CA - 4% Cap Rates In Office Properties Must Be A Dream

2023-04-14 09:19:51 ET

Summary

- Dream Office has moved lower since our last article.

- Q4-2022 performance was actually quite sturdy and they sold a property at a stunning 4% cap rate.

- We look at the numbers and update our thesis.

All values are in CAD unless noted otherwise.

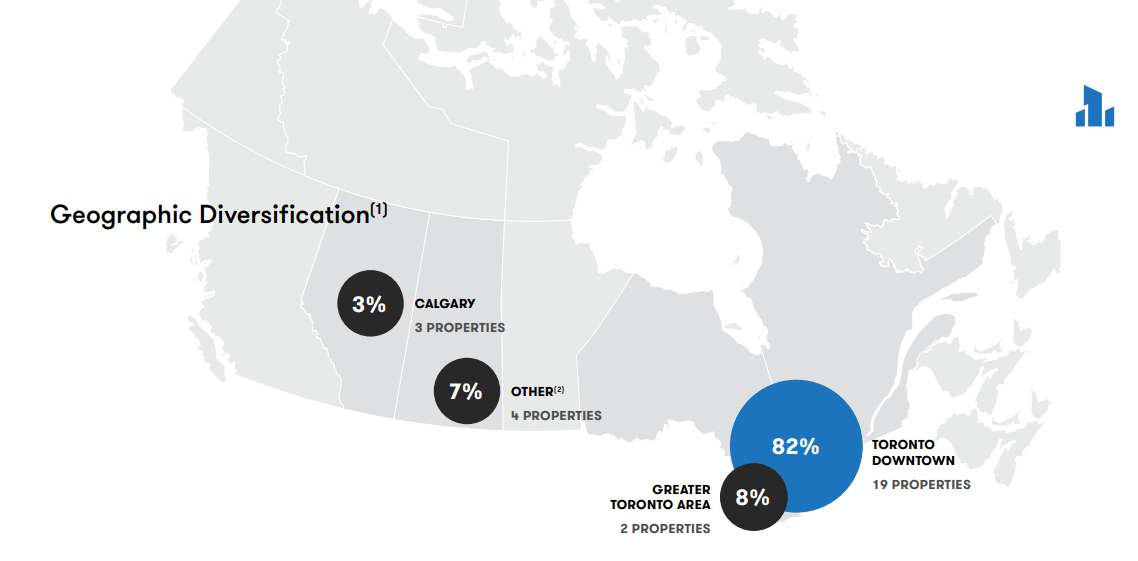

When we last covered Dream Office Real Estate Investment Trust (DRETF) (D.UN:CA), it had a portfolio of 26 active office properties, 2 properties under development and one held for sale. There was another and that was held as part of a joint venture. Majority of the 28 property portfolio was located in downtown Toronto (82% of the portfolio fair value), with Saskatchewan and Kansas making up the "other" in the graphic below.

{kind=link}

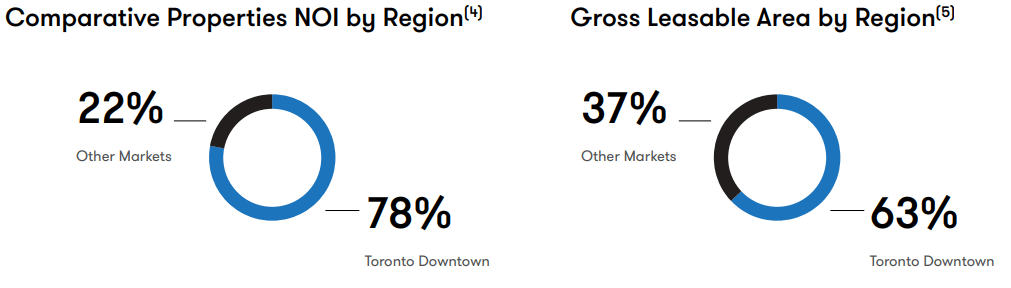

The picture did not look vastly different when viewed from the net operating margin [NOI] or GLA lenses.

{kind=link}

We gave this REIT a neutral rating back in January as we were not on the same page as the management regarding the fair value of the portfolio. Our thinking was more in line with the 7% capitalization rate implied by the then stock price of $15.21.

The implied cap rate based on the current stock price for Dream, is about 7%. What we mean here is that if the properties were sold at a 7% cap rate, shareholders would get about $15 after paying off the debt. That actually looks about in line with what we think is fair. Similarly, the well covered (payout ratio 65%) 6.8% dividend yield looks enticing, but again, we think that is the minimum margin of safety you need here. So while the company believes the shares are heavily discounted, we think they are properly priced. We are rating the stock as Hold and prefer to play office space via diversified REITs having a heavy offering of industrial and or residential space.

Source: Dream Office: A Look At That 60% Discount To NAV

We are revisiting this stock today because the property that was held for sale was sold in Q1 and it was an impressive deal. Granted it was only a fraction (0.3 million) of the total 5.4 million square feet GLA, but it got our attention. Since our prior thesis was predicated on our disbelief regarding the valuation of the office properties, we take a closer look at the sale to see if a change in rating is warranted.

Q4-2022 Results

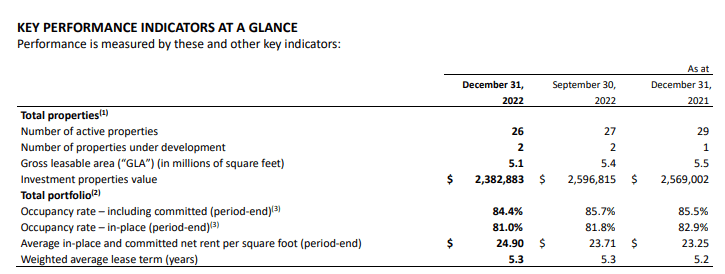

The REITs' Q4-2022 performance was solid with funds from operations coming slightly ahead of expectations at 37 cents a share. The longer term metrics were slightly less impressive. Occupancy rate including committed area, was a bit lower at 84.4%.

{kind=link}

This was slightly offset by the longer lease term and a slightly higher net rent per square foot. The drop in occupancy was due to a sale of a Class B property on 720 Bay Street.

{kind=link}

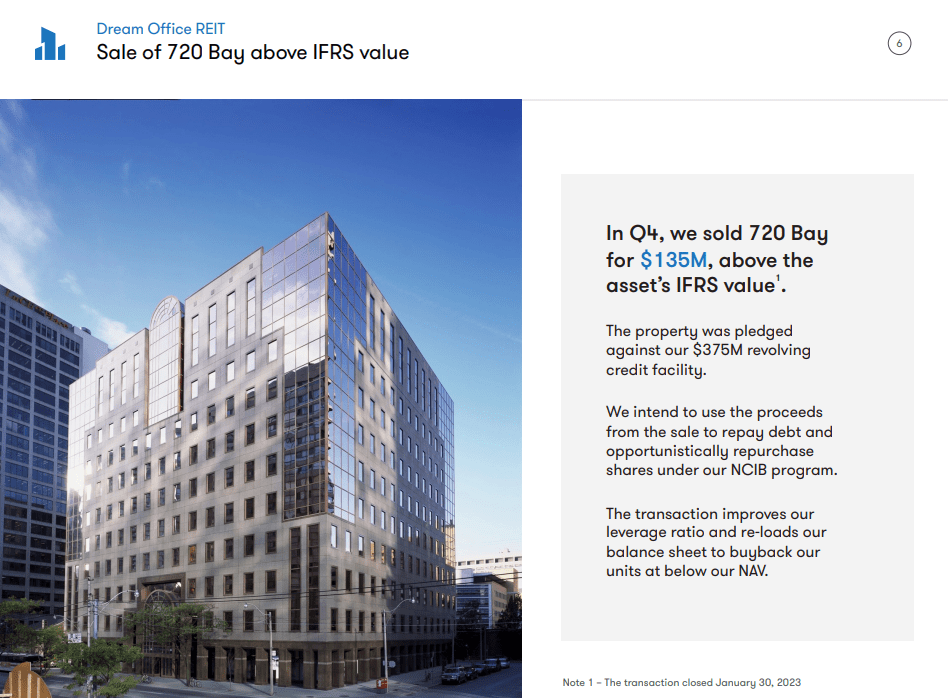

This was fully occupied by the Government of Canada but with just 3 years left on the lease. The cap rate was a phenomenal 4%. That seemed a bit odd here considering even Dream Office's weighted average was 5.48%.

{kind=link}

That data shown above is excluding the 720 Bay Street asset and taking that out lifted the overall numbers.

Mario Saric

Okay. And then maybe one last housekeeping question for Jay. The quarter-over-quarter change in the cap rate, how much of that would have been attributable to the reclassification of 720 Bay?

Jay Jiang

So we back it out actually, and then so 720 Bay is carved out at 135, and then the remaining portfolio in downtown Toronto, I think, went up about 40 basis points. And I think on the carrying value, I think you can imply it back. If we had a gain, about $20 million, you can probably derive the cap rate that 720 Bay was held at.

Source: Q4-2022 Conference Call Transcript

According to Dream Office, this was a building likely to be modified in the future and used as a health science building. We have seen it referenced by some analysts that this was purchased by Alexandria Real Estate Equities Inc. ( ARE ), but we were unable to see a confirmation from Dream or ARE on this. ARE would make sense as they are the health science building specialists and they likely see value in converting this building. That conversion also explains the 4% cap rate. Here the short lease term left was a positive as ARE likely plans to get them to leave as soon as feasible to begin the work. The sale was great for Dream, but we think this generally a one-off event. While another asset may roll in the future at a similar rate, the bulk of the portfolio is not going to approach that. In fact we still remain skeptical of the bumped up cap rate of 5.48% (from 5.16%). Dream Office of course believes this number to be true and this is their side of the story.

By 2024, we intend to reduce debt-to-EBITDA to below ten times. Our net asset value per unit for Q4 was $31.36, based on a stabilized income cap rate of 5.1 for downtown Toronto and 7.6 for other markets, which is consistent in the cap rate surveys movements from appraisers and brokerage reports. This implies $600 a square foot in downtown Toronto and $225 a square foot in other markets, which we feel very comfortable with. We took five properties or 25% of the properties by fair value to third party appraisers in the fourth quarter. In addition performed detailed valuation analysis on the remaining assets consistent with the methodologies used in the appraisal process based on observable market inputs.

Source: Q4-2022 Conference Call Transcript

Valuation & Outlook

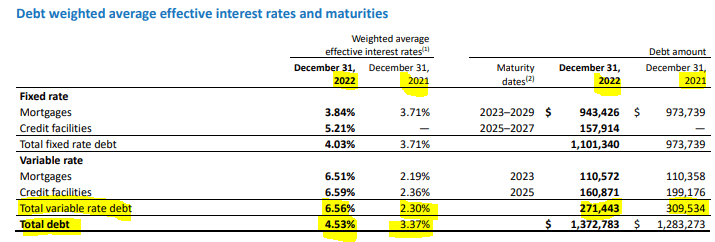

The positives here are that Dream Office is offsetting its slightly falling occupancy rates with mark ups on lease renewals. The FFO is expected to be flat year over year and that is impressive given the backdrop. Dream is also facing pressures on interest rates. At the end of Q4-2022, the weighted average rate was 4.53%.

{kind=link}

This is up substantially from last year's 3.37% and even from one quarter ago at 4.22%. This debt is also extremely short term in nature with a weighted average term of just over three years.

{kind=link}

The company has incorporated 2023 refinancing process into its guidance but risks remain very high over the next 3 years.

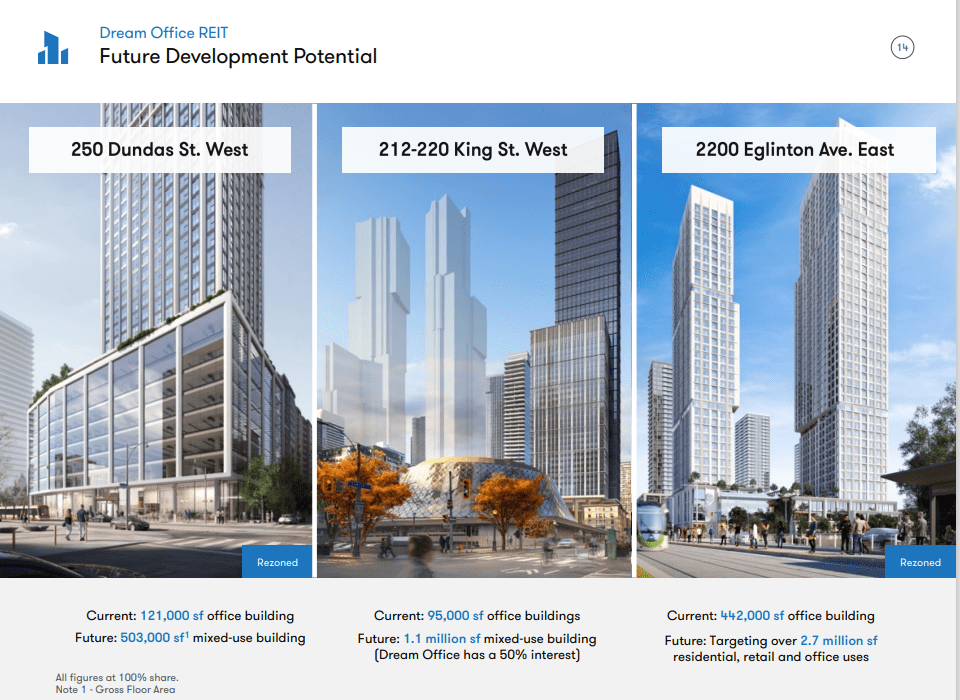

The plan is to continue to enhance buildings and add density where feasible.

{kind=link}

There was this bit of commentary on the conference call about potential of this down the line.

At 2200 Eglinton, we mentioned that we've received approval for about 2.5 million square feet of residential density for the most part in addition to the 165,000 square foot office building. Basically the density is divided into four phases, about 600,000 square feet each. We're in discussions now with the developer. We know very well for them to develop condos on the first phase and after cost the density probably at about $70 a foot. With 2.5 million square feet that's about $175 million plus 165,000 square foot office building. So once we get all the zoning done, once we get make progress on it the $110 million book value could become $200 million and that's an additional $2 a share basically.

Source: Q4-2022 Conference Call Transcript

An extension of this strategy was to bring high-end restaurants to its office buildings and 3 major openings are slated for 2023.

We're very proud to say today that we've completed four deals with arguably Canada's top restaurant tours that total over 30,000 square feet and two more conditional.

When completed, this will total approximately 45,000 square feet of total retail absorption at average rents close to $70 a square foot, and annualized NOI impact of an additional $3 million. These are all in our most desirable assets, completing and supporting our goal of bringing an elevated and all new experience of boutique luxury that is totally unique to Toronto's financial core. We're very proud to share today that we are bringing [Nelos] to Toronto. We are working very closely with owner, [Kostas Spiliotis] and his team. Nelos has grown from its roots in Montreal and is now one of the most sought after restaurant brands globally.

Q4-2022 Conference Call Transcript

While all of this remains an impressive portfolio of work, we remain skeptical as to how much it will offset the core valuation of the buildings.

Verdict

Avoiding a buy the last time around was a good decision and the REIT has steadily moved lower.

At the current price a couple of things stand out. The first being that the market capitalization is about $700 million and the Dream Industrial REIT's holdings total $400 million. Those holdings can be sold to reduce debt risks in the near term. Dream Industrial has certainly moved the right way and offset some of the risks of owning office properties.

If we back that out and adjust for the debt, the implied cap rate is close to 7.4%. That looks fair for the current market conditions and offers investors a good upside if office does come back. We still think this is not a compelling buy as the risks just don't offset the rewards. Investors have a slightly better risk-reward in H&R REIT (HR.UN:CA), (HRUFF) due to their large residential and industrial property holdings, and we even passed on that .

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

4% Cap Rates In Office Properties Must Be A Dream