IIPR - 2 Sin Stocks For The Next 5 Years

Summary

- Sin stocks have historically been much more rewarding than regular stocks.

- They commonly trade at discounted valuations, despite enjoying superior fundamentals.

- We highlight 2 opportunities that could potentially triple your money in the coming 5 years.

Sin stocks are the shares of companies that are involved in businesses that may be considered unethical or immoral.

This includes things like adult entertainment, tobacco, weapons, gambling, alcohol, or even pharmaceuticals in some cases. Some famous examples are:

- Altria ( MO ): Tobacco

- MGM Resorts ( MGM ): Casinos

- Diageo ( DEO ): Alcohol

- Smith & Wesson ( SWBI ): Weapons

- Scotts Miracle-Gro ( SMG ): Cannabis

Some investors prefer to stay away from these companies because they are thought to be making money from exploiting human weaknesses and addictions.

But to each their own. Someone may consider a liquor manufacturer to be essential to our society, while someone else may see it as evil. Our objective here is to provide an analysis of investment opportunities based solely on their financial merits, and it happens that sin stocks have a history of generating exceptionally strong returns.

To give you an example: take a look at the performance of tobacco company Altria vs. the performance of the S&P500:

The difference is massive!

How can sin stocks be so profitable?

There are several reasons for this, but the most important ones are probably the following:

- Lower valuations: Since there is less demand for sin stocks, they will commonly also trade at discounted valuations relative to equally strong companies that share similar fundamentals but operate in other sectors.

- Lower competition: Fewer entrepreneurs are willing to do business in these sectors and as a result, there is less competition and better margins for those who take action.

- Recession-resilience: People don't materially change their behavior in a recession. They still want to gamble. They still want to get a drink, etc. In fact, people have historically drunk even more during recessions.

Today, this is well-known to investors, and yet, sin stocks continue to trade at persistent discounts because of the lack of investor demand for them. ESG has only grown in proportion over the years, and it is pushing larger institutional investors away from these sectors.

But if you are fine with some of these businesses, they can be a great source of alpha for your portfolio, and in what follows, we look at two companies that I have been buying lately. I expect them to triple my money in the coming 5 years.

NewLake Capital Partners ( NLCP )

You don't have to invest in a cannabis cultivator or retailer to gain exposure to the sector. Instead, you can invest in a REIT that owns the real estate and rents it out to these cannabis companies.

It is a much safer business because the landlord always gets paid first and without the real estate, there is no business anyway. You need a place to grow and a place to sell the cannabis. Moreover, the landlord typically earns steady rental income from 10+ year-long leases with automatic annual rent hikes and no responsibilities for property expenses, or even the maintenance of the property.

{kind=link}

And since there are few buyers for these properties, they can be highly profitable. Typically, they sell at much higher cap rates and enjoy better leases than other net lease properties. As an example, a cannabis cultivation facility may sell at a 12% cap rate while a FedEx ( FDX ) distribution center may sell at a 5% cap rate.

That makes a big difference and it explains why one of the most rewarding REITs of all time has been a cannabis REIT. Here are the returns of Innovative Industrial Properties ( IIPR ), the first cannabis REIT to IPO, up until the recent market sell-off:

YCHARTS

It multiplied investors' money by nearly 20x in just 5 years and handily beat the S&P 500 ( SPY ) and the broader REIT market ( VNQ ).

The returns were so massive because:

- It was buying properties at high cap rates, resulting in a large spread over its cost of capital.

- It was one of the few buyers with access to cheap public capital.

- It was fairly small in size and therefore, new acquisitions really moved the needle.

Today, we remain bullish on IIPR, but it is getting larger in size, which means that it will get harder for it to grow. It has also recently run into some tenant issues, which will slow down its future growth even further.

But a new Cannabis REIT recently IPOed and it is set to replicate what IIPR did in its early years. Its name is NewLake Capital Partners, it IPOed last year, and it is still small in size with a $350 million market cap.

It is growing rapidly as it acquires new properties. Its cash flow per share grew by 43% year-over-year in the second quarter. The growth should be even stronger in the second half of the year as the company just closed two major acquisitions.

What's more, its credit facility was recently tripled in size to $90 million, which should enable NLCP to continue making highly accretive investments in Q3 and Q4.

Despite that, NLCP is priced very cheaply, offering a 9% dividend yield, which is quite exceptional for a company that's growing at this pace.

Assuming that they can keep growing rapidly, and eventually also experience some multiple expansion, NLCP could triple your money in the next 5 years. That's actually far short of IIPR's 17x in its first 5 years.

What's the main risk? Cannabis tenants are more speculative than average. Fortunately, NLCP only focuses on limited-license states, and it is yet to suffer any rent delinquencies. Will this last? Likely not. When you invest in a higher-risk sector, it is inevitable to also occasionally suffer setbacks, no matter how good you are at underwriting properties. Investors should be aware of this and be prepared for some volatility along the way.

RCI Hospitality ( RICK )

I like to think of RCI Hospitality as a real estate investment firm that buys and manages strip clubs. It is not officially a REIT, but it is similar to a hotel REIT in the sense that it buys the real estate and then operates the properties.

But while a hotel REIT may buy a hotel at a 6% cap rate, RICK is buying strip clubs at a 25-33% EBITDA yield. It is getting these incredibly high returns because they are very few buyers for strip clubs.

If you are a wealthy local business owner, your wife or husband probably does not want you to buy the local strip club, and if you are a private equity firm, you surely have some investors that would prefer you to stay out of this business. In that sense, RICK is filling a void in the market by providing much-needed capital to strip club owners, and it is getting richly rewarded for it.

RCI Hospitality

A lot of club owners are in their 50s and 60s and are looking to retire, providing many acquisition opportunities for RICK to consider.

They have already acquired 15 clubs in 2022, and they expect to buy many more in the coming quarters.

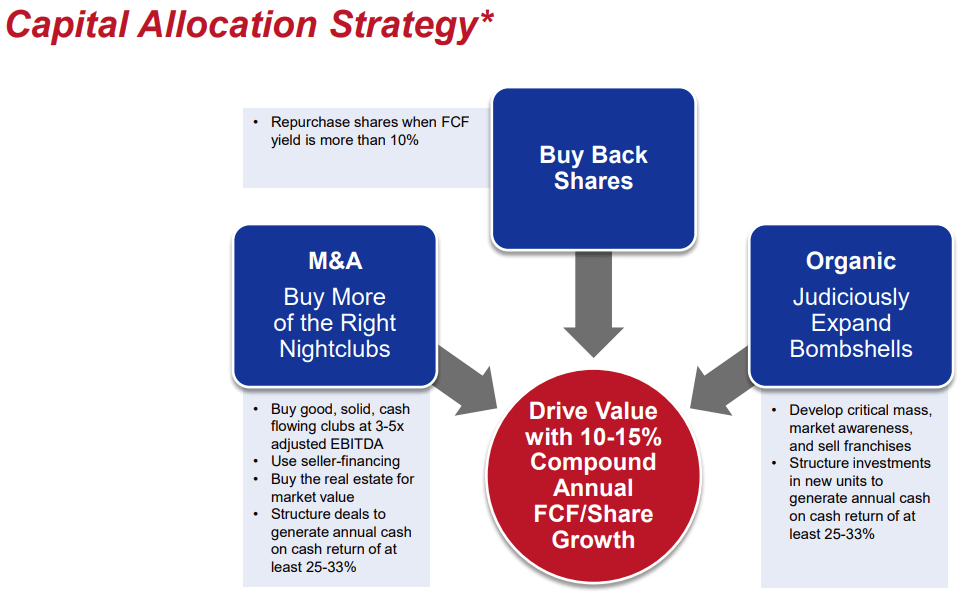

What's more is that the management is extremely good. They are laser-focused on growing the free cash flow ((FCF)) on a per-share basis and have a clear capital allocation policy to achieve that:

{kind=link}

In a recent interview on Barstool Finance, the CEO, Eric Langan, noted that they expect to grow their FCF per share by 30% in 2022, and he thinks that they will likely grow by another 30% in 2023.

Yet, the company is priced at just around 10x FCF. How many companies do you know that are so cheap and growing so rapidly?

This is one of my largest positions and I expect it to more than triple my money in the coming 5 years as the company keeps growing at 20%+ per year and experiences some multiple expansions as it gets larger and more investors take notice of it.

What's the main risk of RICK? I think that it is the risk of strip clubs losing in popularity in the long run. This is already happening for some lower quality clubs, but in a weird way, this may actually even benefit RICK since it focuses on the highest quality clubs, which are then affected by less competition. I don't see the highest quality clubs going anywhere, but this is the biggest risk to keep an eye on.

Bottom Line

Historically, sin stocks have greatly outperformed the rest of the market. But to be fair, some of them are also quite a bit riskier than the average stock.

Personally, I like to invest in real estate heavy sin stocks like NLCP and RICK because it adds an element of safety to them.

Cannabis cultivation facilities enjoy high barriers to entry and generate steady cash flow from long-term leases.

Strip clubs enjoy even greater barriers to entry since they require licenses that are today almost impossible to obtain and their cash flow is recession-resistant as people drink more and still want an escape during recessions.

Priced at low valuations, and growing rapidly, I believe that both companies are very likely to generate rich returns in the coming 5 years.

For further details see:

2 Sin Stocks For The Next 5 Years