ET - 4 Awesome High-Yield Stocks I Am Buying

Summary

- After focusing on dividend growth stocks in prior articles, it's now time to discuss high-yield opportunities, especially in light of economic developments.

- As I believe that we'll see a total return shift from capital returns to income returns, I think it is important to consider high-quality high-yield stocks.

- I present four stocks with varying high yields. I own two of them and might end up owning all of them at the end of this year.

Introduction

It's time to talk about high-yield investments - real high-yield stocks, with yields between 4% and 10%. Over the past few months, we have discussed several model portfolios, which included dividend growth investing and my dividend growth portfolio . One of the most requested topics is to finally do an article on high-yield investing with satisfying yields. While I occasionally cover high-yield investments, I have neglected that area a bit due to my focus on dividend growth over very high yields.

In this article, I will give you four high-yield investments with dividend yields between 4% and 10%. Not only that, all of these investments are either in my portfolio or on my watchlist.

But first, some background info.

Buying High-Yield Makes Sense - But Pitfalls Can Be Nasty

My dividend (growth) portfolio yields close to 2.7%, which isn't a lot. It's not what can be defined as a high-yield portfolio. And that's fine, as I didn't have the goal to rely on income from my investments right from the start.

However, I've always had the goal to include some high-yield in my portfolio. Not only does buying quality high-yields make sense in some situations, but I also need it for tax purposes, as I pay a tax on my total net worth instead of capital gains. So, if I don't sell assets, I will have to get some cash flows to satisfy my government.

Anyway, there are essentially two reasons to buy high-yield stocks.

- Generating a higher income from your assets.

- Buying assets that can outperform the market.

The first one is obvious. Once you have a certain amount of money, you can let it work in your favor. For example, selling some of your low-yield dividend growth stocks and putting the proceeds into high-yield investments might allow you to retire, as cash flows cover more than 100% of your costs.

The higher the yield, the more cash you receive. Again, that's obvious.

However, there's also a second reason to buy these assets: outperformance. Unfortunately, this one is a bit less straightforward. It also comes with pitfalls, which is why I'm covering it.

After all, a dividend does not create wealth.

Wait, what?

A dividend is nothing else than a distribution of cash from a corporation to an individual. The company ends up with a lower cash balance. The investors end up with a higher cash balance. The only difference is that the government got a cut (dividend tax). In other words, paying a dividend ended up destroying value.

{kind=link}

However, that's where the bad news ends. While the transaction itself might not create value, the fact that a company can distribute a dividend is what creates value.

Being able to distribute a dividend is a sign of strength. It also offers investors safety in times of economic trouble, which leads to dividend (growth) portfolios offering outperforming returns with subdued volatility. Even if dividend stocks do not outperform in every bull market, downside protection in bear markets is a big part of long-term outperformance.

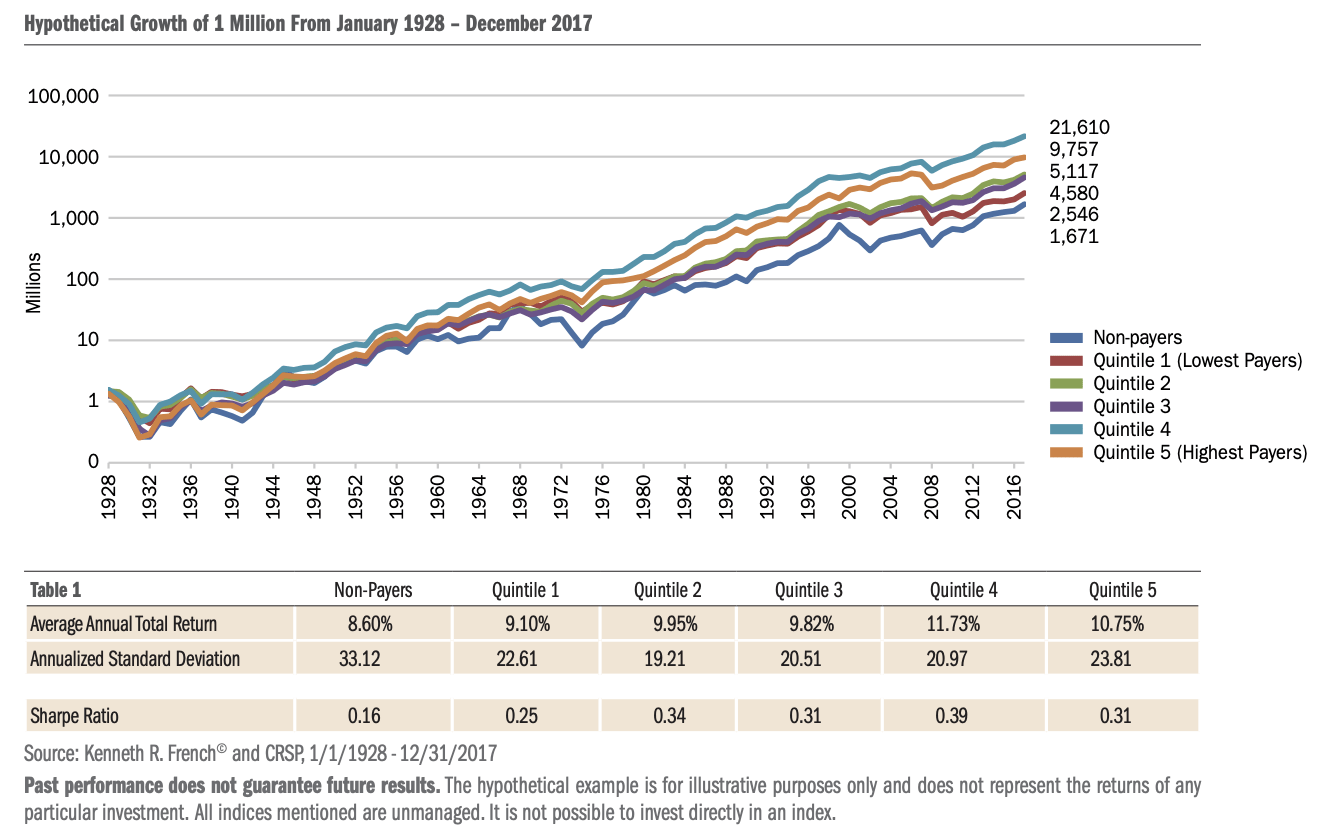

The data below confirms that the higher the yield, the lower the average drawdown.

It is essentially about total returns. As the Vanguard chart above shows, stocks with the highest yields have similar returns to stocks with the lowest yields. The only difference is that half of the total returns come from income returns.

Moreover, and concerning the aforementioned low-volatility outperformance, as the chart below shows, the higher the dividend, the higher the total return and the lower the standard deviation.

{kind=link}

The data below confirms that the higher the yield, the lower the average drawdown.

{kind=link}

However, it's not a linear function. It's not like a stock yielding 20% or higher is going to be the holy grail of investing. As the data above shows, the sweet spot is somewhere between the third and fifth quartile when it comes to achieving the best total return. In other words, it's high yield, but not *that* high.

After all, a lot of very high-yielding investments have terrible total returns. Most of these companies are so mature that growth is completely gone. Or they are investment vehicles like AGNC Investment Corp ( AGNC ) that pay a high double-digit return but come with terrible total returns.

Please note that AGNC is just an example. I have nothing against AGNC. It might be a good play for investors seeking high income, which brings me back to my point.

Before buying random high-yield, be aware of your needs. As much fun as it is to get a lot of cash from your investments, young(er) investors should also incorporate the risks that come with buying mature companies over companies capable of growing over time.

This is something I incorporated in the stock picks I'm about to show you.

With that said, on top of tax reasons, I'm increasingly incorporating high yield as I do not believe in the quick return to market conditions we witnessed between 2009 and 2021. The endless uptrend fueled by cheap money might be over for a while, as I discussed in this article .

{kind=link}

In other words, if expected longer-term capital returns are expected to be low, we need to shift our focus a bit more toward income returns. This means buying more high-yield.

Here are four stocks that you might like.

1. Energy Transfer LP ( ET ) - 8.3% Yield

Let's start this article with the highest-yielding stocks. 8.3% is something to write home about. A $10,000 investment ends up paying you $830 per year before taxes.

The company is a limited partnership . It does not pay any federal income. To qualify as MLP, a company must generate 90% of its income from minerals and natural resources. Shareholders are called unit holders.

MLPs are set up by their partnership agreements to distribute the majority of their cash flow to shareholders, officially called unitholders. This cash flow is what makes MLPs attractive to investors. Most partnerships forecast what they expect to distribute in cash over the next 12 months, which offers some level of predictability for unit holders.

On a side note, this is also why not all foreign investors might be able to buy ET. Some European brokers allow me to buy ET, while others don't. So, please be aware of that. The same goes for the implications this may have for your tax situation. That's not something I can cover, as it varies per follower/country.

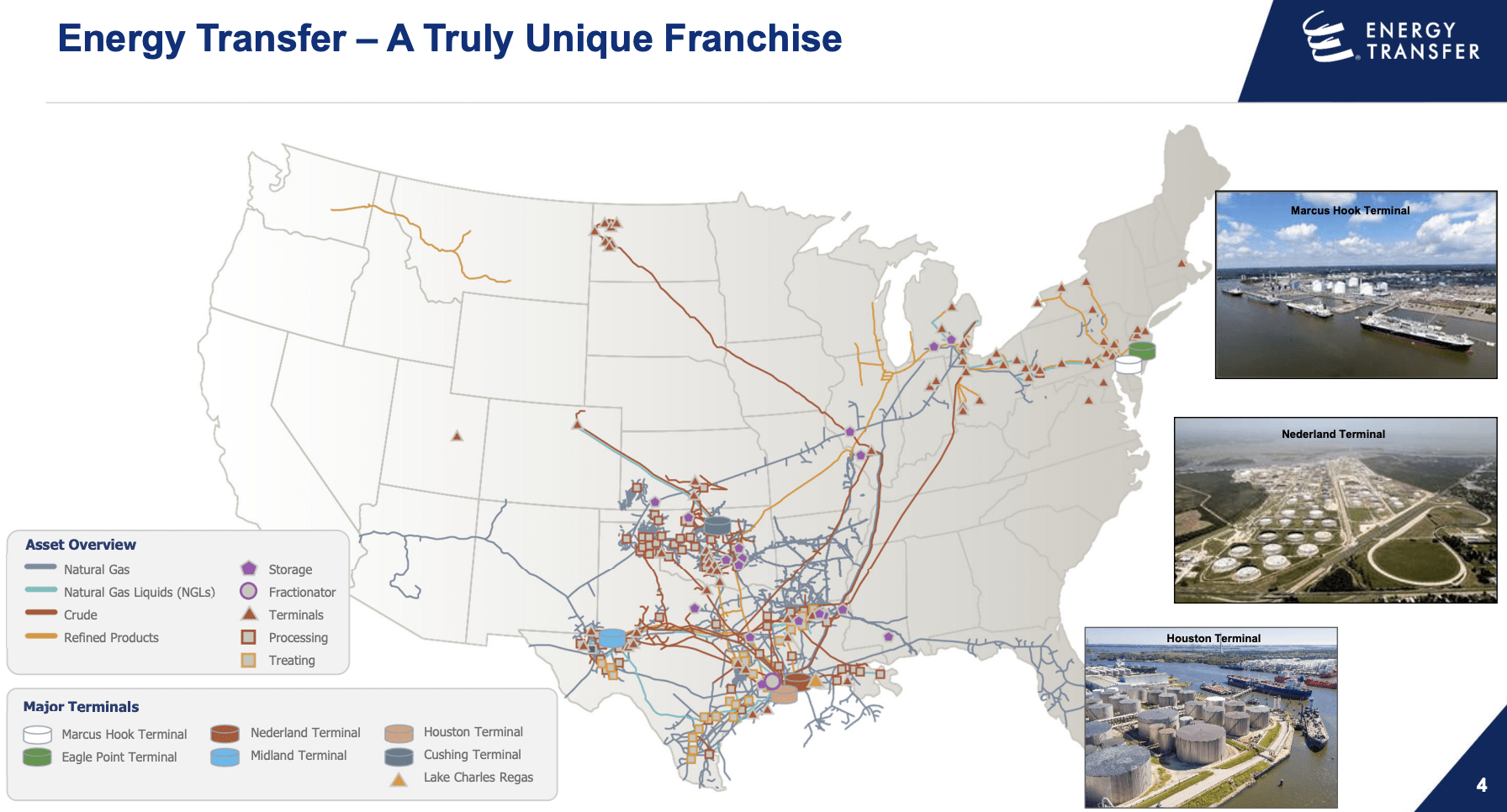

In this case, we're dealing with an energy giant with a market cap of roughly $40 billion. Dallas-based Energy Transfer is an oil & gas midstream company. Midstream is the step between upstream and downstream, meaning it builds, maintains, and owns pipelines and storage facilities for various fossil fuels, chemicals, and related products.

{kind=link}

The company generates between 85% and 90% of its EBITDA from fees. Moreover, it has a highly diversified customer base, allowing it to benefit from more than just high oil production in the South. The company has access to the highest-margin basins, access to export facilities, all major U.S. natural gas basins, and the largest intrastate pipeline system in the US.

{kind=link}

Hence, it not only benefits from high (and rising) international natural gas demand and high oil production but also from an ever-increasing need for specialty and refined products. I think the demand for this grows even faster as supply chains relocate to North America.

The problem is that the company is extremely cyclical. When oil prices crashed in 2015 (before the merger with Energy Transfer Equity), the stock plummeted from $35 to $5. Something similar happened during the pandemic when management cut the dividend by 50%.

The good news is that the company is now back in a good spot. It raised its dividend by 15% in October, bringing the dividend close to pre-pandemic levels.

Moreover, since the pandemic, the company has become more mature. Its investment needs have gone down, allowing for positive free cash flow and rapidly declining leverage. A quick and dirty assumption of $6.0 billion in annual free cash flow gives us a 15% free cash flow yield. That's terrific news for the dividend, potential buybacks, and balance sheet debt reduction.

{kind=link}

Number two also has a very high yield, and it also cut its dividend in 2020. Yet, it's one of my favorite high-yields.

2. Apple Hospitality REIT ( APLE ) - 5.7% Yield

In my quest for more real estate exposure, I ended up putting the APLE ticker on my watchlist, as I've followed this company for years.

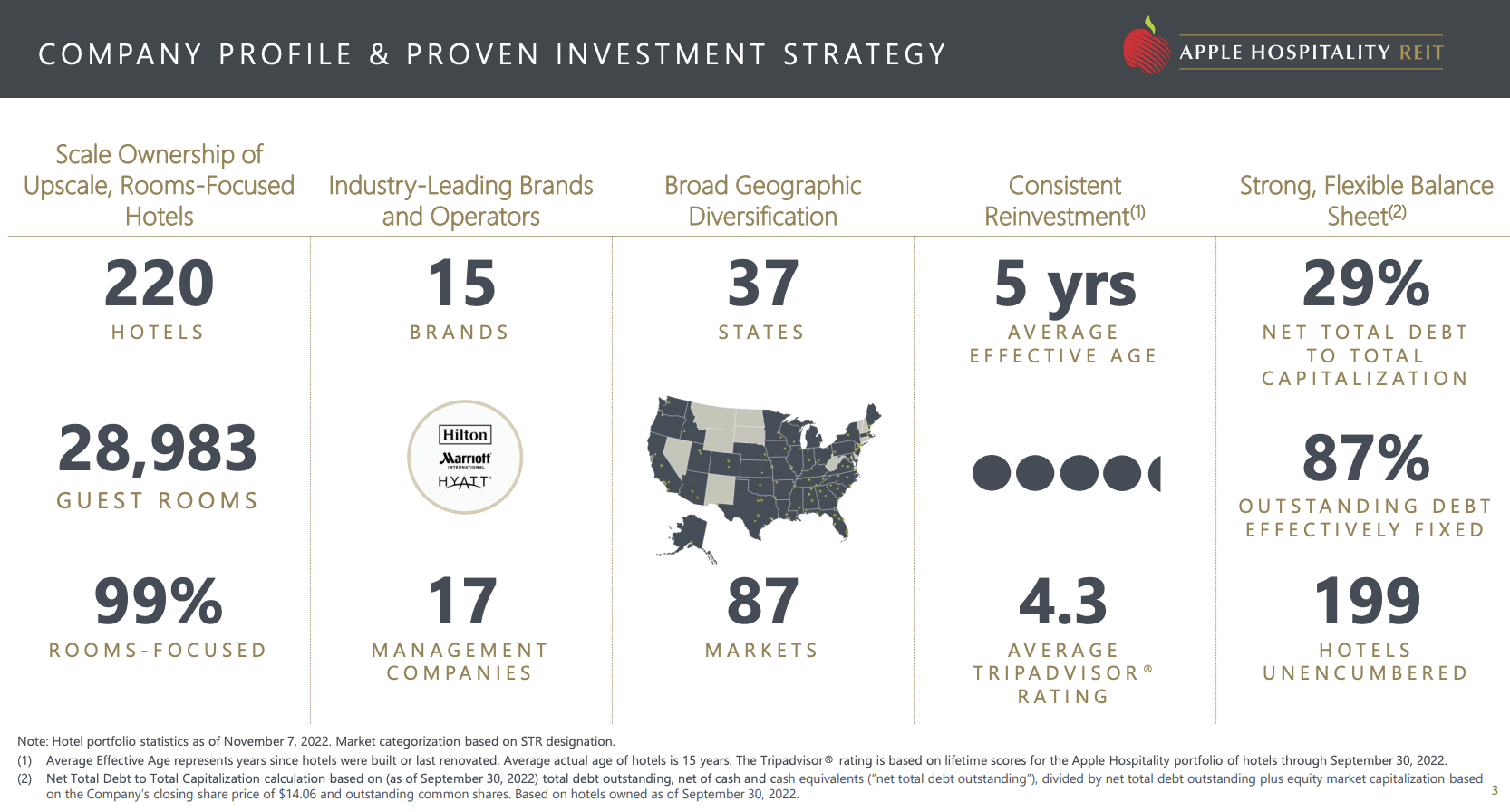

Like Energy Transfer, Apple Hospitality is also cyclical. The company is a giant in the hotel industry as it owns 220 hotels in 37 states, covering 15 brands in 87 markets. This includes close to 29,000 guest rooms. The company is 99% room-focused, meaning it is not exposed to events and other related things.

{kind=link}

Moreover, its hotels are upscale, as its main three brands are Hilton, Marriott, and Hyatt.

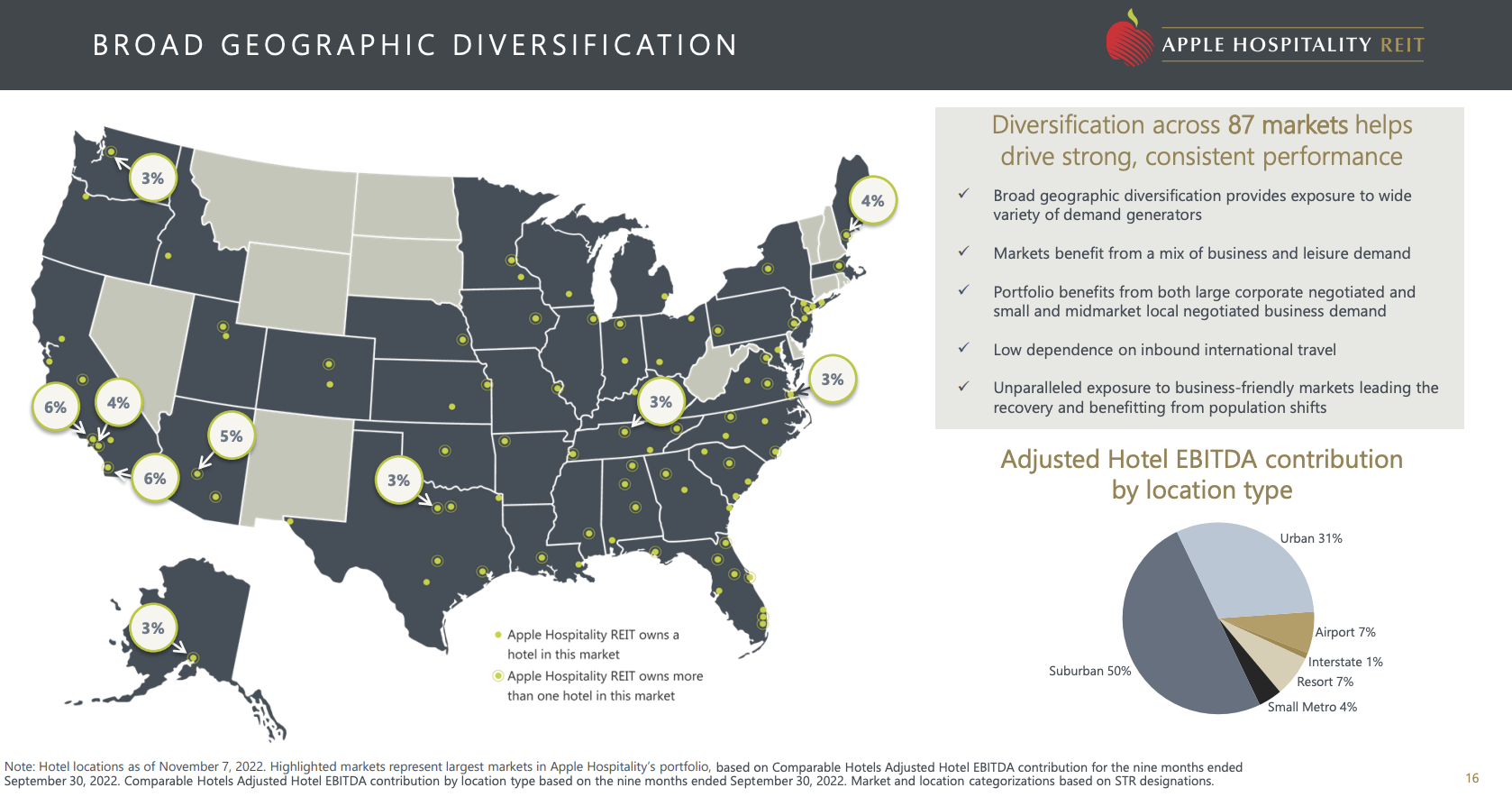

Its portfolio is well-diversified, with high suburban exposure in all major metropolitan areas in the United States.

{kind=link}

Its assets are managed by 27 management companies. The largest is the LBAM-Investor Group, managing 34 properties.

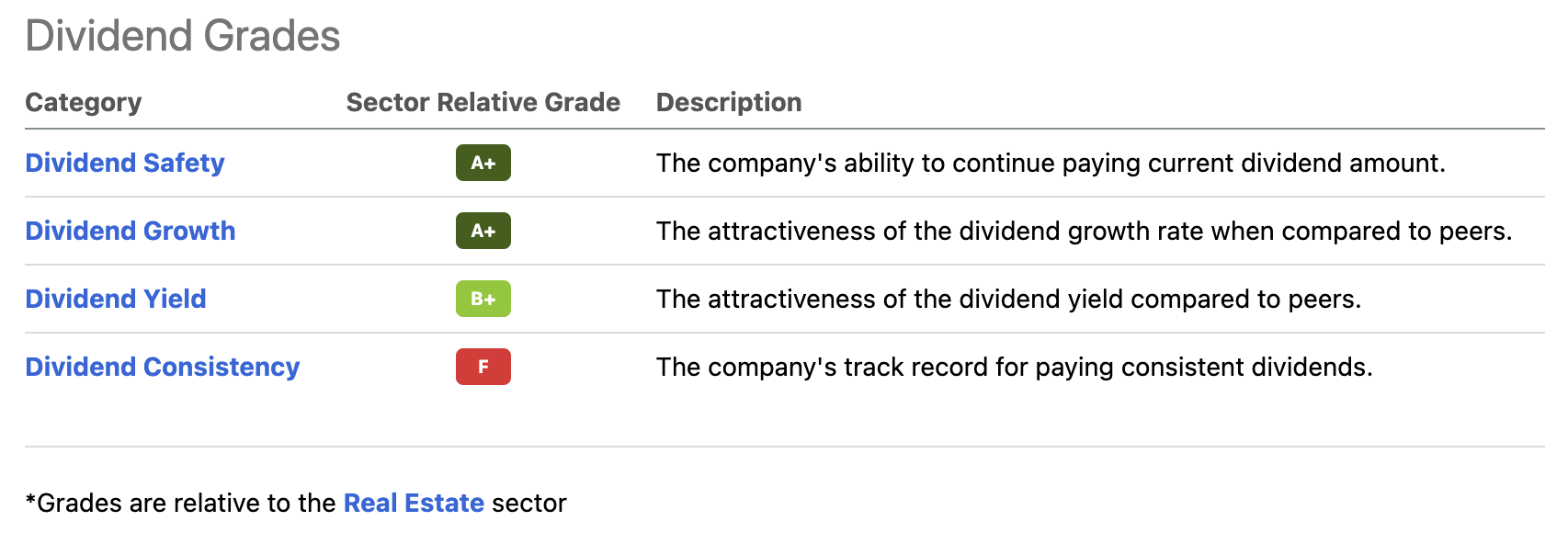

The company has a mixed Seeking Alpha dividend scorecard. It scores very high on dividend safety and dividend growth. Dividend consistency is a big fat F.

{kind=link}

The company currently yields 5.7%. This monthly dividend payer is recovering from the pandemic as it cut its dividend in 2020, as it was dealing with empty hotels and high uncertainty.

Before we got bad news in early 2020, the company was paying $0.10 per month per share. Now, we're back at $0.08. Please note that the spike in the chart below is a special dividend of $0.08 paid in December 2022.

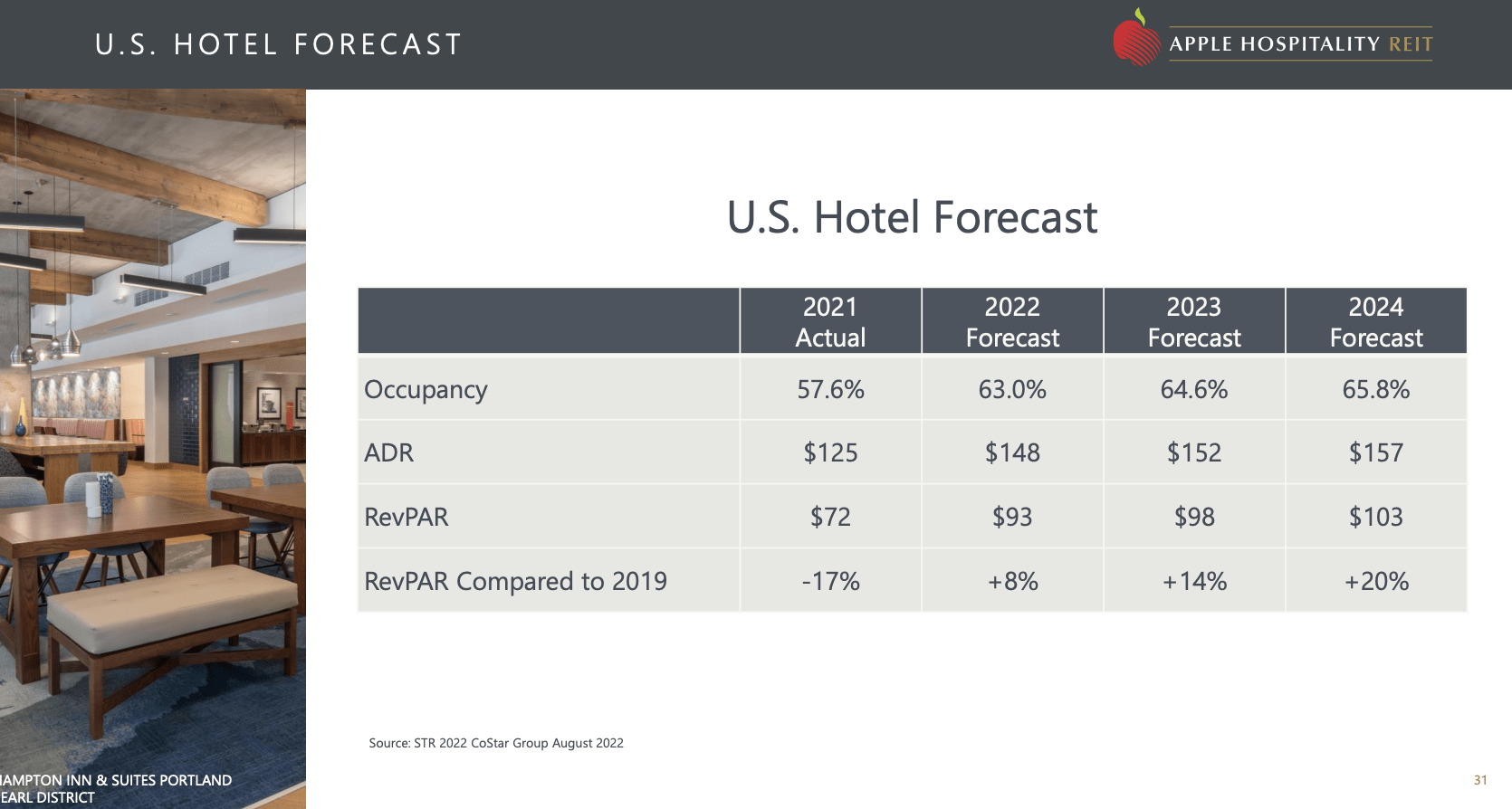

The odds are high that dividends will normalize. Occupancy rates are rebounding and are expected to remain strong. The same goes for revenue per available room, which could end up being 14% higher in 2023 compared to 2019.

{kind=link}

Moreover, the AFFO (adjusted funds from operations) payout ratio is 42%, which is well below the sector median of 73%.

I like APLE a lot, yet I have to mention that its business is cyclical. If a very severe recession were to hit, dividend cuts might be used to protect financials.

The likelihood of large cuts is low. The company caters to higher-income clients and has done rather well in prior downswings. The pandemic was different, as it was a government-mandated shutdown.

Number three is way more defensive and an actual dividend king.

3. AbbVie ( ABBV ) - 4.0% Yield

A dividend king is a company that has hiked its dividend for at least 50 consecutive years. AbbVie is a dividend king, although a "*" applies.

AbbVie used to be part of Abbott Laboratories ( ABT ) until the company announced to spin off its research-based pharmaceutical manufacturing assets.

This separation was effective on January 1, 2013.

As Abbott is a dividend king, AbbVie is a dividend king as well, as it has raised its dividend every year since the spin-off. In other words, pre-spin-off investors did not miss out on anything.

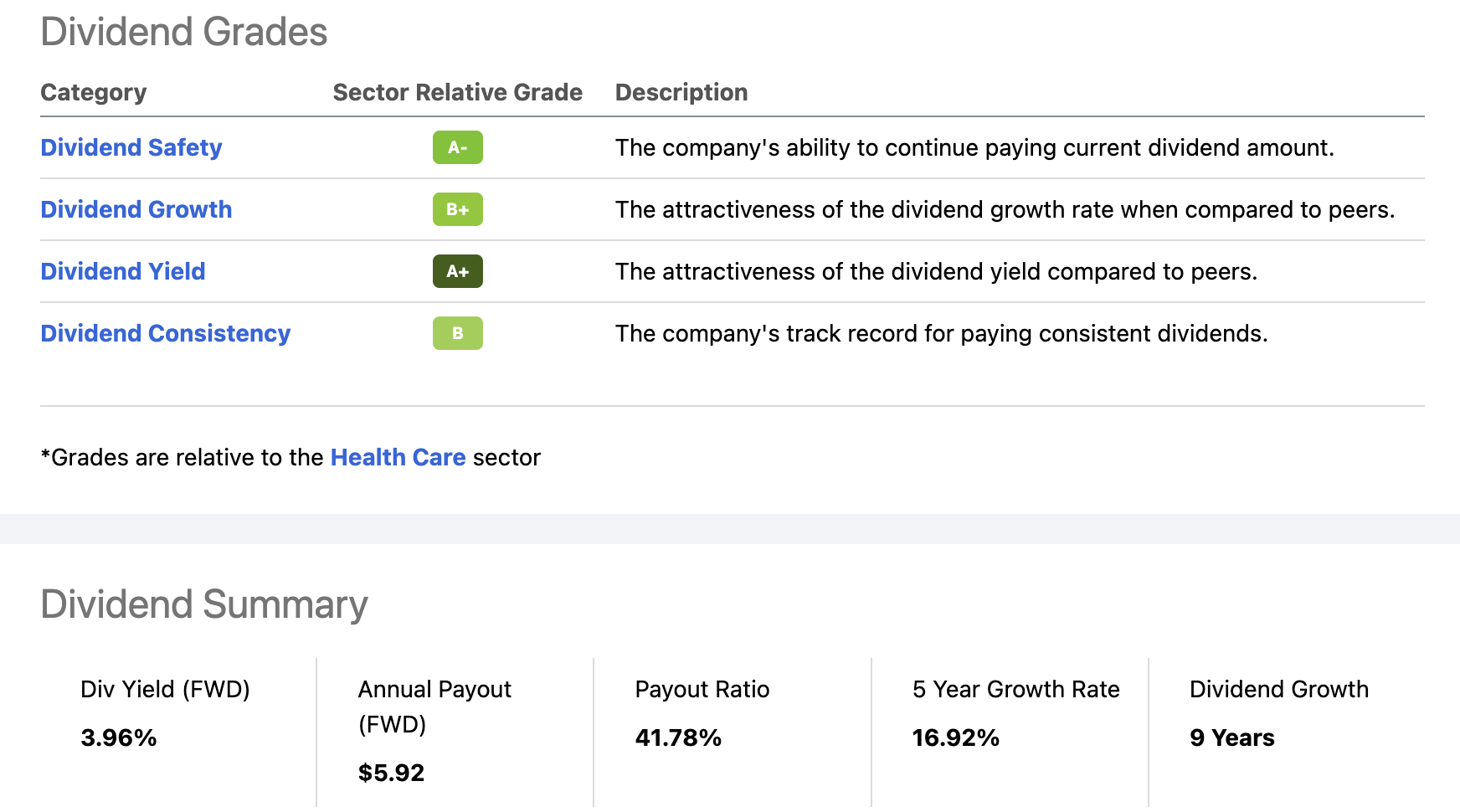

As the Seeking Alpha dividend scorecard shows, the company scores high on its yield, high on safety, and somewhat high on growth and consistency. Needless to say, I disagree with consistency. That should be a big fat A+. However, the numbers are automatically generated, and spin-offs are not incorporated.

{kind=link}

The 5-year average annual dividend growth rate is 17%. That number has come down to 9% over the past three years, which is very decent. It's also backed by high dividend safety, as the payout ratio is 45%.

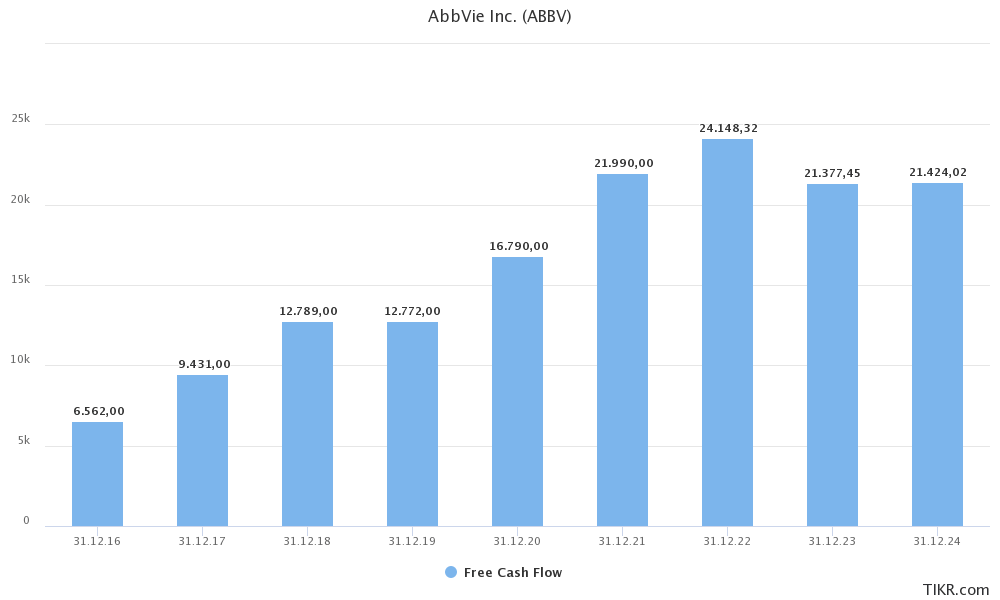

Using the expected free cash flow of $21 billion in 2023 and 2024, we're dealing with an implied FCF yield of 8.0%, which implies a 50% cash payout ratio.

{kind=link}

One of the issues facing ABBV is that its best-selling product Humira will lose patent protection this year. This is a common problem in the healthcare sector.

Humira (part of the immunology division that generated 45% of 2021 sales), which is used to treat rheumatoid arthritis, could do $20 billion in sales this year.

Seeking Alpha contributor Edmund Ingham recently covered the stock, focusing on the Humira impact.

AbbVie will have to drop its price point to compete with the generics however, plus there is the 10% of the market it is not covered for, so an overall 20% decline in revenues in 2023 seems accurate. In my model I have then reduced revenues by 20% between 2024 - 2026, and then by 10% per annum between 2027 - 2030.

This means that the drug will remain a cash cow, even if growth rates are negative.

Even better, there are good alternatives as he writes in his article, citing the company:

Skyrizi and Rinvoq are now on pace to deliver more than $17.5 billion in combined sales, risk adjusted sales in 2025, well above our previous expectations. We now expect global sales for Skyrizi to reach more than $10 billion in 2025, an increase of $2.5 billion versus our previous guidance, reflecting higher performance across basically all of the indications.

As we look beyond 2025, we expect combined sales for Skyrizi and Rinvoq to exceed the peak revenues achieved by Humira, which was more than $21 billion. We expect that to happen in 2027 with continued significant growth anticipated in the following years.

Hence, I'm not that worried. I like that ABBV offers strong and consistent dividend growth, a recession-proof business model, and an outlook of high growth, even if the next couple of years might see subdued growth rates.

Now onto number four, a stock with a similar yield.

4. Extra Space Storage ( EXR ) - 4.0% Yield

Extra Space Storage is one of my all-time favorite real estate investment trusts ("REIT"). I had the stock in my portfolio in early 2020. When I started my dividend growth portfolio in the summer of 2020, I did not include EXR for some reason (a big mistake!).

Last year, I finally added the stock to my portfolio, which means I now own two REITs. The other is its peer Public Storage ( PSA ).

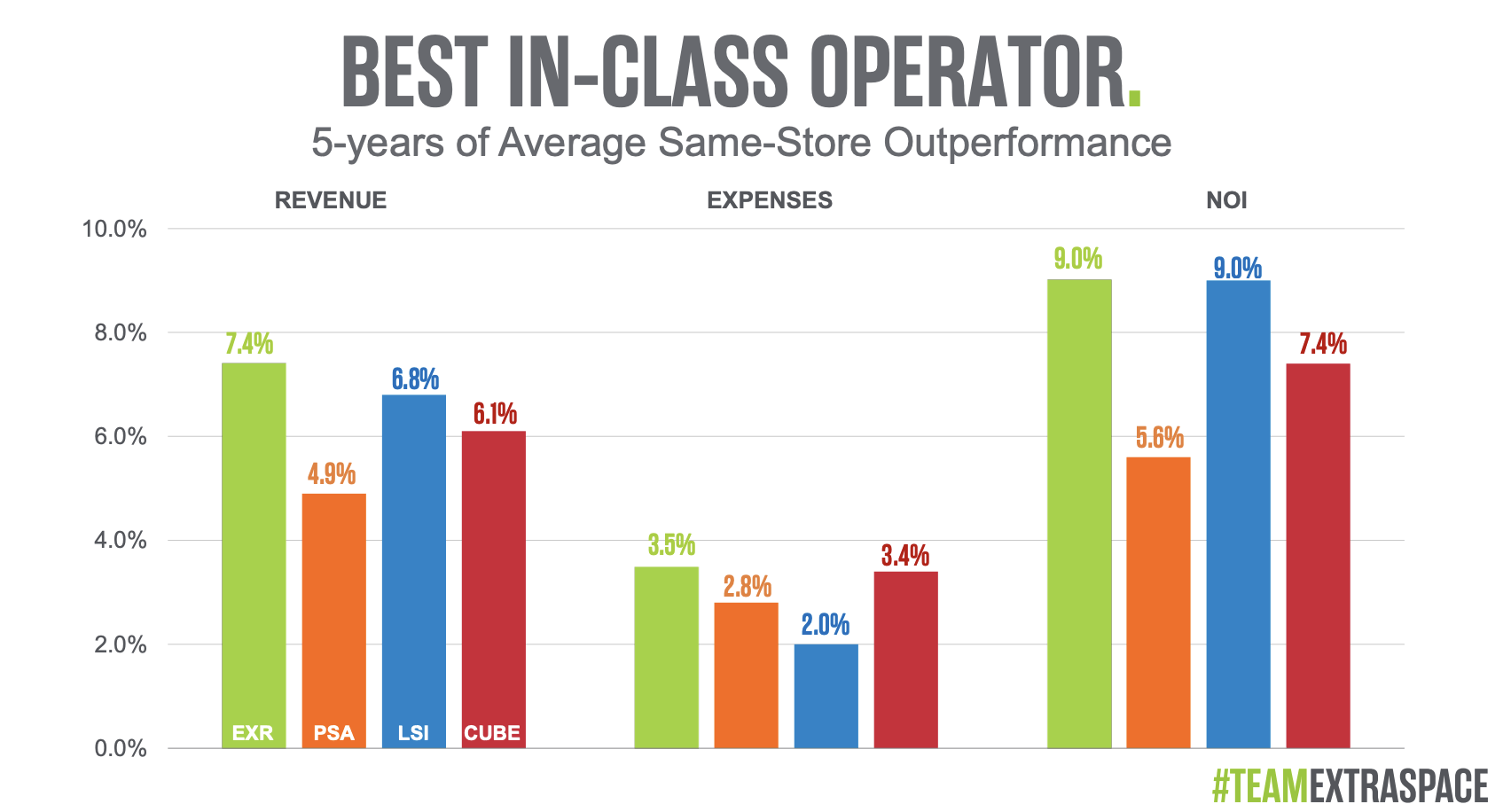

Extra Space Storage is one of America's largest real estate companies and the second-largest self-storage operator. The company operates in 41 states where it owns and manages 1.6 million units. Unlike smaller self-storage REITs, the company is well-diversified with no more than 16% sales exposure in the Northeast and California.

{kind=link}

In addition to adding new properties, the company has outperformed most of its peers over the past five years when it comes to net operating income growth. Despite above-average growth in expenses, the company generated 9.0% compounding annual sales growth.

{kind=link}

Over the past ten years, the EXR ticker returned 451%, which beat its closest competitor by almost 140 points.

Now, the stock is 35% below its all-time high, which has pushed the dividend yield to 4.0%.

This yield is now above the longer-term median - excluding the years before the Great Financial Crisis.

Moreover, dividend growth is strong. The 10-year average annual dividend growth rate is 21.6%. The five-year average is 14.0%.

These are the most "recent" hikes:

- February 2022: 20.0%

- August 2021: 25.0%

- February 2021: 11.1%

- May 2019: 4.7%

The AFFO payout ratio is 74%, which is in line with the industry.

Going forward, I expect dividend growth to slow a bit as pricing tailwinds have eased. The same goes for property values.

Meanwhile, rates have gone up.

The good news is that EXR has a fantastic balance sheet. It has a 6.7x interest coverage ratio, a 6.2x fixed charge ratio, a weighted interest rate of just 3.6%, $1.4 billion in available liquidity (revolver capacity), and a net leverage ratio of just 4.6x.

The weighted average maturity is 5.5 years, which buys the company a lot of time.

Takeaway

In this article, we discussed why it makes sense to buy high-yield investments, and the risks to bear in mind. Given my view on the market, I believe that it makes sense for investors to buy high-yield investments. I think we'll see a shift from capital gains to income gains when it comes to the total return picture.

Hence, I presented four dividend stocks with high yields. I like all of them a lot and believe that the valuations are good. However, I'm not sure that all of them have bottomed. The market is currently pricing in a very dovish Fed, which I believe is a risky bet, especially as inflation remains persistent.

While we're almost certainly beyond peak inflation, it will be much harder to get inflation from 4% to 2% than from 8% to 6%. Hence, I think it's premature to price in a very dovish Fed. That's also why I believe in new buying opportunities down the road.

My strategy is to buy stocks as soon as opportunities present themselves. I'm closely watching all stocks discussed in this article. If the market shows weakness, I am a buyer for sure.

That said, what do you think of these picks? Do you own some of them? Let us know your thoughts!

For further details see:

4 Awesome High-Yield Stocks I Am Buying