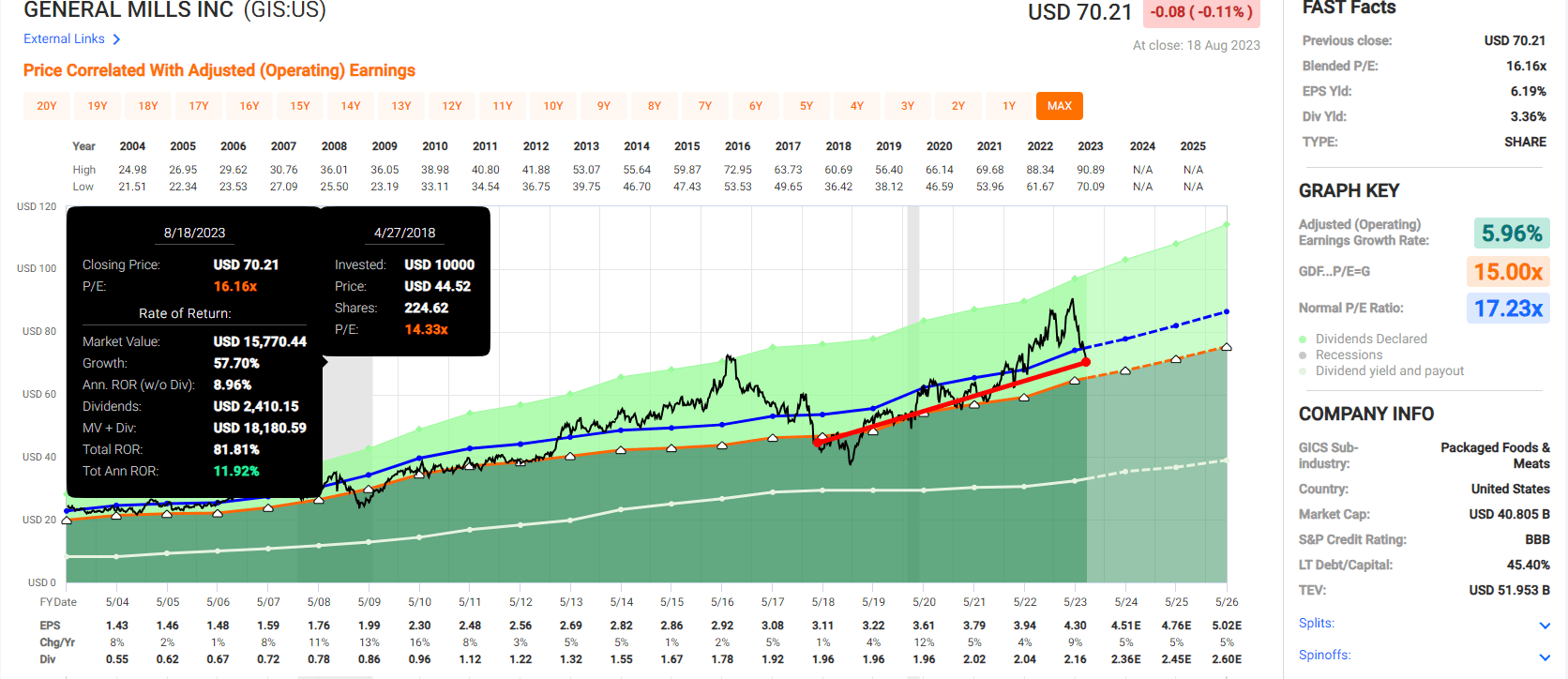

So let's look at what's going on with General Mills.

General Mills Since Announcing It Was Buying Blue Buffalo For $8 Billion

{kind=link}

FAST Graphs, FactSet

General Mills fell 42% from July 2016 to December 2018 in a bear market that was triggered by the TINA (there is no alternative) rally, created by record low interest rates at the time.

High-yield blue chips like GIS, PEP, and even tobacco were the new hotness, and in the race for yield that doesn't lack, Investors thought "no price too high for a dividend stack."

Well, we know how that always ends, eventually. It just so happens that General Mills tried to acquire Blue Buffalo during a bear market. It was a debt-funded deal that many analysts thought was overpriced.

It seemed desperate to Wall Street because the stock already was down 35% when the deal was announced.

General Mills said that it would accelerate Blue Buffalo's growth and that its strategy of selling off slower-growing brands like yogurt and Hamburger helper to recycle the proceeds into hot growth markets like premium dog food would pay off eventually.

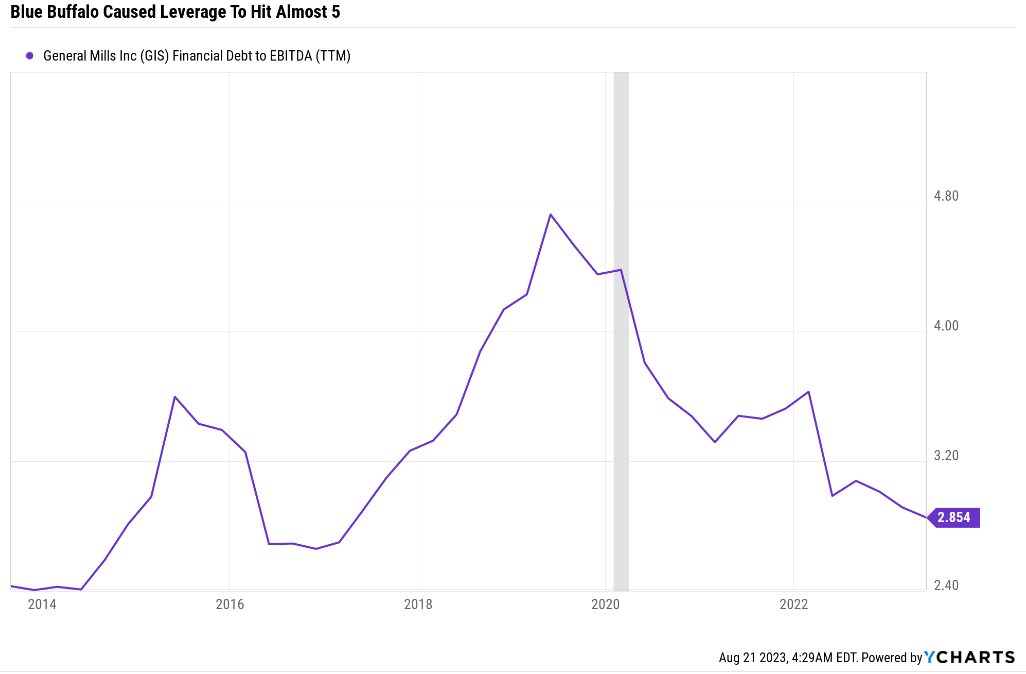

But here's what scared Wall Street and income investors.

{kind=link}

YCharts

4X debt/EBITDA is what rating agencies consider safe for this steady eddy industry. And GIS took its leverage to almost 5X to buy Blue Buffalo. At the time, interest rates were at record lows, but that's what had Wall Street so worried.

They thought low rates made management reckless and overpaying for a hot brand.

GIS froze its dividend for three years as it focused on paying down debt and deleveraging. It's done a wonderful job though S&P has yet to upgrade it back to the BBB+ credit rating it had before buying Blue Buffalo.

Another reason Wall Street is upset right now is that GIS can't keep up with demand at Blue Buffalo. It's capacity constrained, so the big acquisition is leaving money on the table.

Why General Mills Is A High-Yield Ultra SWAN Buy

General Mills' problems are all temporary, and its overall strategy of adapting to changing consumer tastes is a good one.

General Mills adapts with the times and is focusing its marketing on digital advertising for brands that are on trend. It's focusing on more fresh foods over traditional canned, and of course, things like premium dog food.

{kind=link}

FactSet Research Terminal

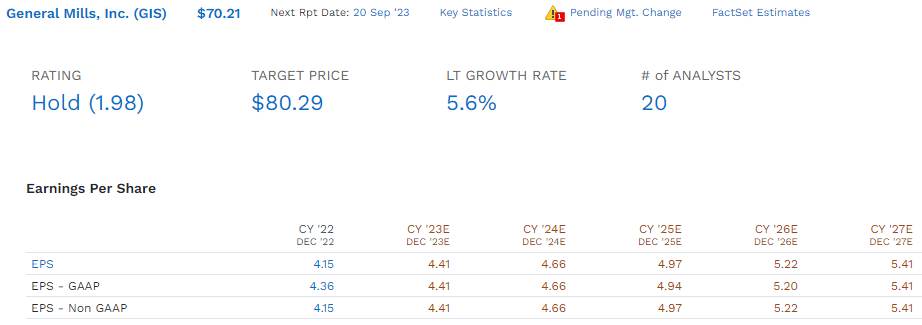

GIS has historically grown from 5% to 6%, and analysts currently think that's how quickly it will continue to grow.

The 3.4% yield is the highest in over a year and historically in the top 15% of all yields GIS has offered over the last quarter century .

Don't get me wrong; GIS isn't a Buffett-style long-term "fat pitch" retirement dream stock. If you buy it today, you will earn 3.4% yield plus 5.6% growth if it grows, as analysts expect.

That's a 9% long-term total return, potentially for decades. The good news is that this is a high-yield Ultra SWAN whose attractive valuation means it can likely do much better in the medium term.

GIS hasn't cut its dividend in 125 years since it began paying one in 1898. That's a dividend that wasn't cut during:

- the 1907 banking crisis

- the 1918 Spanish Flu (killed 5% of humanity)

- WWI

- Great Depression

- WWII

- five other killer pandemics

- interest rates as high as 20%

- inflation as high as 22%

- over 23 bear markets

GIS is built to deliver very safe and growing dividends even though it won't be an aristocrat for decades.

General Mills Summary

- DK quality rating: 89% very low risk 13/13 Ultra SWAN

- historical fair value: $75.16

- current price: $70.21

- discount: 7%

- DK rating: potential good buy

- yield: 3.4%

- LT growth consensus: 5.6%

- LT total return potential: 9.0%

- valuation boost for the next decade: 0.7%

- 10-year total return consensus potential: 9.7% = 152% total return

In the next decade, GIS could deliver about 9.7% returns, historically market-like and likely better than the 5% to 6% analysts expect for the S&P.

GIS 2025 Consensus Total Return Potential

{kind=link}

FAST Graphs, FactSet

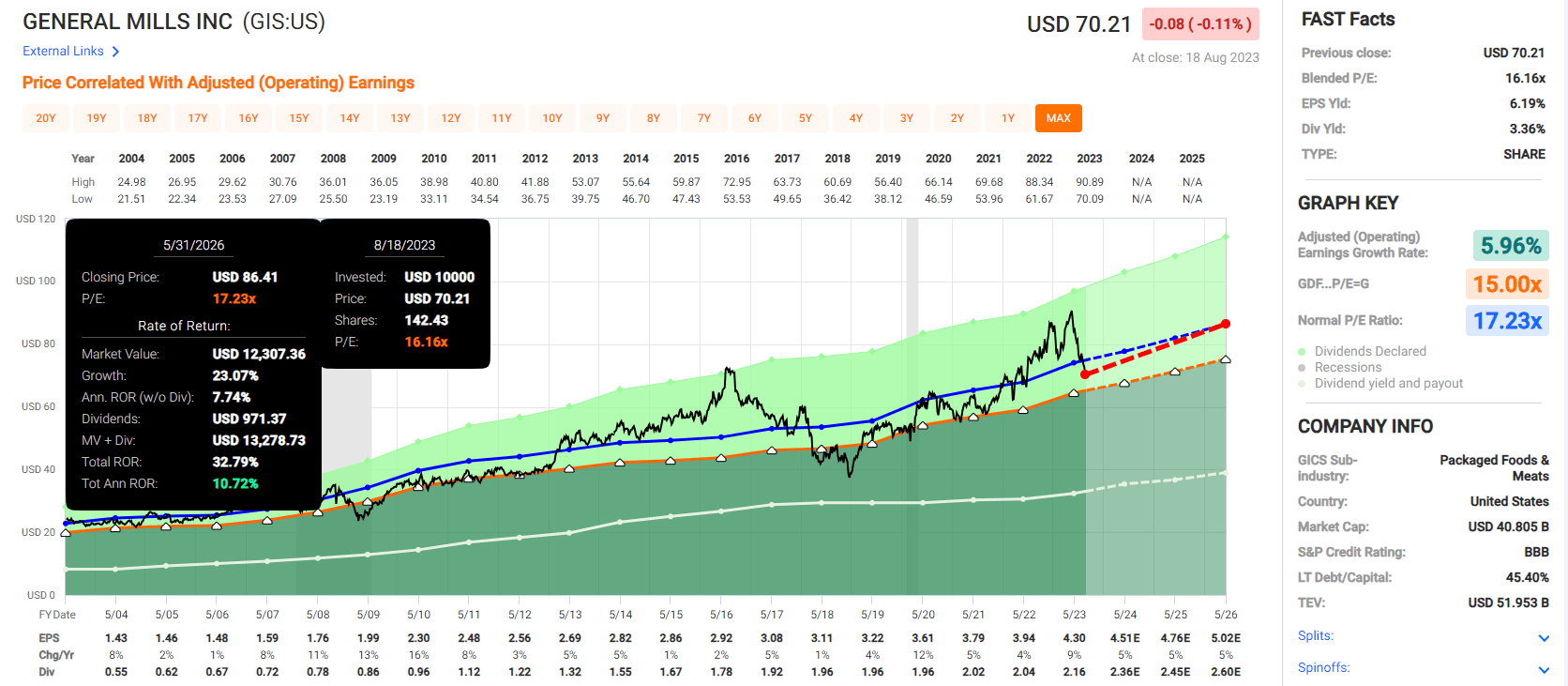

Notice how, thanks to beginning in a bubble, which burst when the market suddenly freaked out over Blue Buffalo supply constraints, GIS isn't that undervalued. Its 22% decline merely brought it from a 21 PE to a 16 PE.

It went from 24% overvalued to 7% undervalued, offering long-term 9% to 11% total return potential adjusting for valuation.

Why The Market Hates Telus

Telecom is a recession-resistant, super steady utility-like business with flaws.

Telus struggled with costs, and some of its side businesses performed poorly, particularly Telus International, or TI, in which Telus owns a 55% economic interest." - Morningstar

Like big pharma, patent cliffs roll around every decade or so, in this case, a new generation of digital communication.

{kind=link}

FAST Graphs, FactSet

Note how Telus' free cash flow can be highly variable, ranging from $123 million in 2016 up to $1.3 billion in 2012.

That's because it can, at times, have to spend a fortune, as much as $2.8 billion, on growth spending, specifically 5G.

But that's expected to start paying off, with free cash flow soaring to a record $4.2 billion by 2028.

- 28% annual free cash flow growth from 2022 to 2028

That's almost 2X the company's previous record in free cash flow.

Telus hasn't cut its dividend in at least 20 years, at least in local currency.

- Currency fluctuations don't count against a company's dividend streak

{kind=link}

FAST Graphs, FactSet

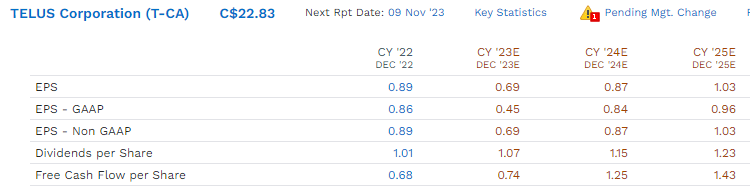

Why is the market partially worried about Telus? Probably because the payout ratios are expected to be over 100% on both earnings and free cash flow basis for several years.

Telus Medium-Term Payout Ratio Consensus Forecast

| Year |

| EPS Payout Ratio |

| Free Cash Flow Payout Ratio |

| 2022 |

| 113% |

| 149% |

| 2023 |

| 155% |

| 145% |

| 2024 |

| 132% |

| 92% |

| 2025 |

| 119% |

| 86% |

(Source: FactSet Research Terminal)

According to rating agencies, 70% is the safe payout ratio for telecoms, and it looks like TU's 6% to 7% dividend growth rate is going to mean it might not reach a safe payout ratio until 2028, the year of its $4.2 billion in consensus free cash flow.

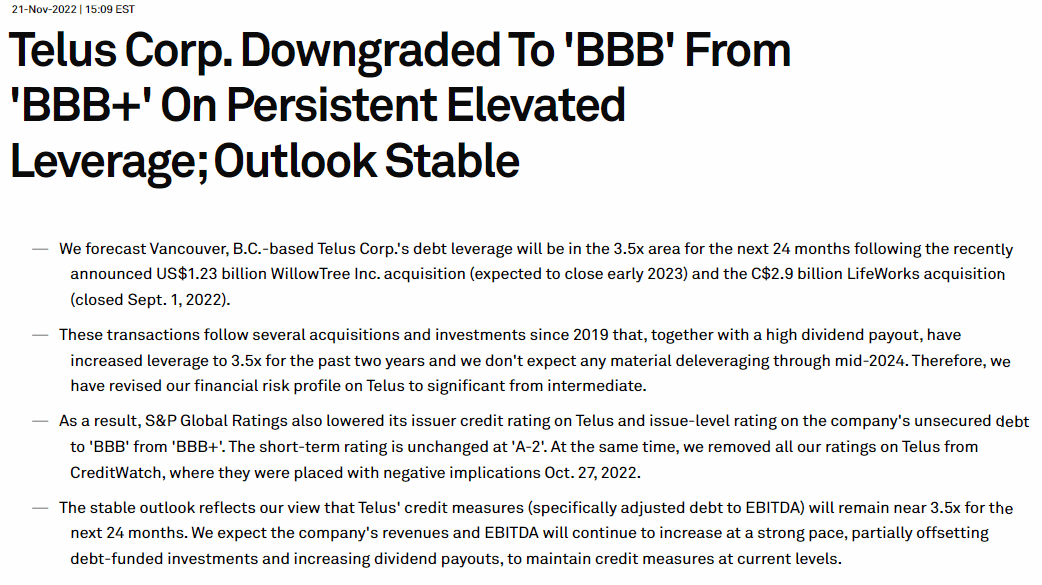

This is partially why S&P downgraded Telus from BBB+ to BBB stable in November 2022.

{kind=link}

S&P

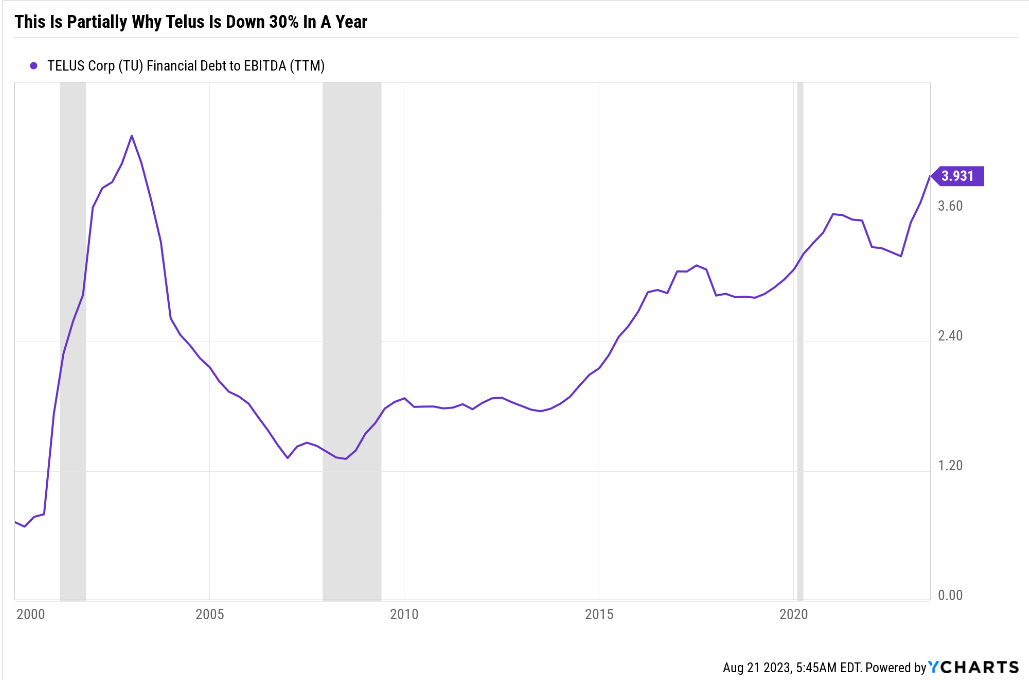

S&P's method for measuring adjusted EBITDA shows elevated leverage for Telus, that's been rising since 2018 due to various five G-related acquisitions.

Acquisitions that have continued and continue to be funded with debt.

{kind=link}

YCharts

It's one thing to fund acquisitions and dividends with the lowest-cost debt in human history. In fact, in 2021, interest costs for the US government hit -1.5%.

A-rated corporations could borrow at negative rates, but Telus was not among them, being a BBB+ rated company.

With leverage approaching a 20-year high and dividends having to be funded with debt, Telus management has no margin of error.

Yes, this is a stable business. So it's not as speculative as it seems to borrow for dividends and acquisitions.

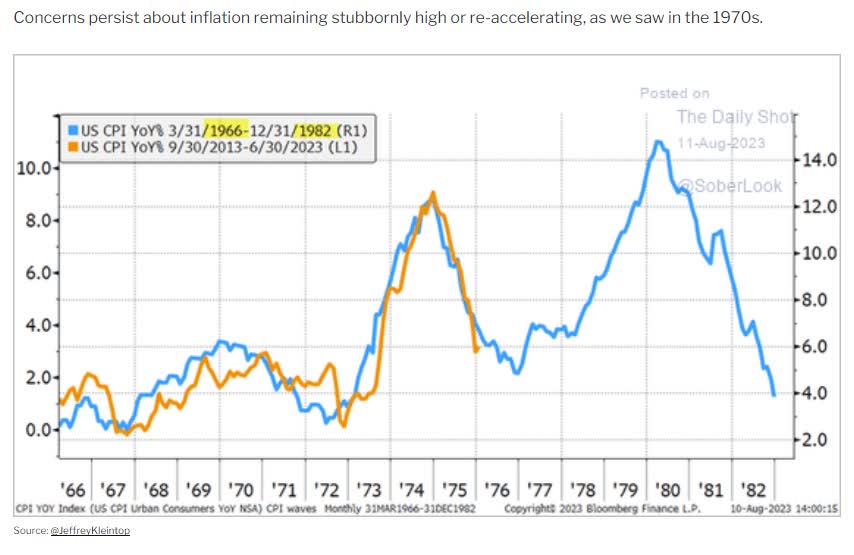

But remember that we're potentially in a higher for longer interest rate world.

{kind=link}

Daily Shot

Is it likely that we get a wage-price spiral like the 1970s that forces the Fed to hike rates to double-digits by 2028? Probably not.

But we can't ignore that we're seeing some strong union pressure resulting in some pretty impressive gains for workers in recent months.

- UPS says drivers to make $170,000 in pay and benefits following union deal

- UAW’s push for higher wages, better benefits could add billions in labor costs

The union’s proposals call for a 32-workweek with 40 hours of pay, pensions extended to all workers, revival of healthcare coverage for retirees, and a 46% wage increase over the contract's life, which would expire on May 1, 2028." - Dallas News

UPS workers just got a contract worth $170K in pay and benefits within a few years.

The UAW is pushing for an extra $80 billion from the big three automakers in a proposed contract to pay each worker $150 per hour in pay and benefits.

The people said that it would increase hourly labor costs to more than $150 per hour at Ford Motor Co. and General Motors Co., including wages and benefits, up from the $64 an hour GM, Ford, and Stellantis NV workers currently make." - Dallas News

$64 per hour is already pretty good money but $150K in pay and benefits would be luxurious given that the average US worker's pay and benefits is $40.78 per hour in June of 2023.

The UAW asks for almost 4X when the big three must spend tens of billions to make the EV transition.

- Ford expects to lose $4.5 billion on EVs this year despite not being able to build enough of them

The current $64 per hour labor costs at Ford (F), GM (GM), and Stellantis (STLA) are already higher than the $55 per hour cost at non-union U.S. assembly plants of Asian and European automakers , an estimated labor cost gap of about $900 million, according to people familiar with Ford’s costs. The people said that labor costs at EV leader Tesla Inc . are even lower, at $45 an hour to $50 an hour . - Dallas News

Tesla (TSLA) investors would be thrilled to see Ford and GM shut down by a strike, ensuring they would struggle to break even on EVs for much of the next decade.

- Automation would have to be cranked up to the next level to support such generous pay packages

Now mind you, this is the UAW's ask. Not likely what they'll get, but the big three could be looking at a nasty strike starting Sept. 14 when the current UAW contract expires.

The largest first-year pay increase from a union contract ratified last year went to a group of 700 pilots for Alaska Airlines subsidiary Horizon Air, who netted a 79.5% wage hike." - Bloomberg

{kind=link}

Bloomberg

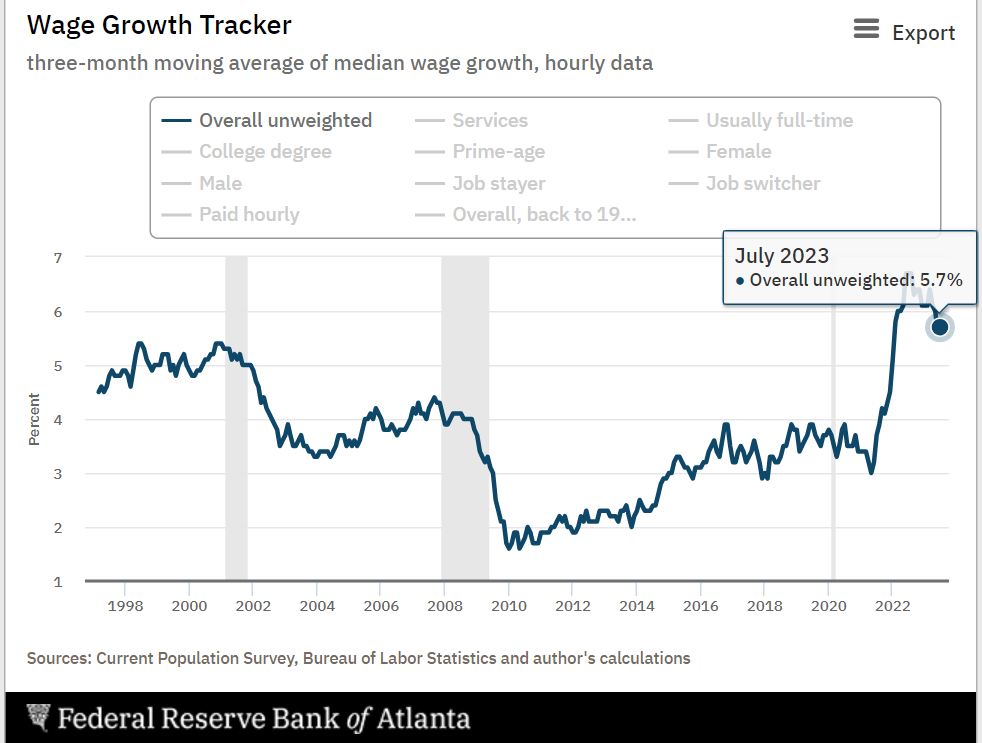

Wage growth is raging for many union workers, which will likely keep pressure on wages throughout the economy.

{kind=link}

Atlanta Fed

The Atlanta Fed's wage tracker is the gold standard of wage tracking because it follows the same cohort of people over time.

It shows that year-over-year wage growth has decreased to 5.7% from 6.7% in July and August 2022.

But here's the problem. Getting to 2% inflation, as the Fed remains committed too, requires either 3.5% wage growth or 3.7% productivity if today's wage growth is to be sustained without triggering elevated inflation.

Is productivity rising? Yes, in recent quarters. And yes, Goldman thinks AI will drive 3% productivity growth long-term and possibly as high as 4.4%.

So theoretically, AI in the coming years might be able to help solve the inflation problem, but until then, we might be left with higher for longer interest rates.

{kind=link}

FactSet Research Terminal

Telus has $1.4 billion in debt maturing by 2025, when rates might be elevated and require it to refinance the current bond yield at 5% to 6%.

Right now, Telus is paying 4.75% average interest costs, and analysts don't expect that to increase much in the coming years... as long as inflation comes down quickly and the Fed is done hiking rates.

Telus Summary

- our quality rating: 75% low risk 11/13 speculative blue-chip

- historical fair value: $17.99

- current price: $16.85

- discount: 6%

- our rating: potential reasonable speculative buy

- yield: 6.5%

- LT growth consensus: 10.5%

- LT total return potential: 17%

- valuation boost for the next decade: 0.6%

- 10-year total return consensus potential: 17.6% = 406% total return

Bottom Line: General Mills Is An Ultra SWAN It's Safe To Buy, But It's Not Exactly Set To Fly

General Mills is a great example of why I use market-determined historical fair values when estimating a company's intrinsic value.

Why was GIS trading at 21X earnings back in May 2023 at its peak? Because companies like PEP, KO, CL, and PG historically trade at 20 to 22X earnings.

Thus, bullish analysts and plenty of investors were saying, "21X for General Mills is fine because that's the industry norm".

Nope, as Ben Graham pointed out, over the long-term, meaning 10+ years, the market is almost always right about a company's fundamentals.

The "weighing machine" of the market says GIS growing at 5% to 6% is worth about 17X earnings, not 21. Anyone who tells you differently is not making a fact-based argument but a speculative one.

If a stable blue-chip with the same basic business model is expected to keep growing at its long-term historical rate, it will likely return to its historical PE. If you want to tell me why GIS will stop trading at 17X earnings and 21X is the "new normal," you better have a good reason.

Is General Mills a value trap? Not at all, it's a 7% undervalued Ultra SWAN that hasn't missed a quarterly dividend payment in 125 years. If GIS ever cuts its dividend, it likely means the world has ended, and we're all too dead to care.

But GIS began overvalued and now has fallen into a bear market that has merely worked off irrational speculative exuberance.

If you want a very safe 3.4% yield with a recession-resistant business model firing on all cylinders going into the 2024 recession? And you're OK with 9% to 11% long-term returns? Then GIS is a potentially good buy.

What about Telus?

Telus is among the more speculative high-yield Canadian dividend blue chips owing to its penchant for aggressive debt-funded M&A and its elevated payout ratio.

As long as things go as analysts and management expect, and Telus' free cash flow explodes higher in the coming years - it should be capable of a safe 6% to 7% growing dividend with a current yield of 6.5%.

That's an extremely attractive proposition to some income investors, highlighting that whatever your risk profile or goals, something wonderful is always on sale if you know where to look.

For further details see:

2 High-Yield Blue Chips At 52-Week Lows Worth Buying