MCD - 3 Restaurant Brands There Will Be One Winner

2023-10-18 05:57:48 ET

Summary

- Three industry titans, one emerging victor.

- From former owner to fierce competitor: Chipotle's rise above McDonald's.

- Domino's Pizza, fading glory, and increased risks.

- McDonald's is a solid company to own but at a lower price.

Preview

Today, I'm going to take a different approach. I won't be delving deep into any of the brands I'm covering. Instead, I'll focus on comparing their numbers and differentiating one from another. I'll also identify who I believe will be the winner in the future.

The stocks I'm about to present are not in the same growth stage, and they attract different types of investors. However, they all boast strong brands and, in one way or another, possess a competitive advantage, although they are not all equal in this regard. Some have been significant compounders in the past, while others have faced challenges. Let's delve into Chipotle ( CMG ), McDonald's ( MCD ), and Domino's Pizza ( DPZ ).

I'm going to compare them based on the following parameters:

1. Past top-line and free cash flow growth

2. Future top-line and FCF growth

3. Margins

4. Returns on capital

5. Solvency

6. Returns to shareholders

7. Historical multiple averages

8. Discounted cash flow analysis

Growth

When it comes to what investors look for in companies, especially in recent years, top-line growth is all that matters. In my opinion, aside from returns on capital, it is the most important factor in creating a massive compounder.

As you can see above, McDonald's, though it did beat the market, is the loser among the 3. It is hard to tell, though, on the basis of price return, because each company has a different type of risk. For McDonald's to deliver those results with a relatively low risk is impressive. But I'm not going to do a risk-adjusted return today. McDonald's only achieved a 2.3% CAGR over the last 5 years, which is very low and is not enough to deliver strong price movement. Yet, as we will examine later, FCF per share growth is the more important factor. The slow growth can be the result of factors such as market maturity, losing market share, or management mistakes. If I were a McDonald's shareholder, I'd like to see the management address these issues. When we examine the FCF growth, it's clear that it is outpacing revenue growth, indicating the presence of operating leverage, which is crucial but somewhat limited. McDonald's delivered a 3.8% FCF growth. Again, margin expansion is limited, and they will need to enhance revenue growth. Looking ahead, analysts appear quite confident about McDonald's top-line growth as they project a 6.1% CAGR increase for the next 3 years. This is nearly triple the growth rate of the past 5 years, although it's still relatively modest.

Now, let's direct our attention to Chipotle, a stock that has exhibited massive compounding potential, primarily due to its impressive CAGR of 14.8% in the top-line growth. Drawing comparisons between McDonald's and Chipotle can be somewhat challenging because they operate in different growth stages, with Chipotle having less mature markets. Furthermore, Chipotle has demonstrated exceptional FCF growth over the past five years, registering an impressive 32%. This rate is twice as high as its top-line growth. It's worth mentioning that while I expect margin expansion to continue, it might not occur at the same breakneck speed as in the past. Importantly, I wouldn't recommend using Chipotle's historical FCF growth rates in a DCF model, as I believe the unsustainable nature of those 30% figures is a critical factor.

Looking ahead, analysts project a 13.4% CAGR in top-line growth for Chipotle over the next three years, and these numbers seem quite sustainable, given Chipotle's substantial global expansion prospects.

DPZ has been a massive compounder since the turn of the millennium, making it one of the strongest stocks to hold. However, things change over time, and we'll delve into DPZ's debt situation later. In the meantime, DPZ has represented moderate growth over the past five years, boasting a 6.6% CAGR. While it's not as low-growth as MCD, I can't see this growth alone driving the stock price upward in the long term, as it did in the past.

When we examine the stock's performance over the last five years, it becomes evident that the S&P 500 outperforms DPZ significantly, with moderate growth being one of the contributing factors. Nonetheless, DPZ does exhibit signs of margin expansion, with FCF growth doubling that of its top-line growth. While this is essential, it might overshadow the top-line growth. As with MCD, I believe the management needs to address this matter, and this is something I would be attentive to in their conference calls.

Furthermore, unlike Chipotle, DPZ may not grow during the challenging year of 2023, as their top-line growth appears to be stagnant, which doesn't bode well for moat resilience. Analysts, however, hold a positive outlook for the near future, projecting a three-year CAGR of 11% , almost double that of the past five years. If this growth is attainable and margin expansion continues, there is potential for outperformance.

Margins

High margins provide a margin of safety. Consider a scenario where you can't pass on rising inflation costs to the consumer, which, in itself, suggests that you lack pricing power. The result can be detrimental. However, if you maintain high margins, you won't have to cut dividends, cease buybacks, default on debts, or halt capital expenditures for future growth. It becomes a temporary bump in your financial journey.

Furthermore, if your margins are not only high but also consistently expanding, it signifies that you possess pricing power. This means you can pass on increased costs to consumers without negatively impacting your sales. This aspect is incredibly significant as it indicates that someone has dug a deep moat, providing you with a competitive advantage in the market.

The variation in margins arises from the distinct nature of these businesses. McDonald's, which offers more ready-to-eat food items requiring fewer employees, maintains relatively higher margins. On the other hand, Domino's Pizza, primarily focused on delivery services, operates with moderate margins. Chipotle, expectedly, has the lowest margins given the freshness of its food and the need for on-site food preparation. It's worth noting that Chipotle is exploring technologies to reduce the reliance on manual labor in food preparation. As you can observe, all three companies maintain relatively stable margins. While McDonald's had a slight margin dip in 2022, its consistently high margins provide a buffer for its financials. I would compare the strength of these margins alongside revenue growth because it's not just about passing costs on to consumers; you must do so without damaging your brand or sales. In this regard, Chipotle stands out as the clear winner. Its top-line growth appears to be steady, and the company has managed to maintain stable margins. Recently, Chipotle even raised its prices once again.

ROC

As I mentioned earlier, besides revenue growth, another crucial factor in long-term compounding is value creation. A company creates value when it achieves high returns on capital across its various ratios, significantly exceeding the firm's cost of capital. It's worth noting that ROIC and ROCE depend on the industry and the type of business. In our case, these three companies are competitors, making it easier to draw comparisons. I'll be focusing on two critical metrics: ROIC and ROCE.

All three of these companies have great returns in both metrics, but I believe Chipotle is the winner, and I'll explain why. The super-high ROC in Domino's is derived from its high debt, resulting in negative shareholders' equity. This makes the denominator smaller, making the percentage look better. The situation is similar with McDonald's, and I wouldn't be enthusiastic about this figure for both of these companies. However, Chipotle achieves great returns above the WACC and, therefore, creates a lot of value without any debt at all. This indicates the company's ability to generate excess returns without taking on more risk associated with debt. In contrast, Domino's takes on a lot more risk to achieve those returns.

So once again, in this aspect, Chipotle comes out as the winner.

Solvency

I like to compare a few indicators to assess if a company is solvent, such as:

1. The amount of cash on hand compared to the debt.

2. How many years of FCF it will take to cover the debt?

3. The current ratio for liquidity.

4. An Altman Z-Score for comparison.

Let's take a look at the following charts:

As we can see, Chipotle can finance its growth without any debt, avoiding excessive risk, especially with the current high interest rates. It would have been advantageous for them to take on some debt during the zero interest rate policy ((ZIRP)) era, but I prefer no debt to too much. On the contrary, McDonald's and Domino's Pizza utilize much more debt. If something goes wrong, it will take them several years to pay down their debts using their FCF, and they might need to use equity to cover their obligations. Overall, there is much more risk associated with both of these firms.

I use the current ratio to assess liquidity, and it appears that all of them can cover their short-term obligations within a year, as a ratio above one is considered good.

The Altman Z-Score is a ratio used to determine the financial health of a company. If it is above three, it indicates that there is a lower risk of going into default. If it's under three, the risk is elevated. As we can see, both Chipotle and McDonald's are in good financial health, while Domino's Pizza carries a higher risk with a Z-Score under three, so caution is advised.

Returns To Shareholders

Let's examine how the three directly compensate their owners with the form of dividends or buybacks. It's worth mentioning that companies in different business cycles, such as more growth-oriented firms like Chipotle, are advised to invest in growth rather than dividends. Additionally, buybacks can be destructive if the stock is expensive.

Chipotle doesn't return value to shareholders in any form other than stock price appreciation, which is understandable, as dividends don't suit this type of company, and buybacks must be done responsibly. McDonald's also engages in minimal buybacks, but it's recognized as a 'Dividend Aristocrat' and currently offers a healthy dividend yield of 2.4% , which is above its five-year average. Domino's Pizza also pays a solid dividend of 1.3% , though it raises questions about why they allocate resources to dividends instead of paying down their debts.

Before we delve into valuation, based on quantitative analysis, we can confidently identify Chipotle as the clear winner moving forward, followed by McDonald's, and Domino's Pizza at the last position. However, nothing is worth investing in unless the price is attractive. A great company can be a bad investment at the wrong price, and the opposite is also true.

Valuation

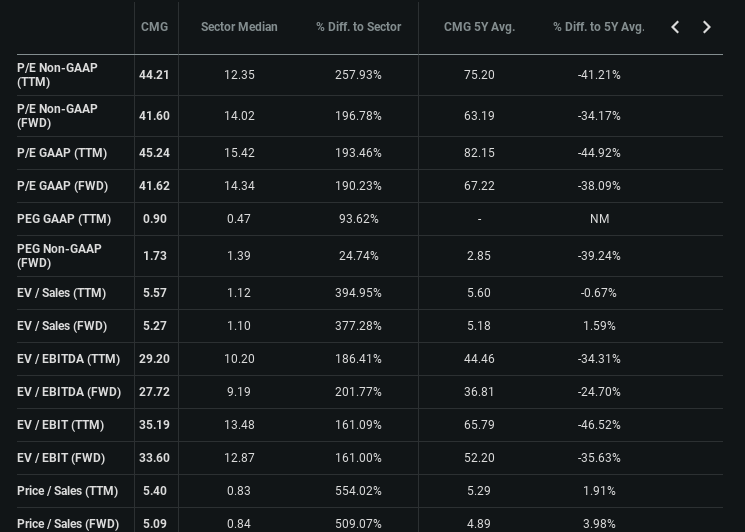

I will perform a two-step valuation: historical multiples and DCF. It's worth noting that historical multiples are influenced by the era of ZIRP, and we should anticipate a decrease in the averages as the equity risk premium rises and investors demand higher returns.

Despite trading at a high multiple compared to the S&P average, Chipotle is significantly below its five-year averages, with no specific reason related to the business itself. The market seems to have two main concerns that could impact CMG's free cash flow: a recession and weight loss drugs. However, I believe that Chipotle's momentum is quite strong, and there are currently no signs of a slowdown. While I don't expect Chipotle to return to its five-year averages, there is potential for multiple expansions from the current levels, in addition to the business growth.

{kind=link}

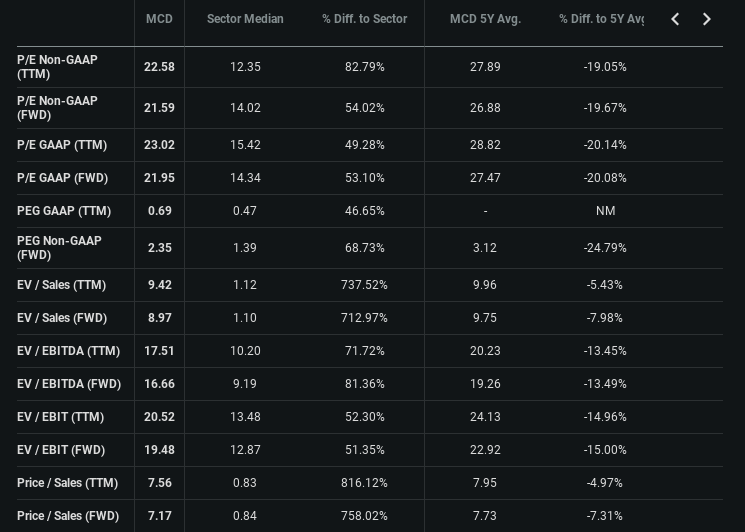

The same holds true for McDonald's, which is at a reasonable multiple, although on the higher side considering its growth rates. But I suppose this is what's known as a 'moat premium.' McDonald's is also trading at a 4.2% free cash flow yield, which is a 20% increase from its average.

{kind=link}

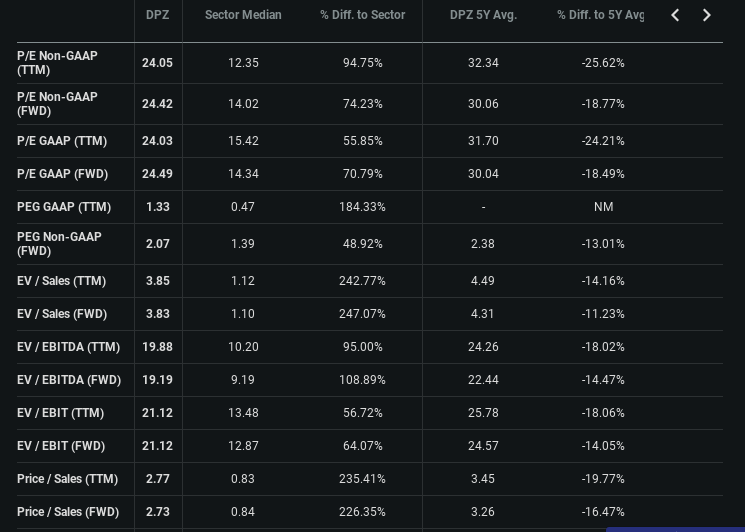

Domino's Pizza is also up 20% from its free cash flow yield average, and it's trading under its other multiple averages. However, considering the moderate path of growth for a company with the risks that DPZ carries, I agree that investors need to seek a lower price.

{kind=link}

DCF

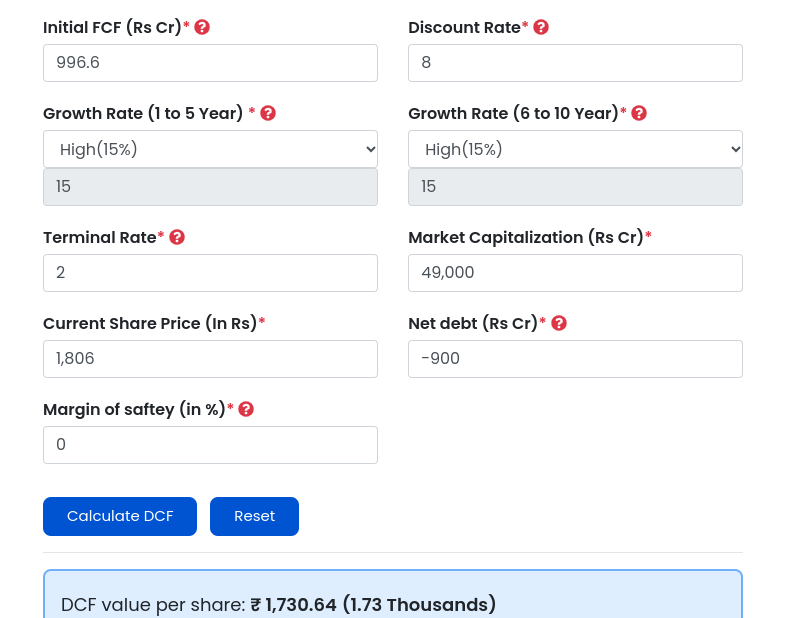

Chipotle's inputs include an 8% discount rate (Alpha Spread WACC ), a solid 15% free cash flow growth, a bit higher than projected revenue by analysts, and a 2% terminal growth rate. The model suggests that Chipotle is slightly overvalued, with an intrinsic value of 1730, representing a 4.5% overvaluation. It's important to note that DCF values are very sensitive, and even a slight change in the inputs can cause a significant price fluctuation. For example, if I were to raise the terminal growth rate to 3%, it would result in an undervalued stock by 9%.

I believe it's challenging to find a high-quality business like Chipotle at a bargain price. Therefore, what may seem like a fair price can be seen as a buying opportunity. I wouldn't describe Chipotle as a bargain, but I do think it presents a buying opportunity.

{kind=link}

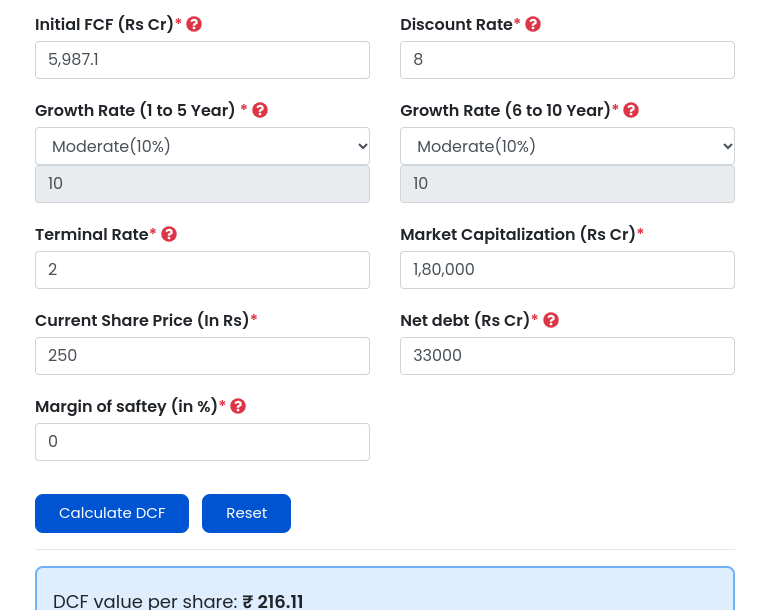

If McDonald's can achieve 10% FCF growth, it seems fairly valued, though slightly overvalued, based on the following inputs: an 8% discount rate ((WACC)), a 2% terminal growth rate, and a 10% FCF growth rate.

The derived price is $216, suggesting a 15% overvaluation. It's worth noting that, as I've demonstrated in my previous articles, DCF models may not fully capture a company's quality, which is why they don't always make compounders look attractive. However, in the case of McDonald's, I believe it is indeed overvalued. While it has a brand premium, which is understandable, it lacks significant growth.

{kind=link}

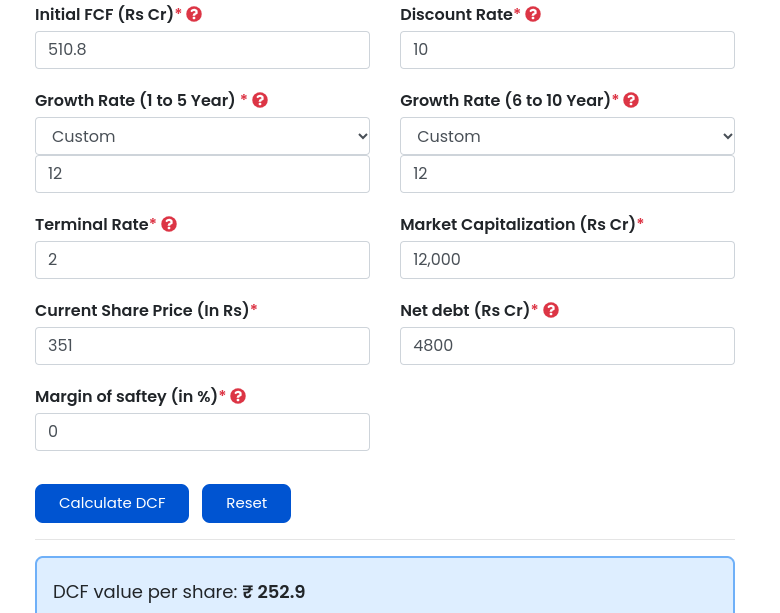

Domino's Pizza appears to be 16% undervalued based on the following inputs: an 8% discount rate, a 2% terminal growth rate, and a 12% FCF growth rate, in line with EPS projections. However, I prefer to be more conservative due to the riskier financials of DPZ, so I'll assume a 10% discount rate. The derived result is $250, suggesting a 39% overvaluation. For a company like DPZ, it's prudent to take a conservative approach to mitigate substantial risks.

{kind=link}

Conclusions

CMG is, in my opinion, by far the best firm among the three, and it appears to be trading at a reasonable price. Therefore, I'm suggesting a BUY rating.

MCD has its own quality, mainly centered around its brand, but the price isn't attractive enough for me to overlook the lack of growth. Thus, I would recommend a HOLD rating, suggesting that you consider buying it at a slightly lower price.

DPZ has been a massive compounder in the past. However, I don't believe this is the current situation. It also carries a significant solvency risk in my view. Therefore, investors would need a much lower price to eliminate this risk. This is the first company in my author journey that I'm rating as a SELL.

Looking forward to your comments. Let me know what you think.

For further details see:

3 Restaurant Brands, There Will Be One Winner