TOL - 30-Year Fixed Mortgage Tops 8%: Interest Rate Landslide Continues

2023-10-19 10:35:26 ET

Summary

- 10-year Treasury and 30-year fixed mortgage rates hit fresh post-2008 highs. 30-year fixed hit 8% yesterday and jumbo mortgages hit 8.06%.

- Rising interest rates have led to a precipitous decline in buyer purchasing power and difficulty in qualifying new buyers.

- Homebuilders are value traps, with ~1.67 million homes under construction in the U.S. as interest rates continue to increase and the working-age population declines.

The ongoing interest rate avalanche continued this week, with both the 10-year Treasury and the 30-year fixed mortgage hitting fresh post-2008 highs. 30-year fixed-rate mortgages hit 8% yesterday , with jumbo mortgages clocking in at 8.06%. On a $500,000 mortgage, buyer payments would now be $3,668 per month, up from $2,108 at a 3% rate. This is on top of 40%-plus increases in home prices since COVID-19, driving buyer purchasing power to near an all-time low . The surge in interest rates is likely to have profound implications for the housing market and the economy at large, and the surge may not even be done. With record-high government budget deficits, we're now knocking on the door of 9% mortgage rates. Mortgages popped another 8 basis points today alone, with some analysts pointing to President Joe Biden's comments on increasing government spending yet again, this time on foreign policy goals. How will the housing market and economy take this, after 14 years of being built around interest rates being at or near zero? Probably not well.

The iShares Home Construction ETF ( ITB ) had a huge rally in 2023 that didn't make much sense, and it now seems like it's being rapidly unwound. Key to why this might have been: Hundreds of thousands of new U.S. homes sold with builder-financed teaser rates from 2022 to now . The National Association of Realtors' tagline was that buyers should " date the rate and marry the house ," buying property at an uncomfortable monthly payment but looking to refinance down the road. However, interest rates just keep going up, meaning that not only can buyers not refinance, but if they want to sell and get out, it's increasingly difficult to qualify new buyers. Now these teaser rates are starting to expire, and home buyers are finding themselves in a shotgun wedding after thinking they'd just date their mortgage for a year.

Does The Interest Rate Surge Make Homebuilders Value Traps?

Likely yes. I've repeatedly argued that homebuilders are value traps despite trading for low P/E ratios. Lennar ( LEN ) trades for 8.1x earnings, PulteGroup ( PHM ) trades for 6.3x, Toll Brothers ( TOL ) trades for 6.1x, and D.R. Horton ( DHI ) trades for 7.9x earnings. There are a lot of cyclical stocks out there trading for 5-10x earnings. Airlines, automakers, and homebuilders are prime examples. If they can consistently make the earnings they've made in 2021 and 2022, then they're a mathematical slam dunk as value investments. But if the business cycle still exists, which it does - then these profits will likely turn into losses at some point.

Currently, there are about 1.67 million units of housing under construction in the U.S. But the working-age population in the U.S. is actually declining . So with mortgages at 8% and the working-age population declining, who's going to live in these 1.67 million housing units? Every new working adult looking to buy a house should be matched by an older person passing away or looking to downsize from this point forward, that's just how the demographic shift works. And the COVID real-estate panic pulled forward years of housing demand, so many of the buyers who would be buying now already bought.

Is there really a demographically-driven housing shortage? Or is today's market the consequence of years of speculative excess? We know for a fact that the housing supply in the U.S. has grown faster than the working-age population and is at levels higher than in 2008. There's no demographic shortage, only a shortage driven by speculation with low-interest-rate mortgages.

I'm doubling down on my housing call here. Without interest rates suddenly dropping back to pandemic levels, homebuilders are likely to get stuck with a ton of inventory they can't sell. And it's hard for interest rates to go down with massive budget deficits crowding out the loanable funds market. It's the classic economics debate over " guns vs. butter," reimagined. I wouldn't necessarily recommend making short bets on homebuilder stocks, but the writing is clearly on the wall to sell here after an irrational run in 2023.

Economic Consequences Of 8% Mortgages

At a $100,000 level of income, no existing debt, and a 36% DTI, buyers could qualify to buy a house worth $721,000 at a 3% rate of interest. At 4%, this drops to $649,000. At 5%, it's $587,000. At 6%, it's $533,000. At 7%, it's $486,000. Now at 8%, it's $445,000. Take mortgages to 9%, and purchasing power falls further, to $410,000. That's good for a roughly 43% drop in buyer purchasing power on the interest rate change alone. This is based on what buyers can qualify for. I've made this point before but I'm making it again here just because it's so mind-blowing. Sure, mortgages were higher in the 1980s and 1990s. But home prices compared with salaries were quite low, such that overall debt-to-income ratios for new homebuyers were far better overall than now. Additionally, the working-age population was booming and urbanization was still very much an ongoing process in the U.S. at that time.

One of the most overlooked pieces of the post-war housing market was that roughly 1/5 of the total U.S. population moved from rural areas to cities between 1960 and 2000. Additionally, the overall population was growing quite rapidly, creating a need to continuously build millions of houses in cities. That's not the current situation at all. With some limited exceptions, you generally can't buy property now anywhere in the U.S. and count on demographics to make it more valuable. With a rapidly aging population, there will be no " greater fool " to sell to unless prices come down.

Housing is thought to be a fairly sentiment-driven market and it is. But what's interesting about this huge interest rate landslide is that it shrinks the buyer pool geometrically with each 1% interest rate increase. If the banks won't qualify the buyers for the loan, they can't buy. That means that the real estate agent and loan officers aren't getting a commission, the title company isn't getting its money, people aren't dropping $40,000 on new furniture to furnish the house, and people aren't buying a second or third car to put in the garage. Because so many people are employed directly or indirectly by the housing industry, housing sales are a very clear leading indicator for the rest of the economy.

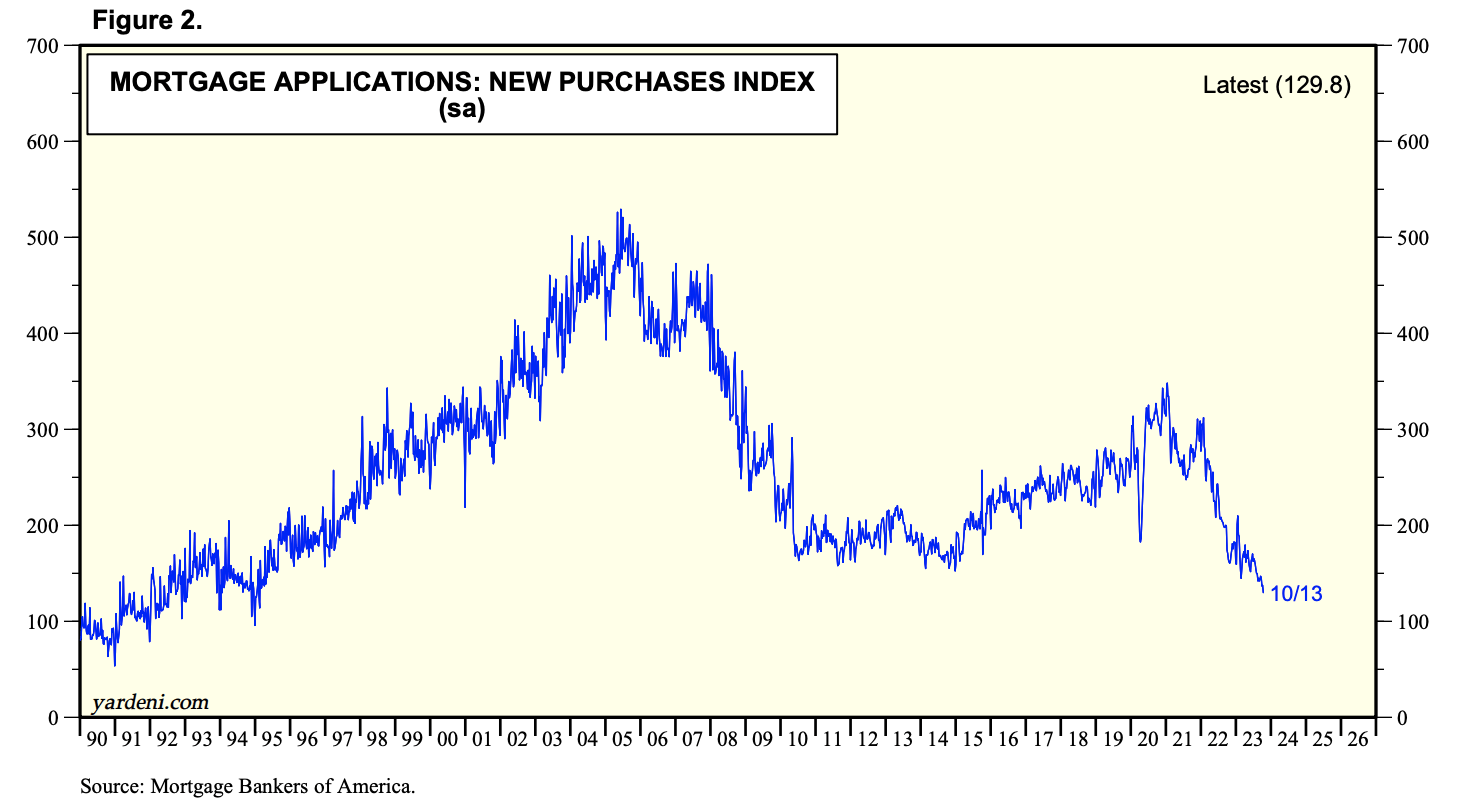

Here we see that new mortgage applications have dropped below even the levels of 2008. 2008 had more to do with unemployment and today's market has to do with skyrocketing interest rates, but new mortgage applications rapidly dropping is something worth noting. Note that this is an index, not a tally of mortgages originated.

U.S. Purchase Mortgage Applications (Yardeni Research)

{kind=link}

Is this because people are rich and they're suddenly paying cash for everything? The answer is no, and this is easily cross-verified by looking at existing home sales as well as the mix between cash and financed buyers. Cash buyers are typically about 25% of the market, this number goes up a little when rates are higher and down a little when rates are lower. Some wacky data from Redfin ( RDFN ) notwithstanding, cash buyers represent about 27-28% of the current market, and are largely divorcées and older homebuyers looking to downsize. When investors pay "cash," it generally just means they're getting their financing from somewhere else than a bank mortgage.

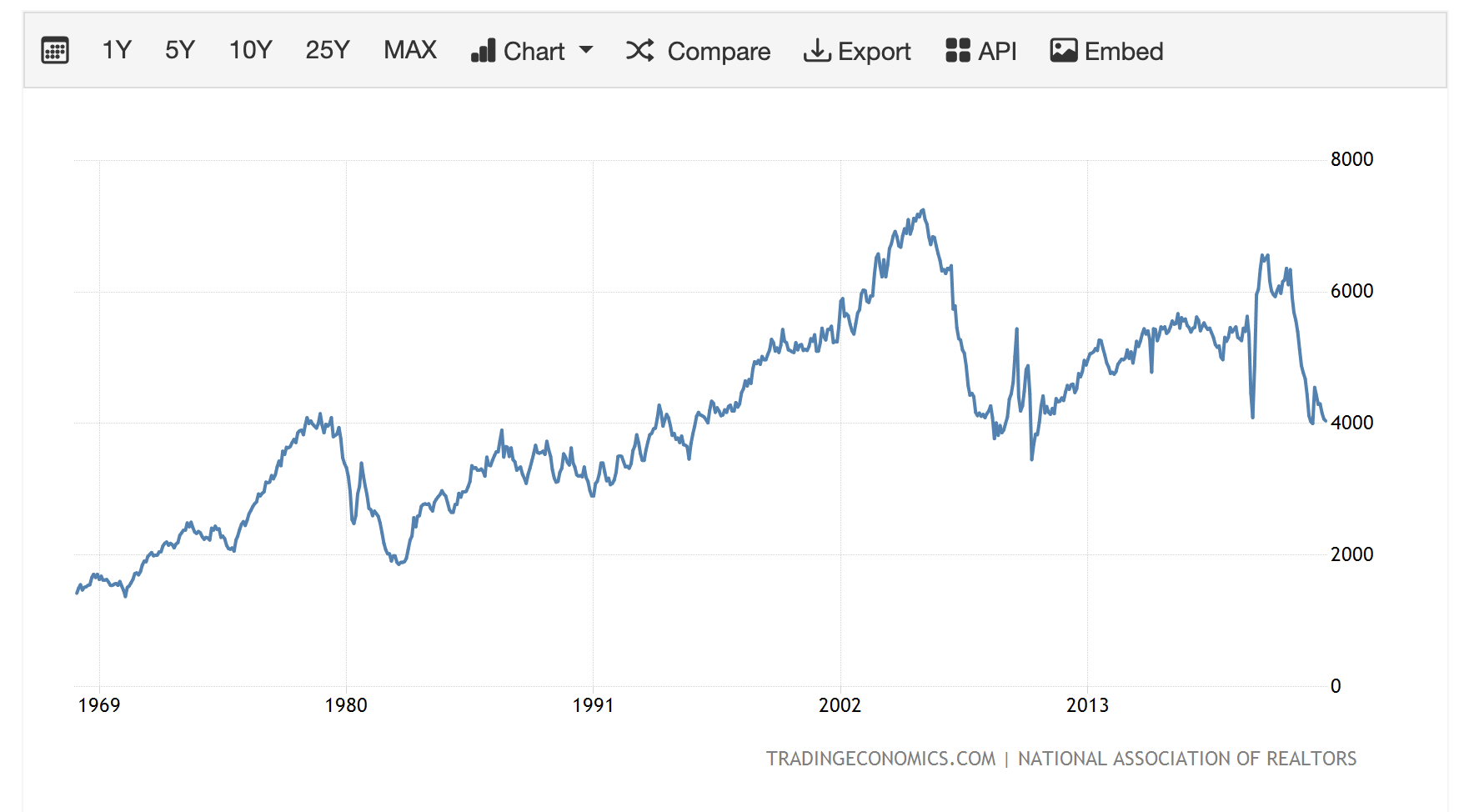

U.S. Existing Home Sales (Trading Economics)

{kind=link}

Here we see existing home sales have dropped from a bit over 6 million to an expected number of under 4 million for this month's release. There are only really three sustained downturns here in existing home sales:

- The Volcker era - when mortgages hit ridiculous heights, the market wouldn't fully recover until the early 1990s despite strong demographics.

- The 2008 financial crisis.

- And finally now, ignoring the one-month blip that happened during the COVID lockdowns.

Note that prices lead sales. We can say that there have been three major down cycles in U.S. real estate over the past 50 years, and we're in our third one. If you line up the housing under construction graph from above with the existing home sales graph here, you can see that they turn at the same points.

If you own a home with a cheap mortgage, the rational thing to do is to hold on to it. Anywhere you move is likely to create a higher mortgage payment for you now, even if you downsize. Also, note that moving from one house to another doesn't actually create any housing supply since you're moving from one house to another (1-1=0). People staying put won't stop prices from falling, it will only delay it.

What's also interesting here is the lack of elasticity with many home buyers. If you'd told me in advance that interest rates would go from 3% to 8%, my guess would have been that home sales would be down 50% or more, not a third like they are. The housing market isn't completely frozen - people are still moving. Unfortunately for them, today's interest rates are making them quite house-poor compared with their older neighbors with 3% mortgages and low-cost basis. The fundamentals of what buyers are able to pay have changed in the housing market, which necessitates a fairly large, steady drop in home prices. To get back to equilibrium, either buyer incomes have to skyrocket (not happening), interest rates have to fall back to COVID levels, or prices have to fall. Prices falling is the most likely outcome by far. The debt-to-income data also shows that millions of people are putting themselves in an unusually precarious position by getting mortgages with higher and higher DTI ratios.

It seems to me that of the 6 million people who would ordinarily buy a house in a year, a little over 1/3 of them are running the numbers and deciding not to put themselves through the wringer. Many of the other 2/3rds might be doing what they're expected to do socially with no consideration for price and value. This mentality led to disastrous consequences in 2007 and 2008. There's no need to force anything as the same forces that are making buying a house exponentially more expensive are making it cheaper to rent, or simply travel the world with the strong dollar. As the old adage goes, don't fight the Fed, and perhaps don't try to compete for loanable funds with a Congress that needs to borrow trillions of dollars per year.

Bottom Line

Mortgages just topped 8%, mirroring a trend in the broader economy where financing is becoming much harder to get. If you don't think this will affect the housing market, think again. Other casualties of rapidly-rising interest rates may include money-losing junk-rated companies, regional banks, and automakers. Will mortgage rates hit 9%? What would the consequences be? Share your thoughts in the comment section below.

For further details see:

30-Year Fixed Mortgage Tops 8%: Interest Rate Landslide Continues