UGI - 7%-Yielding UGI Corp: Discounted Dividend Aristocrat

2023-12-02 10:30:00 ET

Summary

- While the recent market rally may be disconcerting for value investors, plenty of discounted income stocks remain attractive.

- UGI Corp. is a compelling value stock with a steady business model and pays a high and well-covered dividend.

- Despite a decline in stock price, UGI has stable earnings, strong liquidity, and growth potential in the renewable natural gas market.

Value investors who buy for income typically want to see a stagnating share price so that they can accumulate while the stock is cheap. As such, the recent market rally may be disconcerting for those who aren’t yet done building their positions.

However, it’s worth keeping in mind that plenty of dividend stocks remain very cheap on a historical basis, and have only begun to recover from their deeply discounted prices over the past couple of months.

This brings me to UGI Corp. ( UGI ), which I last covered here back in August with a ‘Strong Buy’ rating, noting its capital discipline and attractive valuation. The stock price has declined by 9.4% despite an earnings beat in the last reported quarter.

While I can’t pinpoint a specific reason for the decline in price, I would surmise that high interest rates and the tech-fueled rally in favor of growth stocks might have something to do with it. In this article, I discuss why UGI remains a compelling value stock while the market is seemingly asleep on it, so let’s get started!

Why UGI?

UGI Corp. markets and distributes energy in the U.S. and Europe. Its utility operations serve West Virginia and Pennsylvania and assets include natural gas/electric generation and distribution, midstream services, propane distribution, and renewable natural gas generation.

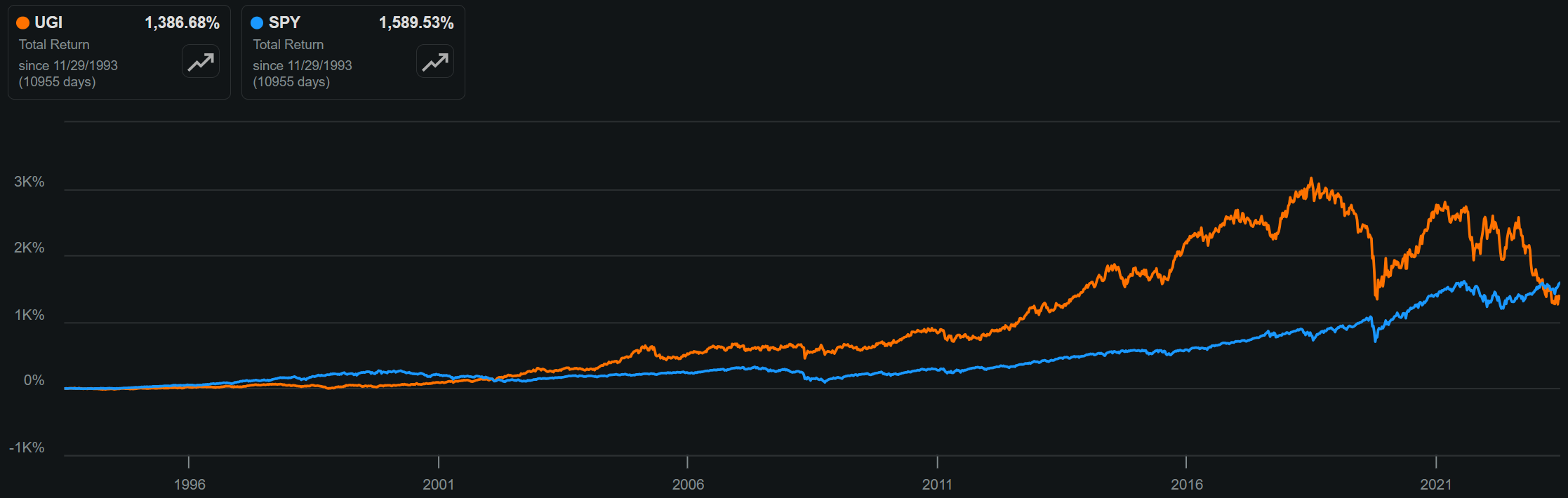

UGI’s perceived slow and steady business model has done well for investors over the long haul. This is reflected by its outperformance in terms of total return compared to the S&P 500 ( SPY ) over much of the past 30 years, as shown below.

{kind=link}

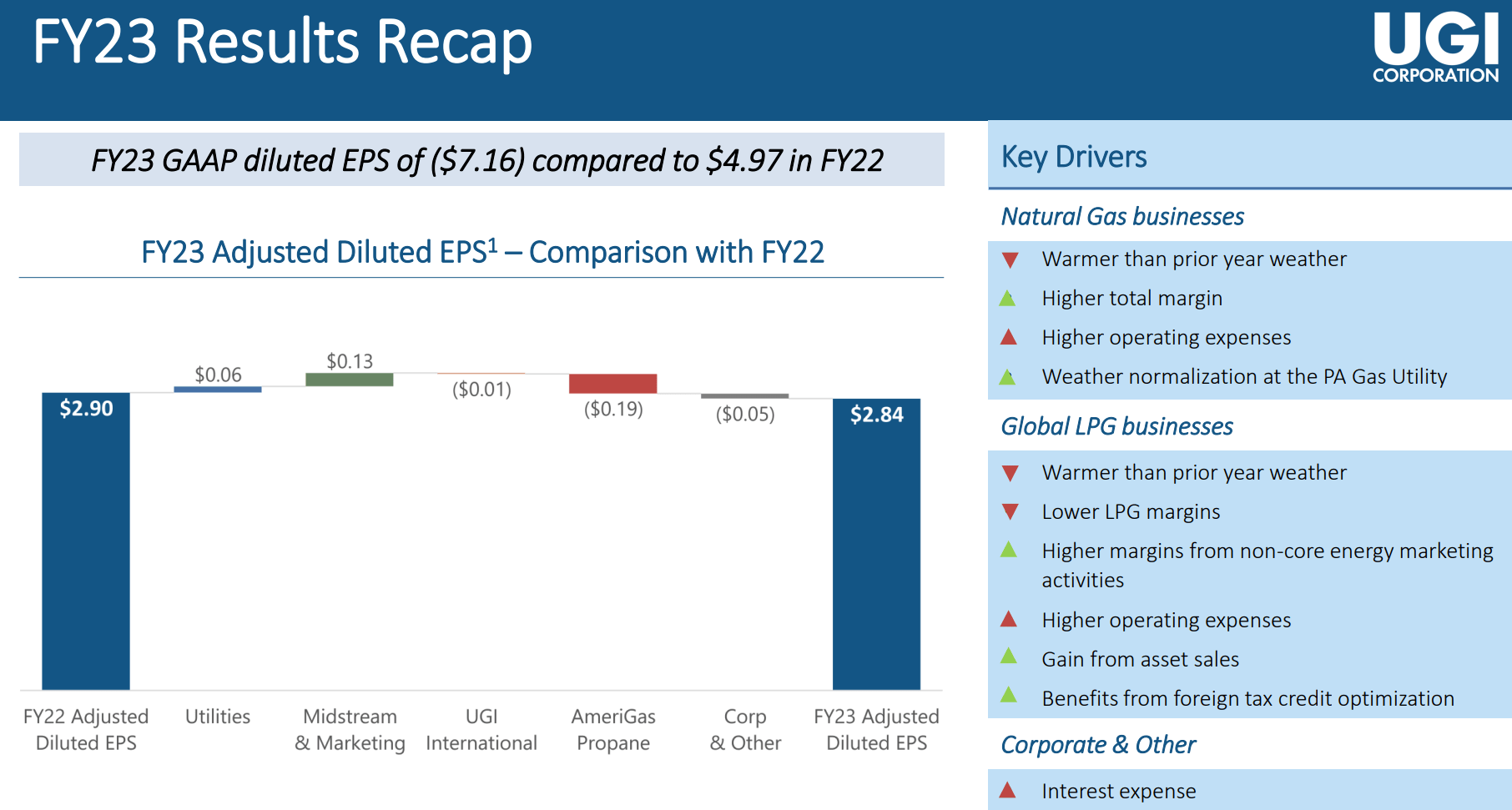

Based on UGI’s dismal price action of a 42% decline over the past 12 months, it would seem as if the sky was falling for UGI. However, that simply doesn’t appear to be the case considering record performance in its utilities and midstream & marketing operations in fiscal year 2023 (ended on September 30). This was driven by higher gas base rates and the weather normalization adjustment implemented at UGI’s Pennsylvania gas utility, as well as increased margins from natura gas gathering and processing activities.

Counter to what UGI’s stock price performance may suggest, its adjusted EPS was relatively stable, declining by just $0.06 YoY for the full fiscal year 2023. As shown below, much of the year-on-year decline was due to weakness in the AmeriGas Propane business, while utilities and midstream and marketing churned out positive results.

{kind=link}

Notably, UGI is seeing increased unit margins in its Global LPG business, which was partially offset by lower volumes, inflationary pressures, and continued investments into its AmeriGas subsidiary, which is the leading propane distributor in the U.S. Its worth noting that a decline in LPG volumes and staffing shortages at UGI’s AmeriGas segment posed a headwind for UGI’s bottom line, as reflected in in the chart above.

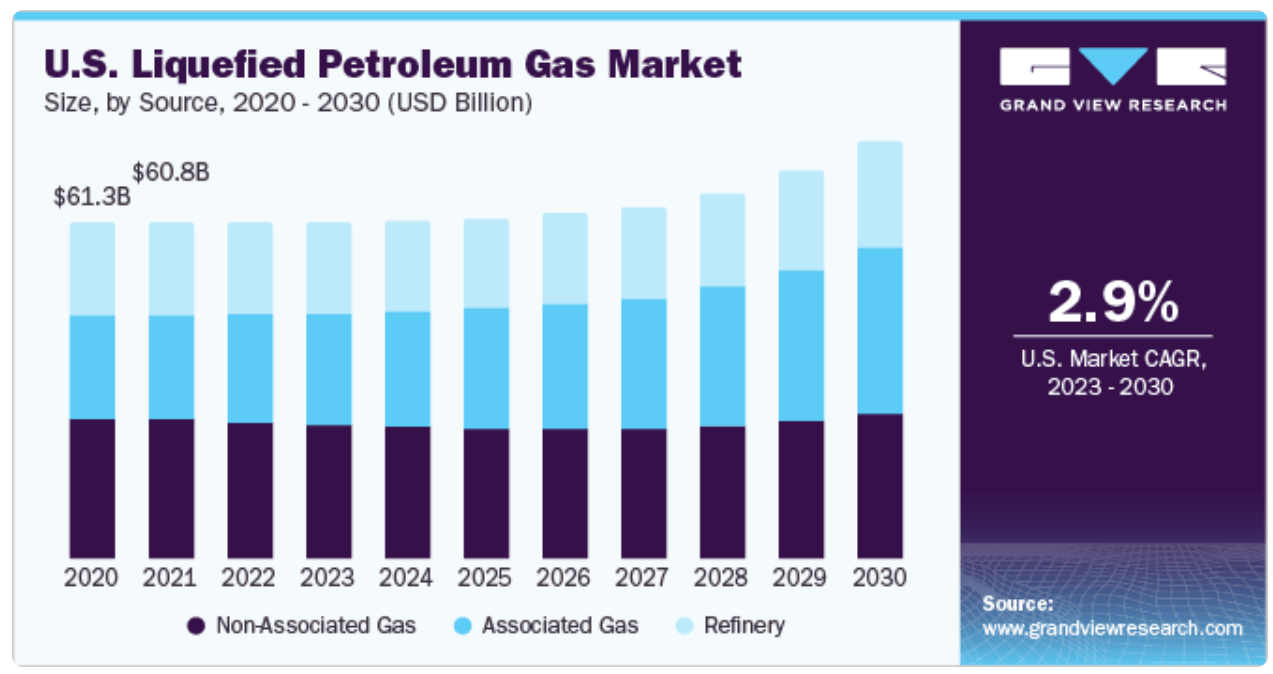

Despite near-term headwinds around LPG and concerns around the end of fossil fuels, LPG is a cleaner burning option that’s designed to wean the world off of dirtier fossil fuels such as kerosene, wood, and coal. In the U.S. market alone, the LGP market is expected to see a 2.9% CAGR in volume between now and the end of the decade, as shown below, and I would expect for UGI to benefit from this trend over the long run.

{kind=link}

Looking ahead, UGI is well-positioned to benefit from customer additions in its key markets and from external growth prospects. This includes two renewable natural gas projects currently in progress and the completion of two projects in upstate New York. RNG projects provide UGI with a sustainable source of energy, with the recently two completed facilities providing 140 million cubic feet of RNG annually, which will be sold to local gas utilities. UGI’s wholly owned subsidiary, GHI Energy, is the exclusive marketer of environmental credits on these projects.

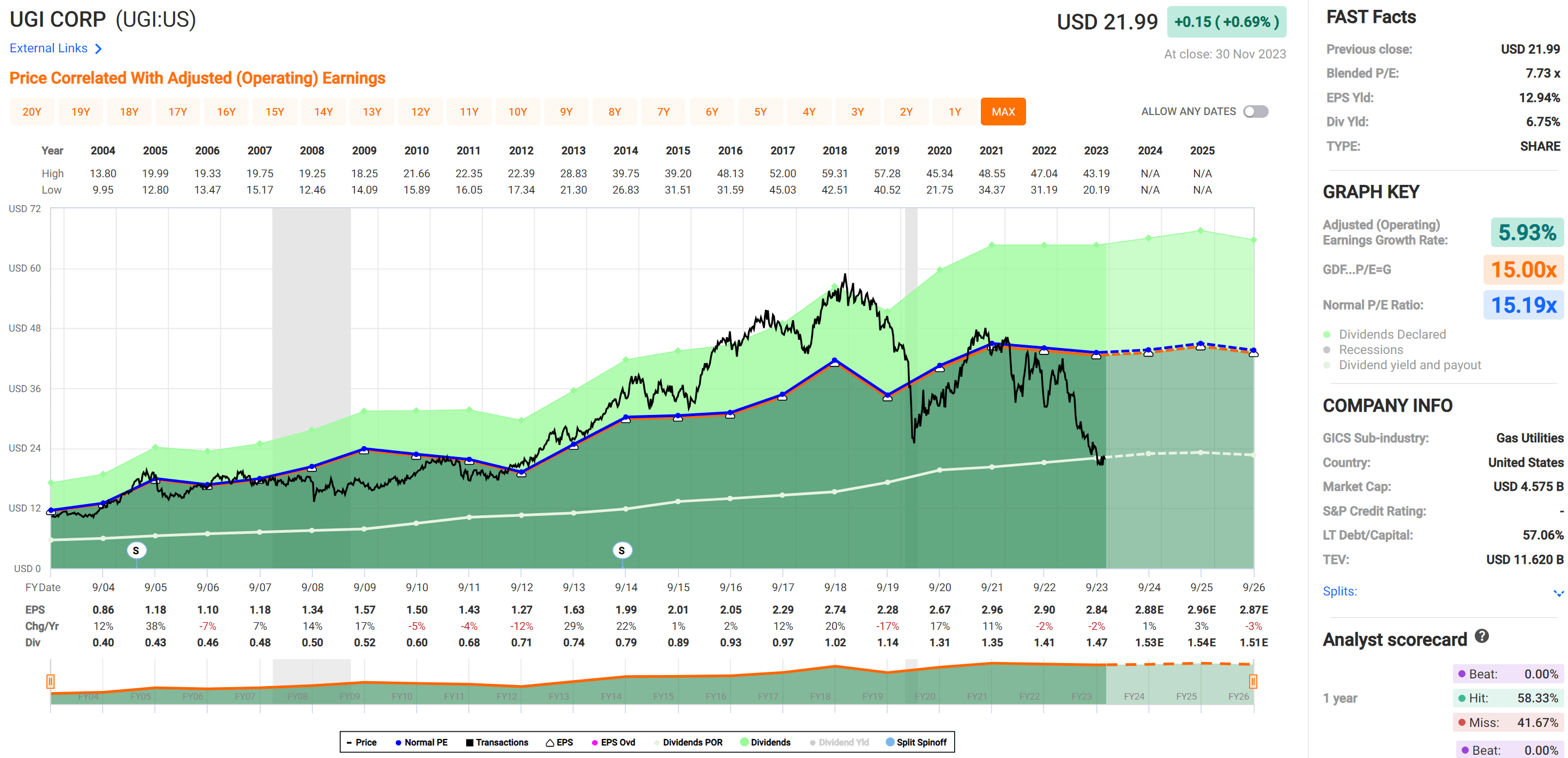

Importantly, investors are into UGI primarily for the dividend, and it’s worth noting that UGI is a dividend aristocrat with 36 consecutive years of increasing its dividend. Over the past 10 years, UGI has seen an EPS CAGR of 6% and a dividend CAGR of 7%. At the current price, UGI yields 6.7% and the dividend is well-covered by a 52% payout ratio.

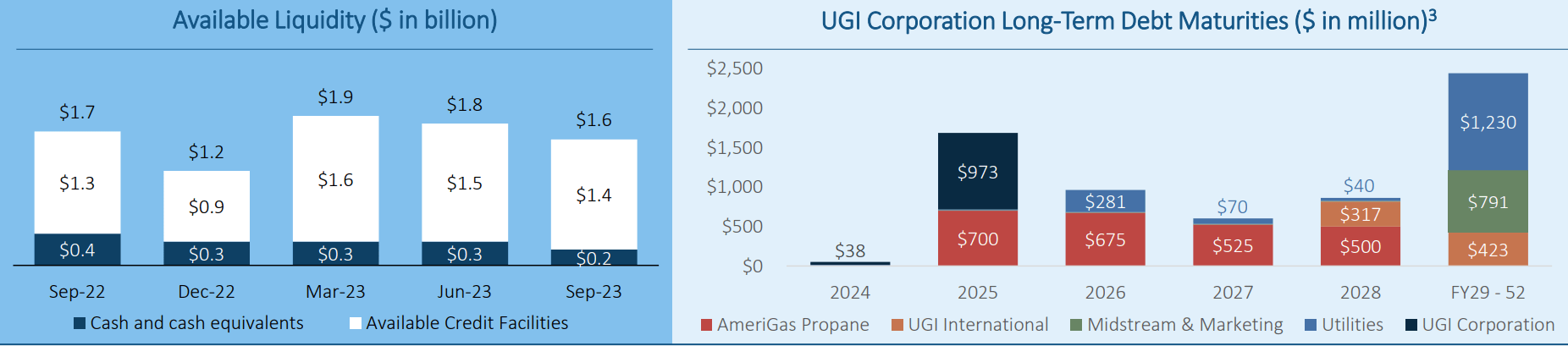

UGI also carries a sizable $1.6 billion in available liquidity and is in compliance with all of its debt covenant requirements. It also recently completed over $2.6 billion of long-term debt financing to support its operations and improve its liquidity. As shown below, UGI has limited debt maturities between now and the end of next year.

{kind=link}

Risks to UGI include the realization of a ‘higher for longer’ interest rate environment, which would increase borrowing costs for the company. While the market now expects interest rate cuts in 2024, there is no guarantee that the Fed would do that. Should interest rates remain high or higher in 2025, then UGI could feel the pressure from higher borrowing costs as it refinances debt. Other risks include the natural volatility of energy markets and weather patterns, which could impact UGI’s margins and customer energy usage.

Lastly, I continue to see solid value in UGI at the current price of $22.44 with a forward PE of just 7.8, sitting far below its normal PE of 15.2. At the current valuation, UGI is priced for a terminally no-growth or declining EPS, which I do not believe to be the case, especially considering UGI’s long track record of navigating all sorts of interest rate environments, all while providing durable energy services for its customers. Analysts expect 3.9% EPS for UGI next year and while it may take the market some time to fully appreciate UGI’s undervaluation, I don’t believe it would take much to move the needle for the stock price in a rationally-minded market.

{kind=link}

Investor Takeaway

UGI’s diversified energy portfolio, steady operating fundamentals and commitment to dividend payments make it an attractive long-term investment opportunity. While short-term headwinds may be causing some volatility in the stock price, UGI’s long track record of shareholder returns, ability to navigate difficult market conditions, and external growth prospects gives confidence for future growth potential.

Due to uncertainties around the direction of interest rates and the presence of other high yielding dividend alternatives on the market today, I'm downgrading my rating from a 'Strong Buy' to a 'Buy' rating. In the meantime, investors get to take advantage of the current bargain price with a well-covered 6.7% dividend yield.

For further details see:

7%-Yielding UGI Corp: Discounted Dividend Aristocrat