VZ - 3 Of My Favorite Dividend Growth Stocks For 2024

2024-01-02 11:14:04 ET

Summary

- Verizon Communications, Eversource Energy, and Intercontinental Exchange are three dividend growth and income stocks to consider for 2024.

- Verizon Communications has shown consistent growth and has a strong dividend yield, making it an attractive long-term buy.

- Eversource Energy is a leading utility company with a diverse customer base and plans for infrastructure investment, offering potential for future dividend growth.

- Intercontinental Exchange is a leader in exchanges and quickly raising its dividend.

The start of the year is an excellent time to start new positions or add to an existing one. The stock market performed well in 2023, but tech and growth stocks shined. Dividend stocks struggled except for the last couple of months. However, the 2024 calendar year may differ, especially if the economic trends stay positive.

In this article, I discuss three of my favorite dividend growth and income stocks for 2024. Two struggled in 2023 but are poised to rebound this year. One has double-digit dividend growth and expanded into a new business line. The three stocks are Verizon Communications (VZ), Eversource Energy (ES), and Intercontinental Exchange (ICE), which are all long-term buys.

Verizon Communications

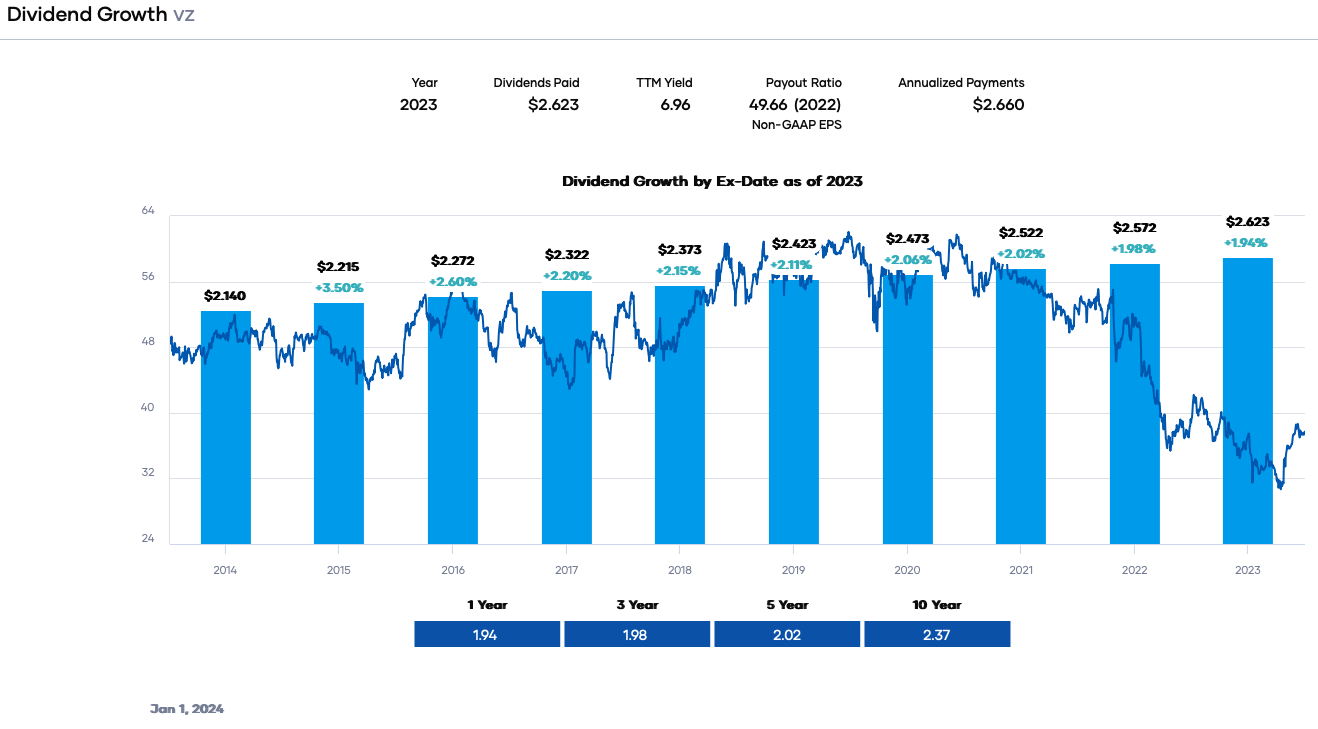

Verizon Communications ((VZ)) remains one of my favorite dividend growth and income stocks. It is one of the three companies controlling the cellular market. It is also a primary player in business and retail broadband. Total revenue was $134,095 million in the last twelve months.

The firm has grown organically and through acquisitions. It last bought TracFone in 2021, adding 20 million pre-paid subscribers. Today, Verizon has 143.6 million retail wireless connections. The Consumer Group has 114.1 million wireless retail customers, with 92.7 million postpaid. The Business Group adds another 29.5 million postpaid clients. It also has about 8.8 million broadband connections, of which 6.9 million are Fios.

We like Verizon because of its consistent growth over time. Currently, broadband is adding subscribers. Granted, the wireless business was performing poorly, but it may have turned the corner at the end of 2023. The business retail numbers are climbing, and consumer retail losses are declining. Additionally, the postpaid wireless losses are decreasing too. If current trends continue, the wireless numbers should show growth in 2024.

Operational weakness and high-interest rates pushed the share price down. As a result, the dividend yield soared to over 8%. A bounce-back in share price has brought the yield to a respectable 7%. The dividend is growing about 2% annually. We expect future growth to continue because of the 50% payout ratio. Verizon is a Dividend Contender with 19 years of growth, and Dividend Aristocrat status should be attainable.

{kind=link}

The dividend is supported by an earnings payout ratio of only about 49% and robust free cash flow coverage. Further, the dividend safety is excellent. Portfolio Insight’s dividend quality grade, a measure of earnings performance, revenue performance, dividend performance, profitability, and financial strength, is an ‘A.’ This score means the equity is in the 90 th percentile. Lastly, the credit rating agencies give Verizon a BBB+/Baa1, a lower-medium investment grade rating.

Verizon is practically a steal, dirt cheap, trading at a price-to-earnings ratio of only ~8.0X, well below the 5-year and 10-year ranges. Investors are not expecting much from the telecommunication giant. As a result, Verizon is a solid choice for investors seeking dividend growth and income at a reasonable price. It is a long-term buy.

Eversource Energy

Eversource Energy ((ES)) is one of our favorite utilities. It is the largest New England utility, with operations in New Hampshire, Massachusetts, and Connecticut. The utility is also one of the few servicing electric, natural gas, and water customers. In total, it has approximately 3.29 million electric customers, 890,000 natural gas customers, and 237,000 water customers. The rate base is $56 billion, and total revenue in the past twelve months was $12,246 million.

The utility is acquisitive, adding to its territory every few years. It purchased NStar's Massachusetts utilities in 2012, Aquarion in 2017, and Columbia Gas in 2020. The fragmented utility territory, especially natural gas and water, means Eversource should have opportunities to expand.

Eversource is also growing organically by investing in its infrastructure—the firm plans to spend roughly $21.5 billion between 2023 and 2027 on capital expenditures. The focus is developing the electric transmission platform, natural gas distribution upgrades, and electricity distribution improvement. Consequently, the rate base will climb, allowing earnings per share to grow 5% to 7% yearly.

Additionally, the utility is a significant player in offshore wind power. The firm is spending to develop power generation in federal waters in three joint venture projects: South Fork Wind, Revolution Wind, and Sunrise Wind. South Fork Wind will deliver 130 MW to the New York power grid by 2023. Revolution Wind is a 704 MW project that will provide power to Connecticut and Rhode Island by late 2025. Lastly, Sunrise Wind will deliver another 924 MW to New York by late 2025. These projects are making Eversource a leader in renewable wind power.

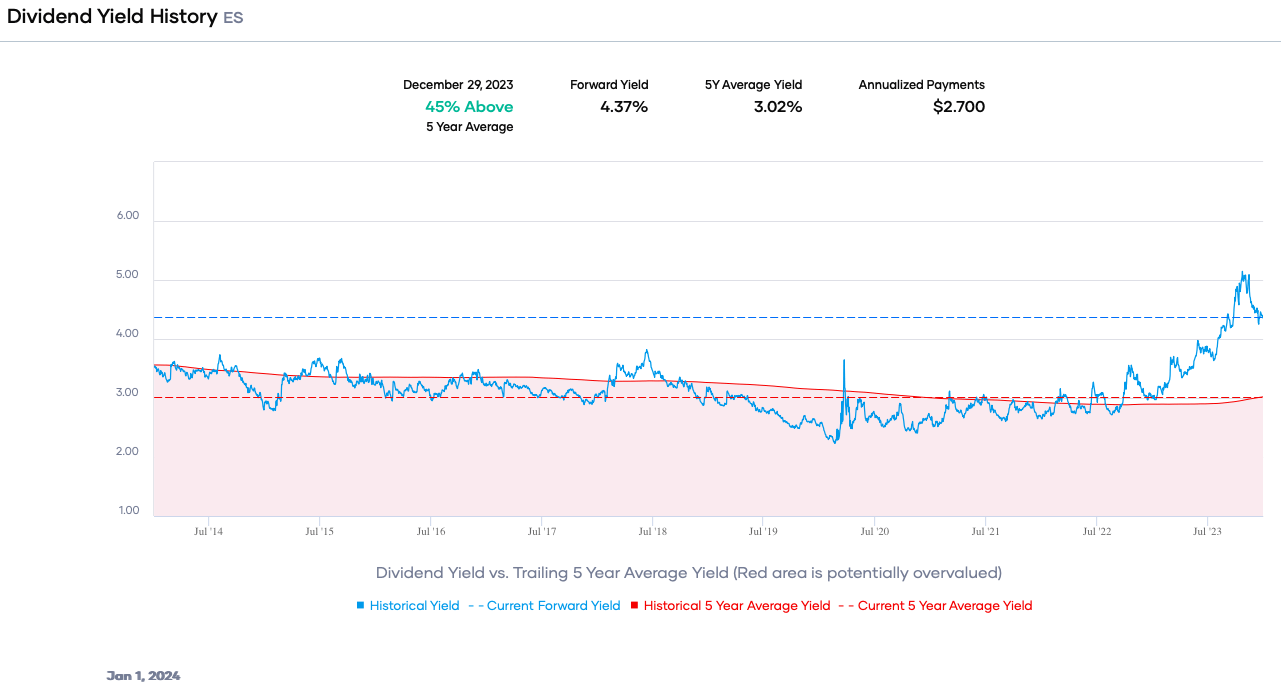

As a group, the Utility sector performed poorly in 2023. Rising interest rates caused share prices to plunge, and Eversource was no exception. Despite the end-of-year bounce back, the share price declined ~27%. Hence, the dividend yield soared and is now almost 4.4%. The generous yield is backed by a moderate 62% payout ratio, indicating the increasing asset base will permit future dividend growth at nearly the same rate. The trailing growth rate is averaging 6% annually.

{kind=link}

The dividend safety is excellent, too. Eversource receives an ‘A+,’ for the dividend quality grade, meaning it’s in the 95 th percentile. The credit ratings are BBB+/Baa2, a lower-medium investment grade rating.

Eversource is undervalued because of the share price decline. It trades at a 13.5X forward earnings multiple, below the 5-year and 10-year ranges. This combined with the generous yield, 25-year dividend growth streak, and safety, makes the stock attractive. I view it as a long-term buy.

Intercontinental Exchange

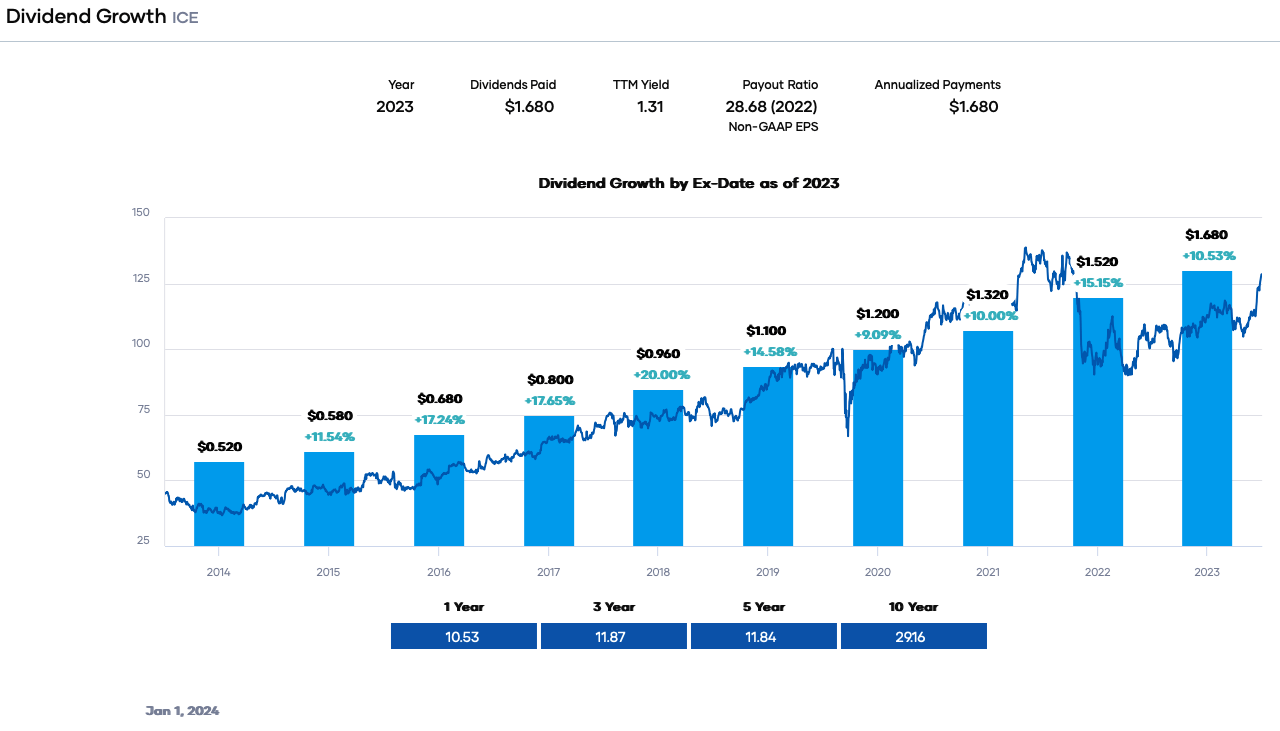

Our last pick is Intercontinental Exchange ((ICE)), a leader in exchanges, fixed-income data services, and mortgage technologies. The firm owns the New York Stock Exchange. Other platforms include derivatives, commodities, futures, and energy contracts marketplaces. Besides trading, it offers analytics and services. Total revenue was $7,555 million in the past twelve months.

Intercontinental Exchange has expanded rapidly by acquisition. The firm periodically buys competitors or uses M&A to move into new businesses. It built the mortgage technology business by purchasing Ellie Mae in 2020 and Black Knight in 2023. In addition, the financial firm grows organically by adding services and natural growth in trading. For example, the company recently added cryptocurrency options data to its feed.

That said, high-interest rates have affected the mortgage business, keeping volumes and revenue low. However, mortgage rates have come down after peaking about two months ago. As a result, volumes may rise. Moreover, the U.S. Federal Reserve may lower interest rates in 2024, a positive.

Intercontinental Exchange is a Dividend Contender with a 10-year streak of increases. The average growth rate has been nearly 12% in the past five years. The modest payout ratio of ~29% probably means more increases in the future. The dividend quality grade is a B+. The one negative about safety is the elevated leverage ratio of 5X because of the acquisitions.

That said, the firm is trading below its 5-year P/E ratio range. If mortgage volumes recover, the top and bottom lines may climb higher. Intercontinental Exchange is a long-term buy.

{kind=link}

For further details see:

3 Of My Favorite Dividend Growth Stocks For 2024