XLY - 3 Deep Value Speculations Income Investors Should Love

2023-08-10 10:40:28 ET

Summary

- Kraft Heinz is experiencing a turnaround and is on track for growth with improved profitability and margin improvement.

- Kohl's turned a corner in 2023 and is on track to improve profitability.

- Verizon is deeply undervalued and offers an 8% yield that may be too good to pass up.

The market hasn't been kind to some of the best-yielding stocks available to investors today. Kraft Heinz ( KHC ), Kohl's ( KSS ), and Verizon ( VZ ) face their share of headwinds like any other company in business today, but they are all navigating the economic conditions well. In all three cases, the stocks are trading at a deep value relative to their past performance and the broad market while paying above-average yields. The lowest yielding is Kraft Heinz at 4.5%, and the highest, Verizon, is nearly double, and all have higher share prices in the not-too-distant future.

Kraft Heinz Turnaround Gains Momentum

Kraft Heinz is deep in a turnaround that has begun to gain traction. The company divested significant portions of the old business to raise capital, shore up the balance sheet, and position for growth, and growth is back on the table. The latest quarterly report is mixed regarding the analysts' expectations but reveals solid execution and pricing power. The company experienced some elasticity but not enough to offset the 11% increase in average pricing. Gains were made in all segments, and the strongest was International, up 8.5%, as growth efforts began to impact results.

More importantly, the company widened the gross and operating margin on a GAAP and adjusted basis to deliver better-than-expected earnings. Earnings outpaced consensus despite top-line strength, leaving the adjusted EPS up more than 1000 basis points better than revenue. The takeaway is that efforts to improve profitability while growing are paying off, no pun intended, and have the company set up for leverage when economic conditions turn.

There is no doubt that Kraft Heinz shares deserved their fall from grace in 2018, but that was then; this is now. Now the company is on track to grow organic revenue by mid-single digits this year and similarly next year, with margin improvement to go along with it. That's good news for the dividend. The 4.5% payout is steady, and the company may resume distribution growth in the future.

While still faced with hurdles, the Kraft Heinz margin improvement helped fuel a significant increase in FCF that will aid growth efforts, margin improvement, cash flow, and distribution payments over the next few years. And the stock trades at a value of only 12X earnings which is ultra-low for a Consumer Staples stock ( XLY ).

McCormick ( MKC ), the leader in flavorings, trades at a massive 33X its earnings, while PepsiCo ( PEP ), the leader in drinks and snacks, trades close to 26X. Even General Mills ( GIS ) trades at a higher 16X, paying similar dividends relative to earnings, about 50% to 58%. The takeaway is that Kraft Heinz shouldn't yield 4.5% but closer to 3% to 2.5% like its competitors and may soon do so. A multiple expansion to put it in line with peers could be worth a minimum of 25% of upside, which is coincidentally in alignment with the analysts' consensus estimates.

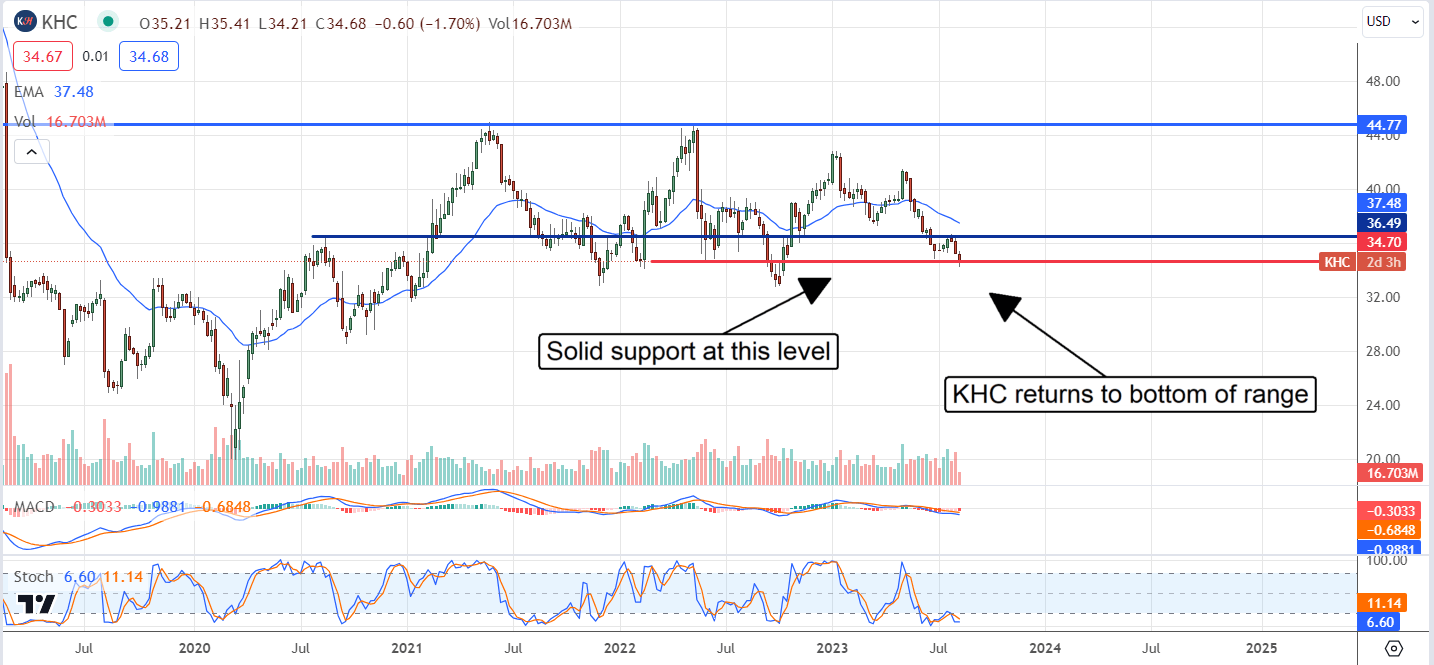

The consensus of 11 prominent analysts ' calls in 2023 has Kraft Heinz pegged at Hold, which is steady compared to the prior 12 months. The trend in price targets is lower and has been weighing on the price action, but it still expects 23% of upside at the mid-point and is more flat than not relative to the past few months. Shares of Kraft Heinz just broke through significant support targets and are opening up the most attractive buying opportunity in nearly a year.

Screenshot/Tradingview/Own work

{kind=link}

Kohl's Is Turning A Corner

Kohl's ( KSS ) struggles are not over, but the company navigates the times better than before. New CEO Tom Kingsbury is guiding the company to a better position, including inventory management and better internal operations. The latest report showed the first glimmers of traction as sales, while down, came in above consensus and were coupled with margin improvement that drove significant strength (and growth) on the bottom line.

The outlook for FQ2 remains hazy, but the company reaffirmed its guidance and commitment to improving the balance sheet and paying the dividend. In that regard, the company's cash position fell on a YOY basis despite the 6% reduction in inventory, but the long-term debt was also reduced by 6% and is freeing up the cash flow outlook.

The cash flow is a concern but sufficient to pay the dividend at current levels. The $2.00 in annualized distributions is about 83% of the 2023 earnings forecast, and there is an expectation for significant earnings improvement over the next few years. Regardless, the company declared the Q3 distribution as expected, and it goes ex-dividend in early September.

Analysts at TD Cowen upped their rating on the stock to Buy vs the consensus Hold following the Q1 report citing CEO Tom Kingsbury as the #1 reason. In their view, his passion for decor and experience in the industry should drive better execution, cost reductions, and margin gain. They see the stock trading at $30, above the current price action and the consensus target.

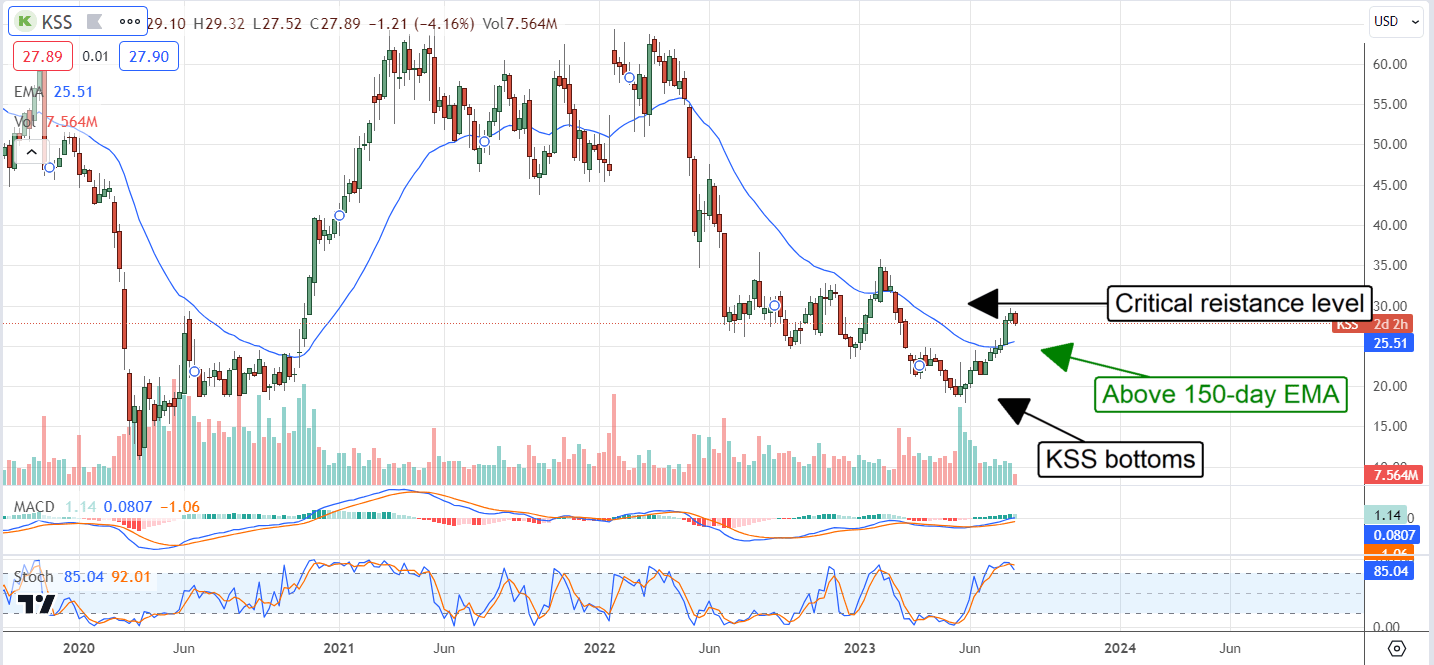

The institutional activity helped the KSS stock price decline to bottom and reverse course earlier this year. The institutions own 98% of the stock and have bought on balance in 2023. Among the company's largest shareholders are LSV Asset Management and BNY Melon, which added to their position recently. Retail investors have also begun to show renewed interest in this turn-around story .

The next catalyst for the market is the Q3 earnings report due out on August 23rd. The expectation is revenue to decline modestly compared to last year, and the bar may be low. There have only been downward revisions to revenue and earnings, which may be mispricing consumer strength. As sketchy as the economic outlook is, the labor market and wage gains remain strong, and fuel consumer spending increases that are not entirely attributable to inflation.

Screenshot/TradingView/Own work

{kind=link}

Verizon Dials Up Dividends And Distribution Growth

Verizon ( VZ ) has had its share of hurdles and headwinds priced into the market. The takeaway for investors is that Verizon shares are incredibly oversold and offer a deep-value opportunity that yields 8%. The Q2 results were mixed, and the consensus is for a YOY decline in revenue and earnings in Q3, but the declines are marginal and play into today's opportunity. The consensus aligns with the company's guidance , calling for core growth and sufficient cash flow to pay dividends.

The analysts are weighing on the price action now, but that headwind is temporary and will soon end. The post-release analyst activity following the Q2 report is mixed, to be sure, but still favorable to higher share prices. There was a flurry of price reductions, including the new low target Wells Fargo & Company set, but all are above the current price action.

Analysts at Wells Fargo rate the stock at Equal Weight compared to a consensus of Hold with a price target of $36. That's 10% below the current price action and suggests a substantial upside is in store for this stock. The most recent activity is a reiterated Overweight from Morgan Stanley with a target of $44.

Coincidentally, the institutions have been buying Verizon like mad in 2023. Net activity is worth more than $9 billion or about 6.5% of the market cap, and total holdings are rising. This is unsurprising given the deep-value and dividend opportunity, including distribution growth. Verizon doesn't have a robust record of increases but a sustained one with a CAGR in the low single-digits . That should continue.

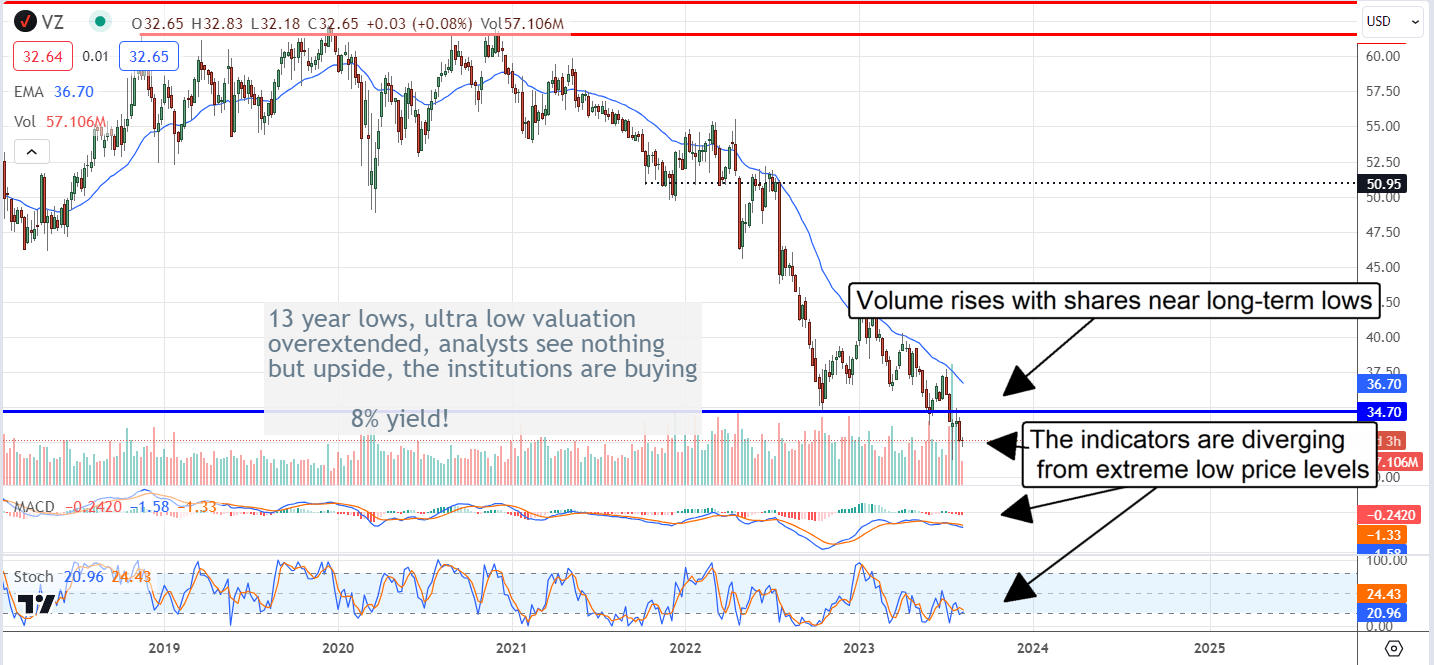

Regardless, there is a pick-up in investor interest , and that is seen in the chart. Verizon is trading at an extreme low, with volume steadily rising and divergent indicators. Verizon may not snap back, but everything in the chart says it is ready.

Verizon is at extreme lows (Tradingview) Screenshot/TradingView/Own work

{kind=link}

For further details see:

3 Deep Value Speculations Income Investors Should Love