CA - 2024: A Rotation Out Of The Magnificent 7

2023-11-27 07:00:00 ET

Summary

- Big Tech wiped out nearly $4T in market value in 2022 but has rallied back strong in 2023, with the Magnificent 7 paving the way.

- The Mag 7: Apple, Microsoft, Amazon, Nvidia, Meta, Alphabet, and Tesla, account for nearly ? of the S&P 500, +44% of the Nasdaq 100, and ~20% of the MSCI World.

- Despite strong Q3 earnings results, valuations of the Magnificent 7 are severely stretched. Through October, the Mag 7 forward P/E was 29x vs. the S&P 500 at 19x.

- Using SA’s Quant Rating System, I’ve identified Strong Buy-rated stocks separated from weak stocks using powerful signals to help investors minimize risk and maximize returns.

Nearly one-fifth of the global stock market ( URTH ) and nearly one-third of the S&P 500 accounts for the Magnificent 7: Apple ( AAPL ), Amazon ( AMZN ), Alphabet ( GOOG ) ( GOOGL ), Meta ( META ), Microsoft ( MSFT ), Nvidia ( NVDA ), and Tesla ( TSLA ).

As of November 22nd, all Magnificent 7 stocks reported top-and-bottom-line earnings beats, with Tesla as the only outlier – falling short. The Magnificent 7 are some of the biggest names in technology. Driven by high-end software and hardware, cloud computing, and the AI boom, these seven megatech names lead the charge. In addition to their demand as technology advances, challenging macro and geopolitical tensions prompt investors to flock to companies considered “safe.” Given their size, cash balances, and overall strength in company fundamentals, investors like the feeling of safety during periods of economic uncertainty. The Mag 7 offers steady product demand, monetizing and upselling customers on diversified products and services, and being ahead of the pack regarding innovation, customer loyalty, engagement, and security. With each Magnificent Seven capitalizing on some level of AI advancement within their businesses, artificial intelligence serves as a revenue generator for these large-growth companies. Where most have benefitted, Tesla fell short in Q3, given its investment in a Cybertruck which Elon Musk says ,

“We dug our own grave with the Cybertruck. "Cybertruck’s one of those special products that comes along only once in a long while. And special products that come along once in a long while are just incredibly difficult to bring to market, to reach volume, to be prosperous."

In 2022, the performance narrative for the 'Magnificent 7' was completely different from the performance that transpired in 2023. Post-pandemic, these stocks experienced a sharp sell-off as investors, fearing a severe recession, liquidated major positions to generate cash. However, in 2023, with clearer insights into inflation and unfolding global conflicts, and following a previous year that saw a $12 trillion wealth wipeout with Big Tech accounting for over $4 trillion in market cap losses , investors sought safety, leading to increased inflows into mega tech stocks. Also, these Mega-Tech companies were at the forefront of AI innovation. This desire for security, combined with the appeal of AI, sparked a significant rally in these seven stocks. Looking ahead, this level of performance seems unsustainable as investors begin to recognize the overstretched valuation framework of these stocks. Most indexes have doubled since early 2018, with Apple and Microsoft maintaining the largest weights.

Historical Weights of Magnificent 7 and US Concentration (Qontigo.com)

The Magnificent 7 experienced a run-up of nearly 99% as of November 10th, and hedge fund positions in mega-cap tech are back to record highs.

Investor Big Tech inflows are back at record highs (Goldman Sachs)

Over the last few weeks, the seven behemoths drove a $2T rally to fend off a Nasdaq correction . Recouping their losses from 2022 and then some, the Magnificent Seven stocks versus the major index total returns are substantial. The S&P 500 gained +18% YTD year-to-date, but “There continues to be a divergence between the magnificent 7 and the rest of the market,” said Jason Benowitz, senior portfolio manager at CI Roosevelt. “There’s definitely a question as to whether or not there will be a catch-up and how it would occur.”

Magnificent 7 inflows and major indices % change in total return

Magnificent 7 inflows and major indices % change in total return (YCharts)

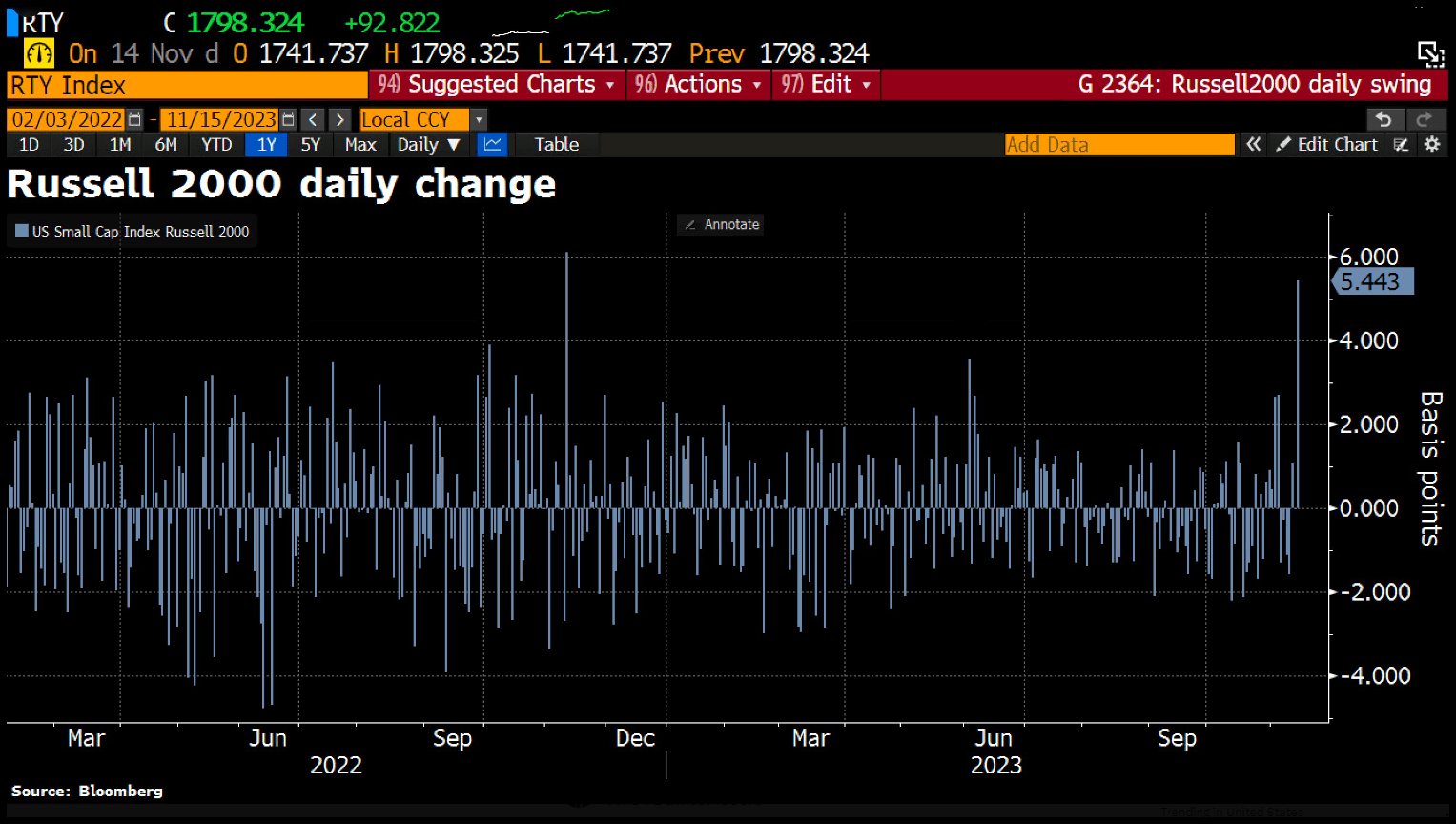

Whether the rally is sustainable remains to be seen. But the Russell 2000 index is seeing inflows as investors continue betting on the Fed’s response to interest rates and monetary policy.

Russell 2000 sees an uptick in daily inflows

Russell 2000 sees an uptick in daily inflows (Bloomberg, Holger Zschaepitz Twitter)

{kind=link}

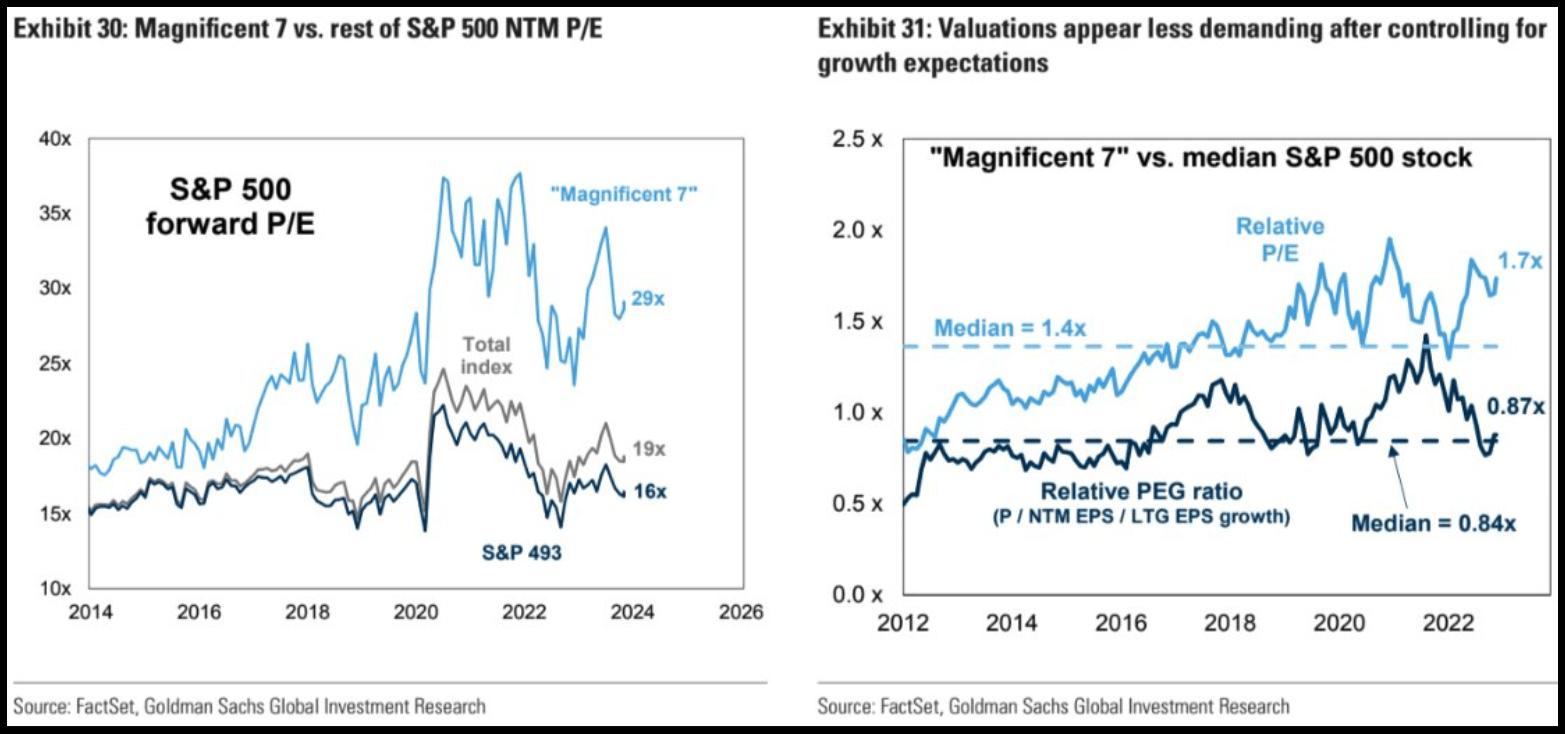

Based on the sales growth and data from FactSet and Goldman Sachs Global Investment Research, the Magnificent 7 is projected to outpace the S&P 500 despite deteriorating conditions. Regardless of the performance of the Mag 7, we may see a reversion into the forgotten asset classes like small- and equal-weight stocks.

Magnificent 7 growth expected to outperform the S&P 500

Magnificent 7 growth expected to outperform the S&P 500 ( FactSet, GS Global Investment Research, Kurt S. Altrichter Twitter)

Should this occur, I’ve identified five Strong Buy-rated stocks using SA’s Quant Rating system. Each stock possesses strong fundamentals, offers diversification into varied industries and they are significantly undervalued compared to the Mag 7, offering potential upside.

2024: Economic Outlook

Economic growth advanced strongly in the latest quarter to 4.9%, and as of November both investors and consumers have shrugged off Fed hikes. Despite recessionary fears in 2023, the Fed made strides towards a soft landing, defying the odds with better-than-anticipated GDP and tech rallying for major index gains.

Although the Fed projects 1.5% U.S. GDP growth in 2024, many economists are still concerned that stronger growth and sticky inflation could lead to elevated rates longer than the market anticipates. With inflation above the Fed’s 2% long-term target, it's uncertain whether we’ll see an inevitable recession in the near term or later in 2024. Given the ‘higher for longer’ mantra, spiking yields dragged the broader stock market and stock price performance down, to at best flat, for many companies through July 2023.

Magnificent 7 is extremely overvalued compared to the market

Magnificent 7 is extremely overvalued compared to the market (Bloomberg, Bernstein Analysis)

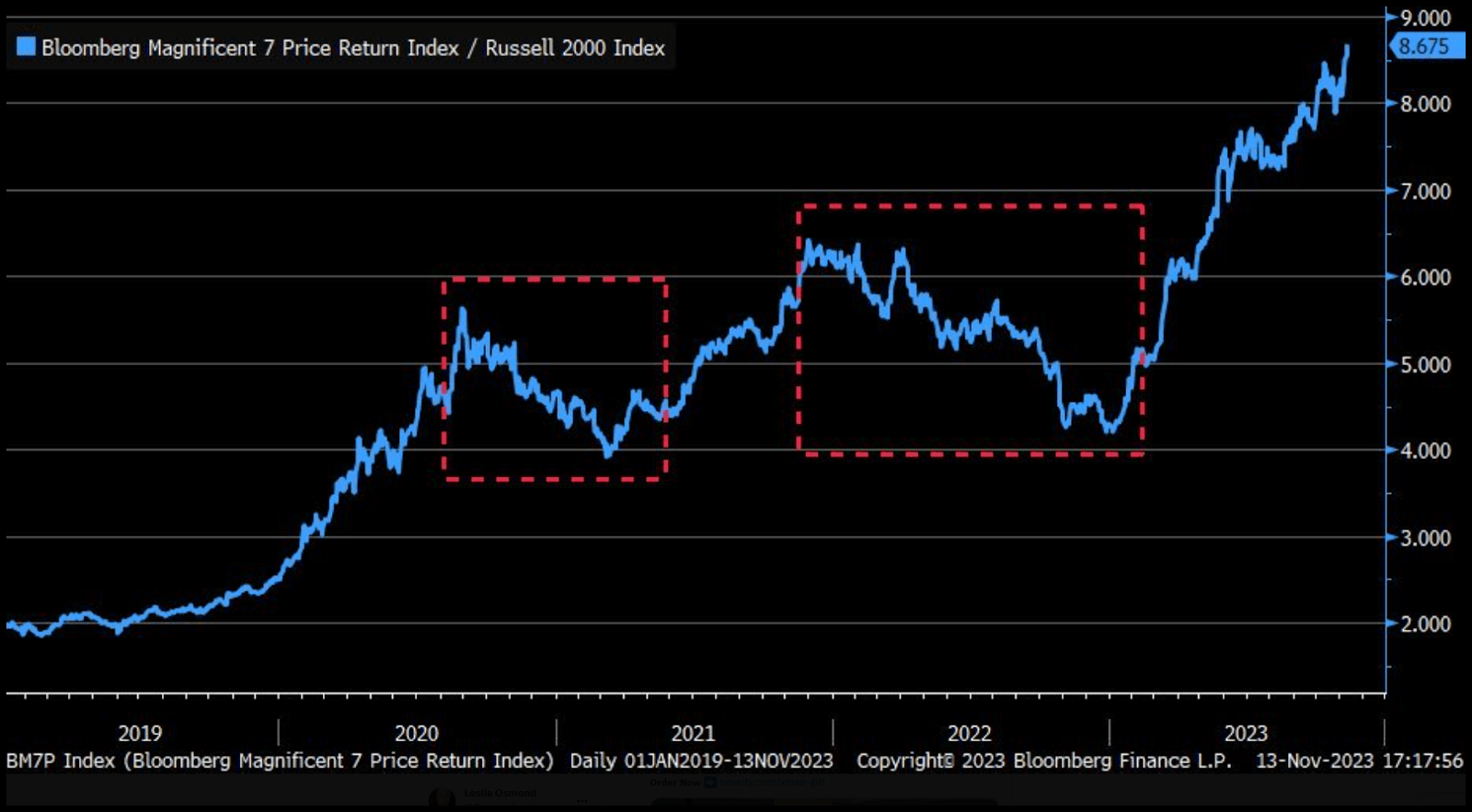

Looking at the implied “fair value” of the Magnificent 7 compared to the rest of the market, it’s clear the largest constituents of the S&P 500, Big Tech, are highly overvalued. Although the Magnificent 7 drew considerable investor interest this year, a change in this trend could occur. The latest price movements of the Russell 2000 Index suggest that a market rotation might be in progress. With Big Tech witnessing significant gains, the Magnificent 7 might see a reversal in their fortunes, potentially lagging behind small-cap stocks.

Magnificent 7 Could Underperform Small Caps in 2024

Magnificent 7 Could Underperform Small Caps in 2024 (Liz Sonders, Bloomberg)

{kind=link}

Where FAANG stocks have been household names, evolving as tech advancements and AI propel them forward, through November, more than 82% of S&P 500 companies exceeded earnings growth expectations, which is above the 77% five-year average. Nvidia has been one of the biggest catalysts for tech, crushing Q3 earnings . Year-to-date, the seven mega techs have seen a serious run-up.

-

Apple: +53% YTD

-

Microsoft: +57 YTD

-

Amazon: +70% YTD

-

NVIDIA: +252% YTD

-

Alphabet: +52% YTD

-

Alphabet: +53% YTD

-

Meta: +172% YTD

-

Tesla: 117% YTD

But, we’re seeing signs of wavering, as the market reacted positively to the Fed’s pause, a cooling labor market, with hopes of more dovish behavior. Christopher Wood, Head of Global Equity Strategy at Jeffries, writes :

It is the delayed but ongoing impact of monetary tightening which represents the greatest risk to risk assets, with the greatest risks facing the formerly booming world of private equity and the still booming world of private credit…the relevant seven companies [generate] on average 53% of their revenues from outside America. Still, at some point, even their valuations should become vulnerable to the impact of monetary tightening.

When you factor in the premium investors pay for the Magnificent 7 - versus stocks that offer just as attractive metrics, but without the premium price tag - you may be missing out on the significant upside.

The Magnificent 7 are highly overvalued compared to the total index

The Magnificent 7 are highly overvalued compared to the total index (FactSet, Goldman Sachs Global Investment Research)

{kind=link}

Seeking Alpha’s Quant Ratings and Factor Grades System showcases stocks with the collective shared traits of value, growth, profitability, rising earnings revisions, and momentum that are best equipped to withstand volatility. Whether we experience a recession in 2024 or not, using a data-driven process that relies on the statistical measurement of a stock’s financial metrics and scoring how it compares to the sector can offer great insight when selecting stocks as potential diversifiers out of the magnificent 7. I have selected five stocks in varied industries that have performed well in 2023, possess excellent factor scores, and maintain bullish momentum. While past performance does not guarantee future results, check out our top five stocks for a possible rotation out of the magnificent 7.

5 Stocks to Buy

This year’s stock market rally has been a story of the Magnificent 7, whose year-to-date performances have lifted the S&P 500 by 18%. When selecting stocks in a rising rate environment, my picks are unique and offer diversification, especially given the extreme concentration of Big Tech in indexes. Consider five alternative stocks for diversification with strong quant ratings for a rotation out of Big Tech.

1. Abercrombie & Fitch ( ANF )

-

Market Capitalization: $3.64B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 11/21/23): 1 out of 539

-

Quant Industry Ranking (as of 11/21/23): 1 out of 41

Black Friday has come and gone as we enter the shopping season, and what better stock to kick off the holidays than apparel? Heavily branded clothing retailer Abercrombie & Fitch ( ANF ) peaked in 2007 and has since made a tremendous comeback. Strong supply chain and sales growth, lowering inventories and freight costs, are helping drive a healthier, more profitable business, as showcased in ANF’s consecutive earnings beats.

ANF Stock Growth & Profitability

Despite announcing a Q3 top-and-bottom-line earnings beat that included a net sales increase of +30% year-over-year, Abercrombie slumped 8%, likely due to investors taking profits given the stock is trading at multi-year highs.

“Entering the important holiday season, our fiscal 2023 year-to-date results give us the confidence that we can continue to deliver for our customers and drive profitable growth,” said CEO Fran Horowitz.

Abercrombie has a strong balance sheet, raised guidance, and anticipates operating margins of nearly 10% versus the previous 8% to 9% and net sales growth of 12% to 14%. Abercrombie’s brand strength has allowed the retailer to soar to 52-week highs despite potential consumer spending headwinds and economic uncertainty. Abercrombie’s focused brand growth and ability to leverage a transformed operating model has resulted in growth and a long-term target of $5B in revenue and +10% operation margins for 2025.

ANF Stock 2025 Targets (ANF Q3 Investor Presentation)

Abercrombie’s Quant Factor Grades, which rate investment characteristics on a sector basis are highlighted below. Abercrombie was picked as an Alpha Pick on October 2, 2023, and has had an incredible 26.23% return since selection into the portfolio.

ANF Stock Factor Grades

ANF Stock Factor Grades (SA Premium)

Abercrombie’s growth, profitability, and revision grades indicate it has excellent potential and is fundamentally sound compared to the sector. Abercrombie’s B- profitability grade comes with a 59% gross profit margin ((TTM)) and more than $473M in cash from operations. Although the stock’s D+ valuation is a bit stretched, it possesses an ‘A+’ growth grade, A+ momentum, and eight upward earnings revisions, showcasing this fast-growing company compared to its sector.

ANF Stock Valuation & Momentum Grades

Abercrombie comes at a premium. Reviewing its underlying valuation metrics showcases some attractive discounted figures, including forward EV/Sales of 1x versus the sector’s 1.15x and forward EV/EBITDA figures, a -18% difference from the sector. Where ANF is trading at its 52-week high, +291% over the last year, one of the most common questions I receive is: Why pick a stock that’s rallied to highs?

Annualized Return of US Stocks by Price Momentum (AQR and Kenneth R. French Data Library)

The case for momentum investing highlights the false theory that if a stock is at its 52-week high, it is overbought, and if it is at its 52-week low, it is an excellent value. While momentum is only one factor employed by Alpha Picks, studies have distinguished the winning strategy between 52-week highs and lows. When stocks go up, they’re likely to keep going up, versus being able to catch a falling knife when stocks go down unless you can nail the inflection point. That said, I have another well-known retail stock offering tremendous fundamentals and diversification outside of the Mag 7, yet it is trading at its 52-week high. ANF is the #1 ranked company in the consumer discretionary and apparel retail industries. There are many other Top Ranked Consumer Discretionary stocks if you want to look beyond the retail industry.

2. The Gap, Inc. ( GPS )

-

Market Capitalization: $6.82B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 11/21/23): 2 out of 539

-

Quant Industry Ranking (as of 11/21/23): 2 out of 41

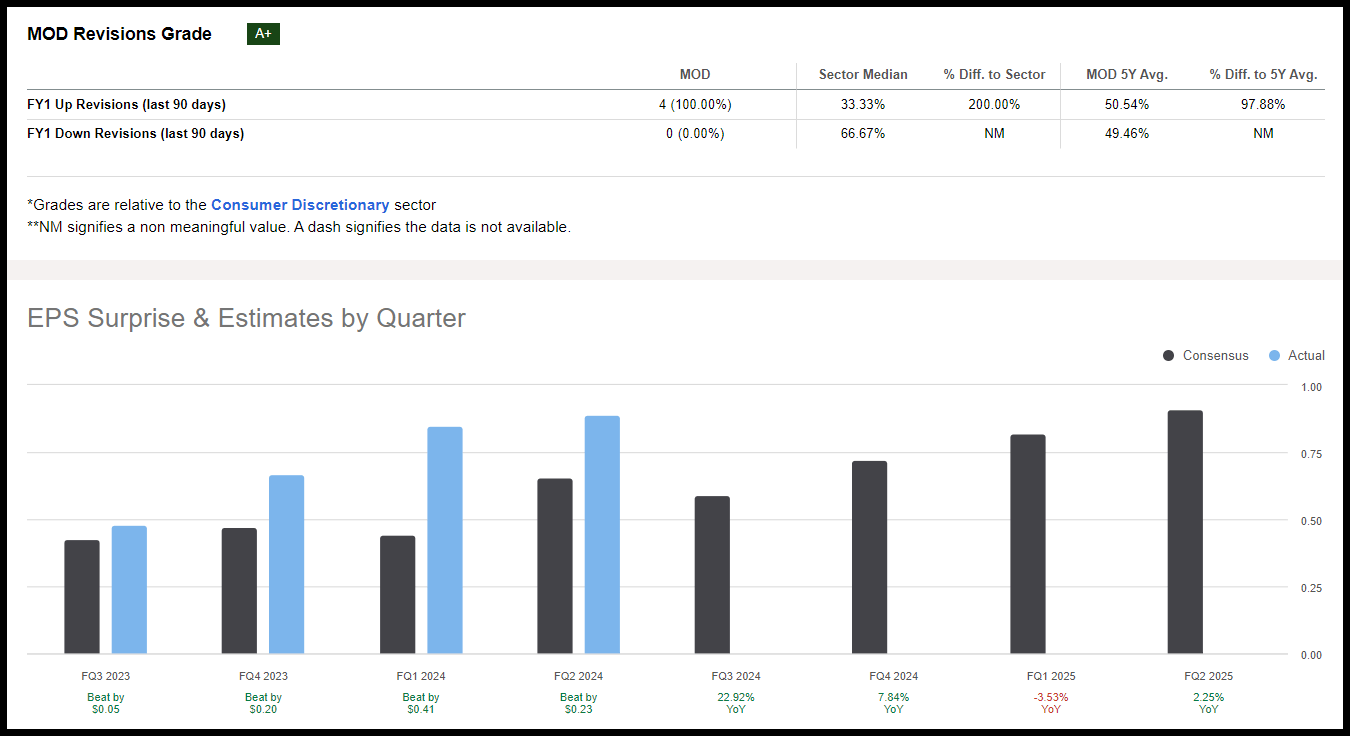

Where Abercrombie is the #1 ranked Consumer Discretionary and Apparel Retailer, its competitor, The Gap ( GPS ), is second. Surging 30% after crushing Q3 earnings, the retailer’s improving margins and inventory positions prompted a lift to other mall retailers . Gap has done incredibly well, with three consecutive earnings beats, resulting in 14 Fiscal Year analyst upward revisions over the last 90 days with zero downward.

GPS Stock Revisions Grade (SA Premium)

The Gap Stock Growth & Profitability

A strong balance sheet, better-working capital, and focus on operations efficiencies have allowed the Gap to improve margins, expenses, and cash flow. Despite revenue being down nearly 7%, gross margins expanded by 260 basis points in the quarter. EPS of $0.59 beat by $0.39 and revenue of $3.77B beat by $157.50M. As expressed by Gap CEO Richard Dickson during the Q3 Earnings Call :

“Gap brand, as you know, has tremendous heritage as a pop culture brand that delivers, leads trends, [and] celebrates individuality and self-expression. The brand enjoys 90% brand awareness among U.S. consumers,” which is why the company is placing a strategic focus on reigniting big ideas and championing originality, especially online to further reignite the iconic brand.

The $544M YTD cashflows have been strong and important in returning cash to shareholders in the form of dividends throughout the year. Given consumer trends, mixed economic data, and potential slowing sales and growth into 2024, The Gap is at high risk of cutting its dividend, as showcased in the Quant Warning Banner .

The Gap has indicators of a stock at risk of cutting its dividend.

The Gap has indicators of a stock at risk of cutting its dividend. (SA Premium)

Stocks that historically show signs of potential cuts possess weaker Dividend Safety grades. Over the past 11 years, 64.4% of stocks with an F Dividend Safety rating cut their dividend. Does this mean you should sell the stock? Not necessarily. It means you should be careful about relying on a company’s dividend for your income if its grades are less than ideal. Sometimes, when a company cuts its dividends, the saved cash returns to the company, which can be positive for the stock. The Gap’s dividend scorecard below highlights my dividend Quant grades based on Dividend Safety, Dividend Growth, Dividend Yield, and Consistency.

The Gap stock has a weak dividend safety rating.

The Gap stock has a weak dividend safety rating. (SA Premium)

GPS Stock Valuation

GPS is up more than 65% YTD and more than 30% over the last year. While still trading at a relative discount, The Gap’s forward PEG of 0.34x versus the sector median of 1.53x is more than a 77% difference to the sector. Additionally, forward EV/Sales are a -35% difference, and the stock’s Price/Cash Flow is very attractive. With bullish momentum allowing the stock’s price performance to significantly outperform its peers quarterly, consider this stock for a portfolio.

3. Celestica Inc. ( CLS )

-

Market Capitalization: $3.36B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 11/21/23): 3 out of 566

-

Quant Industry Ranking (as of 11/21/23): 1 out of 18

Like Big Tech, many smaller companies want in on the action and cutting-edge support offered by artificial intelligence ((AI)), Machine Learning ((ML)), and data center connectivity for the future. A leader in supply chain solutions, Celestica Inc. ( CLS ) offers global expertise at every stage of product development. One of the largest electronic manufacturing services ((EMS)) and tech IPOs in Canada’s history, the stock is +137% YTD and +143% over the last year.

CLS Stock Valuation & Momentum

Offering tremendous valuation grades, CLS trades at an extreme discount, as shown in its ‘A-’ valuation grade, despite nearing its 52-week high. CLS’ forward P/E ratio of 11.96x is a 47% difference to the sector, and its all-important forward PEG is more than a 65% difference.

CLS Stock Valuation Grade (SA Premium)

As displayed in incredible quarterly price performance, its six-month 134% run-up is more than a 788,000% difference to the sector, and over one year, it beats its peers by more than 4,380%. As mentioned earlier, the case for momentum investing is strong. Just because a stock’s price has risen to 52-week highs doesn't mean that the stock has gotten more expensive; the factors have changed. A stock’s earnings may have increased 2 times, but the stock is only up 50%, or earnings increased 4 times, and the stock is only up 2x. A stock can be cheaper than it was but in a better position and should be revalued higher. Renowned stock investor and advisor Marty Zweig’s number one rule was, “The trend is your friend. Don’t fight the tape.” His second rule is “The cheap get cheaper, and the dear get dearer.” Given CLS’ incredible momentum and undervaluation, let’s dive into growth and profitability. In the case of CLS, the Value grade is now A- vs. 3 months ago, it was an A. The stock is up almost 30%, but the valuation is the same. Conversely, the Growth grade is now B, and 3 months ago, it was B+. Both growth and value have been lock-step while the price has appreciated.

CLS Stock Growth & Profitability

Another of my Alpha Picks, Celestica Inc., reported tremendous earnings beats for Q3, marking eight consecutive top-and-bottom-line beats. With an EPS of $0.65 beating by $0.05 and revenue of $2.04B beating by $52.78M, the company anticipates continued revenue growth across each of its businesses, despite anticipating "a negative $0.15 to $0.21 per share (pre-tax) aggregate impact on net earnings on an IFRS basis" in Q4. Although the stock has faced macro headwinds, Celestica benefits from tailwinds that include robust demand from its core CCS division, whose end market is Hyperscale Cloud Platforms, and is expected to grow at a CAGR of 37.8% and is +10% sequentially As the demand for advanced computer capacity to support AI and machine learning expands, the outlook for Celestica continues to be positive.

ATS and CCS Revenue and Profitability by Segment

ATS and CCS Revenue and Profitability by Segment (CLS Q3 2023 Investor Presentation)

Overarchingly, the company is performing well, as highlighted by RBC Capital’s upgrade earlier this year. Seven Wall Street analysts have revised estimates over the last 90 days, and as fellow Seeking Alpha analyst Thomas Potter highlights , Celestica is a hidden gem in the tech industry. If you are looking for an information technology stock outside of Canada, here are the top-ranked IT Stocks .

4. Dorian LPG Ltd. ( LPG )

-

Market Capitalization: $1.73B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 11/21/23): 1 out of 237

-

Quant Industry Ranking (as of 11/21/23): 1 out of 56

With its subsidiaries, Dorian LPG Limited ( LPG ) is the Quant Strong Buy-rated energy company you didn't know you wanted to own! Through its tankers, LPG is the leading owner and operator of very large gas carriers, “VLGCs,” which capitalize on transporting liquefied petroleum gas. Owning a fleet of 25 modern VLGCs, LPC offers safe, reliable transportation worldwide.

LPG Stock Valuation

LPG’s discounted valuation is highlighted by a forward P/E ratio of 5.17x versus the sector’s 10x, nearly a 50% difference. Additionally, its trailing PEG of 0.04x is more than a 76% discount to the sector. Despite a one-year run-up of 132%, Dorian LPG continues to be on an uptrend.

Dorian LPG Ltd ( LPG ) 1-year Trading Chart

Dorian LPG Ltd (LPG) 1-year Trading Chart (SA Premium)

The tight oil market with high gas prices has helped LPG’s momentum, and undervalued, LPG poses a unique buying opportunity going into 2024, especially considering its strong fundamentals, growth, and profitability.

LPG Stock Growth & Profitability

One of the highest-yielding dividend stocks according to SA’s Quant Ratings, Dorian LPG’s 9.36 dividend yield ((TTM)) coupled with a B- Safety grade make it attractive for investors looking to hedge against inflation. Although the company missed second-quarter earnings, LPG stock more than doubled in value over the last 12 months. LPG’s average Time Charter Equivalent (TCE) rates increased by $24,496 per operating day from $40,632, and shares of the stock rose more than 10% following a Jefferies upgrade from Hold to Buy, along with raised price targets.

We are raising our VLGC rate forecast to $75,000/day for 2024, up from $45,000/day. This boosts our Dorian EPS estimate for next fiscal year to $8.67 from $3.68 (consensus is $4.02). Over the next four quarters, we project $10/sh of FCF generation. Even assuming a conservative 20% target FCF yield would give Dorian an upside to $50.

LPG Stock Profitability Grade (SA Premium)

Despite the top-and-bottom-line earnings misses, analysts continue to review estimates up, with zero downward revisions. The company’s Growth Grade and Profitability Grade are very strong, showcased in forward and year-over-year revenue growth, a 93.54% EBITDA Growth (YoY), and tremendous margins. Dorian is our #1 ranked energy stock, but it has a smaller market cap at $1.7BN. If you are looking for an Energy stock on the larger side, here is a ranked list of the Top Energy Stocks . Consider this stock for a portfolio, along with my final pick, Modine Manufacturing.

5. Modine Manufacturing Company ( MOD )

-

Market Capitalization: $2.71B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 11/21/23): 3 out of 539

-

Quant Industry Ranking (as of 11/21/23): 1 out of 36

Despite the cyclical nature, supply chain disruptions, and headwinds the auto industry faces, Modine Manufacturing Company ( MOD ) is an operationally efficient provider of heat transfer systems and components. Supplying multiple segments in the automotive industry, Modine’s customers include HVAC, Commercial Electric Vehicles, Data Centers, and more. Focused on sustainability, MOD has pushed the tech boundaries to increase profitability while solving thermal issues. Demand for EVs and autonomous vehicles has allowed Modine to develop smart electric products, heat and cooling packages, and comprehensive tools for monitoring the status of thermal systems. Another one of my Alpha Picks, MOD, has returned over 150% since its selection into the Alpha Picks portfolio on December 22, 2022, Modine continues to crush performance, as evidenced by its earnings surprises and analyst upward revisions.

MOD Stock Revisions & EPS (SA Premium)

{kind=link}

Modine Manufacturing Growth

Evolving technology, AI, and emphasis on climate solutions have provided tailwinds for the growing company. Modine has experienced tremendous margin expansion, sales growth, and debt reduction over several quarters.

Despite economic uncertainty, Modine’s focus on building an M&A pipeline and improving its performance technologies and climate solutions resulted in another earnings beat. Q2 EPS of $0.89 beat by $0.23 and revenue of $620.50M beat by $4.33M. Additionally, MOD ported adjusted EBITDA OF $81.2m, a 59% increase from the previous year. EBITDA margin saw a 430-basis point improvement for the same period, and as the company focuses on organic and new growth,

“Our commercial team continues to win orders with key relationships in our pipeline and add new opportunities to the sales funnel as we evaluate and develop high-quality prospects. Our goal is not to be a high-volume products part of the data center market. Instead, we’re focusing on relationships with key customers, supporting them with system solutions and ongoing services as they grow globally,” said Neil Brinker, Modine President & CEO.

Continuing to expand its manufacturing presence, this strong quantitative buy plays a growing role in the electrification of commercial vehicles while trading at a very attractive price.

MOD’s Valuation

Modine Manufacturing stock comes at a good value, even with its stock price up more than 156% YTD and +147% over the last year. Quant-rated a strong buy with a C- valuation grade and trailing P/E GAAP at 13.39x compared to the sector at 15.94x, MOD is undervalued. Over the last 3-months, despite the 20% surge in the stock price, the Value and Growth grades are almost unchanged. The trailing PEG ratio has a B+ grade, trading more than 66% below the sector. Given the stock is on an uptrend, as evidenced by its A+ momentum grade and upwards-sloping 200-day moving average, healthy tailwinds, and volume growth into FY24, support this buy at a discount, along with each of my other picks when compared to the extreme premium price tag of the Magnificent Seven. There are several other Top Consumer Discretionary stocks that are attractive alternatives to the Mag 7.

Conclusion

Despite potential economic slowdown and recession concerns for the new year, S&P 500 companies have exceeded earnings expectations, including six of the Magnificent 7. Fear can make it difficult for investors to rotate completely away from companies they consider “safe,” especially those comprising substantial weights in major index funds. Strong balance sheets, overall fundamentals, and ability to weather economic storms and contractions are why investors prefer the Magnificent Seven compared to lesser-known companies with less cash and earnings pressure.

But many lesser-known companies with tremendous fundamentals are trading at a discount. For investors wanting to rotate out of the Mag 7 for diversification, consider the five strong Quant buys stocks: ANF, CLS, LPG, GPS, and MOD.

Magnificent 7 has a premium valuation (LPL Research)

Although Top Technology stocks are attractive, we could see a rotation into smaller companies, as demonstrated recently by the Russell 2000. Investors want stocks with robust fundamentals that can deliver results, offer tremendous valuations with better growth rates, showcase profitability metrics, rising earnings revisions, and strong fundamental tailwinds. We have many stocks with strong buy recommendations and larger market caps that can be found using Stock Screens to suit your specific investment objectives. Browse our Top Rated Stocks . Alpha Picks might be ideal if you're interested in a monthly selection of the top 'strong buy' quant stocks, limited to just two top ideas each month. Seeking Alpha’s quant ratings and investment research tools help to ensure you are furnished with the best resources to make informed investment decisions while taking the emotion out of investing.

For further details see:

2024: A Rotation Out Of The Magnificent 7