ET - 3 Net Debt Heavy High Yielders

2023-10-30 16:44:49 ET

Summary

- Enterprise valuation is in part the process of forecasting a company's future expected free cash flows and discounting them to determine its equity value.

- Companies with large net cash positions and a high probability of upward free cash flow revisions have considerable potential for capital appreciation, in our view.

- Altria, Energy Transfer, and Kinder Morgan are high yield stocks with net debt positions, but they cover their dividends with traditional free cash flow.

- Altria and Energy Transfer yield close to 10%, while Kinder Morgan yields close to 7%. These three ideas may be worth a look for the risk-seeking income investor.

By Brian Nelson, CFA

The enterprise valuation process is also called the discounted cash-flow method. The process involves forecasting a company's future expected free cash flows long into the future and discounting them back to today, using an appropriate discount rate called the weighted average cost of capital. A company's net cash position is then added to the present value of future expected free cash flows, or a company's net debt is subtracted from the present value of future free cash flows to arrive at its equity value. This equity value is then divided by weighted average diluted shares outstanding in order to arrive at an estimated fair value.

We can deduce two very important dynamics from this method. First, a company that retains a lot of free cash flow and doesn't shell out capital in the form of capital spending or dividends has the potential for significant capital appreciation. Second, a company that has a huge net cash position is better off when it comes to equity value considerations than a company with a huge net debt position. Breaking down enterprise valuation into these two simplistic forms of cash-based intrinsic value is one of the reasons why we're huge fans of companies that have huge net cash positions and generate gobs and gobs of free cash flow.

Within this construct, we can also evaluate what drives stock price returns. When a company's trajectory of future expected free cash flow changes, so should its fair value estimate, and its stock price. In this light, it becomes important to find those companies that are not only generating strong free cash flow, but also have the potential to surprise to the upside with respect to free cash flow revisions. Some of our favorite stocks reside in the areas of big cap tech and the stylistic area of large cap growth because these companies have huge net cash positions and have the potential to drive free cash flow above existing expectations.

We continue to reiterate that the key components of a company's valuation are the following: net cash on the balance sheet and future expected free cash flows. These two cash-based sources of intrinsic value generally account for almost all of the value of a firm. There are some exceptions, where contingent liabilities and a more complicated capital structure come into play, but when it comes to simplifying what drives share prices, that's about it. It's probably no wonder then that we love net-cash-rich, free-cash-flow, secular growth powerhouses, and it's also probably no wonder why these companies have grown into some of the strongest-performing stocks on the market, dominating last decade.

We're also not new to the concept of cash-based intrinsic value as we've been focused on the discounted cash-flow process since our small firm was formed more than 12 years ago now. One of our first articles on Microsoft ( MSFT ) here was written over a decade ago, and we called Microsoft a steal way back then. We wrote about Alphabet ( GOOG ) ( GOOGL ) long before it changed its name, and one of our first takes on the name can be found here , where we said its valuation had upside. Then, of course, there's Meta Platforms ( META ), where we had been extremely bullish up until last year, as we describe in this article here .

But what about other areas? Where might we find some high yielders for consideration? Well, most high yielders tend to have large net debt positions on the balance sheet, and because they pay out a large percentage of their free cash flow as dividends or distributions, not only are their valuations weighed down by a net debt burden, but their capital appreciation potential is also inhibited by the payment of dividends, itself. Remember, a company's price is adjusted downward by the amount of the dividend on the ex-dividend date. That's why it is so important to add back the dividend return when calculating total return for dividend payers.

With all of this said, we think there are three net debt heavy, high yield ideas that could be of consideration for the risk-seeking income investor. All three of these names cover their dividends/distributions with traditional free cash flow generation. For two of them in the midstream energy arena, it wasn't always the case, but they have worked hard to get their financials back on track, and we've taken note. The three are tobacco giant, Altria ( MO ), and the other two are Energy Transfer ( ET ) and Kinder Morgan ( KMI ). Altria and Energy Transfer yield close to 10% as of the latest tally, while Kinder Morgan yields nearly 7%--all three posting dividend yields higher than the rising 10-year Treasury rate, which stands close to 5% at the time of this writing.

Altria's recently reported third quarter 2023 results on October 26 showcased how its asset-light business model continues to throw off tons of cash. Traditional free cash flow generation came in at ~$5.9 billion during the first nine months of 2023 , while cash dividends paid came in at ~$5 billion, resulting in a very nice free cash flow coverage on a near-10% yielding stock. We view this strong coverage as highly unusual for such a high yielder. Though revenue growth at Altria hasn't been great, its gross profit continues to hold up. The firm's goal is to achieve mid-single-digit dividend growth on an annual basis, which seems attainable given existing free cash flow coverage. For income investors that aren't worried about ESG-related criteria, Altria could make for a great diversifier in a high-yield dividend income portfolio. Even with its ~$23.6 billion net debt heavy balance sheet, our fair value estimate of Altria stands north of $60 per share. You can view the first page of our 16-page report on the name in this article .

Energy Transfer is scheduled to report its third-quarter 2023 earnings soon, so our latest analysis considers the first half of 2023 . During that period, the midstream energy giant generated ~$5.9 billion in operating cash flow and spent ~$1.7 billion in capital, achieving free cash flow that was plenty good enough to cover distributions to partners and controlling interests of ~$2.1 billion and $862 million, respectively. Granted, the company still holds a massive net debt position, but we continue to be pleasantly surprised at the considerable improvement in midstream traditional free cash flow this decade. At the end of June, Energy Transfer's cash position stood at $330 million, while its short-term debt and long-term debt came in at ~$3.5 billion and ~$44.7, respectively. Though its valuation is weighed down by net debt and its capital-appreciation potential faces headwinds from a lofty payout, shares aren't too expensive and may be worthy of consideration for those seeking hefty income in a tax-sheltered account.

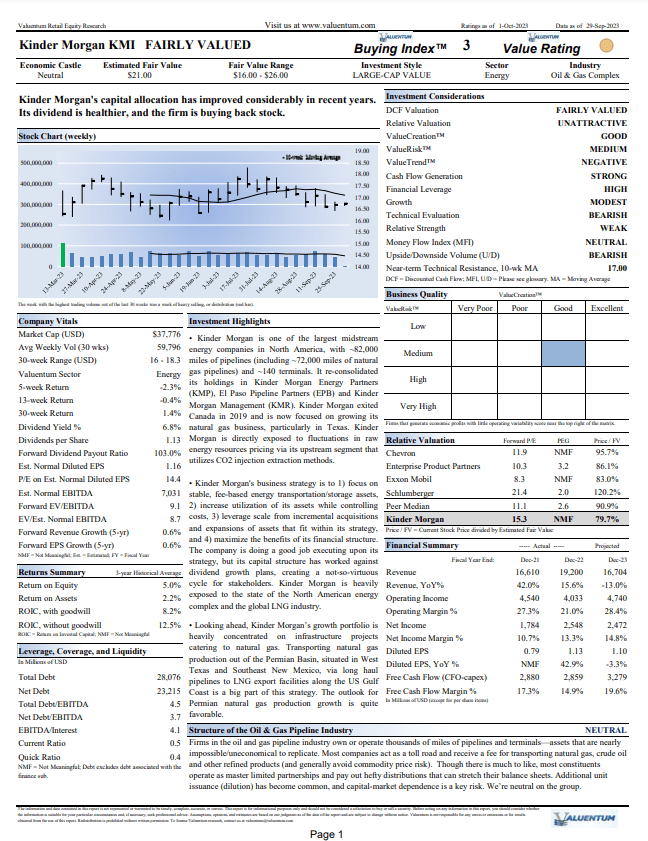

Now, on to Kinder Morgan. The company's third-quarter report wasn't one to write home about as both distributable cash flow and adjusted earnings fell from the same period a year ago due in part to higher interest expense. However, demand for natural gas and storage solutions remains strong. The midstream giant's project backlog came in at $3.8 billion at the end of September, up modestly on a sequential basis. Though Kinder Morgan noted it expects to "finish 2023 slightly below (its) plan on a full-year basis," its interconnected portfolio of assets remains a key competitive advantage that's not going away anytime soon. Looking at its 10-Q shows a company that is now comfortably covering its cash dividend payments (~$1.9 billion through the first nine months of 2023) with traditional free cash flow ($2.48 billion through the first nine months of 2023), and that's great when it comes to its dividend sustainability. Kinder Morgan's massive net debt position of ~$30.9 billion at the end of the third quarter still leaves a lot to be desired for equity investors, but for those laser-focused on the payout, the firm is much healthier today than it was last decade.

The first page of our 16-page report on Kinder Morgan. (Valuentum)

{kind=link}

All things considered, net debt on the balance sheet isn't something that we like much given our focus on the cash-based sources of intrinsic value to the equity: net cash on the balance sheet and future expected free cash flow. Altria, Energy Transfer and Kinder Morgan all have hefty net debt positions, but they are covering their cash dividends/distributions with traditional free cash flow, as measured by cash flow from operations less all capital spending. If they can continue to do this and grow free cash flow in the years to come, dividend growth may also ensue. Though these three net debt heavy high yielders aren't our favorites -- we like net-cash-rich, free-cash-flow generating, secular growth powerhouses -- they are nonetheless worthy of consideration for the risk-seeking high yield dividend investor.

For further details see:

3 Net Debt Heavy High Yielders