SFL - 8.8%-Yielding SFL Corporation Has More Dividend Hikes In Store

2023-12-07 11:00:00 ET

Summary

- Shares of SFL Corporation have experienced a significant rebound since my previous update, notably outperforming the overall market.

- The company's robust contracted revenue backlog of $3.4 billion provides predictable cash flows, shielding the company from each asset class' rate volatility.

- The stock's yield has dipped to 8.8% due to the rally, yet it remains highly attractive given SFL's prospects for sustained dividend growth.

In late June, I shared my thoughts on SFL Corporation ( SFL ), urging investors to grab its then-10.5% dividend yield before a potential rebound. I am pleased to say that this prediction played out nicely, with the Bermuda-based shipping giant recording a significant rebound.

Specifically, since my previous update, SFL has recorded a price gain of about 23.7%. Combined with its hefty dividend, SFL's total returns have climbed to an even more impressive 26.4%. That's not a bad return to achieve in five months. It's certainly a lot nicer than the S&P500's price return of 4.38% during the same period.

SFL Stock Returns Since Last Update (Seeking Alpha)

The stock is currently yielding 8.8%. The stock's rally, inherently diminished the yield. It's worth mentioning, however, that SFL's dividend raise from a quarterly rate of $0.24 to $0.25 has served as a slight counterbalance to the impact of the former.

Despite the strong upswing in the stock price over the past few months and the fact that its yield has dipped since my last update, I maintain a strong conviction that SFL represents an excellent investment opportunity.

In fact, I believe that SFL has further dividend hikes in store, meaning that its 8.8% yield retains its compelling appeal. As a result, SFL has now secured its position as my second-largest individual holding, excluding ETFs.

Robust Contracted Revenue Backlog Ensures Predictable Cash Flows

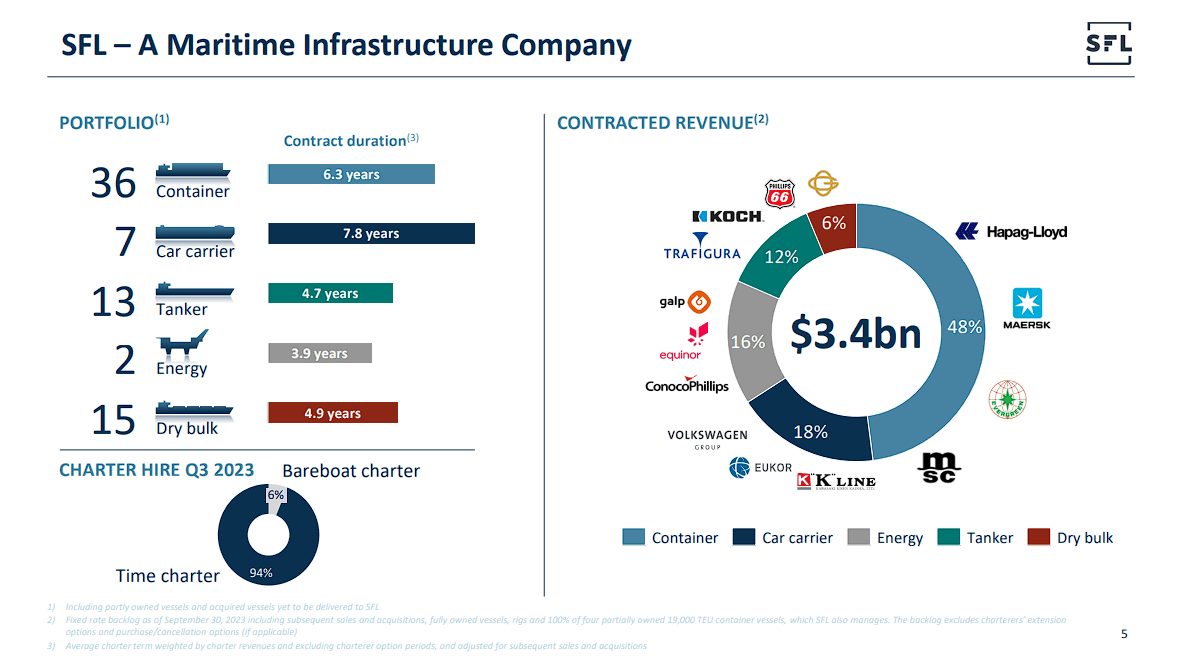

I feel quite confident in SFL's present dividend stability and future growth potential. This can be primarily attributed to its resilient contracted revenue backlog valued at $3.4 billion, boasting a weighted remaining charter term of 5.9 years.

This resilient backlog serves as a formidable defense, safeguarding the company against the volatile fluctuations in spot rates that typically impact each asset class throughout their distinct market cycles.

Simultaneously, the consistent renewals that often occur sustain the forward backlog high, ensuring that SFL remains insulated from any potential fluctuations in its cash flows over the medium term.

{kind=link}

SFL's Contracted Revenue Backlog (Q3 Investor Presentation)

If this weren't the case, SFL's exposure across five distinct asset classes would probably turn its quarterly revenues into the most tumultuous roller coaster in the market.

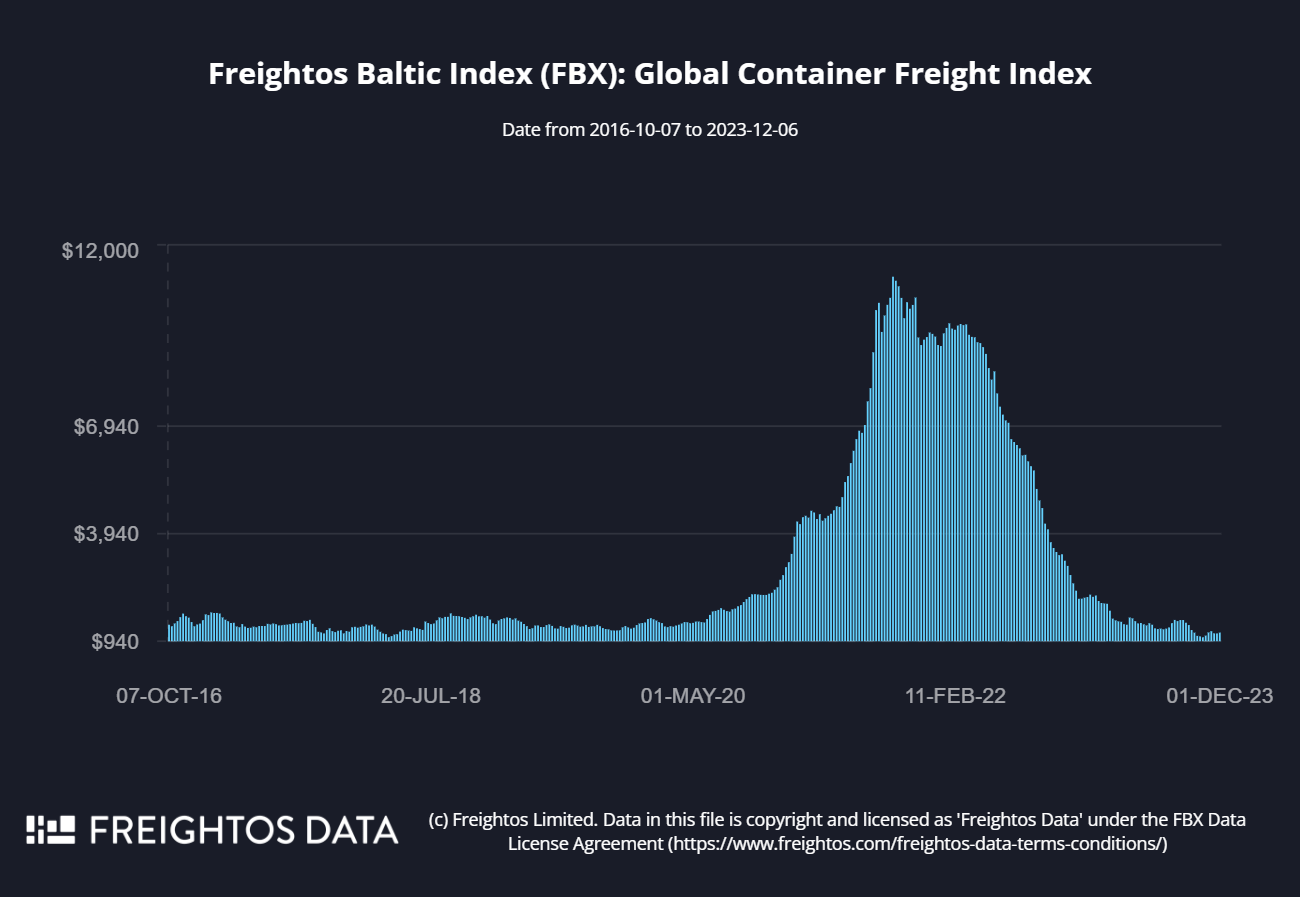

Take containership rates, for example, that skyrocketed during the pandemic only to slump lower and lower in recent months. By the way, you can read my latest updates on Danaos ( DAC ) and Global Ship Lease ( GSL ) here and here as I go through how the two containership lessors continue to reap the fruits from the multi-year charters they managed to sign during this parabolic period.

{kind=link}

Freightos Baltic Index (FBX) Global Container Freight Index (Freightos)

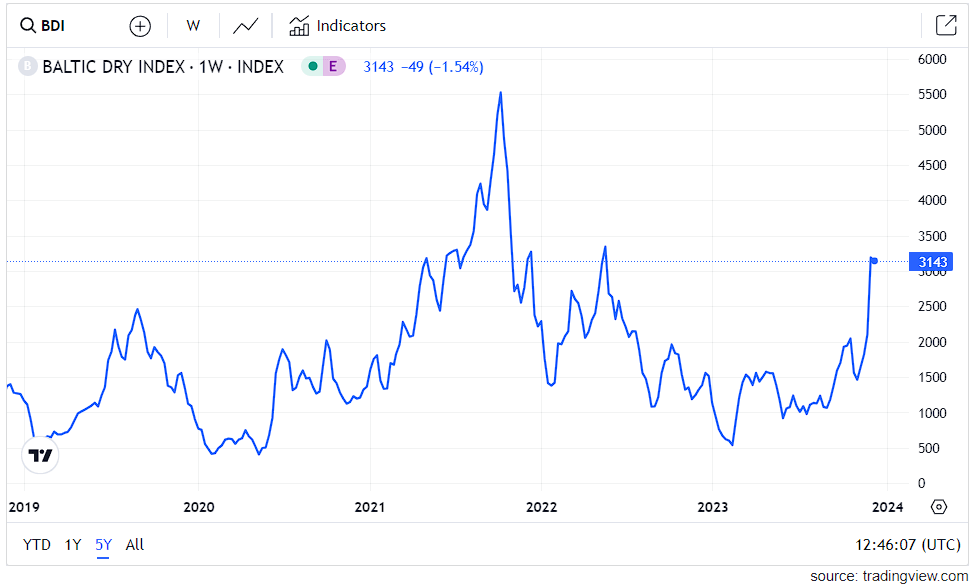

The dynamic landscape of the dry bulk asset class further underscores my point, as dry bulk rates have experienced significant and unpredictable fluctuations in recent years.

{kind=link}

Dry Bulk Index (Trading View)

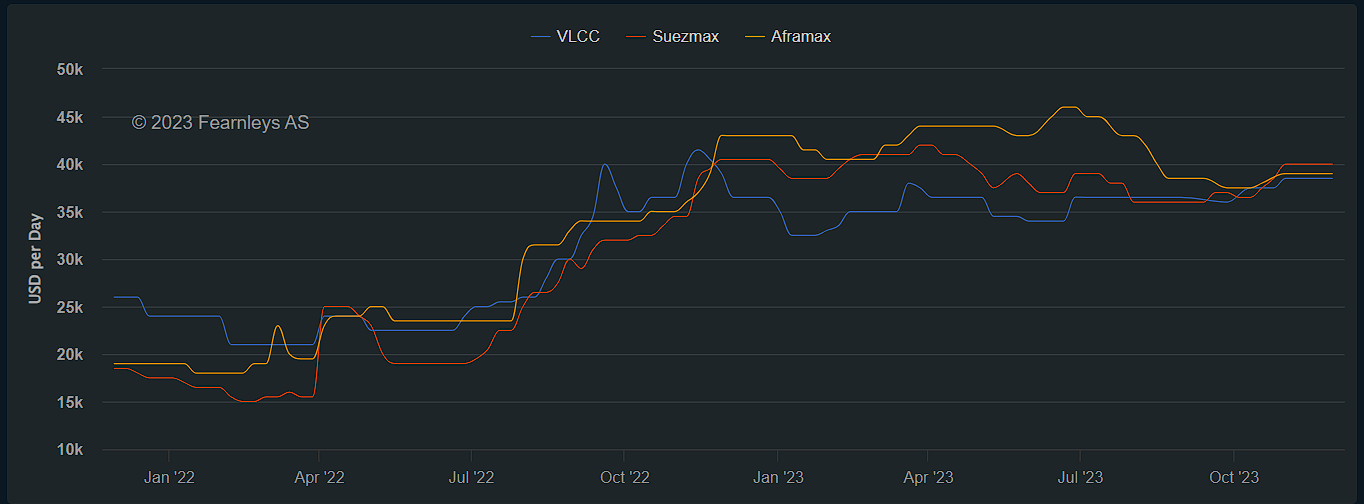

Certainly, this implies that the company may occasionally miss out on potential gains. Take, for example, the recent surge in tanker rates. Due to its fixed rates, SFL is unable to capitalize on these increased rates.

{kind=link}

1-year tanker rates (fearnpulse)

Yet, it is the foundational stability that SFL thrives upon, enabling its cash flows to consistently maintain a high level of stability and predictability across diverse asset class cycles.

Consequently, SFL's focus predominantly revolves around capital allocation. The essence lies in the skillful deployment of contracted cash flows by the management, channeling them towards expansion initiatives, optimizing the balance sheet, and delivering capital returns. This is what drives the stock's investment case. It's not so much about the short-term movement of rates in the shipping arena.

Capital Allocation Suggests Further Dividend Hikes Are Coming

Taking a look at SFL's capital allocation, I believe that the company is poised to continue improving its balance sheet while increasing capital returns. This includes the possibility of further dividend hikes ahead.

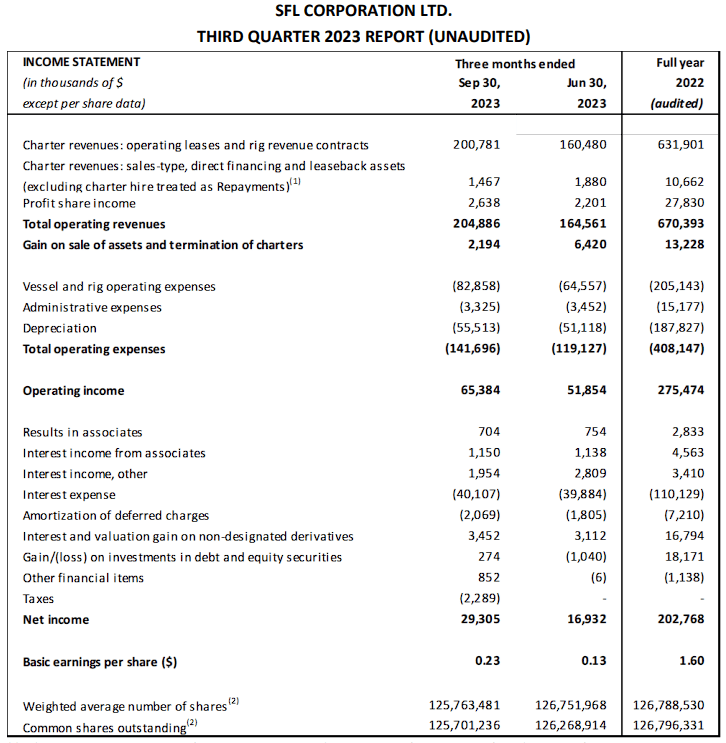

For starters, the company's quarterly operating income currently amounts to about $65.4 million.

{kind=link}

SFL Income Statement (SFL Q3 Report)

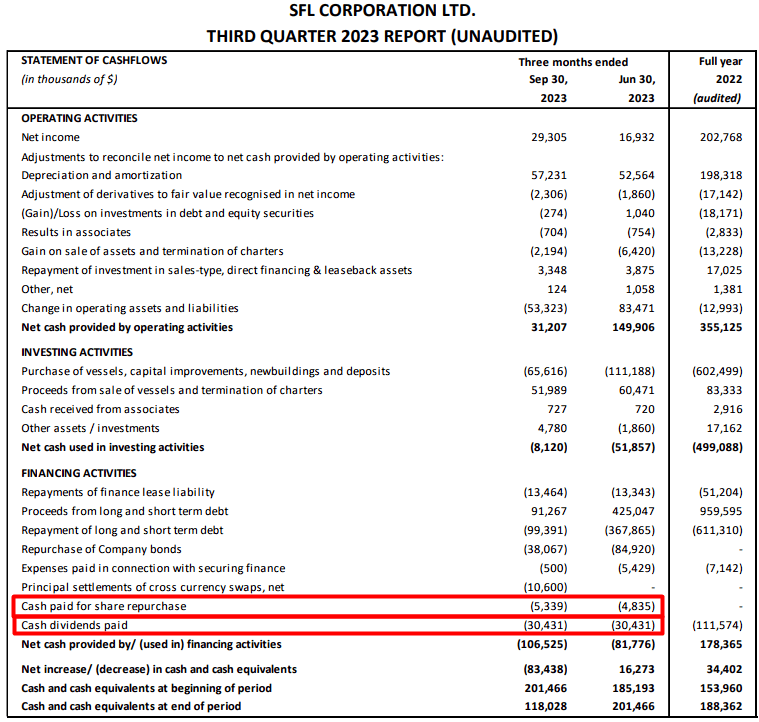

The company's operating income adequately covers the $30.4 million paid in dividends. With the company able to afford additional capital returns, SFL has started repurchasing stock in recent quarters, with about $4.8 million and $5.3 million repurchased in Q2 and Q3, respectively.

{kind=link}

SFL's Cash Flow Statement (SFL Q3 Report)

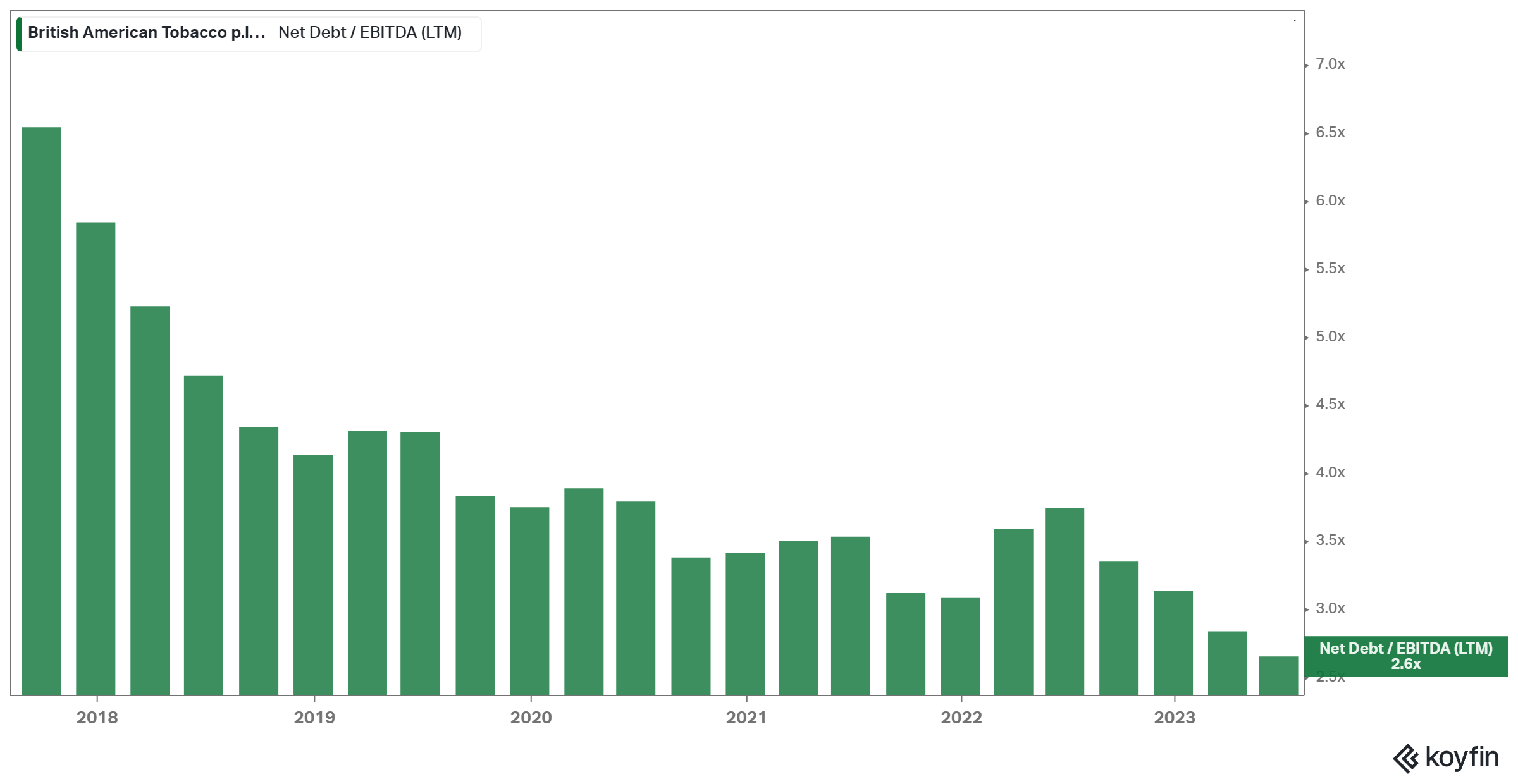

The company has been utilizing its excess cash to reduce its borrowings, which should, in turn, lower leverage and allow for higher profitability. Indeed, SFL's net debt to EBITDA has declined significantly in recent years.

{kind=link}

SFL's net debt / EBITDA (Koyfin)

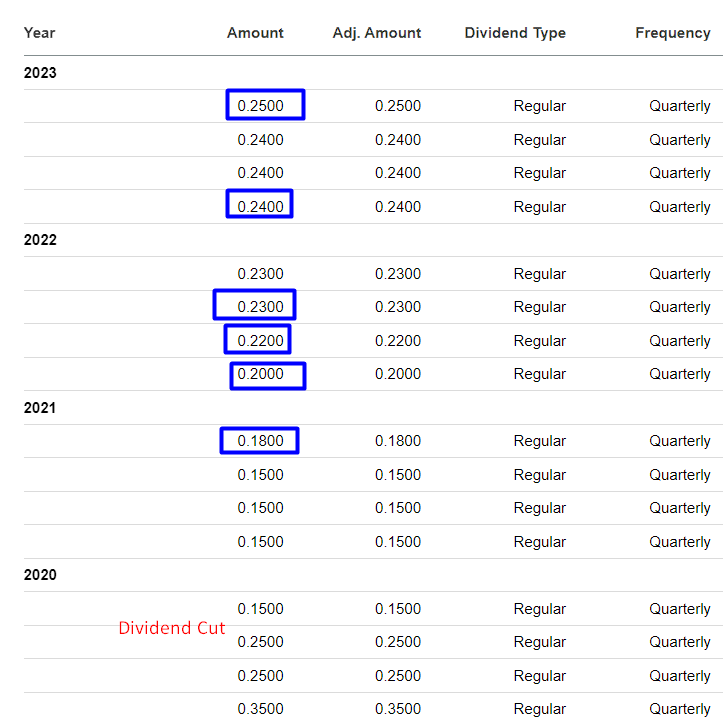

You can see SFL's improved profitability and growing capital returns capacity in the company's dividend history. SFL has increased its dividend six times since the 2020 cut.

{kind=link}

SFL's dividend history (Seeking Alpha)

I believe that SFL's rigs, in particular, will continue benefiting the top and bottom line significantly moving forward. This should be another favorable catalyst for the company's dividend growth prospects.

Specifically, SFL owns two harsh environment drilling rigs: the jack-up rig Linus and the semisubmersible rig Hercules. In Q3, the rigs generated about $64 million in contract revenues compared to roughly $19 million in Q2 due to the drilling landscape experiencing a revival lately.

In the short term, and by that I mean Q4, SFL's management expects lower revenues for Hercules due to a long mobilization period from Canada to Namibia, where the rig is due to work for a contract with Gulf Energy.

However, according to Ole Hjertaker, SFL's CEO, in 2024, Hercules will be operating in Canada at the highest drilling rate "in this cycle today". With the costs for bringing this drilling unit online behind us and demand for rigs on the rise, it makes total sense to expect a notable rise in SFL's revenues and profits outside of its core vessel fleet.

Takeaway

Overall, SFL stock's performance since my last update has exceeded my expectations, outperforming the overall market by a wide margin. While shares are currently offering a reduced yield due to the strong share price gains, I believe that SFL's investment case remains highly attractive.

During the dynamic shifts in each asset class's rate fluctuations, SFL's contracted revenues stand as a bulwark, ensuring robust cash flows. Coupled with strategically positioned rigs poised to capitalize on favorable energy market dynamics, SFL's dividend appears poised for a sustained upward trajectory.

Therefore, despite recent gains propelling SFL to the second-largest position in my portfolio, I am planning on selling a single share for the time being.

For further details see:

8.8%-Yielding SFL Corporation Has More Dividend Hikes In Store